A lot of investors believe putting money into an ETF or mutual fund holding Treasury Inflation-Protected Securities is a very safe ‘core’ investment. After all, these are investments in U.S. Treasurys, so there is no credit risk.

But there is interest-rate risk and diversification risk, and price swings for these mutual funds and ETFs and be quite dramatic.

When the price goes up, all looks good. But when TIPS prices decline sharply, as they did in 2013, investors can be stunned.

So, what are the risks?

I analyzed data for five widely traded ETFs, two of which hold only Treasury Inflation-Protected Securities:

- iShares TIPS Bond (TIP)

- iShares Core US Aggregate Bond (AGG)

- Vanguard Total Bond Market ETF (BND)

- Vanguard Short-Term Inflation-Protected Securities ETF (VTIP)

- Vanguard Short-Term Bond ETF (BSV)

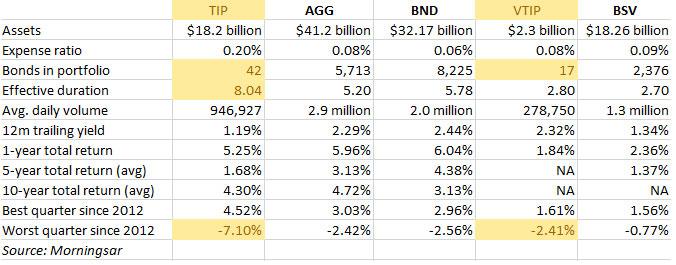

1. TIPS funds are not diversified. There are only 40 Treasury Inflation-Protected Securities currently trading on the secondary market, and each time a new one is created at auction, another one matures. The big TIP ETF – with $18.2 billion in assets – has only 42 items in its portfolio (the extra two are short-term Treasury investments). Vanguard’s short-term TIPS ETF has only 17 bonds in its portfolio. If you look at the TIPS maturity chart, those 17 TIPS take you out to July 2022.

An investment that holds only one ‘peculiar’ kind of Treasury issue cannot be considered diversified. It also shouldn’t be considered a ‘core’ holding.

Compare this to the bond holdings in AGG (5,713) and BND (8,225). Although some of these are not Treasurys, the risk is spread across a much larger universe of holdings.

Even Vanguard’s short-term bond fund, BSV, holds 2,376 issues, compared to 17 in VTIP.

2. The TIP ETF is riskier because its duration is higher. Holding all the current TIPS on the market results in an effective duration of 8.04 years, meaning this ETF would lose 8% of its value if the typical TIPS yield rose by 1%. Compare that with the duration of AGG (5.20) and BND (5.78). These funds will tend to be much less volatile, for good or bad, depending on where the market is heading.

Here is a comparison of how these three funds have performed over the last two years, with the TIP ETF shown in blue:

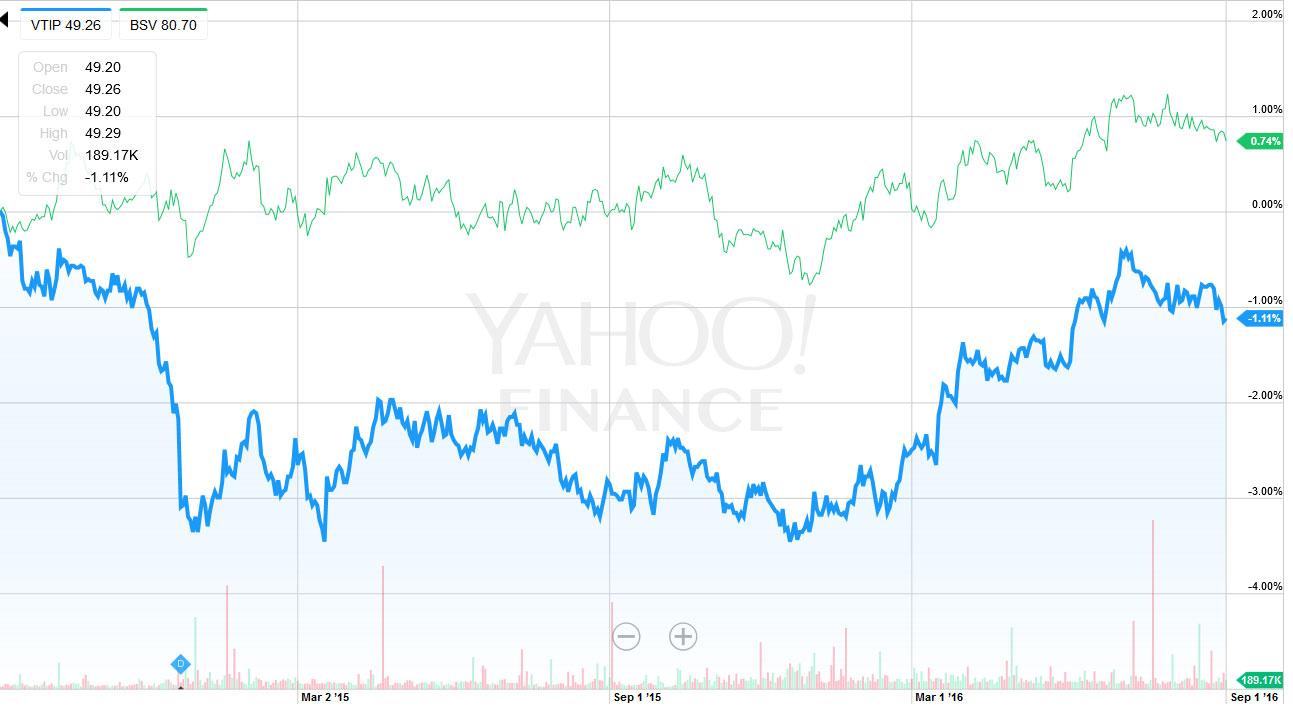

Also, even though the duration of VTIP is nearly identical to Vanguard’s BSV short-term bond fund (2.8 versus 2.7), its has been a lot more volatile over the last two years, because the yield on short-term TIPS has risen faster than the overall bond market. Here is that comparison, with VTIP shown in blue:

3. The TIP ETF can be surprisingly volatile. In the second quarter of 2013, the TIP ETF lost 7.1% of its value. That is a shocking figure for a theoretically ‘rock solid safe’ investment. In that same quarter, AGG lost 2.4% and BND lost 2.5%, more in line with how you would expect a ‘core fund’ to perform.

The short-term TIP fund, VTIP, lost 2.4% of its value that quarter, despite its much lower duration compared with AGG. Compare that to -0.77% for Vanguard’s BSV, the short-term total bond market ETF.

4. The TIP ETFs have much lower daily volume. The big iShare TIP fund has a daily volume of about 946,000, about a third of the volume of the AGG fund. VTIP is even lower at about 278,000 daily shares. Although I don’t think this creates a lot of risk, light trading can magnify price swings in times of financial crisis.

What’s the alternative to TIPS ETFs and mutual funds?

I am an advocate of devoting a portion – maybe 15% to 20% – of your portfolio to super-safe investments like Treasurys, I Bonds and bank CDs. Inflation-protected investments should be a big part of this. My preference, though, is to buy TIPS at auction – when the yield looks favorable – and hold them to maturity. This strategy creates zero trading costs or ongoing expenses. And there is no risk in holding a TIPS to maturity, except that when it matures you might not like the current state of the market (ummm … my problem today).

I also recommend buying I Bonds every year up to the Treasury’s cap ($10,000 per person per year) and holding them until 1) you need the cash, or 2) a higher fixed rate makes rolling them over to new I Bonds desirable.

I consider Total Bond Market funds to be fairly low-risk, but not part of my super-safe allocation. But I do use these funds in my retirement accounts as fixed-income investments. Even if interest rates begin rising, the higher return will help balance off the lower NAV value.

VERY good points. After I had extolled the value of TIPS a friend invested in Vanguard’s TIPS fund (which I never suggested). When he sustained an 8% loss over a couple months he was shocked at how volatile this “safe” investment could be. There are only a few investment writers who stress the difference between bond funds and bonds but everyone should read them. Larry Swedroe comes to mind. Len