Updated June 12, 2026

The U.S. Treasury instituted a new TIPS auction schedule in 2019, eliminating one 30-year reopening and adding a new 5-year originating auction. More details.

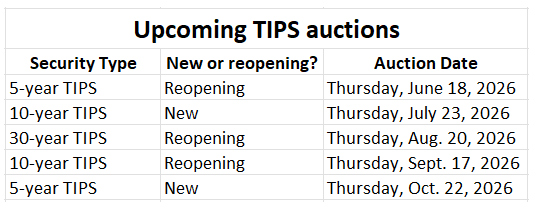

Here is Treasury’s schedule of auctions:

- January. New 10-year TIPS.

- February. New 30-year TIPS.

- March. Reopening of January 10-year.

- April. New 5-year TIPS.

- May. Reopening of January 10-year.

- June. Reopening of April 5-year.

- July. New 10-year TIPS.

- August. Reopening of February’s 30-year.

- September. Reopening of July 10-year.

- October. New 5-year TIPS.

- November. Reopening of July 10-year.

- December. Reopening of October 5-year.

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

– Tipswatch.com

From this morning’s press release of Treasury’s Quarterly Refunding Statement:

TIPS FINANCING

Given the intermediate- to long-term borrowing outlook and the structural balance of supply and demand for TIPS, Treasury believes it would be prudent to continue with incremental increases to TIPS auction sizes in order to maintain a stable share of TIPS as a percentage of total marketable debt outstanding. Over the February to April 2025 quarter, Treasury plans to maintain the February 30-year TIPS new issue auction size at $9 billion, increase the March 10-year TIPS reopening auction size by $1 billion to $18 billion, and increase the April 5-year TIPS new issue auction size to $25 billion.

This has been the trend for several years, with the 5- and 10-year auctions getting larger and the 30-year holding. I still think eliminating the 30-year reopening and replacing it with a new 20-year would be the way to go.

David, yes I noticed that. For me this particular announcement was an early stage peek behind the curtain regarding what Treasury anticipates the landscape of the total marketable debt outstanding will look like in the short term of the new administration – incremental increase across the board (“to maintain a stable share of TIPS as a percentage“.) Of course, there was also a press release today announcing the intended nominee for the new Assistant Secretary for Financial Markets. So the marketable debt landscape could change drastically one way or another from what the other press release seems to imply. Time will tell.

I know I’m being impatient since I’d guess you are working on an article about the upcoming 10 year TIPS auction, and I know this topic has been covered before, but …

There must be some good reason to buy on Vanguard (or similar brokerage) at the auction, if you are buying a substantial amount. I just can’t figure out what that reason is.

I’m guessing that the auction is primarily for very large traders to secure the amounts they need, and as a result, this creates a secondary market for smaller investors.

Words of wisdom, please.

The only way to buy this 2035-maturing TIPS (for a short while at least) is through the Thursday auction. It settles on Jan. 31. You could probably find some on the secondary market before then, but sellers may be focused on big-lot purchases. The advantage of the auction is that you get the same high yield as the big-money investors, without any big-ask spread. Also, if you want, you can make a very small purchase at the auction, as low as $1,000 on the brokerages, without commissions. If you skip the auction and wait a month, you could possibly find a better real yield. That happened last year and I bought more later in the year. But I am not going to worry about 10 to 20 basis points. My main focus is to fill the 2035 year on my TIPS ladder, and this auction will be my first chance, ever, to fill that year.

would you over purchase Jan 10 2025 yr TIPS, to use for 2036 since as of now there aren’t any 2036TIPS.

Yes, but I have lined up nominal Treasurys for that purpose.

Why nominal instead of TIPS?

I like nominal yields for one- or two-year terms. Easier and very certain.

I find this confusing: “over-purchase Jan 10 2025 yr TIPS, to use for 2036”

Did you mean “over-purchase Jan 2025 [issued] 10-year TIPS [maturing Jan 2035] to use for 2036”?

If so, that’s similar duration and probably close enough, though you didn’t ask me. It’s common to weight the duration between the last available prior to the gap (which is about to be 2035) and 2040 for all gap years. If you only need 2036, you’d put 80% into 2035 and 20% into 2040. If it’s not a lot of money, just buy the 2035s.

If your ladder needs constant income across the whole gap, the math gets easier this year with the gap dropping to 4 years: just split the gap years 50/50 into 2035s and 2040s.

One note, with the recent increase in yields: if the coupon on the new 10-yrs is 2.25%, I prefer the 2034s with lower coupons, less to reinvest. Far out on the curve, I prefer 2052s to 2053s and 2054s because I don’t need to income today and like the huge discount due to the low coupon. I feel like I’m stretching my LMP dollars.

I suspect the commenter was talking about a one-year investment to provide cash to buy the 2036 TIPS next January. I use nominal T-bills and CDs in this way to set up the January purchases for the gap years.

Any estimate of coupon for January 2025 TIPS auction?

It’s early to give a prediction. Right now you are looking at a real yield of 2.29% and that would create a coupon rate of 2.25%. Things will probably change a bit in the next two weeks.

My dilemma is putting it all in this one for the year, or half in January and half in July. Rates are very tempting.

I am going to focus on the January issue because I like January maturities for options for future RMDs. (They start next year for me.)

I am wondering if there is any reason why a retail investor would participate in a reopening auction as opposed to buying the same bond from the secondary market?

One reason could be if the investor is making a very small purchase. TreasuryDirect allows auction purchases of just $100 and brokerages generally allow a minimum of $1,000 at an auction. Even with the small purchase, the small investor gets the same high yield as the million-dollar auction investor. The other reason is that buying at auction is a lot simpler than buying on the secondary market.

Thank you. That makes sense.

Thank you for your post.

Do you post, or have you considered posting, to Substack. As a reader it’s much more convenient to use an aggregation site like Substack. Thank you

No, I don’t post to Substack, sorry.

Hi, I determined that $45K will be required in 10 years to support my lifestyle.

Do I buy 45 or 38 TIPS of new 10-year TIPS on auction on Thursday, CUSIP 91282CJY8?

Thank you in advance

Good question. I would suggest $45k because the coupon payment is going to be paid out along the way and if you did less you would need to reinvest and set aside those payments for January 2034. (That could work in a tax-deferred account.) If you do $45,000 you get that amount back, adjusted for inflation, in 2034. Other readers may have ideas on this ….

Thank you

What is a reasonable vehicle to reinvest coupon payments in tax deferred? I am thinking of VTIP or newly introduced IBIJ

Great question. The only traditional TIPS fund I would own (don’t have any now) is VTIP, which has a low duration and does a better job of simply tracking inflation. The IBIJ 2023 defined maturity ETF is an interesting possibility for your purposes, as long as you can invest what might be small amounts without any commissions. I am pretty sure iShares will issue a 2034 version later this year, too.

I have been reading your comments and I purchased the recent 5 year (June) and 10 year (July) Tips because of the positive real yields. Please compare the attractiveness of the August 2023 30 years TIPS purchase at Treasurydirect versus the 30 year treasury bond versus the I-bond.

I will be posting a preview of the 30-year TIPS auction on Sunday, Aug. 13. The term is too long to be a good investment for me. But the current real yield of 1.87% is double the I Bond’s 0.9%. The I Bond has advantages of never being marked-to-market (so you will never lose any money) and a flexible maturity date. The nominal 30-year bond is yielding 4.21%, which sets up an inflation breakeven rate of 2.34%, probably about right.

David, thanks for an excellent, helpful site. My question: Reading your comments above gives me the impression that you prefer to buy TIPS at auction rather than in the secondary market. Are there reasons for that other than avoiding the spread in the secondary market between buy and sell prices (which I guess figures to cost me half the difference between them)?

I write about each auction, so I prefer to invest there. But as real yields have increased, I’ve been filling in longer-term spots on my TIPS ladder through the secondary market. The only negatives are sometimes-high investment limits and the slightly lower yields for small purchases.

Thanks, David. I hadn’t realized that I’d pay a somewhat higher price on small purchases in the secondary market (though I’d suspected it). Good to know. Alan

Do you have any concern that QT, which only started in earnest in September, will lead to serious demand issues in the Treasury market?

We saw the massive dislocation caused by aggressive QE, driving the 10 year yield down to 0.5%

Is there reason to be concerned that withdrawing $95 billion a month, or $1.14 TRILLION a year, from Treasuries and MBS might cause a similar dislocation in the opposite direction, perhaps a less appreciated factor than what happens to Fed Funds over the course of the year?

This time, Japan, China and other foreign buyers may be sellers as well instead of buyers, particularly if the notion takes hold that the 40 year bull market is Treasuries is over.

Yes, definitely a concern and I believe the Fed has to accomplish at least $2 trillion in Treasury roll-offs. Quantitative easing caused a boom in many assets: stock and bonds, for sure, but also housing, crypto, meme stocks, etc. A lot of that is starting to unwind. So far, the Fed’s Treasury balance sheet has fallen from about $5.7 trillion in April 2022 to about $5.4 trillion in January 2023. That’s it. Not impressive so far.

Any thoughts about buying the January 19th 10yr TIPS auction vs waiting for the April 20th 5 year? Split funds between the two?

Too early to guess the coupon on the 10 year?

I’m wondering whether the $95 billion/month Treasury runoff is just beginning to bite and affect demand, whether that might have more of an impact than the course of Fed Funds over the next year

I need to add the 2023 year to my TIPS ladder, so I will be highly likely to buy at the Jan. 19 auction. And if yields hold up, I am also likely to buy at April’s 5-year auction. It’s very hard to predict where real yields will be heading. This market has been highly volatile.

Hi David,

Vanguard has the Jan 19, 2023 10 year tips listed as “reopen”. I guess that will be clarified whenever it is officially announced on the treasury site. So far, I don’t see that auction in the treasury site’s “upcoming auction” list.

It won’t actually be “announced” until Jan. 12, but here is the Treasury’s auction schedule, showing a new issue on Jan. 19. https://home.treasury.gov/system/files/221/Tentative-Auction-Schedule.pdf

So Vanguard is doing the funky label. 🙂 They will likely fix it by at least Jan 12.

Pingback: I Bonds: A not-so-simple buying guide for 2023 | Treasury Inflation-Protected Securities

Hi David. What do you think about the 5-year TIPS on 10-20-2022? Thank you

I’ll be posting a preview story on Sunday morning. If things stay as they are right now, this auction will be highly attractive, in my opinion.

Will you also mention the reopening of the 10 year TIPs in November in your story? That’s already available for purchase for around $96.41 per $100 for the 9 years 8 months remaining.

I was a buyer of that TIPS at the originating auction In July (real yield 0.630%) and again in September (1.248%). I won’t be mentioning it in this article previewing the 5-year auction, but it is likely to be attractive. It’s currently trading at 1.60%. The next four auctions — new 5-year, 10-year reopening, 5-year reopening and new 10-year are all likely to be attractive.

A news story yesterday said the president talked about negative interest rates with the head of the Fed. How do possible negative interest rates (whatever that actually means to the little guys) fit into making a decision to buy TIPS?

Negative nominal interest rates would be a disaster for future bond investors. If the 10-year nominal Treasury yield went negative, it would mean the 10-year TIPS real yield would be somewhere in the range of -1.50% to -1.75%. That would be about 100 basis points lower than the record low for a 10-year TIPS. All of this would mean soaring bond prices for bonds you already own, but future bond-buying would be extremely unattractive.

Greetings: Excellent site. Can you direct me to resources that may help identify current and historical market “real” yields (versus nominal) for 5 and ten year TIPS. My objective is to assess relative real yields over time. Thanks.

Frank, you can get this at the Treasury’s Real Yields Curve site, for both nominal and real yields: https://www.treasury.gov/resource-center/data-chart-center/interest-rates/Pages/TextView.aspx?data=realyield

what do you think of the FRN?

I looked at it in the past and didn’t like it as an investment for a small investor. Might deserve another look if short-term rates rise … https://tipswatch.com/2013/11/06/the-new-treasury-floating-rate-notes-why-they-look-like-a-bad-deal/

the FRN auction tomorrow is a reissue, does that have any significance?

I don’t understand the significance of the TIP ETF. Is that just the current price, and why do I care if I am holding the actual bonds? I also prefer to buy when inflation sentiment is out of favor, and buy at a discount. The government pays you to buy their paper, that seems like a good thing for the investor.

Ambrose, I don’t invest in the TIP ETF or any TIPS mutual funds, but the price of that ETF is a good indication of current sentiment. It is up more than 5% since February, which indicates that both Treasurys and inflation protection are in high demand. The 10-year TIPS is now yielding 0.12%, down about 60 basis points since the January auction.

have you a POV on the 10 yr now open?

I’ll be posting later today on that new 10-year TIPS.

Pingback: The 10-year TIPS quandry: What should the Treasury do in January 2015? | Treasury Inflation-Protected Securities

Ed, I would have thought that too, especially in 2011 when the S&P actually downgraded the US debt at the apex of a similar crisis. Instead the exact opposite happened, as I detailed in this posting: https://tipswatch.com/2013/04/25/the-tips-earthquake-when-did-it-happen-and-why/

What actually happened was a severe decline in the stock market and a flight to safety, with Treasurys and especially TIPS benefiting. Back in 2011, the fear was a government with spending out of control. That has lessened a bit now, since government spending isn’t the key issue. But it is still an issue, and inflation is still a threat.

Dave, I was thinking that if the USA looks uncertain to repay its debts, higher yields for USA to borrow will result. You seem to be reckoning oppositely … I don’t follow.

Ed

Ed, not seeing any upward trend yet in yields. Seems inevitable, but busting the debt limit is very negative for the stock market and very positive for Treasurys, as odd as that sounds. So the trend right now is for lower yields.

Beware the “Ides of October”

Dave,

From Goldman-Sachs just now:

After October 17, the Treasury can keep conducting auctions to roll over maturing securities, but it cannot increase outstanding debt. If the debt limit is not raised before the Treasury depletes its cash balance, Goldman fears it could force the Treasury to rapidly …

The upcoming 30 yr TIPS auction might have an elevated yield due to concerns …

Will bear extra watching, maybe …

Best,

Ed

JJ, the Treasury does a TIPS auction each month, and sometimes it is a new issue. That means the base interest rate (coupon rate) and yield to maturity will be set at auction. So for a new issue, you won’t know coupon rate for sure, and the yield you get will be close to the coupon rate. The price you pay for the TIPS will be close to par value, as long as the yield is positive.

When a TIPS is reissued, it carries the coupon rate from the original auction. A few months will have passed, so the yield could have moved strongly up or down from the coupon rate, meaning the price you pay for the TIPS could be less or more than par value.

Once a TIPS is issued, it trades on the secondary market, so it is easier to estimate its likely value at auction. With a new issue, the price can be a little harder to estimate.

Take a look at this post for a recap of all the new and reissues of 2012 and you can see the pattern: https://tipswatch.com/2012/12/30/recapping-2012-the-year-in-tips/

Could you explain, or direct me to where on the site an explanation already exists for, the difference between new and reissued TIPS as listed above? Thanks.