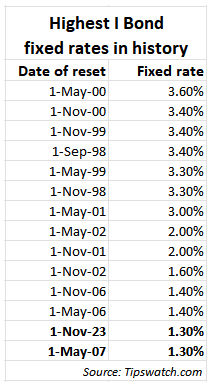

A new fixed rate of 1.30% looks like a real possibility.

By David Enna, Tipswatch.com

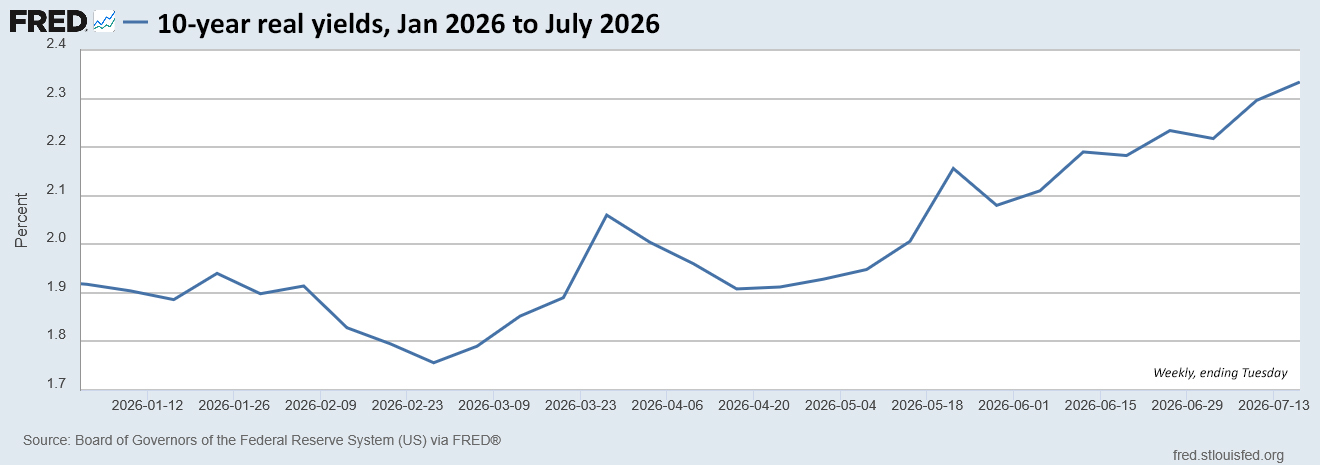

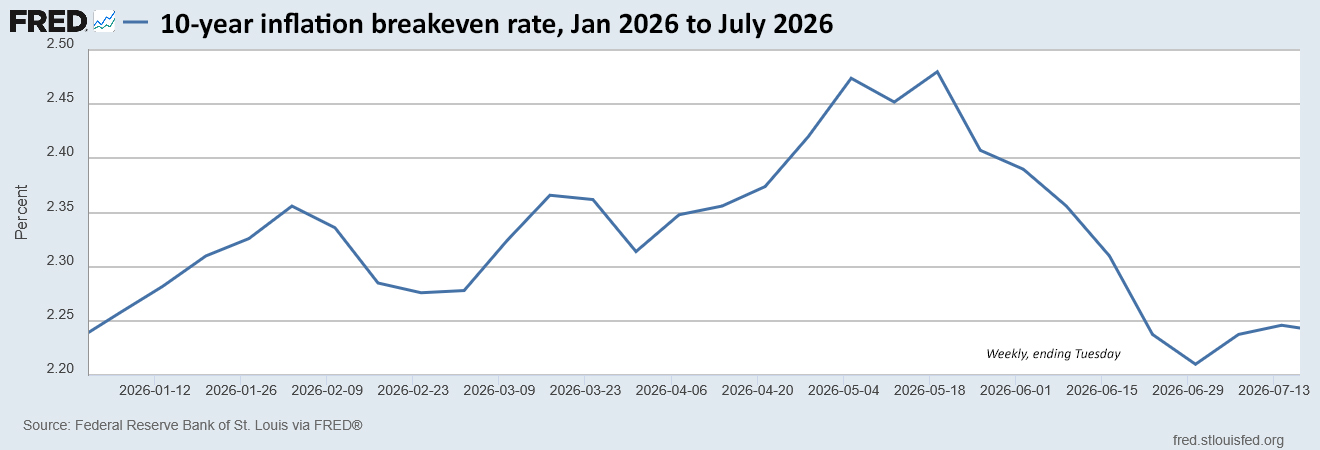

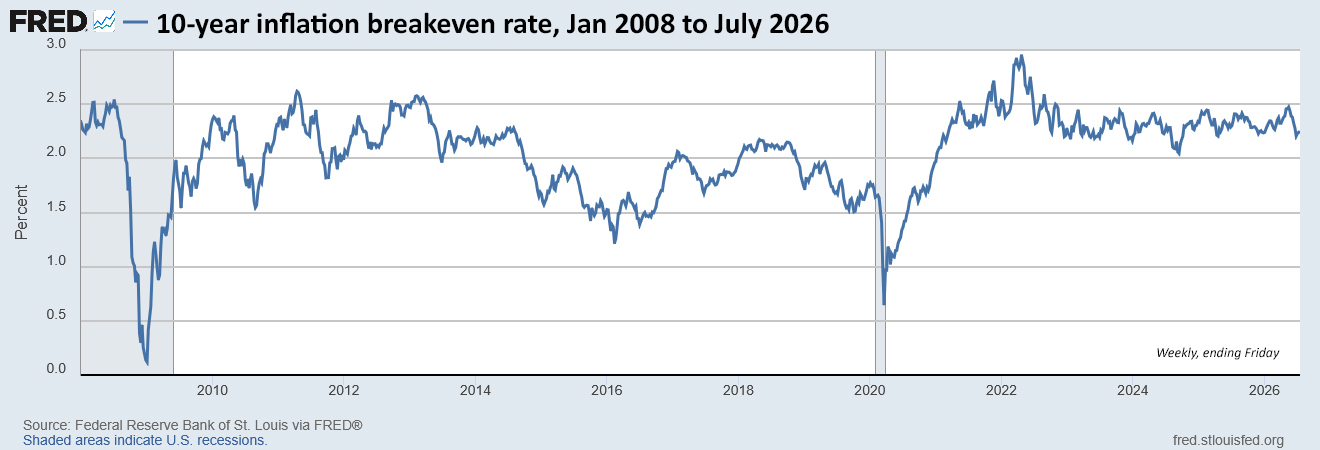

We’ve seen a fascinating explosion in real yields in 2026 as the war with Iran, inflationary pressures and soaring federal deficits are straining the U.S. Treasury market.

This move higher is significant for investors in Series I Savings Bonds, a Treasury investment with returns pegged to U.S. inflation through a combination of fixed and variable rates:

- The I Bond’s fixed rate will never change. Purchases through October 2026 have a fixed rate of 0.90%, which means the return will exceed official U.S. inflation by 0.9% until the I Bond is redeemed or matures in 30 years. A new fixed rate will be set Nov. 1, 2026.

- The inflation-adjusted rate (often called the I Bond’s variable rate) changes each six months to reflect the running rate of inflation. That rate is currently 3.34%, annualized, for six months. It will also adjust on Nov. 1, 2026, rolling into effect for all I Bonds, no matter when they were purchased.

- The I Bond’s current composite rate is 4.26%, annualized, for a full six months for any bond purchased from May to October 2026.

For I Bond investors, the fixed rate is the most important factor, especially for investments likely to be held for many years. Once purchased, an I Bond holds that fixed rate forever, while the variable rate will change every six months.

The fixed rate math

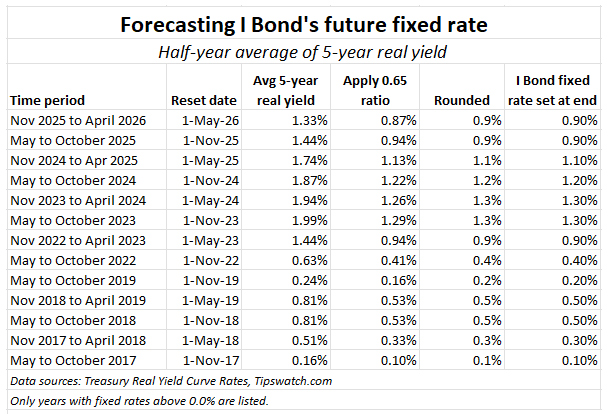

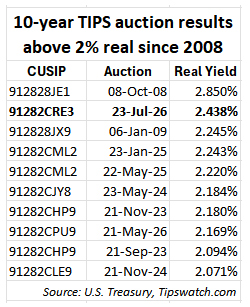

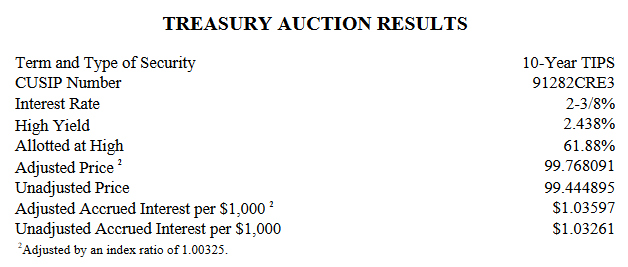

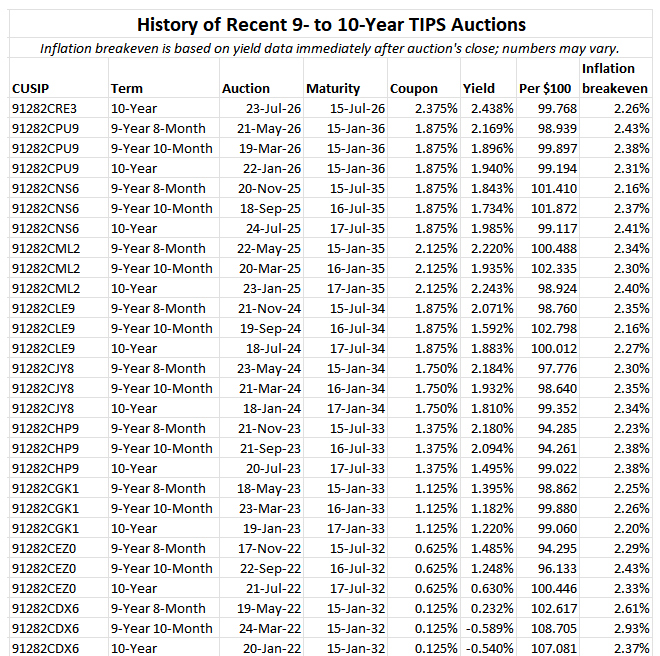

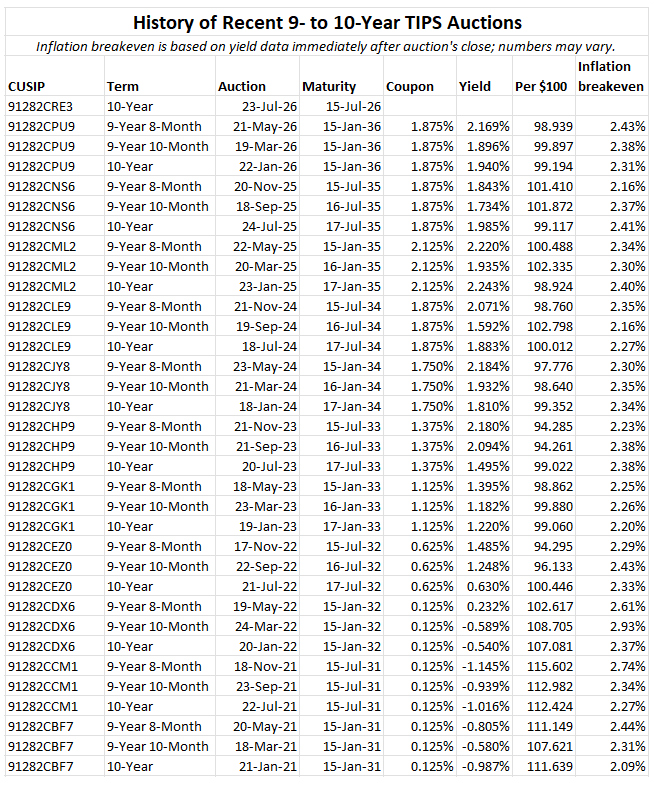

How is the fixed rate set? There is no announced formula and in theory this decision can be made at the discretion of the Treasury Secretary. However, over the last decade the fixed rate could be accurately forecast using this formula: Apply a ratio of 0.65 to the six-month average real yield of the 5-year TIPS. Here are results of that ratio since 2017:

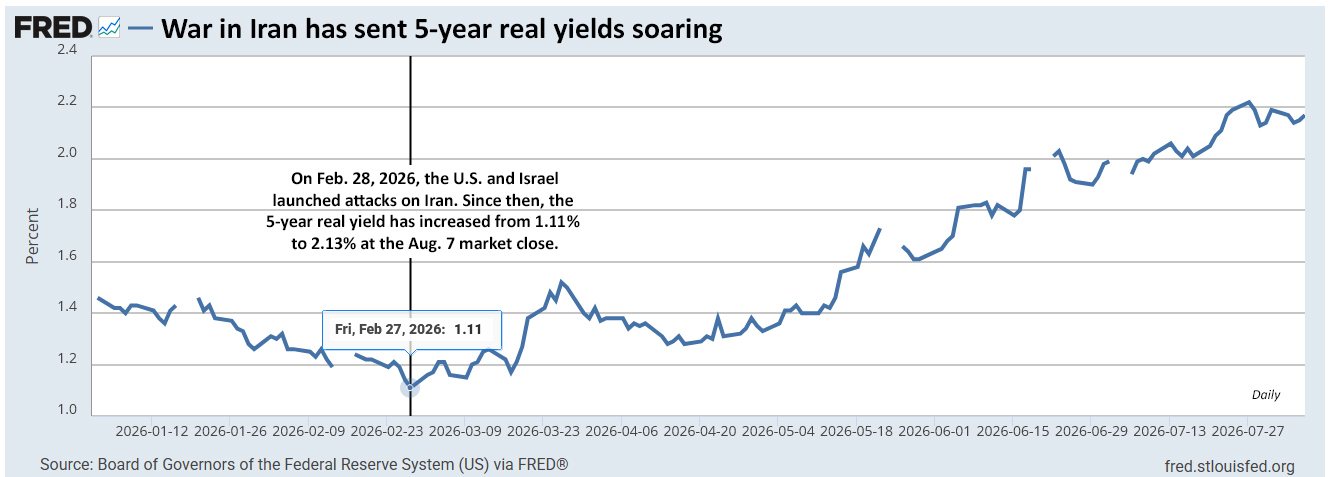

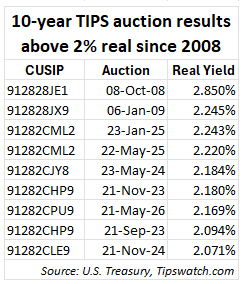

On Jan. 1, 2026, the 5-year TIPS was yielding 1.46%, but that rate began steadily heading lower, right up to the day before the Iran war began on Feb. 28, 2026, when it closed at 1.11%. Since the launch of war, the 5-year real yield has increased 102 basis points, to 2.13%.

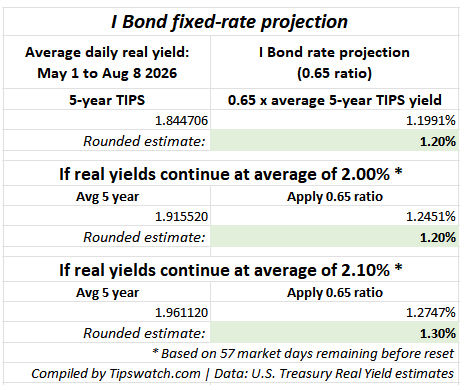

So the rate picture has dramatically changed since the I Bond’s May 1 reset. Because of these elevated 5-year real yields, the fixed rate is almost certainly going to increase above the current 0.90%. Let’s look at a projection, based on 5-year real yields from May 1 to Aug. 8, 2026:

We are just a bit more than halfway through the six-month period from May 1 to Oct. 31. So far, the average 5-year real yield has increased to about 1.84%, which would translate to a new fixed rate of 1.20%. And that projection looks solid if rates continue at elevated levels.

Just a reminder: The Treasury sets the I Bond’s fixed rate to the tenth decimal point, which means that any six-month ratio result of 1.151% or higher will be rounded up to 1.20%, and any ratio result of 1.251% or higher will be rounded to 1.30%. At this point, the current 0.65-ratio of 1.1991% is solidly above the 1.20% trigger.

The current 5-year real yield is 2.13%, as of Friday’s market close.

There are 57 market days remaining before the November 1 reset. In the two calculations above, I projected a rate of 1.20% if the average 5-year real yield falls to 2.00%. But if it continues around 2.10%, the fixed rate will rise to 1.30%.

Conclusion. With 2 1/2 months to go, we are right on the edge of the 1.30% fixed rate. The 1.20% fixed rate looks locked in as long as 5-year real yields remain anywhere near the current average of 1.84%, and the 1.30% rate is highly likely if rates continue at 2.10% or higher.

What about the variable rate?

Because of the recent surge in inflation, I had been expecting the I Bond’s variable rate to also increase from the current 3.34% at the November reset. This is not at all certain, however. Non-seasonally adjusted inflation fell 0.35% in June, a big surprise. The July inflation report, to be released Wednesday, could also be rather tame, with all-items projections hovering around 0.1%.

We will get a lot better idea after that July inflation report is released. I will be posting an analysis Wednesday morning.

Is there an investing strategy?

Yes. If you haven’t yet purchased I Bonds up to the $10,000 per person per year limit, hold off on any investment. The November fixed-rate reset is going to be an improvement over the current 0.90%.

If you are like me and already purchased up to the limit, there will be opportunities to use the still-existing gift-box option after the November reset, for people with a trusted partner. Plus, the new rate will be available to everyone from January to April 2027.

I will be writing about this topic often as we get closer to the November reset.

Qualifications

The projection presented in this article is based on 10 years of Treasury history in setting the I Bond’s fixed rate. But the Treasury could change course at any time. So far, in both of President Trump’s terms, the rate formula has remained accurate.

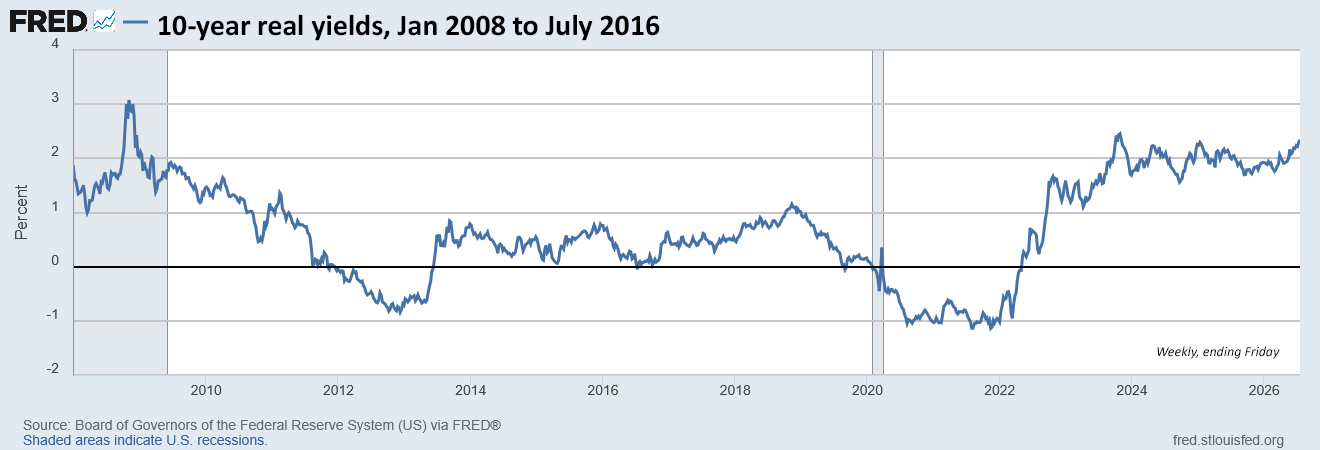

Keep in mind that the Treasury actually saves money by lending to I Bond investors at a real yield of 0.90% or 1.30% as opposed to the current 5-year real yield of 2.13% or 30-year real yield of 2.96%. Plus, savings bonds account for a minuscule portion of Treasury debt.

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

—————————

Donate? This site is free and I hope to keep it that way. Some readers have suggested having a way to contribute. I welcome donations, any amount. And FYI, ads on this site pay for about one visit to Costco.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Worth noting, the fixed rate formula didn't work nearly as well earlier in the history of I-bonds (formula/actual): 05/01/03: 0.90%/1.10%;…