Tipswatch.com, updated May 1, 2026

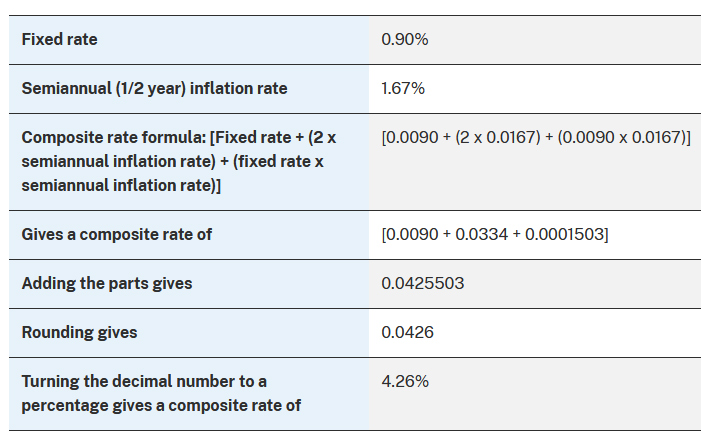

I Bonds purchased from May to October 2026 will pay a six-month composite interest rate of 4.26%, based on a permanent fixed rate of 0.90% and a six-month inflation-adjusted rate of 3.34%. Both the fixed rate and inflation rate will be reset again on Nov. 1, 2026.

The way I Bonds work

An I Bond is a Treasury security that earns interest based on combining a fixed rate and an inflation rate.

- The fixed rate will never change. So if you bought an I Bond in 2014 with a fixed rate of 0.2%, it will continue to have a 0.2% fixed rate for the life of the bond. Purchases through October 2026 will have a fixed rate of 0.90%.

- The inflation-adjusted rate (often called the variable rate) changes each six months to reflect the running rate of inflation. That rate is currently set at 3.34% annualized. It will adjust again on Nov. 1, 2026. Each reset applies to all I Bonds, no matter when they were purchased. (However, the effective start date of the new interest rate will vary depending on the month you bought the I Bond, a Treasury oddity.)

- The I Bond’s current composite rate is 4.26%, annualized, for a full six months for any bond purchased from May to October 2026.

Here is a chart from Treasury Direct showing how the timing of the rate change depends on when you purchased the I Bond:

| Issue month of your bond | New rates take effect |

|---|---|

| January | January 1 / July 1 |

| February | February 1 / August 1 |

| March | March 1 / September 1 |

| April | April 1 / October 1 |

| May | May 1 / November 1 |

| June | June 1 / December 1 |

| July | July 1 / January 1 |

| August | August 1 / February 1 |

| September | September 1 / March 1 |

| October | October 1 / April 1 |

| November | November 1 / May 1 |

| December | December 1 / June 1 |

How is the interest rate determined?

To get the actual rate of interest (the composite rate) the Treasury combines the fixed rate and the inflation rate. The combined rate will never be less than 0.0%. However, the combined rate can be lower than the fixed rate. If the inflation rate is negative, it can offset some of the fixed rate.

If the inflation rate is so negative that it would take away more than the fixed rate, the I Bond pays zero interest. But it cannot go below zero. This means that I Bonds are protected against deflation. TIPS, on the other hand, will see their principal balance decline in times of deflation, and therefore are less protected.

Here is an example from Treasury Direct on how the composite interest rate is determined:

How do I Bonds earn interest?

An I Bond earns interest monthly from the first day of the month of the issue date. The interest accrues until the bond reaches 30 years or you cash the bond. Interest is compounded semiannually. Every six months from the bond’s issue date, all interest the bond has earned in previous months is added to the bond’s new principal value. Interest is earned on the new principal for the next six months.

However, when you are tracking your total value on TreasuryDirect or with the Savings Bond Calculator, keep in mind that the values displayed for bonds that are less than five years old do not contain the latest three months of interest.

You can redeem the bond after 12 months. However, if you redeem the bond before holding it five years, you lose the last three months of interest.

• Track current & historical inflation rates used to set the variable rate

• I Bonds: Here’s a simple way to track current value

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

How does the Treasury set the fixed rate?

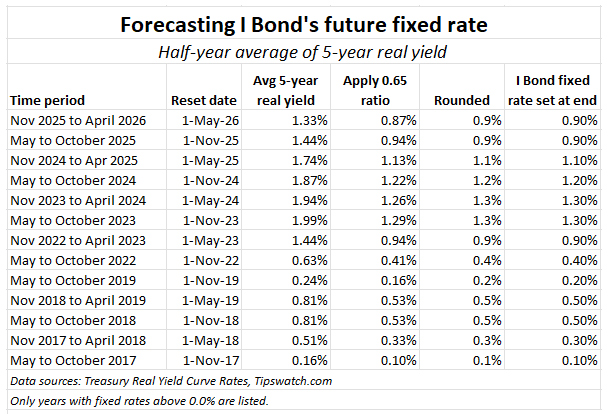

There is no announced formula and in theory this decision can be made at the discretion of the Treasury Secretary. However, over the last decade the fixed rate could be accurately forecast using this formula: Apply a ratio of 0.65 to the six-month average real yield of the 5-year TIPS. Here are results of that ratio since 2017:

Why are they a great investment?

- First, I Bonds are the most conservative and most safe of all investments. Your principal is 99.9999999% safe and it will never decline, ever. If inflation falls to below zero, the inflation-adjusted rate will fall to zero, but not below zero.

- I Bonds allow you fantastic flexibility. You can redeem them after one year, costing you three months of interest. Or redeem them after five years and pay no penalty, or just hold them for 30 years and cash out.

- I Bonds protect you against unexpected inflation. If inflation in the next 30 years suddenly soars to 7%, 10%, 15%, your principal will increase by that amount because of the inflation-adjusted interest rate.

- I Bonds allow you to defer federal income taxes until you redeem them, so you pay zero in taxes until they are sold. This is a big advantage over TIPS, which carry current-year income taxes for both the coupon rate and the inflation adjustment to principal. (Both TIPS and I Bonds are free of state income taxes, an advantage over bank CDs.)

- I Bonds are simple to track as an investment. Use the web-based Savings Bond Calculator, update your information, and check it a couple times a year. (The Treasury contends that this calculator is for paper I Bonds only, but it works fine for electronic versions.) This is another huge advantage over TIPS held at TreasuryDirect, which is a do-it-yourself proposition, even for downloading yearly tax forms. Want to track current value of your TIPS? Open up Excel and get to work. Treasury Direct is not going to tell you.

Is it difficult to purchase and manage I Bonds at TreasuryDirect?

A lot of readers don’t like TreasuryDirect, which can be a bit clunky. But the process of buying and redeeming I Bonds at TreasuryDirect works well. First you need to open an account, and I wrote a guide to walk you through the basics: Ready to open a TreasuryDirect account? Here are some tips.

When you set up the account, you will be linking a bank or brokerage account to TreasuryDirect. Then to buy I Bonds, you simply log into TreasuryDirect, set the purchase amount and date, and the purchase will be made. You can purchase I Bonds near the end of a month and get credit for a full month of interest. TreasuryDirect makes timing the purchase easy.

How do I use I Bonds for higher education?

If you use interest from a Series I bond to pay for higher education, you may not have to pay federal tax on the interest. However:

- If you want to use the bond for your education, you must be the owner of the bond.

- If you want to use the bond for your child’s education, then you or your spouse, or both, must own the bond. Your child may be a beneficiary but not a co-owner.

- Your modified adjusted gross income has to be less than the cut-off amount set by the Internal Revenue Service. This amount typically changes every year. See IRS Publication 970 “Tax Benefits for Education.”

What are the downsides to investing in I Bonds?

- Investments are limited to $10,000 per person per calendar year for electronic I Bonds held at TreasuryDirect. The Treasury stopped issuing paper I Bonds in lieu of a federal tax return on Jan. 1, 2025. Some investors find this amount too small to make a difference in their asset allocation. However, an investor using multi-year purchases can build a substantial stake in I Bonds.

- I Bonds cannot be redeemed in the first year of ownership and redemptions before 5 years will incur a penalty of the last three months of interest.

- You cannot create a joint account at TreasuryDirect, so a couple would need to set up two accounts, one with I Bonds registered as Spouse 1 with Spouse 2, and the other, Spouse 2 with Spouse 1.

- You cannot own I Bonds in a tax-deferred account. Even though I Bonds earn tax-deferred interest, the fact that they cannot be purchased in an IRA can be cumbersome for investors looking to move money within tax-deferred accounts, without tax consequences.

When I redeem my I Bonds, do I have to cash in the entire purchase, or can I do it in smaller amounts?

Here is what TreasuryDirect says:

For electronic bonds held at TreasuryDirect: You can cash a minimum of $25 or any amount above that in 1-cent increments. If you cash only a portion of the bond’s value, you must leave at least $25 in the TreasuryDirect account. Redemptions are comprised of principal and interest. (In a partial redemption, we pay interest only on the partial amount you cash.)

For paper I Bonds: Local banks have varying policies on how much they will cash in one transaction and some banks don’t cash savings bonds at all. If you send your bonds to Treasury Retail Securities Services, we cash them regardless of value if you meet requirements for cashing. Note: Individual paper bonds may not be split and must be cashed in full.

I bought I Bonds last year. Why does TreasuryDirect show less interest than I know I should have earned?

TreasuryDirect has a policy that makes sense, but it causes a lot of confusion: When you view your account balances on the site, it will not show you the last three months of interest earned until you have held the I Bonds for 5 years. You can’t redeem an I Bond for one year, and then from one to five years you will lose the last three months of interest. After five years, TreasuryDirect will show the full amount of interest earned. During the first five years, your I Bond continues to earn interest, but TreasuryDirect won’t show you all that interest until you have held the I Bond for 5 years.

I created a post that will walk you through the interest rate calculation: “Don’t go ballistic over the way TreasuryDirect reports I Bond interest“.

My interest calculations don’t quite line up with the TreasuryDirect numbers — off by a few dollars. Why does that happen?

TreasuryDirect calculates interest on an I Bond using a baseline $25 investment, then uses “pseudo-compounding” to raise that baseline each month. Then the baseline number is rounded to the nearest penny and is applied to your actual investment, meaning 400x for a $10,000 I Bond. This formula is going to sometimes differ from traditional interest rate calculations, by very small amounts.

I wrote about this: Let’s ‘try’ to clarify how an I Bond’s interest is calculated

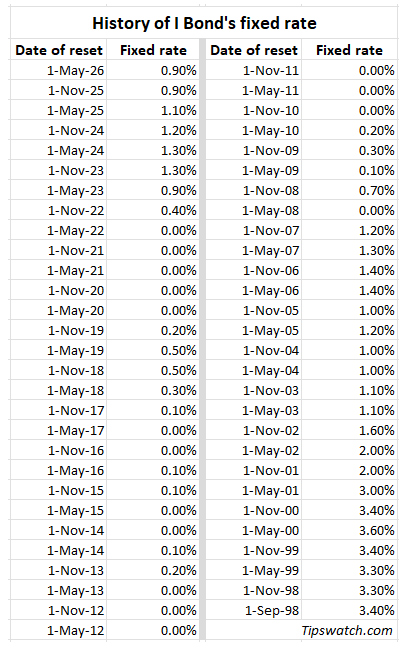

Fixed rate history

The fixed rate set each May and November applies to all bonds the Treasury issues in the six months following the date when it sets the rate. The fixed rate continues for the life of the bond. The Treasury has revealed no set formula for setting the fixed rate.

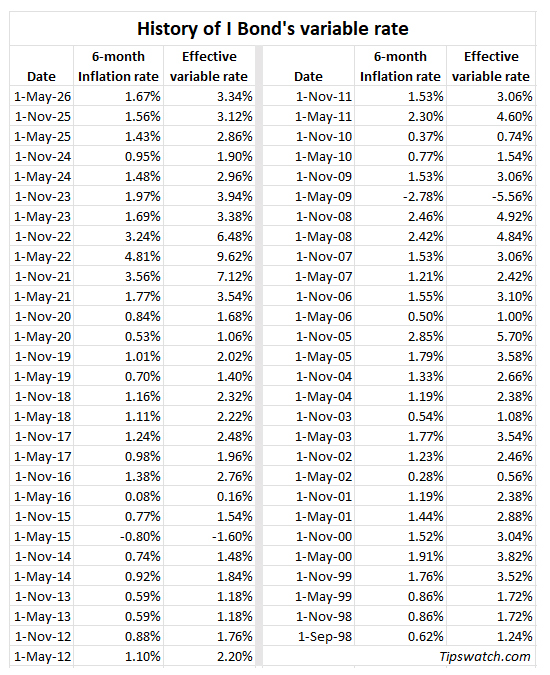

Variable rate history

As of May 2026, the new variable rate for all I Bonds is 3.34%. Here is a history of the I Bond variable rate since its inception in September 1998:

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

David: I happened to see this Q&A on the TreasuryDirect website:

“Question: What is the Series I bond?

Answer: The Series I bond is an accrual type savings bond tied to inflation. The bond is issued at face value with a 30-year final maturity–a 20-year original maturity period immediately followed by a 10-year extended maturity period.”

Do you have any insight on (I) why this 20 year plus 10 year maturity structure was adopted and (ii) whether it has any practical significance?

I have never seen this before. Good find. I think this must be a nod to the 20-year doubling feature of EE Bonds, but it really makes no sense for I Bonds, which basically can be redeemed after 1 year with a penalty or after 5 years with no penalty.

you may have addressed this already but now that BLS officially isn’t releasing October CPI how will this affect I bonds ? Thanks.

There won’t be much effect on I Bonds because the October inflation report is the first of six months that will determine the I Bond’s next variable rate. Reports for November and December and later months will catch up to reality before the May 1 reset.

Start of this Year in January, both me and my wife purchased 10K I bond individually and purchased 40K gift I bond for each other. i.e.

I have purchased: 10K I bond for myself + 40K gift I bond for my wife

My wife purchased: 10K I bond for herself + 40K gift I bond for me

Now question is:

Or would we be blocked from purchasing additional I bond for next 4 years because of 10K limit per year (10K * 4 years = 40K gift)? Would gift I bond purchases be block too!

For Next year, should we first purchase individual 10K I bond for ourselves and then deliver gift I bond. (As I understand from TD website, if you deliver 10K gift I bond first then it would count toward recipient limit for that year)

I can’t answer this with certainty. I can tell you that I was able to buy two sets of $10k in I Bonds the traditional way last year, and then two more sets in gift boxes. At the end of 2024, we delivered the gift sets with no problem. And then in 2025 we are able to buy $10K each the traditional way, no barrier.

It appears — but we have no definite guidance from TreasuryDirect — that you need to buy the first $10K the traditional way and then deliver the gift box I Bonds. If you deliver gift box first, then you won’t be able to buy the traditional way that year. In other words, a gift-box delivery will complete your traditional $10,000 limit. So buy the traditional way first, then deliver the gift boxes. You won’t be limited in future years (at least I wasn’t).

This issue has been widely discussed here and on the Bogleheads forum, and that is the best advice I can offer.

Thanks a million for the amazing tips! I do have one question. I want to convert some I Bonds—from paper to electronic form—that are in my name and my son’s name, who sadly passed away ten years ago. My question is: will there be any tax consequences simply from converting them to electronic form (without cashing them in yet), in case the ownership is considered to have changed?

I am not a tax expert, but I don’t believe there is any tax consequence to converting savings bonds. Taxes are due at redemption or maturity.

AMC, my wife and I each bought our own $10k I-Bond in our own account in Jan 2024. In August 2024, we bought each other 5 $10k I-Bonds as gifts. In December of 2024 we transferred those 10 I-Bonds to each other. Then in January of 2025 we each bought our own $10k I-Bond again. During this year we have bought gifts for each other again and have already transfer several but will transfer the rest before the end of this year. Next January we will buy or own BEFORE we buy any gifts for each other just as David has said.

If we are buying I bonds this year, are we better off to do it in April or wait until after May 1. With all the chaos going on do we trust that I bonds will continue to work as they have in the past?

I will have more to say on this later this month. But I will let you know I have already bought my 2025 allocation.

How does the US Treasury get away with pretending inflation is 1.9% right now? Serious question!

As of the latest report, November 2024, the U.S. inflation rate was 2.7%.

I was referring to the variable rate on I-bonds, currently at 1.9%. Why, when official inflation is 2.7%, can the US Treasury get away with an I-bond variable rate almost a third lower than the official inflation number?

The variable inflation rate is set by non-seasonally adjusted inflation from October to March and then from April to September. Those six-month periods cross over the variations in non-seasonal inflation. You need to look at two sets and average them to get an idea of annual inflation. In the current case, that is 1.9% + 2.96% = 4.86%, average of 2.43%. The actual inflation rate just before the last reset (based on inflation through September 2024) was 2.4%.

Is it better to buy an I-Bond at the end of this month (January) or forego a couple months of interest and see what the next fixed rate will be? When and where is this announced?

I am posting an article on this topic tomorrow morning, Jan. 5. https://tipswatch.com/2025/01/05/great-mystery-an-i-bond-buying-guide-for-2025/

If you purchase I Bonds through an existing LLC with a single owner (me) and the LLC dissolves (I retire) or is sold, what happens to ownership of the I Bonds?

This is out of my area of expertise. Seems like a question for a lawyer.

You will need to fill out the Treasury Direct Form: FS Form 4000 (Revised September 2022)

Request To Reissue United States Savings Bonds

If you are the “Entitled Person of the LLC” you can name a new owner and transfer the bonds to that person.

It will take a while to complete the transfer (like forever).

Hi, we bought I bonds in our names and in trusts a few years ago and we need to change our email addresses at treasury direct. I know they can be fussy. Is there any particular way to go about it that won’t cause issues?

Thank you

PS, are you able to change my email address ….

When you log into your account at TreasuryDirect, you can click on the ManageDirect tab and then go to “update my personal information.” On that page you can change your preferred email address. …. For Tipswatch.com, I have deleted your previous user and now you can just subscribe again with your new email address. Look for “Follow Blog via Email” area on the top right of the desktop page.

Purchased I-Bonds on 03/15/2021 and 01/27/2022 (at 10K each) as replacement vehicle fund. Been fortunate my twenty year old car has been reliable) but don’t want to push things much further).

My question is, “Would Monday, December 2, 2024 be a good time to sell my I-Bonds? My understanding is, selling early in month after the 1st of month is good time to sell. Or may wait to sell Tuesday, January 2, 2025 if I see $3500 of added interest income will create a negative 2024 tax filing issue (v;

It is good to redeem early in the month because you earn no interest for the month of redemption. And if you need to push the potential tax hit into 2025, it makes sense to wait until early January.

Thank you.

Douglas E. Says

I bought I – bonds in Dec ’21 without knowing the Tipswatch site. They have a fixed rate of 0%. I should been smarter and read Tipswatch and waited for a higher fixed rate (even though the variable was not too shabby.

I have to believe that with the treasury now yielding about 4% I really have no better option to sell the I – bond and buy the 10 year treasury. Does anyone have a better idea?

Those December 2021 I Bonds were a pretty good investment, believe it or not. For the three years ending in December 2024 they will have earned an average 5.57% average annual interest. They are still paying 2.96%, but in January they are going to transition to paying just 1.90% for six months. I can’t advise you what to do now; that’s your personal choice.

I bought the 10000 max for 2024 back in Jan. If I sell my 2022 bonds with the 0% fixed rate can I roll them now or must I wait until 2025?

There is no way to buy more than $10,000 for an individual in the traditional way. And redeeming an I Bond has no effect on the purchase cap. There are other options, though, such as the gift-box strategy (if you have a trusted partner) or using a trust or corporation. If you wait until January, you will be able to buy again up to the $10,000 limit.

Do you have any experience with automatic redemption at maturity of I-Bonds held in electronic form at Treasury Direct?

Does it work as advertised?

What do you need to do to assure that the proceeds are sent as an ACH transfer to your bank account and not shunted into a zero % Certificate of Indebtedness?

No, because no I Bond has ever matured through the 30-year term. The earliest that will happen is September 2028. And those early I Bonds were issued in paper form, so they would have to be converted to electronic I Bonds to automatically mature at TreasuryDirect. But I have had TIPS and T-bills mature at TreasuryDirect, and the payout has always worked flawlessly going to my registered bank account. (Which I have designated for the payouts.)

Do you mean that converted to electronic I Bonds to automatically mature at TreasuryDirect is not available until September 2028?

Ray, the question was about automatic redemption at maturity, which comes 30 years after the original purchase. So if you bought I Bonds in August 2024, the automatic redemption at maturity would happen in August 2054. I Bonds don’t have to be held to maturity, but to redeem early the owner has to go into TreasuryDirect to place a redemption order.

I overpaid taxes last year but Turbo Tax would not let me buy I Bonds when I filed because me my wife passed away last year and I was filing a joint return?

That sounds odd. People with joint returns get paper I Bonds this way all the time. Sorry for your loss.

Does TurboTax not include the option to edit the default owner registration on the refund I Bond? I wonder if that might have been the reason.I didn’t have any problem changing registrations in FreeTaxUSA, but I did accidentally leave a button clicked that resulted in one of the paper bonds arriving with the intended co-owner listed as beneficiary. Ultimately not a big deal, but I did feel irritated at myself for a few minutes when the mail arrived.

Never done this, so I don’t know. These paper I Bonds are the only ones with “AND” registration for a couple filing jointly. The reason, I assume, is that it is a joint return and obviously the bond should to go co-owners.

Hi. I used my federal tax refund to buy $5,000 in TIPs, but I had no idea they would send me a paper I-Bond in the mail. Do you have any insights into how I can get this paper I-Bond moved into my Treasury Direct account? Thank you!

The tax return I Bond purchase will always be in paper I Bonds. Back in May 2022 my friend Jeremy Keil wrote a guide for converting to electronic form … https://tipswatch.com/2022/05/08/ready-to-convert-paper-i-bonds-into-electronic-form-heres-a-step-by-step-guide/

I did this recently for other paper I Bonds and it is a bit cumbersome and tedious, but it did work.

I understand interest on I bonds is only earned from the prior month on the first day of the following month. So, if I want to earn my full month’s worth of interest for October (assuming I’ve held my bonds for at least 5 years) then do I have to wait until November 1 or November 2? I would think November 1 is the answer however Investopedia says November 2. Which is correct? Thanks.

Interesting. I would think Nov 1. Did Investopedia give a reason? The redemption would probably be delayed until the next business day, I’d guess.

I just read the article more closely and they are saying the US Treasury always pays interest on the 1st of the month and not again until the first of the next month. Withdrawing on the 2nd of the month enables you to collect the I bond interest payment on the first. So it sounds like the interest is not actually posted until the close of business on the 1st so you can’t cash it in until the 2nd in order to be able to collect the prior month’s interest.

If this is true, the US Savings Bond Calculator by Treasury Direct is deceiving because they say the value goes up each month, they don’t specify the day of the month.

How does 3 mos penalty in interest calculated as I bond interest varies. I purchased I bonds in Oct 2022 when the inflation was high. Now the rate is in 3.38%. Will i loose 3 month of the “new” interest rate ?

The penalty applies to the most recent interest earned. You have to wait until a full 3 months have completed at 3.38%.

Does anyone know about using the gift box approach for an individual with a Special Needs Trust (SNT)?

My sister has a SNT which has maxed its I bond purchases this year. I would like to use the gift box within the SNT to purchase I bonds in her name but not sure that is allowed. Thanks for any insight and help!

Thank you.

If I sell the 5/24/22 Series I Savings Bond today, is the 3 month prepay penalty approximately 24 days at 3.38% annually, and the remainder of the 3 mo at an interest rate of 6.68% annually?

Also, if I sell the 5/31/22 Series I Savings Bond on 6/1/23, is the 3 month prepay penalty approximately 1 month at 3.38% annually, and the remainder 2 mo at an interest rate of 6.68% annually?

Finally, if I sell the 7/5/22 Series I Savings Bond on 8/1/23, is the prepay penalty basically 3 months of interest rate at 3.38% annually?

If you sell the May 2022 I Bonds today the penalty would be three months at 6.48%. If you sell on June 1, the penalty would be two months at 6.48% and one month at 3.38%. If you sell the July 2022 I Bonds on Aug. 1, the penalty would be two months of 6.48% and one month of 3.38%. The penalty applies to previous entire months, not divided by days or weeks.

I guess that last one (Aug 1) is one month at 6.48% and 2 months at 3.38%.

I want to sell my Series I Savings Bond after one year (I know I will incur 3 mo prepay penalty), but on what date(s) can I sell to minimize the prepay penalty? Purchase dates in 3 different Registrations at $10,000 each are as follows: 5/24/22, 5/31/22, and 7/5/22. As you can see, one year has passed on the 5/24/22 purchase starting today. I look forward to hearing from you.

I Bonds are issued by month; not a specific day of the month. The May 2022 I Bonds can be redeemed on Aug. 1, 2023 and that will shift the penalty into three months of 3.38%. The August 2022 I Bonds can be optimally redeemed on Nov. 1, 2023.

I purchased a $10,000 bond in May of 2022 and when I check my account it does not show any interest, also at what interest am I earning now, I assume not the same high yield earned when I purchased it and finally how can I determine how much I will actually get if I close out my account? I would like to speak to someone concerning this but can not find a phone number to call. Thank you for your assistance. Joe

This page has the info you need: http://eyebonds.info/ibonds/10000/ib_2022_05.html … On the TreasuryDirect site, you probably have to click through for one more page to see that info.

Apparently, a purchase of the I-bond in April and May last year has taken the advantage of the highest interest. After that the i bond interest has dropped! The May 1st 2023 I bond rate has dropped to 4.3%. I bond no longer attracts people. The CD rate more than 4.0% is not difficulty to find at the bank.

I bought i bonds for my husband in 2020 and 2021 but because he could not remember his account number left it in my gift box. He finally figured it out this year but I made the mistake of gifting the 10k from each year to his account this year ( ie 20k straight away). Did we go over the 10k limit for 2023? Can he buy more i bonds this year?

Most likely $10,000 will be returned to the gift box and he can’t buy anymore.

If you sell an I-Bond on the first business day of the month do you earn interest for the entire month?

No. Interest is earned on the last day of the month.

How do I transfer my I bond to family member? I be heard you don’t get the paper bond back. It becomes electric!? How then do you keep track of what you have?

Also I have a few I bonds, 5K and 10K

30 year bonds.

Are these taxable when I cash in one?

Thank you so very much!

Is the 3 month interest penalty for cashing in before 5 years taxable?

Thanks

No. It won’t be reported as interest on the Treasury’s 1099-INT.

It has turned to April and tax filing deadline again since April 2022. It is not difficult to find a CD rate 4% right now. Is it still good time to continue buy I-Bond and why?

If your investing time-frame is 5 years, then a 5-year CD paying 4.5% looks attractive. I like I Bonds for the simplicity automatic adjustment to inflation. But 4.5% is pricing in 4.1% inflation with the I Bond’s fixed rate at 0.4%. I buy I Bonds every year simply to protect against another surprise period of high inflation. This worked well in the last two years.

What i-bond rate do you predict in May 2023?

Fixed rate? Could hold at 0.4%, or slightly higher

Thank you

I’m trying to understand how purchasing a $10K I bond at 6.89%, knowing it will drop in 6 months to 3.26%, and the unknown after that… does it compare to purchasing a 10K CD for 60 mos at a fixed rate of 4%.

I’m trying to follow all the math examples you provided to see why purchasing an I Bond makes sense, right before the rates drop. But, I’ll admit, I’m just not that smart, which is why I’m trying to read and learn more about all this.

So, hopefully, can you explain it in a way that doesn’t make my brain hurt 🙂

As I have noted in recent articles, 5-year CDs are competitive with I Bonds right now. If you can get a 5-year CD at 4.5%, then the inflation breakeven rate with the current I Bond is 4.1%, which is very attractive. So as a 5-year investment the CD looks good. I Bonds have a few other advantages: tax deferral and the state-income-tax exemption.

I-Bond was purchased last April. So far, the actual monthly earning rate is about 0.47% or annual rate 5.6% based on the interest earned. The actual annual earning rate is not 7.12% as we saw last April but low. Is it because the current holding has not included the last 3 month interest? Can you explain it? Thank you.

I assume you are looking at the value in TreasuryDirect, which will not show you the last three months interest until you have held the I Bond for 5 years. That 3 months of interest has been earned, but you don’t get it if you redeem early. If you purchased $10,000 in April 2022, your current actual value is $10,684.

How did you caculate the interest earned since last April is $684 based on the $10k i-bond, by the way?

I am getting this question often, so I will be posting an article tomorrow morning on this topic.

If you decide to make the election to have interest taxed annually (vs. when you redeem and receive the 1099-INT), how do you locate the 2022 interest? TD says “If the savings bonds are in a TreasuryDirect account, you can see the interest earned each year in the account.” The only interest shown is YTD on the website, which would include 2023 interest. How do you isolate the 2022 interest?

One way would be to go to this page: http://eyebonds.info/ibonds/index.html and click on the month and year that you purchased the I Bond. Then you can see how much interest you earned by month through 2022. You can adjust the purchase amount there, too. You would have to add up the monthly totals to get the yearly interest.

According to Treasury Direct, every six months the interest earned in the previous six months is added to the principal value of the bond. However, I don’t see this happening with my i-bonds that I purchased seven months ago. Is this due to the 3 month delay in reporting interest in the first five years? Are there specific intervals at which interest is added to the principal value of the bond, or is it determined by purchase date?

The interest for the previous month is added to your total on the first day of the next month. But when you look at the totals on TreasuryDirect, you will never see the last three months of interest until you have held the I Bond 5 years. Each six months, the interest is compounded, increasing the base amount earning interest.

New to I Bonds.

We file joint tax return. Had tax preparer file $5,000 I Bonds purchase with tax return. He advised the I Bonds would be in the husband’s name, as his appears first on tax return. When the paper I Bond arrived, we were surprised it was a single ($5,000) I Bond. (Had asked the tax preparer to purchase five $1,000 I Bonds. Not a huge deal that we received a single I Bond instead. Was surprised that the I Bond was issued to Spouse 1 OR Spouse 2.

Can the paper I Bonds not be issued in $1,000 increments, when bought with tax return?

Does the issue to Spouse 1 OR Spouse 2 mean either of us would be able to cash it in without the other spouse’s signature? Not that we would do that. Just very confusing.

In past years, I think the Treasury issued these in $1,000 amounts, but I’ve heard from others about getting the one $5,000 I Bond last year. I don’t think you or your tax preparer can do anything to alter what will be issued. The OR ownership seems to be limited to paper I Bonds, because the electronic versions have WITH ownership. Sorry, I don’t know if only one of you can cash the I Bond, but that’s probably true.

Just spoke with Treasury Direct. The I Bond referenced in yesterday’s comment can be converted to electronic in either spouse’s TD account.

For future reference, the paper I Bonds issued to Spouse 1 OR Spouse 2 can be redeemed by either spouse, singly.

For an iBond purchased less than 5 years ago, I understand there is a loss of the last 3 months of interest. Is the last 3 months the current month and prior 2 months, or is it the prior 3 months? For example, If I purchased an iBond on 11/23/2021 and redeem it today, I think that means I would lose the interest payments for Nov2022, Dec2022 and this month Jan2023, is that correct? Or, would I lost the interest payments for Oct2022, Nov2022 and Dec2022?

I Bonds pay interest on the first day of a month, for the previous month. So it is Oct, Nov, Dec.

I am fairly new to learning about iBonds and I wish I would have looked into that many years ago. I very much appreciate this website and thank you for helping out so many of us newbies. Also, this topic may have already been discussed, but I wanted to ask if it is fair to think of an iBond investment like a non-deductible traditional IRA? From my understanding, an iBond investment will grow tax-deferred for up to 30 years, which seems similar to an IRA. The earnings that accumulate each year are not taxed until the iBond is redeemed / surrendered, which is why I thought that it seems similar to a non-deductible traditional IRA. I realize that there are many different types of investment choices with an IRA, but with respect to the tax-deferred growth, an iBond seems similar. I know that the limit for an IRA contribution this year is $6000 and an iBond is $10,000.

Yes, an I Bond earns tax-deferred interest, so as an investment it is much like a non-deductible traditional IRA (except there is no need to pay RMDs after you reach age 72). Because an I Bond can be redeemed after 1 year with a penalty or after 5 years with no penalty, you can decide when to redeem and pay the taxes. It’s a very flexible investment.

In addition to being similar to a non-deductible IRA, there are other advantages to I Bonds. You can contribute $4000 more per year than to an IRA and there are no income qualifications. Contributions to an I Bond also do not reduce what you can contribute to your traditional IRA. Also, unlike a non-deductible IRA, you owe no state or local income taxes on redemption.

I invested $10,000 on 6/13/22 and I only gained $156 in value on 11/1/22. That seems low given that the interest rate was 9.62%. Help!

You will not see the last 3 months of interest on TreasuryDirect until you have held the I Bond 5 years.

We know the composite rate for I bonds issued from November 2022 through April 2023 is 6.89%. The composite rate formula: [Fixed rate + (2 x semiannual inflation rate) + (fixed rate x semiannual inflation rate)] = [[0.0040 + (2 x 0.0324) + (0.0040 x 0.0324)] = 6.89%. The people bought I-bond in April 2022 has earned the highest interest. Do you know who and how to determine the fixed rate? Thanks.

The fixed rate is set by the Treasury with no public formula.

When the I-bond fixed rate is 0, investing TIPS is better, especially when the inflation rate goes low. Do you agree?

Not necessarily. Depends on the TIPS real yield at the time. Right now, TIPS are the better investment because of a 100+ basis-point advantage. Other times, when the spread is small or TIPS real yields are negative, I Bonds are the better investment, even if the fixed rate is 0.0%.

What am I not understanding about the interest?

Doesn’t 9.62% on 10,000 = $962.00?

It would, if you got that annualized rate for 12 months. But it only lasts six months.

I basically have the same question, bought mine July 2022….also not sure when should I buy my next $10000…January or wait till april 2023?

I will write a suggested guide in early January, but here are the keys: 1) if this is a shorter-term investment, buy in January to start the clock running. 2) If it is a longer term investment, there’s no harm in waiting until mid-April, when you will learn the new variable rate and get an idea of where the fixed rate might be heading. An April investment will match the return of the January investment, dollar for dollar, but with a time lag.

Why are index ratios for month of Oct 22 flat or slightly lower even when inflation is north of 7%.

October inflation accruals for TIPS are based on non-seasonal inflation in August, which was down 0.04%. This is how the indexes work.

Thanks. Where can I find the data on the non-seasonal inflation?

Sanjay, I post nonseasonal inflation numbers for each month on my Inflation and I Bonds page: https://tipswatch.com/tracking-inflation-and-i-bonds/ The rate you see for each month is applied to TIPS principal balances two months later.

Thank you for your advice about I bonds. we placed our order on October 25 but I read an article that not all the orders will go through by the 28th and that is the deadline for the higher rate. I have not received a notification that it went through… Is there a way to know?

Thank you for your comments on buying treasury‘s at the last auction. It was a good decision. Is there another option coming up that we should be aware of?

Since so many people seem to be interested in these treasury‘s, could that change the price in there for the return?

Thank you

You could be OK, but the Treasury is supposed to send you a confirmation email that your order has been placed. I would have thought the buying process would be automated for people with active accounts, but who knows? … On TIPS, real yields have been declining since that auction; can’t say if that trend will continue.

thank you, I did get a notice the day that we made the purchase but that notice said your purchase has been scheduled, it didn’t say it had been done. Is that a confirming email we are looking for? I have been trying to go on to my account to see if the purchase went through but it just keeps crashing.

That notice sounds good.

Thanks for posting this article. The 9.62% is variable, meaning it WILL change correct? And, if I read the article correct this variable interest rate WILL change again in 6months? Also, like an IRA, can am I “adding” another $10k next year, or is it considered a separate investment every year I chose to invest the max $10k? Obvs, curious if I max it out every year if it will earn at the 9.62% forever?

The 9.62% rate for six months is ONLY for i Bonds purchased anytime before November. If you buy in November through April the variable rate starts at 6.48%.

Can you confirm the I-Bond interest rate from November 2022 to April 2023 will be 6.48%?

The variable rate will be 6.48%.

The variable rate is NOT I-Bond actual rate. The actual rate of interest for an I bond is a combination of the fixed rate and the inflation rate. The actual rate has not been known yet until November. Is it correct? Thank you for your answer.

OK, of course the variable rate is not what you call the “actual rate.” Not every time. Not when the fixed rate is above 0.0%. The Treasury calls this the “composite rate” which is fixed rate + variable rate (there is a formula the Treasury uses, so it could be slightly higher than that sum if the fixed rate is high). We will find out the next fixed rate on Nov. 1.

We created a trust to buy I bonds, but I have tried twice today and after entering everything I get a notification “our verification process is having problems, please try again later”. I assume this is a website problem, but is there anything that I could be doing wrong to trigger this response? I have created an individual account in the past so I think I know how to do it..

TreasuryDirect has been doing updates on Sunday, and it is possible you got caught in that.

Thank you! At least I know it’s not me!

My husband and I each created a revokable living trust. I remember than when buying personal bonds it was recommended that we buy in person A’s name WITH person B, so that the bonds would go to my husband if I die. Do I enter something similar when buying with the trust? Thank you,

I have no expertise in this area, but here is information on TreasuryDirect: https://www.treasurydirect.gov/indiv/help/treasurydirect-help/user-guide/291-300/#292 It says “An entity is not permitted to: Name a secondary owner or beneficiary in its registration”

More information is here: https://www.treasurydirect.gov/indiv/help/treasurydirect-help/user-guide/291-300/#Trust

Thank you, your website is very helpful!

Hi David,

Thanks for providing such excellent information on this site!

I purchased a $10k I Bond on 12/31/2021, but the security was issued on 1/03/2022. It is not clear me to me whether this purchase counts for calendar year 2021 or 2022? I see the following information on my account dashboard. Does Treasury Direct consider the “purchase requested” or “security issued” as the official date of purchase? I can’t seem to find this information in their FAQs. I’m trying to see if I can purchase more in 2022.

Security Type Date Transaction Amount

Series I Savings Bond 01-03-2022 Security Issued $10,000.00

Series I Savings Bond 12-31-2021 Purchase Requested $10,000.00

Thank you.

If the I Bond was registered as January 2022, it is a 2022 purchase and you are at your limit. I always recommend buying I Bonds a few business days before the end of month to avoid this problem. For this month, the ideal days would be Oct. 26 or 27.

Thanks for the quick reply!

In April I made a mistake. I did not wait for a little time to purchase the I-Bond in May but April. As a result, I did not earn the higher interest rate. I plan to purchase a gift i-Bond. Should I buy it in October or November? Will the November likely have the higher rate than October?

If you purchased in April, you did great. Your I Bond earned 7.12% for six months and now will earn 9.62% for a full six months. All I Bonds earn all future variable rates, but the starting month depends on the month you purchased. In your case, the 9.62% begins right now, in October. The November variable rate (probably about 6.4%) is likely to be lower than the October rate (9.62%). But it is possible that the I Bond’s fixed rate will increase in November. So it’s a toss up. If you are a short-term investor, gifting in October probably makes more sense.

When will people know the November rate? Will it likely be higher than 9.62%?

It isn’t likely to be higher than 9.62%. Probably about 6.2% to 6.4%; one month of data remains, which will come Oct. 13. I track this here: https://tipswatch.com/tracking-inflation-and-i-bonds/

Has the November rate come out?

Rendy, we now know the variable rate will be 6.48%, but we don’t know if the Treasury will raise the fixed rate above 0.0%.

Thanks for the info. Shall we know I-Bond rate before the November 1st? If no, do you recommend buying the I-Bond gift on October 26 or 27 or wait until November?

We bought I bonds in Jan 2022 and I THOUGHT that I indicated that they were for tax year 2021. I tried to buy bonds yesterday again (for 2022) but the treasury direct website says that I have reached my maximum for the year. I am looking on their site and I can see when they are purchased, but I cannot see which year they were allocated to. If they are allotted to 2022, can I change them t0 2021? If so ….how?

I can’t remember every step but I thought I remembered being very careful to put them in for 2021.

If you made the purchase in January 2022, even one day into the year, the purchase counts as a 2022 purchase and there is no way around that. You cannot purchase I Bonds to in 2022 to be applied to your 2021 purchase limit. The month you purchase is month of issue. You can purchase more I Bonds in Jan 2023, or look into the gifting strategies … https://thefinancebuff.com/buy-i-bonds-as-gift.html

Thank you! I think I was confusing it with the 5K we overpaid for our taxes to buy 5K more in I bonds. My accountant said be sure you indicate that it is for 2021. We did buy 5K more with our tax refund for 2021 but the purchase was made in 2022. Which year does that count for? We have done 20K this year the regular way, can we overpay our 2022 taxes and apply the 5K to purchases for 2022? Also, is it worth it to consider creating trusts in order to buy 10K more each? How big a deal is that? We don’t have trusts right now. Thank you very much for your help! Your site is great.

The $5000 tax refund doesn’t count against the annual cap, but the limit is $5k per tax return. So the next time you can do that is when you file in 2023

Thank you, is the 5K bond we bought with in the year 2022 with our tax refund for 2021 – is that counted for 2021 or 2022. I understand it doesn’t count in the 10K limit. Do you think it is worth creating a trust if the only reason we would have one is to buy i bonds?

Hi David,

I think I asked this before in one of your other articles, but couldn’t find it. Anyway, once the 12-month hold has been lifted, what can be expected when you cash it out? With the high rates, I have no plans on doing so. Just curious. Can you withdraw any amount just like a checking account (only dollars, no cents of course)? Do you have to do something weird and only withdraw in $25 increments? I would think not, but hey it’s the government. Also, is this all electronic or do you have to have a check mailed? Thanks!

Obviously, don’t cash out now because the 9.62% annualized rate is at risk. Don’t want to lose that. From TreasuryDirect: “You can cash a minimum of $25 or any amount above that in 1-cent increments. If you cash only a portion of the bond’s value, you must leave at least $25 in the TreasuryDirect account. Redemptions are comprised of principal and interest. (In a partial redemption, we pay interest only on the partial amount you cash.)”

Would this be an idea worth considering or have any chance politically, fiscally, economically? A special variation of the I Bond specifically for very conservative, very safe retirement investing to be renamed the R Bond, the R being for both retirement and for Roth. The annual purchase limit and the ages for redemption would be the same as for IRAs and there would be a 5-year minimum holding period for each bond (similar to the I Bond holding period to avoid the 3 month interest penalty as well as the minimum for Roth IRA accounts). Eliminate the fixed rate so it would only earn an inflation rate set every 6 months, never going below zero. Eliminate any income tax (as with the Roth). No maximum holding period during individual’s lifetime, but must be redeemed upon death to beneficiaries.

Seems like a reasonable proposal. Right now, the I Bond serves as a “stealth traditional IRA,” since earnings generally aren’t taxed until you redeem. Eventually, taxes will be owed, so investors need to prepare for that. One issue with the Roth idea would be if the I Bonds could be purchased if the buyer didn’t have wage income, as is required with current Roth investments. And would you keep the current Roth limit on purchases by people over certain income levels? I’d keep the fixed rate, though.

Since I Bond interest is exempt from federal taxation if used to pay for higher education expenses for yourself or a dependent and contributions to a 529 account qualify as an exempt education expense. Can I cash in my I bonds, make the contribution to a 529 account in my name making the interest exempt from federal taxation, and later change the beneficiary of the 529 account to cover higher education expenses for my grandchildren?

I’m not an expert on this topic but author Harry Sit has an excellent article: https://thefinancebuff.com/cash-out-i-bonds-tax-free-college-529-plan.html

I have two questions about i-bonds:

First, I’m trying to decide whether to buy some i-bonds now, late August 2022, or wait till November 2022 in case the fixed rate goes up a little. I know you don’t have a crystal ball, but what would YOU do?

Here’s a more general question:

I recently retired. When I was working, I chose to maximize my Roth IRA first each year, and then purchase what i-bonds I could afford. Having an extremely low risk tolerance, I’ve ended up with my Roth IRA investments in CDs.

Recently, the interest rates on the i-bonds have been so much higher than what I’m getting with my Roth IRA CDs, that I regret not having purchased more I-bonds instead.

In less than a year, I will be 59 and 1/2 and therefore able to make withdrawals from my Roth IRA without penalty. I’m thinking of withdrawing $10K per year from my Roth IRA then and buying 10K of i-bonds with it each year.

Is that a good idea? I guess another way of asking this question would have been to just ask whether i-bonds are a better investment than Roth IRA CDs in general.

Thank you very much for any advice.

Hello Pat. I am not a financial adviser, but I would recommend buying now to lock in the 9.62% for six months. That’s $458, too good to pass up. It’s unlikely the fixed rate would rise, at this point. Could change.

I don’t like the idea of removing money for a totally tax free Roth to invest in a taxable i Bond. Do you have another way to raise the money?

Thank you very much for the quick response!! This is very helpful to me.

It would be difficult for me to go back to work now, due to health issues and taking care of an elderly disabled parent (and frankly, I’m kind of burned out after working office jobs with rigid hours for 40 straight years.) I have a small pension, which pretty much just covers expenses. I’m not old enough yet to file for early Social Security benefits, of course. I could probably raise a little bit of money selling on Ebay some of the junk around the house that I don’t need.

I’ve bought I-bonds on treasurydirect over the last two years, both times at the maximum $10,000. The first were purchased 03/2021 and the second 03/2022. I’m a bit annoyed because it would seem that ibonds do not actually track inflation. The Bureau of Labor Statistics reports that year over year inflation from 03/2021 to 03/2022 was 8.5%, but my ibonds held for that same period have only increased 3.8%, looking at the current value of my holdings.

I feel swindled. At first blush, the treasury’s choice to have the bonds recalculate every 6 months seems like it would make no difference, but in effect it causes the bonds’ interest rates to lag inflation by essentially 6 months, reducing one’s expected returns in a period of rising inflation by half.

What is your take on this? I’ve put $20,000 into ibonds and their current value is $20,500. Maybe I just chose a terrible time to buy? If so, I recommend that others beware: these are not a fundamentally safe bet. You are still gambling about where you expect inflation to go, and you must time the “market” to get out ahead.

This question is addressed in the Q&A: ” … keep in mind that the values displayed for bonds that are less than five years old do not contain the latest three months of interest.” TreasuryDirect will not show the last three months of interest until you have held the I Bond for 5 years. I have tracked the I Bond’s variable rate for more than 10 years, and I can assure you it accurately reflects official U.S. inflation.

The I Bond you bought in March 2021 would only show 14 months of interest and the one you bought in March 2022 would only show two months of interest. You actually picked very good times to buy and your investment is doing fine.

Scott, I wrote an explainer on this topic, inspired by your question: https://tipswatch.com/2022/08/09/dont-go-ballistic-over-the-way-treasurydirect-reports-i-bond-interest/

I consider being TIPS on secondary market. For example, there are TIPS maturing 01/13/2023, i.e. 5.5 months from now. They have 0.125 coupon, 101,04 price, and large negative yield to maturity -2.138%, which does not look good. But if inflation adjustment for 5.5 months is anywhere close to 4% or 5% (same as for I-bonds), then buying it would still be a very good deal, much better than for 6 month T-bonds.This is my first attempt in buying TIPS on secondary market. Am I making some silly mistake in my analysis?

These very-short term TIPS are complex and yields can be deceiving. In this case, the index for accrued principal is 1.265. So if you buy $10,000 of par value for this TIPS you are actually buying $12,650 of principal. You are going to have to pay a small premium, so your actual costs (as of Friday) would have been around $12,757 for $12,650 of principal. There will be a big inflation accrual in August (based on June inflation), 1.37%, but after that, it is very hard to predict where inflation will be running. I doubt — but who knows — that inflation will continue running at a 9% annual pace from July to November, the months that will set your final inflation number on the Jan 15 2023 maturity. Predictions for July are running at about 0.3%, or less, because gas prices are falling. You could be looking at an inflation accrual gain of about 2.10% at the Jan 15 closing, hard to predict, plus the final small coupon payment. That would be decent.

I am not a financial adviser and I can only give an opinion: This TIPS probably looks OK, but it probably won’t greatly out-perform other similar investments.

Thank you very much for such a quick and detailed reply! I hear from numerous comments that it may take Fed perhaps 2 years or more to bring inflation down to 2.5%. But you may be right, and in November it will be small. My problem is that I am confused by terminology, and large negative yield to maturity -2.138% looks concerning. Or maybe this is already taken into account in the price? For now, I like 6 months T-bonds with rate about 3%, which does not involve these uncertainties.

I can’t find an answer to my question anywhere on the Treasury Direct website. Tried calling but gave up after 1 1/2 hours on hold. Can you guide me? In 2002 and 2003 I bought one I bond each year online. I was not required to set up an account to do so. Three times a year I go to the Calculate section and find out what my bonds are worth, so I know they’re there. In Dec. 2021 I bought two more I Bonds and set up a TD account under my now-married name. The earlier bonds were in my pre-married name. I do not have physical paper bonds for the earlier bonds. I want to move them from TD purgatory into my new account. How do I do this? There must be some forms to fill out and a correct process. Thank you for any help.

As painful as it seems, talking directly to TreasuryDirect is probably the only way to solve this issue. You had to have an account to buy the I Bonds electronically, but maybe that account was with Legacy Treasury Direct? Do you have any paper work to show an account number for those purchases? Or, do you just need to merge the two accounts? It’s definitely doable, with the name change, too.

Hi

Is there any time of the year that it’s better to purchase I bonds than other times of the year? or just but today and start earing interest

In general (other years, but not now) I recommend waiting until mid-April and/or mid-October to make an I Bond purchase decision, because after the March and September inflation reports are issued, you will know the I Bond’s next variable rate and can judge the potential for a higher fixed rate. But this year, because of the 9.62% variable rate, it is better to simply buy now and get 6 months of 9.62%. You can buy near the end of the month and you get full credit for that month.

Experts ever recommended buying I-bond at the end of April because they predicated the interest had reached high enough and it may not continue to go high. Now the inflation hits 9.1 percent, the new peak. People chose buying I-bond after May did a better decision. People who has already bought this year I-bond and want to take advantage of the new higher interest rate, they have to buy the I-bond as a gift for the family member and late redeem it some time next year. How do you think about it?

Well, as a “expert” who strongly advised buying I Bonds in April, I disagree. The idea was to lock in 7.12% for a full six months, and then 9.62% for a full six months. And whatever future rate comes, both buyers will get that future rate for six months. Buying in April was the “better” decision, but buying now is a “wise” decision. When you buy an I Bond, you get the current interest rate for six months, and then all future interest rates for six months.

Now it is easy to disagree buying I-Bond in April is better. Hopefully experts can advise whether it is better to buy the I-Bond in October or November in the month of October but not do so after October.

I recommended buying in January, so I am taking the rest of the year off. If you need advice: Buy now. It’s still fine.

I have a $20,000 Ibond dated 4/1/2007, which I bought before the purchase limits increased. The TD site says that my specific bond currently pays 8.57% while elsewhere on the site it says the bond should pay 11.09%, as does your chart in this posting. What gives? Are different rules in place for bonds over $10,000?

That I Bond will have the 7.12% variable rate until October, then switch to the 9.62% variable rate for six months. It has a fixed rate of 1.55%, correct?

Thanks. I guess that’s the “Treasury oddity” you mentioned.

if I buy $10,000 I Bonds right now, when will it be smart to buy a second set of $10,000?

If you buy $10,000 in electronic form today, you won’t be able to buy any more for your personal account at TreasuryDirect until January 2023. The key factor looking ahead into 2023 is that the I Bond’s fixed rate could rise above 0.0%, possibly in November 2022 or May 2023. So waiting until closer to May 2023 for the second set might make sense.

I am purchasing bonds for my elderly father. How do I document my sister and I as the beneficiary so we don’t have to go through probate. We have all his other accounts set up with all our names on this but that doesn’t seem possible with I Bonds.

I am assuming your elderly father already has a TreasuryDirect account? If so you will want to register each purchase with 1) him as the primary owner and one of you as beneficiary which uses the payment on death registration, for example, JOHN DOE POD TO JANE DOE. Or, 2) you could use the two owners registration, with him as the primary owner and one of you as the secondary owner. That uses the WITH registration, for example, JOHN DOE SSN 987-65-4321 WITH JANE DOE SSN 123-45-6789.

I am not an estate lawyer or even any kind of expert, but I think either form of ownership would pass the I Bond to the second named person as the sole owner after the primary person’s death.

To divide these equally, just register half your purchases with Sibling1 as the secondary owner and the other half with Sibling2 as the secondary owner. You will all need separate accounts at TreasuryDirect, I believe, as least at redemption.

If I buy I-bond as a gift for someone else this year, can I change my mind and change the gift to my own purchase next year or change the gift for a different person? Thank you for your answer.

No, I don’t think you can give it to yourself. The I Bond is no longer “yours” after you designate it as a gift. You can name yourself or another person as beneficiary, however, in case the person dies.

Thank you so much for great information about I-Bonds, it is especially helpful for newbies! After reading this post along with replies to questions, I think I understand that if I were to use the TD Gift Box to purchase a gift this year (2022) for my spouse to deliver next year (2023), that gift purchase would start earning interest right away, I think at the current rate May rate of 9.62%, is that correct? I wanted to be sure a Gift Box would start earning interest before it’s delivered and I didn’t see any conformation of this on the TD website.

The TD website is vague about this, yes. But from every source I follow, your understanding is correct. Put it in the gift box FOR SOMEONE ELSE. It does start earning interest immediately. When you deliver it to that person in a future year, it will count against their purchase cap that year.

Thank you so much, I appreciate it.

My question revolves around how to set up my TD account so that my wife can inherit my iBoinds most easily should I pass first, or vice versa. I set up my first purchase yesterday and simply registered myself as owner. I did not see anyplace to set a beneficiary while setting up my account, but apparently you designate the beneficiary with each individual purchase. Is it ‘best’ for estate planning purposes to register my account as ‘Owner 1 (ie me) with Owner 2’ (ie my wife)? Since I opened my account as simply Owner 1, can I change my account to say ‘…with Owner 2’? If not, should I simply designate her as my beneficiary at each purchase? Also, my wife and I would like to buy $20k/yr of iBonds and I don’t want how I title our accounts to reduce how much we can purchase per year. Please advise.

Yes, you can change the registration for securities you have already purchased and also change the “default” registration for each future purchase. You will probably want to use the WITH registration. Each spouse needs a separate TD account to buy $20,000 a year.

My question is what happens to the remaining balance after a partial I bond redemption in Treasury Direct? Since there will no longer be an exact I Bond, how is the balance of that bond displayed in my TD account?

Following

When opening TD account, it asks about

Taxpayer Identification Number Certificate

By checking this box I certify, under penalty of perjury, that:

The number shown on this form is my correct taxpayer identification number.

I am not subject to backup withholding because: (a) I am exempt from backup withholding, (b) I have not been notified by the Internal Revenue Service (IRS) that I am subject to backup withholding as a result of failure to report all interest and dividends, or (c) the IRS has notified me that I am no longer subject to backup withholding.

I am a U.S. person as defined by the IRS.

What does it mean? Should one check it if s/he is required to file tax return?

No, checking that box only certifies that the IRS has NOT required you to do backup withholding.

In January my wife & I purchased $10,000 each of I-Bonds. Can I now gift her another $10,000 & she gift me $10,000. Is this OK? Thanks for your informed response.

Yes, you can each place $10,000 in TreasuryDirect’s “gift box,” for delivery later to your spouse. They begin earning interest and can stay in the gift box until next year, or later. When they are delivered, they count against the $10,000 purchase limit in that year, so you technically cannot double up in one year.

OK great understand. I purchase now & deliver next January at which time I can purchase another gift & hold that till the following January. Thank you very much for this would have never discovered this without your excellent advice.

Sorry but I just read on the Treasury Direct website that the total for each individual is $10,000 which is to includes any gifts. You can obtain another $5,000 in paper I Bonds that are purchased with your tax refund.

This is correct. You can buy $10,000 for yourself and place $10,000 in a gift box for another person. That gift is no longer yours and doesn’t count against your purchase limit. When you deliver it to the other person, it then counts against their purchase cap. You can’t both buy and receive $10,000 in I Bonds in one calendar year. If you try to do that, TreasuryDirect will simply move the gift back to the gift box where it originated.

Hi,

I really enjoy your information and depth of knowledge on I-Bonds. I understand the paper limit is $5,000 per tax return, so for a couple filing jointly the limit is $5,000. However, my son gifted me paper I-Bonds with his refund via his tax return, does this count towards the $5000 or is this a vehicle to add incremental I-Bonds annually.

I’ve never seen this question before. I don’t think it would count against your cap on electronic I Bonds, and it probably wouldn’t count against the paper I Bonds, either. But I’ve never seen TreasuryDirect address this question.

If you choose to redeem your I bonds after 1 year but before your five year you loose out on the last three months of interest payments. Does that include the inflation adjustment for those last three months or is it just the nominal interest rate set at the beginning?

Am I correct in understanding that the $5K paper I-Bond one can purchase in lieu of a tax refund (Form 8888) is in addition to the $10K purchased on TreasuryDirect? Since it doesn’t count toward the $10K, it’s a way for an individual to buy $15K of I-Bonds per year? Thanks!

Yes, this is correct. The limit is $5,000 per tax return, so for a couple filing jointly the limit is $5,000.

If I wanted to buy before the Tax Day – April 18th, 2022, what tax year data is used to determine taxable income / limit for the $10k purchase.

If I buy before April 18th and if it applies to 2021 tax year, when would I be eligible to buy another $10k – one year from date of purchase or any time during the next physical tax year?

What happens if you buy $10k and your annual income exceeds the cut off limits?

If you sell property and have a long term capital gain on it, does that impact your cut off limit?

Also, I assume both my wife and I can buy $10k worth of I-bonds if we file a joint return?

The $10,000 limit is per person for a calendar year. There is no income test for the purchase, so don’t worry about that. … A couple needs two separate TreasuryDirect accounts to buy $20,000 a year.

Paper I Bonds were protected from loss if lost or stolen, from what I remember. We converted our paper I Bonds to electronic bonds at Treasury Direct.

Now I wonder if the same protection is still there. For example if somehow my account were hacked, and the bonds were somehow cashed by a thief, would I still be protected? Or should I have just kept the paper bonds for better protection?

Not expecting any issues like this, but would like to know the answer.

The Treasury doesn’t give specific assurances. The general belief is that if the Treasury itself is hacked, you will be protected. If you get phished and reveal account information, you are at risk. The Treasury sends many notifications of account activity, so you will get a warning.

Just here to ask about updates on the treasury website. I understand it won’t show anything for the first three months due to the penalty. However, I have some from 12/2021 and figured it would show something by now. December, January and February are the first three months of penalty. Granted the first landed on a Friday. I’m not too concerned, but figured I would ask when I could/should expect the update. Ten business days? A month? Just curious.

Hi Joe, I believe your December purchase should have shown the interest for 1 month starting on Apr 1st. I too purchased $10k Dec. 2021 and my interested of $60 showed up April 1st.

Hi Steven,

That’s what I figured. I checked it again first thing this morning and I still didn’t see anything. However I went back and checked it around 9:30 AM and I saw the $60. Maybe it just didn’t update on mine? I don’t know. It’s there now though.

*********************************************************************

As a follow up question, when they compound the interest every six months, I would assume that is only with the fixed rate, correct? So in other words with a 0% fixed rate, there is basically no compounded interest for the entire life of the bond? Or would the next six month’s rate apply to it (ie $10,356 would be counted towards the new rate set in May)?

Thanks!

Thank you for very helpful/informative website. ?s on buying paper I bonds: 1) It seems this can only be done if you are owed an IRS refund for a tax year filing by filling out form 8888 with your tax return, correct? 2) Assuming this is correct and if you intend to buy say $5k of I bonds (or at least have the possibility to do so) then would it make sense assuming you need to pay in 1/4ly tax estimates that several weeks before you expect to finalize/file your return that you would make an additional estimated tax payment of $5k so that you would have a refund coming to you? 3) If one is not obligated to make estimated 1/4ly tax payments could you voluntarily do so say via the EFTPS.gov website?

Q 1: Correct, paper I Bonds are only available in lieu of a federal income tax refund, limited to $5,000 per return.

Q 2: Yes, overpaying your estimated taxes is one way to ensure a tax refund in the amount you want.

Q 3: Yes, I believe anyone can pay estimated taxes. If you are still working, you could also set up over-withholding to get the same result.

can you own I bonds in a roth ira account?

No. I Bonds cannot be purchased in any sort of tax-deferred account.

I agree it would be convenient to be able to purchase I Bonds in a retirement account, using tax-deferred money. But TreasuryDirect does not allow tax-deferred accounts. One thing to keep in mind: Interest on an I Bond grows tax deferred, so it is basically a “stealth” traditional, non-deductible IRA.

Correct, but if OP and his wife would establish a Trust and add the account to TD (just need the Trust number and can be done in an hour online) then each person with a trust can also contribute $10,000. $40K for a couple every year this way.

I’m using I-Bonds as a place to park my daughter’s college fund and it’s looking like the next period’s composite rate will be around 4% for the next six months. Regarding the forfeiture of 3 months of interest if they’re sold within 5 years, what if inflation reverses and the composite rate becomes 0% when it’s reset next Fall? Do I just hold the I Bonds for three more months at 0% and those three months constitute my forfeiture? Or do they go back to the last 3 months where I received interest?

My guess is that the next variable rate could be as high as 8% for the next six-month period. That would happen if non-seasonally adjusted inflation comes in at 0.7% or higher for both February and March. But you are correct that the 3-month interest penalty is on the last three months of interest earned. So you should avoid taking the penalty after the interest rate has been high, if possible. If the rate is zero, the penalty would be zero.

Yes, I meant 4% for the six month period – or the equivalent of 8% annually. Thanks!

Hi David,

I had a question about the 12 month change number. I’m a math geek and played around with the numbers and found out how all of it is calculated. However, I’m confused on why you include 12 month number. Is it somewhat like a stock 1 year graph? Just additional “info.” Or does it kind of forecast what will happen next year as far as percentage and therefore the chance of inflation going up (or down)? For example, inflation was 1.2% in October 2020 vs 6.2% October 2021 or 276.589/260.388 which equals a 6.22% increase. Just curious if I was missing something. Thanks!

I am assuming you are talking about the 12-month inflation numbers on the “I Bonds and Inflation” page? Yes, that is “additional info” and shows the trend over the last 12 months. It does not predict the future at all. I also use these number to talk about the inflation-based increase in TIPS principal balances, so it is helpful to have them here.

I’m new to any kind of bonds but I’m kinda kicking myself about not knowing about I Bonds until now! Regarding the formula to calculate the composite rate:

For a 6-month period, is the adjusted rate used actually 2X the inflation rate?

Composite rate = [fixed rate + (2 x inflation rate) + (fixed rate x inflation rate)]

I’m fairly certain that is the case but I’m astounded that I never knew about this. I’ve had a couple of financial planners since 2002 and not one has ever even mentioned they exist!

———

One other generalized question:

When the Fed starts getting involved and actually starts raising interest rates in their attempts to “control” inflation, should we expect the fixed rate to increase and the adjusted rate to significantly decrease?

Timewise, does that happen quickly or is it something that takes years? (just realized that is probably an economics dissertation!)

What I call the “inflation-adjusted variable rate” (a term not used by the Treasury) is 2x the six-month inflation rate. But that is an annualized rate, only in effect for six months. I think your understanding looks correct. In most cases, the composite rate will equal the fixed rate + variable rate, but if the fixed rate is rather high (not true recently) the formula will reflect a slightly higher composite rate, because of the effect of compounding.

The Fed raises short-term interest rates, which probably will have little effect on the I Bond’s fixed rate. But if you see the 10-year nominal Treasury rising to a level of 2.5% or higher, that should push 10-year real yields above zero, and THAT could at least make a higher fixed rate possible. I don’t expect that to happen before the May reset.

Thanks, David. I of course now see that Joe had almost the same exact question last week regarding the Fed and potential impacts to an I Bonds fixed rate. I appreciate BOTH responses. Lots to learn.

I noticed today (April 17, 2022) that the 10 year treasury rate is at 2.83%. So possible fixed rate increase in May after all?

Don’t look at the nominal rate. Look at the real yield of a 10-year TIPS. Still negative at -0.06%. Why raise the I bond fixed rate? But … we are definitely much closer to that possibility.

Thanks for the reply. I should have read your latest post today on 5 year TIPS. Would have answered my own question.

Hi David,

I have been reading your posts and you have answered many questions.

I was wondering what numbers you focus on and when they come out. I’ve seen your excellent charts on the index and percent changes, but where do these numbers come from and how are they interpreted. For example, looking at your “Q&A on I Bonds” page, January’s inflation index hasn’t been posted. When are they expected and where would I find them if not for your website? I understand that we won’t know the numbers for the next 6-month rate, but I would think as it gets closer to March/April, we will have a pretty good idea of what it should be around (ie at least 3.00% by example only).

I know you have no crystal ball, but I would like to think it is similar to knowing it’s going to be hotter in the summer than it will be in the winter. How much? Who knows, but we know it will be. Same with the fixed rate. I read your article on why buying now will payoff with 0.0% (ie 14 years to br

Good questions, Joe. The non-seasonally adjusted inflation numbers shown on the “Inflation and I Bonds” page come from the monthly inflation report issued by the Bureau of Labor Statistics. The January report will be issued Feb. 9 at 8:30 am EST. You can go to bls.gov that morning and read the entire report (which I always link to in my monthly inflation article).

No one can accurately predict future inflation, especially more than a month out. The experts have been way off on estimates over the last year. I’ve been guessing that inflation from September 2021 to March 2022 will run in a range of about 2.25% to 3.75%, which would result in a new I Bond variable rate of 4.5% to 7.5%. That’s a guess, but it does look like “headline” inflation will be fairly high through March, because the baseline numbers for January to March 2021 were pretty low. But non-seasonally adjusted inflation might run a little lower. Those numbers were higher than the headline numbers back in January to March 2021 … 0.43% for January (versus 0.3% for headline), 0.55% for February (versus 0.4%), and 0.71% for March (versus 0.6%).

Hi David,

Thanks for the reply. I see my message cut off for some reason. I mentioned that I saw your article about comparing to wait for an uptick in the fixed rate vs going ahead and taking the 7.12% and how it would take years to catchup/break even.

On that note, I meant to also ask about the government and raising interest rates. They’re talking about 3-4 rate hikes this year. Does this have anything (effect) on the fixed rate for I Bonds or is that apples and oranges? I know it’s not a total direct relationship, but does it lean towards the fixed rate going up for I Bonds? Thanks again.

Short-term rate hikes probably won’t have any direct effect on the I Bond’s fixed rate, but keep an eye on the 10-year nominal Treasury. As of today it is yielding around 1.88%, if it climbs to about 2.5%, that could bring 10-year real yields to close to zero. The 10-year real yield will need to be maybe 0.25% or higher before we see any increase in the I Bond’s fixed rate. In November? Possibly.

How are the bonds affected in those years when the inflation rate was negative?