Let’s take a deep dive into the language of TIPS.

By David Enna, updated June 14, 2026

Also see: Q&A on TIPS

Treasury Inflation-Protected Securities are a complicated investment, and it’s hard to find plain-language explanations. I have a Q&A on TIPS that answers many questions, but I thought it would be helpful to discuss, in detail, the complex language of TIPS. If you understand the language, you will better understand TIPS.

Par value

Par value is the bedrock of a TIPS investment. At some point, when you buy a TIPS at auction or on the secondary market, you will enter a dollar amount in a box. The dollar amount you enter is the par value of the TIPS you are purchasing.

Par value, almost always, is not what you will actually pay for that TIPS. The actual cost will be determined by a combination of factors, but par value is 1) the amount the Treasury guarantees will be returned to you at maturity, no matter what happens with inflation, and 2) the base amount you will use to determine the current accrued value of your TIPS.

Coupon rate

After the initial auction of a TIPS, the Treasury sets its coupon rate at the 1/8th-percentage-point increment below the auctioned real yield. (All coupon rates are set at 1/8th percentage points … 0.125%, 0.250%, 0.375%, etc. If the TIPS auctions with a negative real yield, it gets a coupon rate of 0.125%, the lowest the Treasury will go for a TIPS.)

For example, at the July 21, 2022, auction of a new 10-year TIPS, the auctioned real yield was 0.630% and the coupon rate was set at 0.625%.

The coupon rate remains the same until that TIPS matures, even if the real yield to maturity rises or falls in the future. For example, that July TIPS later reopened in November with a a real yield of 1.485%, but its coupon rate remained at 0.625%.

The coupon interest on a TIPS is paid out semi-annually, every six months. It is not reinvested. But while the coupon rate remains the same, the amount actually paid will rise (or possibly fall) to match the accrued principal of the TIPS.

Real yield to maturity

What is it? It is the total return your TIPS investment will earn above (or below) official U.S. inflation for the term of the TIPS. The term “real yield” means “yield above inflation.” Other Treasury issues and bank CDs have a defined “nominal” yield, but investors can’t know the future real yield. TIPS have a defined real yield, but investors can’t know the future nominal yield. It all depends on future inflation.

The real yield of any TIPS is constantly changing, based on market sentiment. But the important factor is: When you buy a TIPS you plan to hold to maturity, you have set in stone your real yield to maturity. The market may reprice that TIPS, but your real yield doesn’t change, unless you sell before maturity.

A key thing to remember about the real yield: After you purchase a TIPS, and pay a premium or discount to par value to create the real yield to maturity, this is what you will earn going forward:

Inflation accruals + coupon rate

In other words, your real yield was set by the price you paid. After that, you earn the rate of inflation + future coupon payments based on adjusted principal.

Pricing of a TIPS

How is the price of a TIPS determined? At the original auction, investors bid based on the desired real yield to maturity, because at that point there is no set coupon rate. At a reopening auction or on the secondary market, investors know the coupon rate, so bidding is based on how much the real yield will vary from that coupon rate.

You will see TIPS prices based on a factor of 100 (no $ sign), and that is how much you will pay for $100 of the TIPS’ current value (par value + inflation accruals). If the coupon rate is below the market real yield, then the price of the TIPS will be lower than 100, such as 99.85. If the coupon rate is higher than the market, the price of the TIPS will be higher than 100, such as 100.15. Here’s an example of how that worked for the 10-year TIPS issued in July 2022:

Originating auction. Even at an original auction, the TIPS price is unlikely to be exactly 100. That’s because: 1) the coupon rate will be slightly below the auctioned real yield (when the real yield is above 0.125%), and that will slightly lower the price you pay, and 2) even a new TIPS will have some inflation and interest accruals. A new TIPS is issued on the 15th of the month, but the settlement date is on the last business day of the month. So an investor is getting about 15 days of accrued inflation and interest.

Take the July 2022 10-year TIPS as an example:

The auctioned real yield, called “high yield” in this chart, was 0.630%, so the Treasury set the coupon rate at 0.625%. That set the unadjusted price for par value at about 99.951. But then you have to calculate in the fact that this TIPS would have an inflation index of 1.00495 on the settlement date of July 29, plus it would earn a few cents of interest in those 14 days.

- $100 par value x .99951 unadjusted price = $99.952

- $99.952 x inflation index of 1.00495 = $100.446 adjusted price

- Plus the investor would prepay for about 2 cents of accrued interest.

Reopening auction. Now let’s quickly look at the result of the 10-year TIPS reopening auction on Nov. 17 for this same TIPS, CUSIP 91282CEZ0. Over the four months from the originating auction, real yields soared higher, so the pricing was quite different.

Note that the coupon rate remained at 0.625%, set by the original auction. But the auction resulted in a much higher real yield to maturity, 1.485%. And because of that, the price paid by investors was deeply discounted.

- $100 par value x .92312 unadjusted price = $92.3126

- $92.3126 x inflation index of 1.02147 = $94.2946 adjusted price

- Plus the investor prepaid for about 23 cents of accrued interest

The key factor here is that the real yield to maturity was created by market demand, and because the real yield was higher than the coupon rate, the price of the TIPS was lower. When you buy a TIPS, whether at an opening or reopening auction or on the secondary market, the real yield to maturity is the key factor to consider. If you hold to maturity, it sets your future return over U.S. inflation.

Non-competitive bidders — that’s all of us — at both new and reopened TIPS automatically get the high yield. Big-money investors make competitive bids, which could be rejected. All winning competitive bids also get the high yield.

Accrued interest. As a side note, you pay for the accrued interest after the sale closes, but this money is not added to the principal of the TIPS. You will get that money back at the next coupon payment; in the case of this July 2022 TIPS, on January 15, 2023.

Inflation accruals

Inflation accruals for TIPS are based on non-seasonally adjusted inflation from two months earlier. The Treasury takes that inflation number and creates an inflation index that changes every day, up or down depending on if inflation was positive or negative two months earlier. For example, non-seasonally adjusted inflation rose 0.41% in October 2022, so TIPS inflation accruals in December are rising 0.41.%. In November, non-seasonal inflation dropped 0.10%, so inflation accruals will decline 0.1% in January.

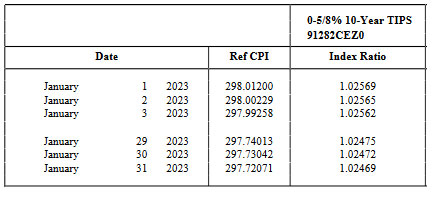

Each month, on the day the U.S. inflation report is released, the Treasury issues new inflation index ratios for all TIPS for the month two months ahead of the report. Here is the full list of January inflation indexes, based on November inflation. And here is how those numbers look for the TIPS issued in July, CUSIP 91282CEZ0:

In that chart, note that the index ratio for Jan. 1 is 1.02569 and through the month will decline to 1.02469 on Jan. 31 because November was a slightly deflationary month. These inflation indexes are crucial because they set the base principal amount for all TIPS, every single day. That means if you sell a TIPS on the secondary market, you will get the full value of your earned inflation.

Accrued principal value

TIPS have a “market value” — set by the market based on constantly changing real yields to maturity, but also a “current principal value,” which ignores the market shifts and simply measures the current total of par value + inflation accruals. If you are holding to maturity, you can simply track the current accrued principal value with this equation:

Par value x inflation index = Accrued principal

If you bought $10,000 par value of a TIPS and it currently has an inflation index of 1.05672, that TIPS now has $10,567.20 of accrued principal. That number is important because it is the base for the next coupon payment. As it rises, the coupon payment also rises.

At maturity, any TIPS will pay par value x inflation index, along with one final coupon payment. It’s not complicated if you hold to maturity.

Current market value

The accrued principal value is one factor used to determine the current market value of a TIPS on the secondary market. As market real yields rise and fall, the price of the TIPS rises and falls. So the price could be 90 for $100 of value, or 110 for $100 of value, depending on how much the coupon rate varies from the market-set real yield.

Secondary market purchase. When you purchase a secondary-market TIPS at a brokerage, you will be putting a dollar amount in a box, just like at TreasuryDirect. But that is not what you will pay. It is the par value you are purchasing. Your actual purchase would look something like this for a TIPS with a price of $95 and an inflation accrual of 1.15:

- You place an order for $10,000 par value

- Principal you are purchasing: $10,0000 x 1.15 = $11,500 accrued value

- Your cost: $11,500 x .95 = $10,925

- Plus some small amount of accrued interest.

- And in some cases, a brokerage commission.

So, in this simplified example, you’d be paying $10,925 for $11,500 of principal. From that moment on, until maturity, you’d be earning inflation + coupon payments. You accepted a below-market coupon rate, but were rewarded with a price discount. It all balances out. Par value is $10,000, so even if severe deflation strikes, you are guaranteed to receive at least $10,000 at maturity, along with coupon payments along the way.

As you go through the brokerage purchase process, you may see “yield to worst” listed as the yield. That is the real yield to maturity. This “worst” terminology refers to callable bonds, but TIPS aren’t callable and the worst yield is the actual real yield to maturity.

Inflation breakeven rate

This is a measure of market sentiment toward future inflation. It is calculated by subtracting the real yield of a TIPS from the nominal yield of a Treasury of the same term. For example, at the Dec. 20 market close, the 10-year inflation breakeven rate was 2.24%, based on Treasury estimates.

- 10-year Treasury note was yielding 3.69%

- 10-year TIPS had a real yield of 1.45%

- 3.69% – 1.45% = 2.24%

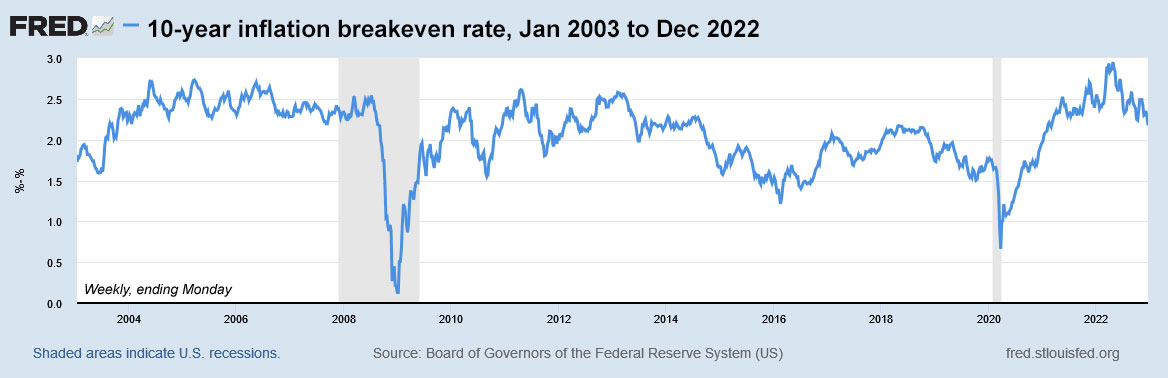

Keep in mind that the inflation breakeven rate isn’t a great predictor of future inflation. It just measures market sentiment. Here is the trend in the 10-year inflation breakeven rate from 2003 to 2022. Look at the 2012 to 2018 era. Do you see any prediction or even hint of our current surge to 40-year-high inflation, topping 7% a year over the last two years?

The inflation breakeven rate is a useful tool, however, because it shows how “expensive” TIPS are versus a nominal Treasury. The lower the inflation breakeven rate, the cheaper the relative cost of a TIPS. Right now, with the 10-year at 2.24%, we are at the border of expensive, but the inflation trend has dramatically changed in the last two years. TIPS look attractive, in my opinion.

Deep dive: Real yield calculation

This section is for numbers nerds. It’s OK to skip this and just rely on the Treasury reporting.

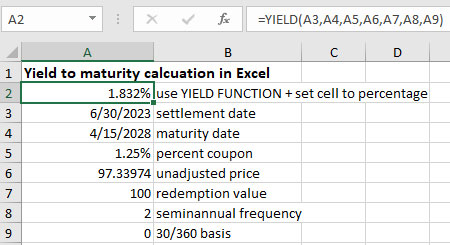

Several readers have asked how to do a calculation to check the real yield to maturity that is reported by the Treasury or brokerage. I will admit I always just trust their reporting, but a reader came up with the answer, using Excel’s YIELD function:

The real yield (“High Yield” in Treasury Auction Results) is a classic Yield To Maturity calculation using the issue date, maturity date, coupon rate, coupon frequency, unadjusted price and face value of the bond. It also is based on the day count assumption of a 30/360. If you wish to replicate the computation the easiest way is to use the YIELD function in excel. For this auction it would look like this, YIELD(6/30/2023,4/15/2028,1.25%,97.339740, 100,2,0). YTM is found by finding the rate necessary in the basic bond value equation so that the discounted future coupon payments and bond face amount equals the price paid for the bond. This is done by iterations using different rates until you find the correct value. Best to let a computer do it for you!

So, using Excel’s YIELD function, this is how you can set up the formula and find the result (this example shows a reopened TIPS auction on June 22, 2023):

Final thoughts

I know that TIPS are an esoteric and confusing investment. I was at a party the other night and a friend told me, “I have TIPS in my portfolio but I have no idea how they work.” Yeah, I hear you. Things get less complicated if you invest in individual TIPS and hold to maturity, ignoring market swings. Then you can track current value with a simple Excel spreadsheet: Par value x inflation index.

I am sure I didn’t get close to answering all the possible questions or solving all the mysteries. I’ve been writing about TIPS for more than a decade and I still come across new concepts. It’s a learning process and I hope this article helps. If you did find this article helpful, please share it with friends who are new to investing in TIPS.

• Confused by TIPS? Read my Q&A on TIPS

• TIPS on the secondary market: Things to consider

• Upcoming schedule of TIPS auctions

• TIPS investor: Don’t over-think the threat of deflation

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

* * *

Follow Tipswatch on Twitter for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Sill question. I have TIP cusip 912810fs2 10,000 maturing 1-15-2026. Vanguard sent me a notice saying “your bond will be redeemed for $10,000. Now I’m pretty sure TIPs don’t require that level of “pay attention” where if I sell today I get 16K but if I wait a week for it to mature, I’ll get 10K. But this will be the FIRST time one matures at Vanguard so I’m just making sure. I get that the 10K is the only part that’s “guaranteed” and the 6K is market value adjustment on inflation. I just want to be sure this isn’t like an “option” where if I forget to redeem before the date, I receive less. Thanks and sorry if this is profoundly “newbie” question.

912810FS2 is a 20-year TIPS issued in January 2006. It will have an inflation index of 1.63714 on Jan. 15, so you will be getting $16,371.40 at maturity, plus one final coupon payment. Vanguard seems to be telling you the par value ($10,000) but the message was needlessly confusing. That would be OK for a nominal bond maturing at par value, but not a TIPS. So you were rightfully confused.

THANK YOU! I all but knew “all was well” but I’m hardwired for worry!

I can confirm that Vanguard incorrectly tells you that payout is par value rather than actual payout.

Thanks again for the extra confirmation.

New subscriber — thank you for this great blog. I can’t seem to comment directly on the blog despite being logged in, so I apologize for hijacking this thread.

For the calculation of accrued interest, it is not 30/360, but rather, actual/actual (since these are Treasuries).

Day count is hideous, but effectively the accrued interest in this analysis is from 4/15/2023 to 6/30/2023 (which is 76 days) — you can prove this in Excel by typing in both dates and taking the difference.

You then have to divide the 76 by the actual number of days in the full coupon period from 4/15/2023 to 10/15/2023, which is 183 days (again, do it in Excel).

Then, 76/183 x .0125/2 x $1,000 = accrued interest per thousand (you divide the 1.25 by 2 since the period is semiannual) and get $2.59563 per $1000 which matches the above. If you use 30/360, you will get the wrong answer although it will of course be close.

Yay! The reader’s description of YTM is sort of odd also, but the yield calculation he/she provides is indeed correct.

Thank you for sharing your expertise. Very helpful.

I have a question about reinvesting TIPS. Treasury Direct says I can’t reinvest TIPS, but when I purchase a TIPS there is a place for me to schedule a reinvestment. Currently two of my shorter duration TIPS are scheduled for reinvestment. So which is true? Can I reinvest or not? And if I CAN, how much will be reinvested?

I have never seen a way to reinvest TIPS on TreasuryDirect. (But I stopped buying TIPS on TreasuryDirect about 10 years ago.)

Hi David, I’m constantly thinking “oh, now I think I fully understand TIPS” followed soon after by noticing something that I can’t get my head around. Please help with this one. I recently purchased some TIPS maturing on the 2040 – 2045 range. One of them (CUSIP 912810RL4) was purchased just slightly above par value – let’s use round numbers – say I bought $1000 for $1010. But the inflation factor is currently 1.36829 which gives a projected maturity in 2045 of $1368. I realize it has a low coupon (0.75%) but still, why would the market price be so much lower than the accumulated principal? I’m obviously missing something fundamental about TIPS or maybe just being stupid.

The current market real yield is around 2.5%, but you will — from now on — earn only 0.75%. So … big discount at purchase.

So I think you’re saying what I had originally thought … that this is a reflection of the coupon being low and so short term return is low. I guess it’s hard to wrap my head around the fact that the likely maturity value (assuming somewhat normal increases in factor over the next 20 years) is discounted so heavily. The mantra of “hold TIPS to maturity” is then true more so than ever when coupon rates are low and the time to maturity is long. Personally, I wish all TIPS had super low coupons but I realize others are not in the same boat.

Hello David,

I have noticed a small anomaly in my TIPS purchases, and I wonder if you might have an idea about what is going on. I have made three TIPS purchases this year through TreasuryDirect. In my TreasuryDirect account, if I go into the Security History for any of my TIPSs, and look at the details of the “Security Issued” transaction, everything looks as expected until I get down to the item labeled “Accrued Inflation Compensation”. This item, I would think, would be the amount of the inflation accrual as of the issue date of the TIPS, but that isn’t exactly what TreasuryDirect shows there. To take the most recent example, I purchased $2000 par value of the 10-year TIPS issued on July 31, 2025, and I expected that the inflation-adjusted principal on the issue date should be $2000 * 1.00108 = $2002.16, for an inflation accrual of $2.16. But TreasuryDirect shows $2.14 here, and the purchase discount is also reduced by the same amount, showing $19.80 instead of $19.82. There are similar discrepancies of different amounts in each of my other TIPS purchases (In each case, the numbers are less than expected).

Have other folks observed this kind of discrepancy? Is there an explanation for it? Does “Accrued Inflation Compensation” mean something different than what I think it means? It is hard to believe that TreasuryDirect would have made a mistake on this, so I think I have to assume it is intentional.

These discrepancies probably aren’t going to make a huge difference for me. The sum of the discrepancies for my three TIPSs is less than $1, and I think it basically just means that amount will be counted as an inflation accrual (when the correct inflation index is applied at the end of the year) instead of as a purchase discount, so it may be taxed differently. For such a small amount it probably won’t make much difference, although I imagine if one were to purchase a lot more TIPSs, then it could become more substantial. For now, I just want to understand what they are doing, and why they are doing that instead of the expected ([Inflation index] – 1) * [Par value].

For what it’s worth, I worked out a formula that gives me the numbers they have for “Accrued Inflation Compensation” in each of my TIPSs. It seems to be something like this:

(1-(N/X)) * (I-1)*P

where I=inflation index as of issue date, P=par value, N=number of years between issue date and maturity date, and X is a number between 1163 and 1175. Obviously, this is unlikely to be the formula that TreasuryDirect actually uses, but if I use this and round the results to the nearest cent, it works for my small set of data points. I don’t have a good idea of what the number X might represent. My guess is that it isn’t meaningful on its own but may arise from a combination of other parts of the calculation they use.

I have to admit that I almost never look at TreasuryDirect calculations for TIPS principal balances and accruals. One oddity there is that TD only posts the inflation-adjusted value as of the date of the last coupon payment. So for a TIPS issued in February, the inflation adjusted value is current from Feb 15. That isn’t a great help. When you go to the “Current Holdings > Summary” page you should see par value listed in the right-hand column. Does that par value number look correct. For example, for a $2,000 par value purchase, does it show $2,000? And when you go to the “Current Holdings > Detail” page you should see the correct inflation accrual as of the date of the last coupon payment. That’s all TD will show you.

I don’t think I have ever used the “History > Security History” page. I haven’t bought a TIPS at TD in 7+ years. When I look at details for the last one I bought in April 2018 TD shows the correct par amount, and that is it. So I am can’t duplicate what you are seeing.

But it looks like you are getting to “Security History > Detail” through the text link on the Current Holdings page. That page will show par value and also the purchase price, which reflects the discount or premium you paid. That page, I think, is simply showing details of the purchase transaction. The accrued inflation shown therefore would be based on the July 31 settlement date, not the current date. Hope this helps.

When you went to “Security history > Detail” for your 2018 TIPS, were you in the “Security issued” transaction? When I go to “Security history” I see two transactions. One is “Purchase requested” and the other is “Security issued”. “Purchase requested” does indeed show only the par amount, but “Security issued” has the other details I’m talking about (at least in my account — But maybe since 2018 they have changed the details they display.)

Anyway, yes, I see the correct par values, correct amounts for purchase price, accrued interest, etc. Only one TIPS has received a coupon payment so far, and that one shows the correct inflation-adjusted principal for the date of the coupon payment. The only things that seem off are in the details for the “Security issued” transaction, the “Accrued inflation compensation” and the “Discount” are both a little less than it seems they should be.

In your article announcing the auction results, where you said, “In summary, an investor purchasing $10,000 of this TIPS at today’s auction paid $9.911.68 for $10,010.80 of principal as of the July 31 settlement,” this is as if they are saying you only received $10,010.70 of principal. Not a big difference, obviously. I probably shouldn’t worry about it, but I guess I’m a little weird about wanting to understand things.

OK, I think I figured out what they’re doing. What TreasuryDirect is calling the “Discount” is actually the unadjusted discount, the discount as it would be before multiplying by the inflation index. In other words, par value minus the unadjusted price. And then they apparently are changing the inflation accrual by the same amount to get what they are calling “Accrued inflation compensation”. This explains all of the discrepancies I see in the numbers. I’m still pondering why it would make sense to do this.

Hi David (or anybody else who can answer),

I’m really confused about something with the secondary market. Specifically regarding bid/ask prices and accrued inflation in the principle. For example, looking at the WSJ TIPS page, I see one 20 year TIPS maturing next January:

CUSIP: 912810FS2

Maturity: 2026 Jan 15

Coupon: 2.000

Bid: 100.3

Asked: 100.3

Yield: 0.665

Accrued principal: 1607

So, am I really to believe that I can buy ones of these TIPS for just $100.30 today, and that — barring some catastrophic deflationary event — next January I will be paid ~$160? If so, I’m backing up the truck.

Thanks,

David

If only that were true! But it is not. If you were to buy this TIPS today you would be purchasing 60%+ extra principal and paying a premium price. You would pay upfront for the principal you will be receiving back in January 2026. In other words, at prices right now, you would be paying about $16,217 for $10,000 in par value.

Hi David,

Although I have invested in TIPS for years, I really am not familiar with the secondary market and am still researching it. I notice that in the secondary market many issues with a very low coupon are selling at a discount, which, of course, makes sense. What I am curious about is if inflation is higher than expected, would I do better than an equivalent bond (at a higher coupon rate) selling near par, given that the inflation adjustment would be based upon the principal amount, which would be much higher than my discounted price.

No, because you are buying a certain amount of principal at a discounted price. The coupon payments aren’t based on what you paid. They are based on the amount of principal. After the purchase is completed, focus on the amount of principal.

Thanks for all this info! I just managed to use the “free” online version of Excel to compare the rates of two TIPS purchases I made this week. If I can refind my tiny saved spreadsheet, may use again in the future. If I get really obsessed, might buy the program…

Hi David,

Thanks for all the information you provide on this site. Last year, I purchased TIPS on the secondary market through Fidelity. To be honest, I’m somewhat disappointed at how little interest they are paying out every 6 months compared to what I invested (due to low coupon rate.) I understand that over time, due to inflation, both the semiannual interest payments as well as the value of the principle should increase – resulting in higher interest payments near the end of the term and a large payout of inflation-adjusted principle when the bonds mature. Nominal treasuries, on the other hand, pay a constant amount of interest over the life of the bond and at maturity you get back the principle you paid. This has me wondering, when comparing TIPS to nominals (using the inflation break even point, for example), do analysts simply look at the total amount of money you get back over the life of the bond (sum of all interest payments and return of principle)? Or do they take into account that with nominals you evidently get more of the money sooner compared to TIPS? With TIPS it seems like more or most of your return comes later in the life of the bond. Obviously, due to the time value of money, the sooner you get your money, the more it is worth.

I’m sure Tips Guy will provide a much more succinct answer but I did want to throw my two cents in. Let’s say you want a 10 year tip. You could be buying literally a 10 year that was issue late last year at a higher rate of interest, OR you could be buying an 11, 15, even 20 year TIP with a super low coupon rate. So ALL OF THEM will give you the same return (assuming no deflation) but the one you buy with near nil interest coupon is sorta kinda going to act like a “zero coupon” bond. (Not EXACTLY, because you’ll get SOME interest but the bulk will come from ‘appreciation’ in the form of inflation factor… Tips Guy, I know this isn’t technically on spot but am I on the right track?

Thanks kennethlavoie, but that doesn’t really answer my question. For example, a one-year bond that pays $10 interest every month is a better investment than a one-year zero coupon bond that pays $120 interest at maturity. Even though both pay $120, the sooner you get your money, the more it is worth. My question is, is this difference taken into account when comparing TIPS with nominal treasuries? Or does the analysis just taken into account how much money you get back regardless of when it is received? I don’t really see how they could accurately estimate the time value of money when comparing TIPS with nominals.

Sal, I disagree, naturally. When you buy a longer-term TIPS with a good coupon rate (let’s day 2.0%), the principal value of your par-value investment is continuously growing with inflation until maturity. So as inflation rises, your coupon payment rises. BUT … the bigger deal is that your principal continues to grow with inflation, so at maturity you get par value x inflation index, and you collected 2% on your principal in immediate payments. That’s how a TIPS works, and the reason it is different from a nominal Treasury is that your end result is going to be adjusted for inflation. Buy $10,000 today and in xx years you are going to get a return of $10,000 + accrued inflation. That certainty is what TIPS investors are looking for. Plus, you earned interest of 2.0% paid out each year on the rising principal. The TIPS is pointed at an “end result.”

Nominal Treasurys are fine, too. I have no problem with them. You invest $10,000 and in xx years you get $10,000, plus the interest earned along the way. The principal is always $10,000, so the annual interest payment is always the same. And then it all depends on how well you can reinvest that interest. The nominal Treasury is pointed at “current interest.”

If you think the nominal Treasury’s interest rate will beat the rate of inflation + the real yield of a TIPS, buy the nominal Treasury. If you think it won’t, buy the TIPS.

David, how can you disagree with a question? I simply asked: when comparing the return of a TIPS with a nominal Treasury (for example, when calculating the inflation break-even point) does the analysis consider only how much you invested and the total amount you get back over the term of the bond? Or does it also take into account when you receive the money? As an oversimplified example, if you bought a one-year nominal for $1000, get $5 per month back for 12 months, and then also get your $1000 back when the bond matures (total profit of $60 in 1 year) would that be considered equivalent to buying a one-year TIPS for $1000, getting no monthly payments, and then receiving $1,060 when the bond matures (total profit of $60 in one year)? Thanks!

I’m guessing this question has been asked and answered but I haven’t been able to locate it here, so I’ll ask away! “What do you think of a strategy for buying secondary TIPs, whereby you focus on the LOWEST coupon rate, so that there is less reinvestment risk. My limited but growing grasp tells me that LOW coupon TIPs, longer dated “sorta kinda” act like zero coupon bonds in that most of the return comes from the inflation factor and appreciation that (already) happened due to the difference between current coupon rates and the lower existing rate on the bond in question. I know this puts some of the principal at risk for deflation (I’d love to see some examples of that…I’m still a little gray on that risk). But I don’t want to digress from the core question: Does favoring lower coupon rate on secondary market purchases help to mitigate reinvestment risk?

Buying a longer-term TIPS with a very low coupon rate means you will be buying additional principal (from years of inflation) at a discounted price. So you could end up with a price around par value and par value is protected against deflation. So the strategy seems fine. For example, the TIPS that matures Feb 2043 has a coupon rate of 0.625% and an ask price around 73.99. The inflation factor is 1.33796. Buying $10,000 of that TIPS would cost you around $9,902. Real yield of 2.306%.

Silly question…if I buy a 10K face value TIPs secondary market, and the cost is around 15K, I know 5K of that is inflation accrual which is NOT protect from DEFLATION…but will my return on that 15K be what I think it will be? (i.e. if I’m thinking I’m getting 2% real yield, is that on the whole 15K? I just want to be sure I’m not doing anything silly. I’ve got quite a collection of TIPs in the past 6 months, but some of them were like 12K-15K for 10,000 face value.

Kenneth, if you buy $10,000 par value of a TIPS and the cost was $15,000 and the real yield to maturity was 2%, then you are going to earn a real yield of 2% on whatever the accrued inflation is at the date of purchase. It might be $15,000, or close to it. If deflation sets in, you’d still earn 2% above inflation, but the accrued principal would be declining.

Great info! I’m having trouble deriving unadjusted and adjusted price that matches the auction data below:

Term and Type of Security 5-Year TIPS

CUSIP Number 91282CJH5

Series AE-2028

Interest Rate 2-3/8%

High Yield 2.440%

Adjusted Price 99.921449

Unadjusted Price 99.697130

Adjusted Accrued Interest per $1,000 $1.04059

Unadjusted Accrued Interest per $1,000 $1.03825

TIIN Conversion Factor per $1,000 3 3.876995265

Index Ratio 1.00225

Issue Date October 31, 2023

Maturity Date October 15, 2028

Original Issue Date October 31, 2023

Dated Date October 15, 2023

Using your simple math for Unadjusted Price:

Unadjusted Price is Par Value * (1- Difference of High Yield and Coupon Rate)

Unadjusted Price = 100 * (1 – (.0244-.02375)) = $99.935

This compares to $99.697130 from the auction data

Also, why is the published adjusted price lower than the unadjusted price if the index ratio is above 1 (posted in notes at 1.0025)? I’m getting an adjusted price of $100.1598538 = ($99.935 * 1.0025)?

Not sure what you are calculating, but the adjusted price (99.921449) was higher than the unadjusted price (99.697130). In my article on that auction I looked at a hypothetical $10,000 investment: https://tipswatch.com/2023/10/19/new-5-year-tips-gets-a-real-yield-of-2-440-a-bit-lower-than-expected/

Par value: $10,000

Inflation index on settlement date: 1.00225

Adjusted principal: $10,022.50

Unadjusted price: 0.99697130

Investment cost (adjusted principal x unadjusted price): $9,992.15

Plus, accrued interest: $10.41 (will be returned at first coupon payment)

Total cost: $10,002.56

Hi,

Is there a website which lists all the Inflation-Adjusted Price for the TIPs. For CUSIP 91282CDC2 issue date 10/152021, my brokerage company shows Inflation-Adjusted Price of $104.138

The inflation rate has been over 6.5 during the last two years but the inflation adjusted price reflects 2% annual rate. Please explain this anomaly.

Thank you.

Pricing of TIPS is a little more involved than that. The figure you cite from your brokerage is probably for a specific amount of that TIPS par value being offered on the secondary market at a particular moment in time – and perhaps through that particular brokerage?

The section above on Current Market Value delves into explaining how that part of the TIPS comes about. Basically because that TIPS has a coupon of only 0.125%, it has to be offered at something below par value to make it a competitive offer with current real yields. But that offering price also get modified by the current inflation index of that TIPS.

The current inflation index for any given TIPS can be found at https://www.treasurydirect.gov/auctions/announcements-data-results/tips-cpi-data/ and the Index Ratio for that particular TIPS as of today is 1.22623. So inflation has increased more than 22% from its date of issue through today and the TIPS has been affected accordingly.

My mistake on the inflation accrual. David’s right. My source should have read 1.12263 if I’d read it correctly.

Your brokerage will show you the current “market value” of your TIPS, which reflects both the inflation accrual and market-value discount or premium based on the coupon rate versus current market real yields. One easy way to find inflation accruals for TIPS is to check the daily Wall Street Journal listing: https://www.wsj.com/market-data/bonds/tips. That TIPS, which matures Oct 15 2026, has a current inflation index of 1122 (which means 1.122 times par value). So if you bought $1,000 par value, you now have $1,122 in accrued principal. But the market value is lower because the coupon rate is well below the current market yields. If you are holding to maturity, the only thing that matters is par value x inflation index.

Is it an anomaly that the most recently issued 5-year TIPS (2-3/8% Oct 2028) is not listed on that WSJ page?

It should be there since this TIPS is now trading. I am seeing it an Vanguard with an ask price of 100.96 and a real yield of about 2.16%.

Hi David,

I am missing one thing in your comprehensive review. How does the coupon rate affect the par value of a newly issued TIPS? In your example of a new 10 year TIPS offered in July of 2022, I see that the interest rate is 0.625%, but the PAR value is $99.951. I am not understanding how you derive the par value using the coupon rate.

Thanks much!

Lon

The par value is equal to the amount of TIPS you purchased, and is 100 through maturity. At maturity you get par value x inflation index. In that July 2022 example, the par value was 100 and the unadjusted price was $99.952. The unadjusted price was lower because the coupon rate was set at 0.625%, but the high yield was 0.630%, so the TIPS was sold at a slight discount. The coupon rate doesn’t affect the par value. It affects the market value, which will fluctuate as market yields rise above or below the coupon rate.

Thanks for the quick response! It sounds then like the par value, 99.952 in the example, derives from the difference between the coupon rate and the market? So…there is no way to calculate the par value, but that it should be close to 100? I tried subtracting 0.625 from 100, but I guess that’s not it.

Lon, I repeat that par value is 100. The 99.952 is the market value, which adjusts for the fact that the auctioned-determined real yield was slightly higher than the coupon rate of 0.625%. This was an originating auction. Treasury always sets the coupon rate at the 1/8th percentage point below the high yield. Par value was 100. Multiply that by unadjusted price (market value) of .9952 to reach the $99.52 unadjusted cost of the investment.

Very informative information. Would you or someone be aware of the tax consequences for the various scenarios? That is, I have a significant amount of tax losses that will never be able to all be used in my lifetime. Therefore, I was wondering if any scenario that you have discussed, incur capital gains rather than interest/dividends?

Surely I’m overlooking it, but is there a resource that shows the overall yield performance of matured TIPS bonds? A 5 year TIPS bond I purchased at auction just expired – 9128284H0 – https://www.treasurydirect.gov/auctions/announcements-data-results/tips-cpi-data/tips-cpi-detail/?cusip=9128284H0. I downloaded the CSV and calculated the interest earned (0.00625/2 times the principal times the inflation factor at the time of the interest payment) – because that was easier than finding the interest payments in Fidelity’s site!!! My calculation yielded a 4.42% yield over the 5 years; this does not compound the interest earned.

Comparing to other performance – STIP (~2.5 yr avg maturity) 5 year performance as of 3/31/23 was 3.01% and TIP (~7 yr avg maturity) was 2.75%. 5 year Treasury note yield was ~2.7% in April 2018.

Anyway, it seems that there should be a resource that shows the historical and even the yield to date of TIPS bonds. Fidelity’s site is very confusing because it adjusts the cost basis of purchased bonds with the current inflation factor – I cannot find an apparent way to benchmark individual TIPS performance.

Eyebonds.info has information on every TIPS ever issued: http://eyebonds.info/tips/index.html This is the info for the TIPS that just matured: http://eyebonds.info/tips/hist/tips69hista.html … which earned 20.5% in inflation accruals on top of the coupon rate of 0.625%. This site shows a yield to maturity of 4.42%, same as your calculation.

Thank you for this excellent website. My question has to do with the ‘dreaded’ OID. I bought the 5 year TIP at auction issued Oct 22, 2022 and keep it in my US Treasury Direct personal taxable account. When I go to the Security Details for this TIP in my UST account, it states a Discount that is

Discount = Par – price paid + accrued interest – accrued inflation compensation.

That all makes sense to me.

But, my 1099 OID states an amount in Box 8 that is ~20% higher than the Discount stated by the UST in my Security Details. What is driving this discrepancy?

When I look at the current value of one of my TIPS in TreasuryDirect, it shows me the inflation-adjusted value as Oct. 17, 2022 because (I assume) that is the last time that TIPS compounded the inflation accruals. But the 1099-OID will show the full accruals through December 2022. This could be the reason for the differing amounts?

Hi. I think I basically understand the above, but I’m not understanding why the various TIP funds (VTAPX or VTIP for example) paid such a low dividend amount for the first quarter of 2023.

Average dividend payment has been about 30 to 40 cents per share for a few years, but in first quarter of 2023 it dropped to about a penny a share. Looking over the dividend history, I don’t see it ever dropping this low.

I’ve spoken with three different advisors at Vanguard (in three different departments) and none of them have a clue as to why this sudden drop occurred.

They suggest that I write a letter to the fund manager for VTAPX and ask him, but they freely admit that he probably won’t respond to my letter. Since (they also said) I can neither email or call him, my only other alternative would be to drive up to Pennsylvania and try to get an appointment with him or one of his analysts/accountants.

As to why the question matters: People in retirement count on dividend payouts for ongoing living expenses. I thought I could at least count on the weighted average coupon rate amount for that. Apparently that is not the case for TIP funds/ETFs.

It looks like the March dividend for VTAPX is always the smallest of the year. It was only 0.047 in March 2021 and it looks there was no March dividend in 2020 and several other years. I wonder what months of inflation are used to pay that dividend. Looking back to late 2022, we had inflation rates of 0.41% in October, -0.1% in November and -0.31% in December. That works out to flat inflation for three months, but the fund paid a decent dividend in December (0.559). So it could because there is a lag between inflation reports and the dividend payments.

That is a good observation, thanks. Here is corroborating evidence for what you say:

https://www.nasdaq.com/market-activity/etf/vtip/dividend-history

I can’t find it now, but yes, I do remember reading somewhere that the underlying bonds have a few months delay in the CPI calculation for the principal adjustment…but I thought that was the underlying bond, so surely the fund wouldn’t be applying that as well.

I do notice that about one-third of the underlying bonds in VTAPX were bought in January of the various years. (Random buys each quarter would be more like one-fourth from statistical probability.)

At first I thought that Vanguard was using some kind of formula to “smooth” the dividend payments for each quarter…but then that wouldn’t make sense if March is typically zero or near zero, and the rest of the months are relatively high. If there is no smoothing formula from Vanguard, then the formula would just be the government’s, which is published…so we’re back to lack of randomness?

Another thought is that maybe Vanguard is having to sell some pieces of bonds in certain months to savvy investors who sell after taking their cyclical high dividend payment, and that temporarily cuts the dividend for the rest of us who hold the fund for the long-term? but then they make it up in other quarters to get the Vanguard-published yearly dividend rates?

At this point, I have more questions than answers, and the only person whom Vanguard staff says knows the answer is the fund manager (Joshua C. Barrickman), as I discussed above.

Ben, all TIPS issues get a daily inflation adjustment base on inflation two months earlier (this is the only way it could be done, since the inflation report lags by a month, and then the Treasury has to set the inflation adjustment for the next entire month.) The March inflation report will come out April 12 and will set the inflation accruals for May. So it is possible the TIPS funds have another lagging factor on top of that delay.

Ya. Here is the article I read on that subject (confirming what you also say above), i.e. delay in dividend payout due to the CPI calculation months. Notice that this is for TIP ETFs, not the underlying TIP bonds:

Click to access mechanics-of-tips-en-us.pdf

However, this still doesn’t explain why dividends in the first quarter are almost invariably zero or near zero for TIP funds, right?

I would love to get my hands on that formula from Vanguard or Fidelity et al, wouldn’t you?

Ben

Hello,

I purchased CUSIP: 91282CDC2 directly from Treasury Direct at auction on 10-15-2021. At that time I paid a premium to purchase this 5 years TIP (Paid $10,950.93 for $10,000.00 par value).

Today the same TIP is being sold in secondary market on fidelity.com for:

Price (Bid) 95.799

Price (Ask) 95.998

Ask Yield to Worst 1.271%

Ask Yield to Maturity 1.271%

Current Yield 0.130%

Inflation Factor 1.09035

Inflation Adjusted Price 104.671419

Third Party Price 95.834

Inflation Adjusted Third party Price 104.465

Spread to Treasuries -2.433

Treasury Benchmark 3 YR.(1.625% 10/31/2026)

I assume the par value is $100 for the quoted price above. Need to understand:

The difference between Inflation Factor of 1.09035 versus Inflation Adjusted Price of 104.671419. why are they different? Shouldn’t the Inflation Adjusted Price be approximately 109.00?

Inflation Factor of 1.09035., sounds correct as the inflation rate was over approximately 8% in 2022.

Is it a better deal to buy the same TIPS in an IRA at the Ask Price of 95.998, instead of what I paid 109.509.

Would you consider “Yield to Maturity” of 1.27% as the yield above inflation rate?

Thank you

The inflation factor tells you simply the amount of accrued inflation, and 1.09035 means that your $10,000 par purchase now has accrued inflation value of $10,903.50. Multiply that by the price factor (0.95988) and you get a current market value of about $10,466 (which matches the inflation-adjusted price). If you decide to hold to maturity, you can ignore the market value and know you have $10,903.50 in inflation-adjusted value at this point.

Thank you for the explanation. Currently, the above TIPS have $10,903.50 in inflation-adjusted value at this point. With the price factor of 0.95988 I can purchase the same TIPS today for $10,466 (Approx. 4% discount.)

Am I right in saying that today I can buy the same TIPS at discount of 4% with full forward Inflation adjustments to maturity and a low coupon rate of 1/8% (fixed at the auction).

Yes, that sounds right.

I’m looking at 91282CFR7, issued on 10/31/22. The 3/31/23 Index Ratio is 1.00967. So after 5 months the inflation accrual is less than 1%. Seems very low given the inflation environment we’re in. Please help me understand. Thank you.

OK. The index ratio on the settlement date of Oct 31 was 0.99982 based on inflation of -0.04% in August. After that non-seasonally adjusted inflation was 0.22% in September (applied to November), 0.41% in October (applied to December), -0.10% in November (applied to January), -0.31% in December (applied to February) and then 0.80% in January (with 9 days applied to March). Add it up and you only get to 1.00399 on March 9.

I’m sure you’re correct but I was unable to arrive at 1.00399. I started by subtracting .0004 from 1 then multiplying by 1.0022, 10041, .9990 etc.. Obviously I’m off base but I see the monthly adjustments are lower than I expected. Thank you.

I’m still a bit perplexed why two TIPS with similar maturities have such different YTMs. It seems to me like the chance of overall deflation having an impact over a multiyear time frame would be negligible. What is the logic behind the coupon rate having a significant effect? Possible tax implications? I also don’t understand why the premium/discount would really matter (other than the trivial calculation necessary for determining how much/many you want to purchase), when it seems to me like the YTM would be the overriding concern. Thanks for your wonderful site/analysis/explanations!

The yield differences aren’t that great, really. Usually about 10 basis points or less. Today I happened to be looking at TIPS maturing from 2032 to 2033. There are four issues. One of them is 912810FQ6, with a coupon rate of 3.375%, an inflation factor of 1.673, and a buy price of 115.042. That means this TIPS is going for a whopping 92% above par value. The other three are selling at a discount and the yield difference is only about 6 basis points.

Thank you for all your great information!

One clarification on the guaranteed yield to maturity.

I purchased 9128286N5 with the following:

Price: 97.4646

Inflation Factor: 1.18076

Settlement Date: 1/23/2023

Maturity Date: 4/15/2024

YTM at purchase: 2.62%

My question is this: Since I know that the inflation factor on 2/28/2023 will be 1.17692 based on the -0.31% CPI drop in Dec 2022, would not a more accurate YTM be 2.35% factoring in the negative inflation adjustment that I know will happen between the settlement date of my purchase and the end of February?

After that we do not know what the inflation will be so we can assume it will be unchanged till maturity.

YTM is real yield to maturity in this case, but that number is fairly irrelevant to what you will actually earn between now and when this TIPS matures in April 2024. It was based on the discount you paid at purchase. Keep in mind that real yield is the yield above inflation, and if inflation goes down, so does your return. That TIPS has a coupon rate of 0.5%, so from this point forward you are going to earn inflation accruals + 0.25% coupon payments on April 15 and Oct 15, 2023, and the last one one April 15, 2024.

Thank you for your reply.

To clarify: The real yield to maturity of 2.62% assumes that the inflation factor of 1.18076 stays unchanged through maturity, but we already know that this factor will decrease every day through the end of February as this has already been determined, so wouldn’t the inflation factor that is known furthest in the future (in this case Feb 28th) at the time of purchase be a more accurate reflection of real yield to maturity?

I repeat: The real yield is the yield above inflation. Inflation goes down, and your nominal yield goes down, but your real yield remains the same in relation to inflation. Let’s say that you bought $100 of principal. You got it at a 2.54% discount, plus you will earn 0.50% annually. At maturity, you’ll get that $100, plus any inflation accruals (up or down) and 0.50% annual interest. The real yield was set by the discount you paid at purchase. After that, your return is inflation accruals + coupon payments.

Hi David,

Thanks again for a great posting. One thing I don’t understand are the actual mechanics/rules of the auction. What exactly are the “Big Money” actors bidding on? If the real yield, wouldn’t they just bid it up to infinity?

Or is it like a silent auction and there are a fixed & limited number of $100 TIPs available to be sold to the lowest bidders? So if you bid too high — no TIPs for you. If someone made a very large bid at a low rate would that effectively be a shill and tank the auction for everybody else? In this model would there a certain amount set aside for “Big Money” and then non-competitive? Does the re-issue auction just get whatever is left over after the intro auction?

If this is already explained somewhere else in a comprehensible way, please just link to it.

Thanks,

David

Basically, the Treasury sorts all the competitive bids from high to low. It starts accepting the lowest ones and moves up the yield ladder until it fills the auction funding level, which is $17 billion at the Jan. 19 auction. Once it fills its funding need, it sets the high yield and accepts every bid up to that level. All bidders below that point end up getting the high yield. Of course, all non-competitive bidders (like us) also get the high yield. But bidders above that high yield get rejected. There is more to the process, but that is the basic procedure.

Thank you David-Tipswatch for helping me, a CPA, understand the TIPS bidding yield, etc. process. Even though I have been investing in TIPS on & off for decades.

Firstly, thanks for doing such a great service to individual investors. If anyone wants to do a financial blog, TIPS watch should be the template.

I have a question related to pricing of the TIPS in secondary market. I see that the yield to maturity swings wildly for bonds that are very close to each other in maturity date. I see that the higher the accrued principal lower is the yield.

https://www.wsj.com/market-data/bonds/tips?mod=md_bond_view_tips_full

(on Jan 16th 2023)

2032 Apr 15 – with an accrued principal of 1678 – Yield is 1.427%

2032 Jul 15 – with an accrued principal of 1025 – Yield is 1.306%

Surely the the difference in 3 months is not driving the yield difference.

Is the higher amount of principal that is at risk of deflation that is driving the higher yield?

Definitely, if two TIPS have very similar maturities, the one with the higher accrued principal will generally demand a higher real yield to maturity. But in this particular case, you need to also look at the coupon rate. The Apr 15 has a coupon rate of 3.375%, so it has more principal and a PREMIUM price ($116.21). The July 15 TIPS has coupon rate of 0.625%, so it has less principal and a DISCOUNTED price ($93.25).

Great analysis of TIPS! Could you explain the inverse relationship between TIPS real YTM and price. It seems as the YTM increases so too the price.

It is all about the coupon rate of the TIPS, versus the market real yield. If the real yield rises above the coupon rate, then the market price of the TIPS is going to fall below $100. As real yields rise higher, the price of the TIPS falls more. This is why the TIPS funds did so poorly in 2022; the real yield of a typical TIPS rose more than 250 basis points. …. Of course, the reverse is true. If the real yield falls below the coupon rate, then the price of the TIPS rises above $100, and will continue to rise if the real yield falls more.