Tipswatch.com, updated June 10, 2026

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends.

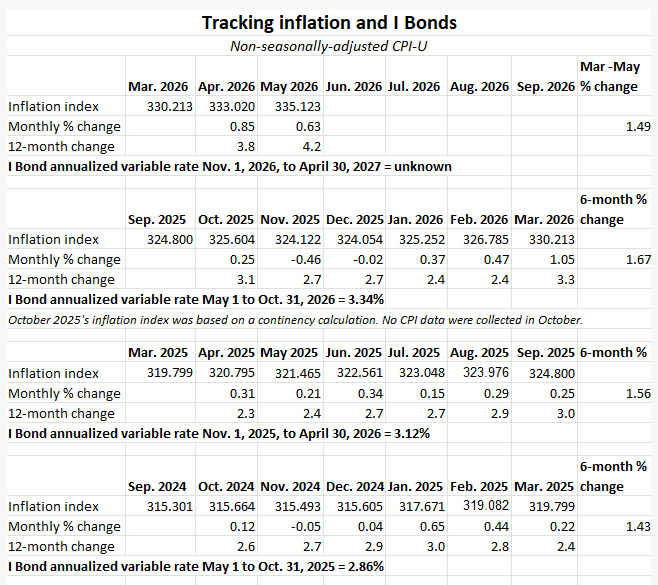

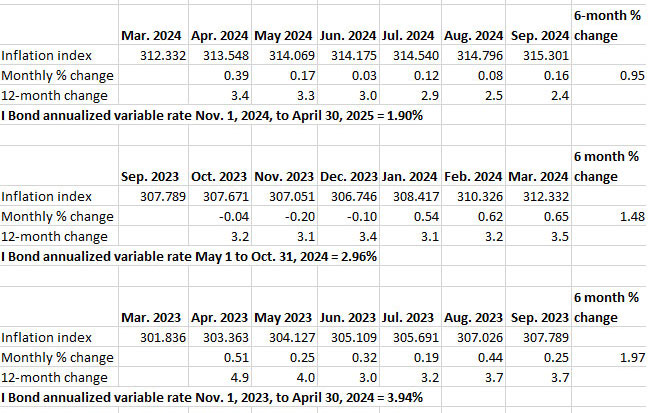

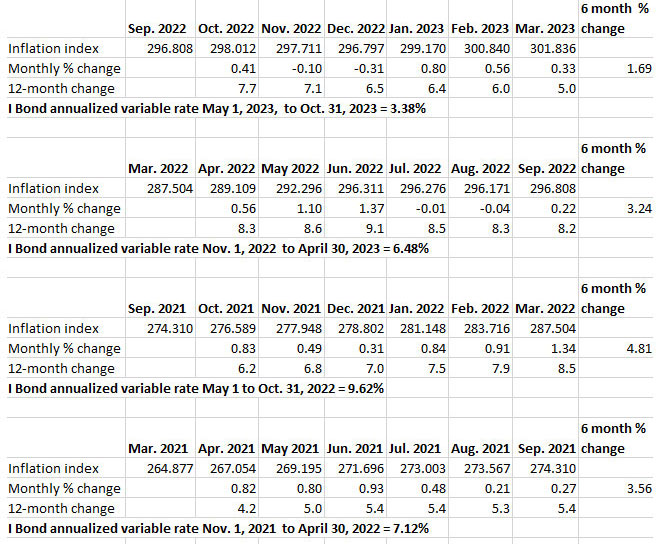

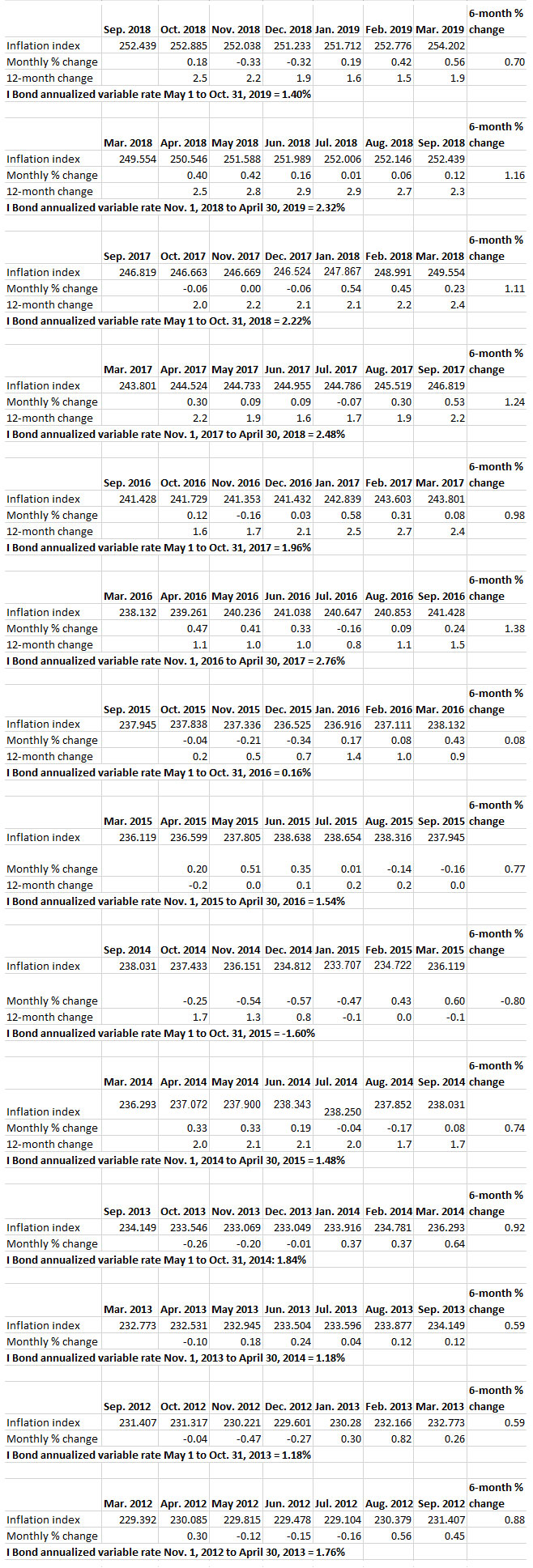

This chart shows monthly and six-month non-seasonally adjusted inflation numbers that the Treasury uses to set the six-month inflation-adjusted interest rate on U.S. Series I Savings Bonds.

The March 2026 inflation report completed the six-month string needed to calculate the I Bond’s new variable rate, reset May 1, 2026. The new rate is 3.34%. Combined with a fixed rate of 0.90%, the I Bond’s composite rate is 4.26% for purchases through October 2026.

All I Bonds, no matter when they were issued, will eventually get the variable rate of 3.34% for six months, with the starting month depending on the original purchase month. Both the permanent fixed rate and inflation rate will be reset again on November 1, 2026.

- May 1, 2026: I Bond fixed rate holds at 0.90%; composite rate rises to 4.26%

- Let’s ‘try’ to clarify how an I Bond’s interest is calculated

- I Bonds: Here’s a simple way to track current value

- Confused by I Bonds? Read my Q&A

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

Pingback: Series I bond rate is 4.26% through October 2026 » Report Via

I just wanted to offer up this free I Bond tracker I developed for anyone who’d like to try it.

https://ibonds.pages.dev/

No login required, ads, or cloud storage of data. Your bond list is stored in browser storage.

Suggestions are welcome.

Pingback: Where is the I Bond’s composite rate heading in November? | Treasury Inflation-Protected Securities

When the fixed rate is 0% an ibond semi annual of 1.015% and then 1.025% (or vice versa) results in less growth than two consecutive periods of 1.02%. My human nature leads to my questioning whether the variable rate adjusting every six months is a good thing for keeping up with inflation, or is it a slightly bad thing as indicated by the simple math? My difficulty is that the semiannual rates will always under deliver vs a year long average of the two semiannual rates. Of course if the adjustable rate was only adjusted yearly, then we could have missed the highest semiannual period, but since there has not been any deflation since May of 2015 I suspect that for the most part the use of semiannual adjustments is not as beneficial for ibond purchasers as would be year long variable rates.

Shouldn’t make any difference. The geometric CAGR will lag the arithmetic average, but the same math applies to the inflation you’re trying to match.

I will be redeeming some of my 0% fixed I-Bonds and buying in November. The fixed rate should rise from 0.9% to > 1.5% for sure. Some where between 1.6-1.9% seems likely. What’s your guess?

I think the fixed rate will rise, but 1.5% might be a reach.

Assuming the rate goes up (or at least stays the same in Nov), then one would be better off waiting to make their $10k annual purchase in Nov, rather than late Oct, correct? And then we could also buy our 2024 annual purchase in late April, grabbing the same fixed rate, correct?

I do believe the fixed rate will rise, but there are no guarantees. I will post an analysis early next week. You are correct that the November fixed rate will continue to April 2024.

Not sure if this is a new question or a reply…but I was wondering if I could gift myself I bonds for future deposit into my account. I realize this would be limited to 10K dollars per year in the future…

Just curious

Earlier in this thread I mentioned that my wife accidentally gifted me I Bonds in excess of the annual 10K per year, last year. Well they were not acted upon and all is good in that respect. Of course, I would not buy more than 5k this year, just in case that was a fluke and I got lucky.

No, you cannot gift I Bonds to yourself. Has to be to a separate person.

Pingback: The Boring Newsletter, 5/13/2023 – Frequently Taxed Questions

This may be a stupid question, but I am curious, in real terms, how well do these *actually* match inflation? I mean in theory you obviously shouldn’t lose any purchasing power, but in reality, how have they held up?

Since they are tied to official US inflation, they track very well over time. But federal income taxes will lower the return, upon redemption. That’s why a high fixed rate is so attractive.

I got the time to test it out. Starting with 100k at November ’07, I got to $151k on a 0% fixed, 163k on a .5% fixed, and 173k on .9% fixed – this would be at October ’23. At a 24% tax rate you’re still taking 139k, 148k, and 156k respectively. Inflation was about 40-50% in that period of time, so it matches pretty well.

I do not want to steal the fire, but 0.9% baby!!

Pingback: When Should I Cash Out My I Bonds? | Keil Financial Partners

I notice that you have .8 as the CPI for January but BLS reported .5. I also saw recently that the last 3 months CPIs were adjusted up from what was initially reported. So does the .8 figure account for those corrections along with the current January figure or am I missing something else?

The 0.8% is for non-seasonally adjusted inflation. The headline number of 0.5% is seasonally adjusted. These number balance out over a year. The CPI adjustments were for seasonally adjusted inflation and didn’t affect non-seasonal adjusted.

The Cleveland Fed Nowcasting had been predicting 0.19% for May and the current MTD June figure is 0.42%. Is this forecasting Seasonally Adjusted or Non-Seasonally Adjusted?

These nowcasting projections are good for seeing a trend, but not super accurate month to month. It is projecting seasonally adjusted inflation.

Default talk for US government debt again rears its head.

Just wondering, worst case, how this could affect my I Bond holdings? Could I lose what I hold? Hope not, but while I realize that whatever value I have would not drop if we suffered deflation, I don’t have a clue about what effect a default would have…

I am assuming all of the effects of this crisis will be short term, and your I Bond holdings won’t be affected at all.

I just wonder if there is a “pecking order” for government bonds if there would be a default. Granted this is likely just an academic question…but would I Bonds be safer than TIPS, for example?

Interesting thing about I Bonds is that they actually pay no interest until they are redeemed, so only I Bonds that are being redeemed would potentially be affected by the debt limit crisis. I am sure when it is all resolved, all earnings for I Bonds and TIPS will be made whole.

Good point. Which is fine for any ibond that one was considering redeeming before maturity (simply “wait it out” instead of trying to redeem during any, hopefully brief, default period.)

However, what about ibonds that unfortunately happen to reach maturity (upon which Treasury Direct, under normal circumstances, would automatically redeem for you) during that hopefully brief default window?

Obviously. you aren’t going to be able to collect during a default. I would hope TD would suspend auto redemptions (and probably *all* redemptions, not just the ones that are automatically triggered at maturity) rather than default on the redemptions during the default period and then let any delayed redemptions happen upon the resolution of the default.

John, the first I Bonds were issued in 1998, so there will be no maturities until 2028. Maturities won’t be a problem, at least for I Bonds. Other Treasurys could see disruptions.

Can the I bond variable rate be negative and if so would you loose money?

Yes, the I Bond variable rate can be negative. The last time that happened was in the six-month period beginning in Sept 2014, with a variable rate of -1.60%. A negative variable rate will wipe out any fixed rate up to that amount, but the resulting composite rate can never drop below 0.0%. So you would not lose money.

A negative percent I Bond fixed rate? What are the chances?

Have not seen this possibility mentioned anywhere, but in the current environment could it be possible? Seems like it could be…

Under current federal regulations, the fixed rate cannot be lower than 0.0%.

Interesting. I did not know that…thanks for the answer!

The variable rate is said to track inflation rate. Why the inflation rate has increased substantially in the recent several months (and that’s why the Fed hiked the base rate aggressively from 0.5 in May to 3.25-3.50 in September), but the variable rate would drop dramatically from the current 9.62% to 6.48% (from November 2022 to April 2023)?

I’ve noticed the “6 month %” change is 3.24. Should the change be on top of the prior variable rate set in May? Would it simply be against common sense that the inflation rate has increased and currently is very high, the Fed base rate has increased, the T-bill rates have increased, but the I-bond variable rate would drop, dramatically?

The I Bond variable rate is set based on six-month periods of inflation — April to September, and October to March. So the current I Bond variable rate always reflects 6 months of prior inflation. But think about this. The last variable rate was 9.62%, and yet AT NO TIME did annual U.S. inflation run higher than 9.1% over the last two years. Now the new variable rate will be 6.48%. If you bought an I Bond with the 9.62% rate and then got 6.48%, you’d get a compounded rate of return of about 8.21%. The current rate of U.S. inflation is 8.2%. It won’t always work out that accurately month by month, but I Bonds over time accurately track U.S. inflation.

The question was how about buy the bond on November 1, without the prior much higher rates in an average? What would be the inflation rate on November 1 and in the next six month then? If the composite interest rate is set below, let alone far below the real inflation rate at the time, it cannot be called inflation-protected as alleged by the Treasury. If the Treasury talks about 10 years, 20 years or 30 years, it might be a different story. But I wonder what the percentage of buyers would hold the bond that long? It would be interesting to know some study showing that the composite interest rate has never below the real inflation rate in any given 5 years since its inception.

I see it similarly. To me, the i-bond is best when inflation is increasing and even better if increasing rapidly. However, once it peaks or moderates, the i-bond floating calculation could result in a negative or zero %, even if inflation is at a really high level. It becomes the rate of change, not just the level of inflation. You can see that currently … based on Jan 2023s inflation index, the floating rate component compared to Sept2022, would yield ~1.6% (change between 299.17 and 296.808, annualized). A significant drop from the prior 6.48%, even though inflation still is high. Probably the worst time to make an initial purchase is at the top of an infl cycle ? I agree with the comment that if you had owned them for a historically long time, you’d probably earn something near the rate of inflation. But many folks just jumped in when the rates started getting much higher than other fixed income instruments. Am I seeing this correctly?

I’m one of those buyers. I have bought since 1998 and held them-some with fixed rates higher than 3%.

TJ, if you plan to be a long-term holder, there is no bad time to buy an I Bond. Short-term investors jump in when the variable rate is high, as it is now, and that is fine. Long-term investors are planning for a future time when inflation potentially and surprisingly soars (just as it did in the last two years). An I Bond does accurately track or exceed U.S. inflation. Plus the interest is tax-deferred, and the maturity is flexible, so you can choose when to redeem and pay taxes.

Simply the best blog on this topic on the web.

Check my math, but my numbers show an ROI of 6.51% if I buy an I-Bond at the end of October and sell it in one year including the 3-month penalty. Now it could be a bit better than that if I can sell it at the beginning of October 2023 instead of waiting till November 1, 2023, since I am allocating the cash at the end of this October. Any way I skin it the results look good whether I sell or hold long.

My rough estimate would be 6.43% without compounding. So your estimate looks good.

Hi. I bought iBonds for the first time in April 2022. I think the 9.62% interest rate began in May 2022? I thought I’d be earning 9.62% for the first 6 months of ownership but maybe not since my purchase was in April. Could you clarify which interest rate I’ll be getting over what time period? Thanks.

If you bought in April 2022, you earned 7.12% annualized for six months and are just now starting to earn 9.62% annualized for six months. Buying in April was an excellent move. After these next six months at 9.62%, beginning in April 2023 you will earn 6.48% annualized for six months. Take a look at my I Bond Q&A https://tipswatch.com/qa-on-i-bonds/

Thank you! Very helpful.

Nancy – Congratulations on your April 2022 purchase. 100% agreement with the annualized returns and “excellent move” comments made by Tipswatch. How are you feeling about it now?

This is not correct. You did not “earn 7.12% for six months”. You earned 3.56% for the six months. The 7.12% is an annualized rate to make it comparable to other investments, but it is not what you earn. You earn 3.56% for six months. After six months, the current value becomes principal for compounding purposes, and then you will earn 4.81% for the next six months, since 4.81 is half of 9.62.

In these articles I almost always say “annualized.” It gets repetitive. But, if you insist…

Senators Deb Fischer and Mark Warner introduced a bill on 27 September raising the annual purchase limit of I Bonds through Treasury Direct to $30,000. The $5,000 limit for paper bonds from income tax returns is not changed. Inflation must exceed 3.5% during an “applicable year” for the new purchase limit to be honored.

The title of the bill is The Savings Security Act of 2022.

On October 1st, the bill had not yet been assigned a number.

I would encourage the readers of this forum to contact their two senators and urge them to support the passage of this bill. Be precise about the description. In addition to citing the title, mention raising the limits on I Bond purchases and name the bill’s authors. There is another bill pending in the Senate called SECURE Act 2.0 which senators and their staff may confuse with this new bill if your description is not precise.

Great information, thanks.

Per Treasury Direct website, if a Series I Bond is redeemed between 12 and 59 month holding period there is an interest penalty consisting of the LAST 3 months of interest. I purchased a $10,000 Series I Bond on Nov 1, 2021. For the first 3 months interest accrued was zero. Starting in Feb 2022 I am earning interest.

Can you confirm interest penalty is on the last 3 months of holding period?

Can you explain lack of interest accrued for first 3 months?

TreasuryDirect will not show the last three months interest as accrued until you have held the I Bond for 5 years. This causes a lot of confusion, but this is the way TD works. For the first three months, it will look like you have earned zero interest, but you have.

Basically just its way of telling you how much they would be worth if you were to sell them right now (after waiting 12 months of course). Otherwise it would get confusing to subtract once you sold them. What?? The site says they’re worth $1000! You only paid me $900! Once 60 months hit I’m sure there would be a nice “bonus” payment seen (ie three months of interest being added on all the sudden).

Maybe a new question, but I could not figure out how to post a new question, and this one is related to this thread…

Just wondering on month 13, what interest is posted as part of the I Bond value. I would like to think it is the interest from the first month, but do not have a clue really. I mean if the first month interest was high, and month 13 interest rate was low, which would show up on month 13?

Hope this question makes sense. Tried my best…

On TreasuryDirect, at the beginning of the 13th month, you will see the interest posted from the 9th month. You have earned interest for 12 months, but the last three months won’t be shown because of the three-month penalty for early redemption.

I think I get it. In other words, interest paid on month 4 is paid from the earnings of month 1, and from that point forward the sequence continues until the 5 year point is reached, when three months interest is paid in a lump…

Cash in before 5 years has elapsed, and you receive what the treasury direct site says your iBonds are valued at.

Right?

Technically, you need to begin month 5 before TreasuryDirect shows you month one. But … you are earning interest every month, TD just doesn’t show it because of the early withdrawal penalty.

In the July 25, 2022 issue of Barrons in an article titled “TIPS, I Bonds Are Smart Ways to Buy Inflation Protection”, the author Andrew Bary writes in regard to iBonds: “Scherer says investors can skirt the $10,000 limit by also investing through trusts and small businesses that are sole proprietorships.” This was news to me — I’ll do some web searching of my own but thought I’d ask here what you know about this.

And as always let me add a Thank You for your valuable and insightful writing on Tips and iBonds.

Yes, this is accurate. Harry Sit at TheFinanceBuff.com has covered the bases on this: https://thefinancebuff.com/how-to-buy-i-bonds.html

I just had something unexpected happen that I would like to share.

I bought the max $10K of I bonds just before the end of April to lock in the current rate.

We usually do not have excess cash, but we did this year, and there was an extra $5k we needed to put somewhere. My wife bought a $5K gift to be deposited into my TD account after the first of the year, as we understood that would be the first available date for the gift, as I already bought the max for this year.

Well, she accidentally gave the gift to me after the five day waiting period, and it now shows in my account, and not in her gift box anymore. I also got the email saying a gift was delivered. Several days have passed and nothing has changed.

I am guessing that this gift will subtract from what I bonds I can purchase next year, but I don’t plan on purchasing any net year, so the point is moot.

The net affect is no different than if the gift was given after the first of the year. Still have to wait 12 months before the funds will be available anyway.

I was just surprised that we did not have to wait until the end of the year to make the gift.

Just wanted to share this surprise, as it saves us the bother of remembering to make the gift 8 months later.

It’s possible this won’t get caught, but from anecdotes I have heard, TreasuryDirect may discover the error and send the gift back to your wife’s gift box. If it does get returned, and she gives you the 5K in January, you will be limited to $5,000 in purchases in 2023. If it doesn’t get caught, you probably could buy $10K next year.

I do not care either way, just was surprised. Do not plan on buying I bonds next year anyway…was curious though about this. I will keep an eye on it and see if something changes.

If they take the gift back, I hope they at least advise us that they did this. Makes no difference to us either way really. As long as we don’t forget the gift has been returned to her gift box…LOL. Even if we forget, it probably does not matter much…

I decided a couple weeks ago to ask Treasury Direct about the gift showing up in my account, when it should not until next year, and explained the situation. Sent the message through the TD site. Never got an answer, but did get an email later saying that I had talked to someone at TD (which I had, but about something else) and no further action would be taken at their end…or something like that. Of course, they did not reference what they were talking about…

I am just going to let it go, as it makes no difference to me, and my curiosity is not that great…my guess is that they do not have controls in place to prevent certain things from happening.

For example, I remember reading on the TD site, that if you purchase more than the annual limit of I bonds you will be warned, the excess would be cancelled, that a refund may take several months, and perhaps even a mention that your TD account might be in jeopardy. Paraphrasing of course, do not remember the exact verbiage.

Well, the saga continues.

I got an email from TD saying I exceeded my annual purchase limits and the excess will be refunded. Not sure if this was in response to my effort to be honest about what happened or not. What bothers me is I did not exceed my purchase limits. The TD system lets a gift be processed, when the TD system should immediately flag the issue and not process a gift until the recipient can receive it.

I replied that rather than refunding anything, the I bonds should be put back in my wife’s gift box, to be given after the start of 2023, which was the original intention and the reason I emailed TD about the issue to begin with. Just trying to be honest at my end.

In any event, not a major issue. Irks me a bit that trying to do the right thing may have resulted in an undesirable outcome…live and learn. Message is: Make sure not to make the same mistake with your gifts of I bonds!

When the money is refunded it should go back into the gift box.

I hope so! That would make sense and work for us! time will tell. I will report back after whatever happens, happens…

Well, looks like I am out of luck. Following is from a TD email in response to my asking that the gift be put back in the wife’s gift box:

“That won’t work.Purchase limits don’t look at when a bond is delivered, the limits look at when the bond was purchased. That’s why it’s called a purchase limit.

We receive notification when an account holder exceeds the annual limitation for savings bonds. We refund any repeat excess purchases. You don’t need to do anything. A refund of the excess purchase will be made to the bank account where the purchase originated.

[snip]

Your funds will be deposited back into your bank account. This process will be completed, and you should receive your refund approximately 16 business weeks from the date of purchase. Each refund needs to be reviewed and approved by an examiner, so it does take time to process.

We will notify you by e-mail when a refund is processed.”

Can only hope now that this is so unusual, that they may actually put the I bonds back into the wife’s gift box… MESSAGE: Make sure not to give a gift to someone if it exceeds their annual purchase limits. (Not sure how the person giving the gift could know that in every case though.)

If by some miracle the bonds end up in the wife’s gift box I will report back.

Of course, you can now reinvest that money into your wife’s gift box, right? But you won’t get the 7.12% for six months, just the 9.62% instead and whatever comes next.

Yes, that is the plan. Our mistake caused this.

Don’t have a lot of excess cash, but planning on purchasing $500 or more per month until the refund appears (in the wife’s gift box), and then putting the $5K refund back into I bonds as well. The intention being to have interest earning cash available as needed in 12 months. Actually going to put all my loose change in i bonds for a while(via the wife’s gift box this year).

Crazy that we had a large chunk or cash(for us) laying in bank accounts that paid nothing for over a year, rather that putting it in I bonds. ESPECIALLY since the majority of our retirement savings are in I bonds, albeit bought 20 years ago, with 3.4% & 3.6% fixed rates. So we know the advantages of I bonds.

One thing I need to check and understand, is if a gift is presented, whether it has to be accepted by the gifted, or if it the gifted person has no option to delay receipt until the following year. I think that may be what happened in our case but do not remember for sure.

In other words, if a person receives a gift that pushes them over the annual limit, does this mean they automatically forfeit the gift? And the funds may be in limbo for 16 weeks to boot? Seems unfair if that is the way things work.

Believe it or not, the gift of $5,000 I Bonds stayed in my account (which already held the max $10K, and I guess became legitimate after the first of the year. So they were never canceled and there was no movement of funds back to the gift box or anywhere. I just wanted to update what I posted above so everybody knows how it turned out.

Hi David,

Hope you enjoyed your trip. Just wanted to leave a comment more so than a question. I’ve been hearing nothing but, “Inflation has peaked!” since the March numbers came out. As we all know, nobody knows what will happen. However, I think the numbers are being used as a trick. Sure, maybe it’s not going to accelerate as fast, but 8% (or whatever it will “go down” to, assuming it does actually go down) is still 8%. If it stays at 8.5% and doesn’t go up, then they’ll be throwing a party (hey, it didn’t go up!), but it’s still 8.5%. People tend to not understand percentages and fractions.

Pure (100% haha) example. Say a stock is $100. It decreased 50% the first day (OUCH!!). So now it’s $50. Well the next day it recovered and increased 50%. But wait a minute, if it decreased 50% and then increased 50%, shouldn’t it be back to the original $100?? Why is it only $75 now?!? Yes, I understand, but how many other people don’t?

I guess my point is people are going to easily misinterpret the numbers (some on purpose for political reasons). One measures velocity/speed and the other measures acceleration. Okay, you accelerated up to 55 MPH in the school zone, but at least you stopped accelerating in it (staying steady at 55 or slower to 54). Either speed is well over the speed limit, but at least the acceleration stopped, right? No, 50+ MPH is still over the limit! Just like 5, 6, 7% is still well above the 2% mark. The question is how FAST can (will) it decelerate.

I believe too much hype will be made of the deceleration (it actually went down, yay!) and they will (try to) forget the actual inflation rate itself. I said “try to” because it’s hard to fool people’s wallets. You mean I have to pay $25 for a #1 combo at McDonald’s??

Rant over.

I am one of the people who “think” that U.S. inflation will gradually lessen, but will remain in a range of 4% to 5% through next year. That is high inflation. But there are so many unpredictable factors; the war in Ukraine is an obvious disruption no one really saw coming. Covid resurgence? Gas shortages? Food shortages? So many possibilities.

Good observation, that is how it is done. And of course they will never admit deficit spending causes inflation.

Still pretty timely considering you are on vacation, traveling, half way around the world. My math gave a similar result, but I was happy that your number confirmed it. Thanks for what you do. Now I just need more cash to buy more I bonds.

Some time I’ll comment on why all bond funds should be avoided. Until then most of Larry Swedroe’s books cover the negatives quite well.

How about just commenting on why i Bonds should be avoided.

They have a given value, it is not subject to market forces, the interest gained is added to the principle, and there is close to zero risk. And worse case the value locks in during a deflationary period.

Other places you might put your money feel good when times are good, but feel really bad when the imaginary gains disappear when things go sour. Gains are imaginary, in most places you put your funds, unless you pull your funds out when times are good.

I don’t think i Bonds can be considered the same as conventional bonds. But I do not know. Please educate me…

Are there any negatives to I bonds? Well the fixed rates are set at the whim of the Treasury and their decision to offer them was based on lowering the government’s borrowing costs.

Some believe the CPI index has been manipulated to understate actual inflation. (Beginning with Fed chairman Alan Greenspan)

The idea that one may cash in early (losing 3 months interest) in order to repurchase at a higher rate is possible.

But one would need to calculate the long-term loss on the invested penalty for a comparison.

Yes I bonds are unique in that you can ‘put’ them to the issuer without penalty after 5 years. But I can’t agree that all other investments are doomed to disappoint. Whether any vehicle is a sound investment depends largely on the price paid.

Well, you did say that ALL bonds should be avoided…

Seems like your story has changed a bit with respect to I Bonds. A fixed rate above zero is certainly great. I have bonds from 20 years ago that average a fixed rate of 3.5 percent.

But even with the zero percent fixed rate, the I Bonds look good to me for a temporary place to put cash for the short term TODAY. EVEN with the 3 month penalty, which can really be two months if you time your purchase at the end of the month.

Reading carefully we see that what I said was all bond FUNDS should be avoided, because they negate all the virtues of holding bonds.

But you have the right approach, all observations should be prefaced with, ” In the past…” Something you don’t hear from the Wall Street hucksters.

So I bonds at 3.5 % were a ‘gift’ we may never see again. But, at the moment, I can’t relate to wishing I could sink $100, 000 into them as has been discussed.

I guess you are right about that. I did not consider the word “Funds” as part of the equation in what you stated….Still, as compared to bond funds it looks like for the short term I bonds are a good deal.

FIphysician has a nice piece on Tips here: https://www.fiphysician.com/tips-and-duration-should-i-buy-short-term-tips/

5 year TIPS currently trade in the secondary market with a premium of about 6%. Isn’t someone in the 22% tax bracket better off buying TIPS through a broker in a Roth IRA than they are with I-bonds? It seems like the tax-free nature of the Roth more than makes up for the small premium on the TIPs.

I have I bonds from back in 2000 and 2001. Great fixed rate. Will keep them until maturity likely.

But I only recently realized that these bonds only pay whatever the annual inflation rate is, plus the fixed rate adder.

This is interesting, as on first look it seems like the calculation is twice the inflation rate plus the fixed rate. Reality is that since this is based on a 6 month period, the net affect is the same as if inflation was a fixed percent for the 12 months after purchase, and the I bonds would pay that on an annual basis. In other words, the net result is simply based on the inflation rate plus the fixed rate for those 12 months. Granted, semi annual compounding of interest adds something.

So my I bonds with an average fixed rate of 3.5 percent, will pay around 10.5 percent over 2022, and not 2 times the inflation rate, plus the fixed rate, which would be much higher.

The calculation explained in the literature sort of implies a net gain of 2 time inflation plus the fixed rate. But reality is from what I can see, that I Bonds just pay the inflation rate plus the fixed rate adder.

Still, I am happy with a likely 10 percent return during 2022.

The I Bond’s variable rate is 2 x a 6-month inflation rate, giving you an annualized rate that is in effect for 6 months. So the rate is doubled, but it only lasts for six months, not a year.

I think that was my point. So the net affect is I Bonds pay whatever the average inflation rate is, and nothing more than that plus whatever the fixed rate is…

Not bad really. Just saying that at first I thought they were even better, but still satisfied with the performance with an average 3.5 percent fixed rate…

Hi David,

As always, thanks for the info you provide.

I thought I would ask your opinion about inflation in general. The government (all politicians) is (and has been) printing money hand over fist for years nows. Yet, inflation has been “kept low.” So here is all of this money hitting the markets, yet inflation is basically stagnate. I would like to think of inflation as watering down money. Just like adding ice to a soda. Eventually the ice melts and now it is watered down. Add more ice and it’s even more watery. Sure, now you have “more soda,” but the ratio is so watered down that you can (non-sarcastically ) ask the question, “Would you like some soda with your water?”

I guess my question is, had the inflation numbers been true (ie the soda would have kept up with the added ice/water) throughout the years (ie 3% here, 4% there), would we even be experiencing these big jumps? My opinion is there is no room to hide it anymore. Not counting the last two rates, the average for inflation average is easily only 1% since May 2010 (I didn’t actually calculate, but with all of those less than 1% numbers, especially the negative ones).

Between the money printed and the percentages that they SAID was Inflation, I can’t help believe that there wasn’t some lying in those numbers over the last decade. My opinion is that this is nothing more than a hidden tax to make people pay for the debt quietly (indirectly). We’re $30+ trillion in debt? Fine, make $30 trillion not worth much. Just like a penny is now practically worthless, so will $30 trillion.

The inflation numbers are definitely nudged here and there by tweaks to the indexes, but CPI is the only official number we have. By the way, inflation from Dec 2011 to Dec 2021 averaged 2.1%, the highest for any 10-year period since the era ending in 2014. The difference “this time” (meaning the pandemic era) is that both Congress and the Fed poured massive stimulus into the system, including multiple direct payments to families. That was unlike the 2009 stimulus, which poured money into banks, but not directly to people. All of that stimulus is now ending, but if “inflation psychology” has set it (and your comments indicate you think it has) then future inflation will be hard to pull back down below the 3% to 4% range.

Same view here. If the CPI were calculated as it was in the Eighties inflation would be 3-5 percent higher than as stated now. The Bureau of Labor Statistics (BLS) invented the term ” hedonic quality adjustment”. If my new computer is ‘better’ than the old one but costs more? They derate the cost of the new one, as an example. Cute.

Well , they do have a point whether you want to agree with the point or not.

The computer one could have bought for 500 dollars 5 years ago is not the same as a computer one can buy today for $500. To simply compare the two on sticker price would be an apples (the fruit, not the brand) to oranges comparison as they are not the same product despite both being called a computer. If you were to buy exactly the same exact spec’d computer today as you could then, the cost would be much less than $500 whereas to buy todays $500 computer back them it would have been much much more (assuming it was even possible, as some of the newer iterations of components weren’t even developed yet back then).

Well said, but it is the essentials that should be the focus I think.

Food, clothing, housing, transportation, medical care.

I thank whatever gids may be a computer is, not yet, essential.

Cheers

I have a question about compounding. I understand the value of my Ibonds shown in Treasury Direct has the most recent 3 months of interest deducted. When does the compounding take place? On the 6 month anniversary of my purchase date or on the 2 dates each year when the variable rate changes? Also, for compounding purposes is the 3 month of interest penalty included in the amount to be compounded or left out?

TreasuryDirect says this: “I bonds increase in value on the first day of each month, and interest is compounded semiannually based on each I bond’s issue date.” I would think the three-month penalty does not have any effect on compounding.

100% agree with Tipswatch that ” I would think the three-month penalty does not have any effect on compounding.”

There is no “compounding penalty” for the 3 month early withdrawal penalty and below is why.

Interest accrues MONTHLY and is added to the bond value on the 1st day of the next month. That is how the savings bond value grows EACH month.

Compounding is every six months on the semiannual anniversaries of each bond.

Dave, In the I Bond manifesto I read that the interest is earned on the last day of the month and posted to your account on the first of the following month. I bought $10,000 apiece for my wife and I in mid-Nov 2021, and no interest is posted yet (Jan 5, 2022). I emailed Treas Dir asking about interest posting but no response yet. Any thoughts?

The interest postings on TreasuryDirect will exclude the last three months of interest until you have held the I Bond for five years. From their site: ” If you use TreasuryDirect or the Savings Bond Calculator to find the value of a bond less than five years old, the value displayed reflects the three-month penalty; that is, the amount of the penalty has been subtracted already.”

And when the bond reaches the five-year point, you’ll get three months’ worth of interest posted all at once. Feels like Xmas.

Thanks David — I am new to inflation-protected securities, and I’ve really enjoyed your content as I’ve studied-up on the concept. I happened upon some mass media coverage of I bonds in November. After doing some research, I determined it is easily in my interest to move funds from a savings account earning 0.5% to I bonds, if only for a year. Given the current trajectory of the CPI-U index, it will likely be longer than that.

In addition to double-dipping for myself, I am considering an I bond gift to my minor children (2 years old and 6 months old). My intention would be to issue the gift and hold it in my gift box until my children approach adulthood — mostly to diversify the ways I am saving for their educations/weddings/home purchase/whatever else a parent might help a young adult achieve.

However, the one issue that gives me pause, is with a fixed rate of 0% — would I regret the investment if we hit a prolonged period of low inflation, so the earnings drop to little-to-none and were uncompetitive with CDs/Online Savings Accounts/Money Markets. Would I then be in for tax complications I don’t understand if I wanted to divest of the I-bonds on my children’s behalf?

Obviously, you don’t have an inflation crystal ball, and I am not seeking (and I assume you would not provide) tax advice. However, I wonder whether you have general thoughts about I bonds as a potential gift/investment vehicle for minor children. Perhaps you’ve written a post here I haven’t com across.

Thanks for your thoughts and for this thorough and informative page.

Charles

I haven’t used the “gift box” technique, but you could also look at creating TreasuryDirect custodian accounts for each child and purchasing the I Bonds there. (I have no experience with that, either.) I wouldn’t be too concerned about the 0.0% fixed rate, but yes, that rate could increase in the future. You could ladder the purchases — buying some each year for several years — to give yourself a chance at a higher fixed rate in the future. I Bonds are a tool for capital preservation, not wealth building, so basically the money you put into I Bonds will simply get pushed out into the future, with inflation protection. Could you combine I Bonds with some asset allocation to the total stock market for your children? Anyway, I am just a financial journalist, not an adviser.

Pingback: [Repost] US Treasury Bonds Rate Set To Increase To 7.12% Rate (I Bonds) – Money Mondays

I would like to know if I can make additional $5000 payment to IRS, and buy paper I-Bonds from the refund that I get when I file my taxes in March/April of 2022.

Any has used this method to buy additional paper I-Bonds from the refund.

Many people do this. You will need to overpay your 2021 federal taxes by $5,000 and then can claim the paper I Bond in lieu of your tax refund. I’d suggest filing by mid-March to make sure you get an I Bond issued before May 1.

Pingback: First rule of I Bonds: Don’t rush to sell your I Bonds | Treasury Inflation-Protected Securities

Enjoy your website data and articles. I am a fan of both I and EE bonds for my “long term” safe cash, buying each year to create a ladder: I think of EE as a 20 year CD and I Bonds as a flexible 5 to 30 year CD. Two concerns that can only be speculation at this point because there is no way to know how government policy will intersect with government debt, inflation and interest rates: 1) the $10K annual purchase limits for EE and for I (and the $5,000 limit on I Bonds for tax refunds) are not indexed for inflation so that limit will gradually be more restrictive over time and those limits have been subject to arbitrary decisions set in the past (once upon a time up to $30,000; then during the transition from paper bonds to electronic bonds, the limit was temporarily $5,000); 2) the EE original maturity date (the period it is guaranteed to double the original purchase) is subject to change: for example in May 1995 it was changed from 12 to 17 years, then it was changed to 20 years in June 2003 and has surprisingly remained there ever since as of late 2021. The 20 years to double are what create the 3.5% annual rate. What are your thoughts on the purchase limits and the potential for change in the EE doubling date?

I agree that the EE Bond terms — doubling the investment’s value in 20 years — are generous in today’s market, and the Treasury has raised that limit several times, but not recently. The doubling is counteracted by the 0.1% fixed rate for 19 years, 11 months, which probably chases most investors away from EE Bonds. The 20 year term makes EE Bonds viable as an “education fund” for a child, but any longer term would make them useless for that purpose. So the 20-year doubling makes sense, and should continue.

For I Bonds, I also agree that the $10,000 per person per year purchase limit should increase, maybe gradually, to at least $20,000 a year. But the Treasury has no incentive to do that right now, with the variable rate so high. So many investors look at I Bonds and say, “That’s not enough to make a difference in my portfolio.” That’s true, and it’s the reason investors should buy I Bonds every year, up to the limit if they can.

Pingback: Animal Spirits: It Wasn't Transitory - The Irrelevant Investor

Pingback: Series I Savings Bonds Rates (Updated October 2021) – RobBerger.com

Pingback: US Treasury Bonds Rate Set To Increase To 7.12% Rate (I Bonds) - Doctor Of Credit

Pingback: US I Bonds seem to be pretty at a pretty good rate this 6 month period and are looking better for next. I’m curious if I happen to be missing something – Frank Radtkee

“Savings Bond Wizard” isn’t available anymore and has not been for a couple of years, as I recall!B

That’s true, now we need to use the rather clumsy Savings Bond Calculator … https://seekingalpha.com/article/4179171-step-step-guide-to-using-treasurys-new-savings-bond-calculator

Pingback: 10 Articles About Inflation Protected Bonds | Troy Taft Blog

Re: purchasing an extra $5,000 worth of iBonds using my Tax Refund: Can that $5,000 tax refund be deposited directly to my Treasury Direct C of I account? Or must that refund be used to purchase paper iBonds? The Form 8888 instructions and the instructions on Treasury Direct seem ambiguous to me:

From Form 8888:

TreasuryDirect® Account

You can request a deposit of your refund (or part of it) to a TreasuryDirect® online account to buy U.S. Treasury marketable securities and savings bonds. For more information, go to http://go.usa.gov/3KvcP.

U.S. Series I Savings Bonds

You can request that your refund (or part of it) be used to buy up to $5,000 in series I savings bonds. You can buy them electronically by direct deposit into your TreasuryDirect® account.

From Treasury Direct:

Using Your Tax Refund for TreasuryDirect

Do you know you can have your tax refund directed to your TreasuryDirect account to use for Treasury security purchases?

TreasuryDirect offers flexible options for all your security purchases. One option to fund your account is to use your tax refund.

You can request the IRS or your state tax department to deposit your tax return directly into your TreasuryDirect account where you can use the funds to purchase savings bonds or marketable Treasury securities. All you need to do is provide TreasuryDirect’s routing number and your TreasuryDirect account number in the refund instructions on your tax return.

On your tax return, enter:

the TreasuryDirect routing number, 051736158, in the “Routing number” field.

your TreasuryDirect account number in the “Account number” field.

“Savings” as the account type.

Providing these instructions in the “refund” area on your tax return will direct your refund to the Zero-Percent C of I in your TreasuryDirect account where it will be available to fund the purchase of one or more Treasury securities.

You can also use your refund to purchase Series I savings bonds in paper form.

I’ve never used the tax refund method, and i had assumed you it would have to be in paper I Bonds, but the wording you present here makes it look like it can be sent to Treasury Direct. Then the question would be: Would that deposited money count against your $10,000 purchase cap?

Exactly – that is my question. I guess I’ll contact Treasury Direct for clarification. I actually had luck in the past getting a helpful response from Treasury Direct to a question I’d posed. Not sure how to go about getting clarification from the IRS.

Here’s the response I got from Treasury Direct:

“You must purchase the paper securities and then the electronic separate. If you put it all in your TreasuryDirect account you will only be entitiled to purchase the $10,000 limit.”

In case anyone is interested I did the tax refund method and received $5,000 worth of paper iBonds a little more than three weeks after filing my tax return. They were sent in denominations of (6) $50, (1) $200, (1) $500, (4) $1000 paper iBonds in twelve (count ’em that’s 12) separate envelopes all delivered by the USPS on the same day (in spite of Louis DeJoy’s best efforts). Since I already have a Treasury Direct account, the next step for me was going into my Treasury Direct account to convert the paper iBonds into electronic iBonds which results in the creation of a manifest which one prints out, signs and mails with the unsigned (12) paper iBonds to a Treasury office. Those were mailed this past Saturday (certified mail/return receipt requested).

So up to this point in time this seems to have worked just fine — I don’t know if I will do it again in the future as I don’t know that I want to spend time worrying about the the performance of the postal service and the IRS. And it was a bit time consuming explaining to my accountant that you could do this using IRS Form 8888, dealing with the conversion on Treasury Direct and traveling to and waiting in line at the post office to mail the paper iBonds to Treasury via certified mail. But at the least it’s been an interesting exercise.

Great info, thanks, Andrew.

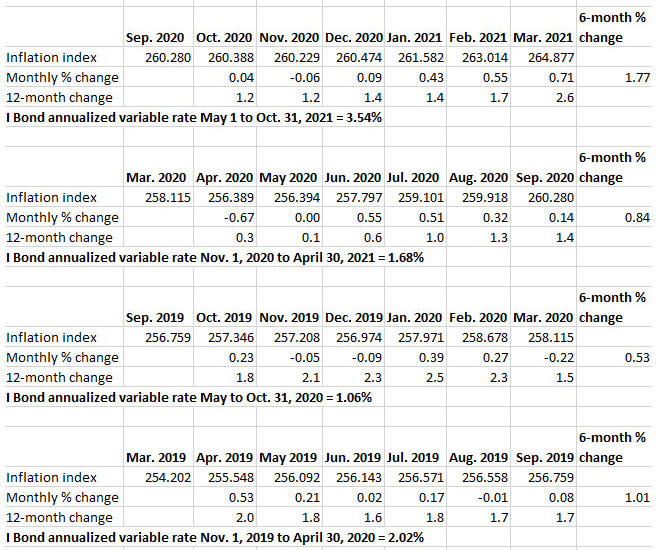

Hey Dave, It looks like you’re missing the six month periods Mar 2019 – Sep 2019 and Sep 2019 – Mar 2020 above. I believe those periods showed inflation of 1.01% and .53% respectively.

Mark, thanks for noticing that. This happens because these image files are so large that they have to be broken up into several files. I seemed to have lost track where one ended and the other began. It is fixed now, and I set up a “reminder” in the Excel file to show the current live section. Appreciate it.

Pingback: I Bonds - I Like Them, Should You Too? | Dividends Diversify

Just one serious problem with having I Bonds through TreasuryDirect. They don’t issue account statements. Ever. The only proof you have of your bond ownership are screenshots, and they don’t contain enough information (like your full name, SSN, and address). Some people are very uneasy with this, and I can understand why. I read a post from one person who wanted to use his I Bond holdings as collateral for a loan, and had a devil of a time satisfying his lender that he did, in fact, own the bonds.

Also, does anyone know what would happen if your Treasury Direct account is hacked? Will the Treasury reimburse you if your electronic I-bonds are stolen?

This has been the subject of a lot of debate. The general consensus is that if that if TreasuryDirect gets hacked in a broad attack, you would be protected. But if you give away your password in a personal phishing attack, you could have a loss. TreasuryDirect has a good security system with two-stage authentication and other safeguards. Nothing is perfect, though.

Yes, that sounds right. If you are careless with your checking account or brokerage account login credentials and someone cleans you out, the bank or brokerage isn’t going to make you whole, either.

And on the couple of occasions when I have done something like redeem a bond, or made a change to my linked checking account, I get an email within seconds. For someone to hack your account, it would take a coordinated effort to extract cash. Add in the two-factor authentication, and it becomes a fairly daunting task.

BTW, gotta love the upcoming interest rate reset, especially if you’ve got older bonds with a high base rate!

Thank you for your info and explanations of I-bonds. I didn’t know where to find out about upcoming variable rates on I-bonds. I also didn’t know I could redeem my 2003 I-bond anytime if I wanted to (which I don’t). Your site is more helpful to me than Treasury Direct’s website. Thanks for maintaining your site.

Thanks Tipswatch, very useful info.

Pingback: Deflation continues: US prices fell another 0.4% in December | Treasury Inflation-Protected Securities

Pingback: U.S. inflation fell 0.3% in November | Treasury Inflation-Protected Securities

Pingback: I Bond watchers: Important inflation report coming Wednesday at 8:30 a.m. | Treasury Inflation-Protected Securities

Pingback: U.S. inflation fell 0.2% in August, what does it mean for TIPS and I Bonds? | Treasury Inflation-Protected Securities

Pingback: U.S. inflation rose a moderate 0.1% in July | Treasury Inflation-Protected Securities

Pingback: Before you buy that 10-year TIPS … consider an I Bond | Treasury Inflation-Protected Securities

Pingback: U.S. inflation rose 0.3% in June | Treasury Inflation-Protected Securities

Pingback: Up next: New 10-year TIPS auction July 24, 2014 | Treasury Inflation-Protected Securities

Pingback: U.S. inflation rose a sharp 0.4% in May | Treasury Inflation-Protected Securities

Pingback: U.S. inflation rose 0.3% in April | Treasury Inflation-Protected Securities

Pingback: Tracking inflation and I Bonds: A new data page | Treasury Inflation-Protected Securities