David Enna, Tipswatch.com (updated June 13, 2026)

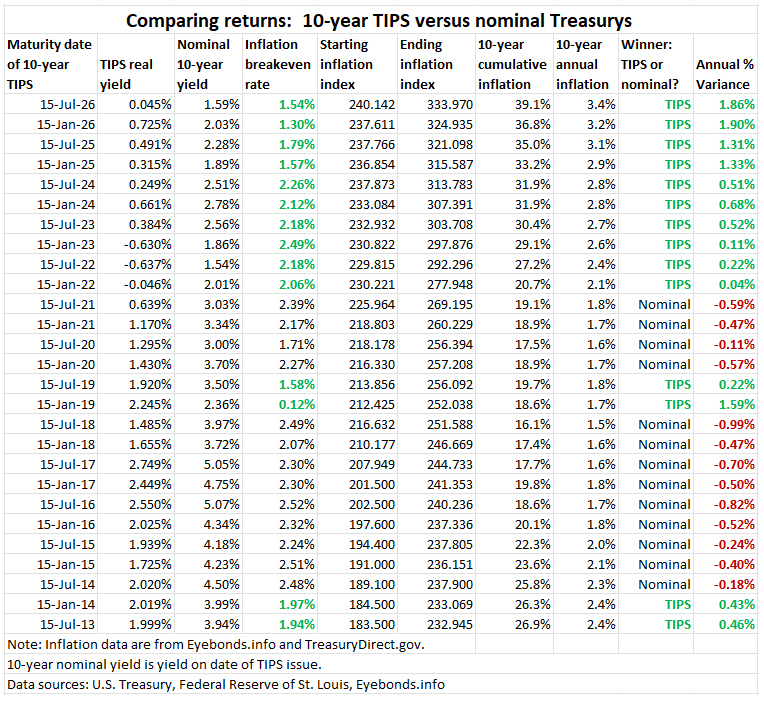

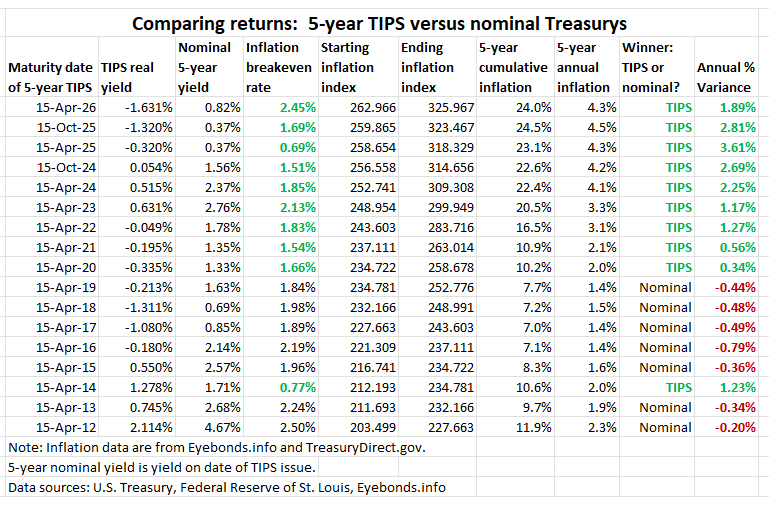

I’ve been writing about inflation-protected investments – Treasury Inflation-Protected Securities and U.S. Series I Savings Bonds – since 2011, and I’ve been investing in these products since 1999. So, how have these investments been doing? I track the performance of every maturing 10-year and 5-year TIPS on this page, as they mature in January, April, July and October.

To view this at a glance, the annual variance number in the last column shows how the inflation breakeven rate compared to actual 5- or 10-year annual inflation. When the numbers are green, a TIPS was the superior investment. When they are red, the nominal Treasury was the better investment.

We recently completed a decade-long period of inflation running at less than 2.0%, causing TIPS to do poorly versus nominal Treasurys. Then in 2021 we entered an era of much higher inflation, and so TIPS maturing recently have done well. The next decade could be entirely different. Never predict the future decade based on the performance of the past decade.

Notes and qualifications

These charts are an estimate of performance.

Keep in mind that interest on a nominal Treasury and the TIPS coupon rate is paid out as current-year income and not reinvested. So in the case of a nominal Treasury, the interest earned could be reinvested elsewhere, which would potentially boost the gain. For certain, we don’t know what the investor could have earned precisely on an investment after re-investments.

In the case of a TIPS, the inflation adjustment compounds over time, and that will give TIPS a slight boost in return that isn’t reflected in the “average inflation” numbers presented in the chart.

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

I did further analyses on the information you provided above. However, I cannot put an image here or email it to you?

David, the charts comparing TIPS to treasuries are very helpful. Would you be able to make them using I Bonds compared to treasuries? Thanks.

For my recent articles on this topic I have included an I Bond comparison. For example: https://tipswatch.com/2025/04/07/a-5-year-tips-is-maturing-april-15-how-did-it-do-as-an-investment/

If the I Bond has a higher fixed rate than the 5- or 10-year TIPS, it will be the winner. Doesn’t happen often, though.

Is the breakeven inflation rate accurate when you simply subtract the TIPS yield from the nominal yield? Seems to me the nominal bond would do worse than TIPS at this breakeven rate, because the returned principal at maturity is lower.

I built a spreadsheet comparing a 10-year TIPS to a 10-year nominal bond and calculated the returned interest and principal over the life of each, assuming inflation matches the breakeven rate. I found the nominal bond returned about 2.5% less than the TIPS overall, which confirmed my suspicion. Then I tweaked the breakeven rate, to make them match, which increased it by at least 0.2%.

I’ve scoured the web and found no evidence to back me up, or even anyone else doing this comparison.

The real yield to maturity and the nominal yield to maturity don’t depend on reinvestments. In the case of the TIPS, the inflation accruals continue building, so you get more at maturity but the coupon payments need to be reinvested. In the case of a nominal, the coupon payments all have to be reinvested. You could do better, worse, or about the same with those reinvestments. Tomorrow morning, I am posing an analysis of the 10-year TIPS maturing this week. After it matures, you can find its annual nominal return, which was 3.241%, versus 1.89% for the nominal Treasury note in January 2015. The TIPS was the big winner, in this case.

Thanks! I think I get it: I neglected to consider the opportunity cost from the TIPS bond keeping more capital tied up for longer, while the nominal bond returned more along the way that could have been reinvested. Then again, I calculated each returned coupon or principal payment in real dollars and added them all up, which should have been a meaningful comparison. Will think about it some more.

Does anyone know of any research/analysis of comparing TIPS with Munis in a taxable account ?

I am very interested in TIPS, but over 90% of my assets are in taxable, and currently use VTEB (Vanguard National Muni).

The problem in taxable is you either you have taxes on phantom income (ladder), or you have to pay taxes from the distribution of principle adjustment for a fund. This leaves you with cash flow issues for the ladder, and with your inflation adjustment diminished for both the ladder and the fund.

Of course, the Muni bonds or fund does not even have the inflation adjustment to begin with, but when you compare TIPS funds to Muni funds (for example, VTEB or VWIUX with VAIPX) the Muni funds have beaten the TIPS funds, after taxes, on a total return basis, presumably due to interest rate risk.

Is it simply not a good idea to hold TIPS in a taxable account ?

The general advice is to hold TIPS in a traditional IRA account, where the phantom tax is made moot. However, those accounts will be taxed on the state level for withdrawals. If you live in a high-tax state, a taxable account might be the way to go. At today’s higher coupon rates, the income will cover the taxes.

Yes, TIPS work the way they are “supposed” to in tax deferred, but I have very little in tax deferred to make a difference.

And yes, the income will typically cover taxes for inflation rates below about 5%. At that rate, a $1M TIPS ladder will generate $20,000 of income, and after you pay taxes on that, you have about $15,000 to pay taxes on the $50,000 principal adjustment.

However, aside from the issue of larger inflation (which is the point of using TIPS), you either give up the income or you shortchange the principal adjustment (depending on using ladder or fund).

In the end, a TIPS ladder or fund in taxable does not provide a real return, it provides a real return reduced by inflation*tax bracket, so you are guaranteed to lose to inflation with TIPS in taxable (unless there is deflation).

The question comes down to is which will do better under an inflationary environment – TIPS or Nominals/Munis in taxable. Do the advantage of TIPS still retain an edge, or do they lose that edge due to taxation.

Just looking for any research or analysis of this, but cannot fund anything to help.

Conventional wisdom suggests holding higher appreciating assets (stocks) in a Roth rather than a traditional IRA, with lower performing fixed income more appropriate for traditional IRAs.

Let’s not forget the Roth option, though, as it can play an important role for many people – those on fixed incomes (retirees) as well as for those with a more conservative investment philosophy.*

With a diversified portfolio, you are going to have some level of fixed income (conservative investors will have proportionately more). Where else can you get a guaranteed tax-free boost to conservative no/low risk asset returns from CDs and TIPS than in a Roth?**

With diversification, you likely have at least some fixed income both inside and outside of retirement accounts. If you can handle the Roth rules (like a possible 5 year holding period and being a certain age to withdraw more than the principal) you can benefit from fixed income being in a Roth.

With a 5-year CD at 4%, the taxable equivalent of it in a Roth account at the 24% tax bracket is 5.263% = 4/(1- tax rate) = 4/(1-.24) . The higher your tax bracket (and include state taxes), the higher the tax-free equivalent yield when in a Roth. Who needs munis? 😊

If you have fixed income in a traditional account and it has experienced a paper loss (due to rising interest rates and the mark-to-market handling of these assets) you can convert it (or a portion of it) to a Roth). So long as you don’t use some of the proceeds for paying the taxes (i.e., you have enough liquid funds outside of your retirement accounts to pay the taxes) you have parlayed it into an even higher yield as that paper loss is just that — when it comes due, you get the whole principal back.**

Some folks will say if you are in this position, you should be investing in the stock market for historically higher returns. Well, OK. I am not saying you should put all your guaranteed fixed into one retirement account or the other or even outside of retirement accounts, just to readjust your thinking.

Additionally, the stock market is a little richly valued these days. If you want more certainty, consider maximizing the work of your fixed income.

* If you have earned income, from a job, you can contribute to an individually owned Roth each year and take advantage of this process.

** This discussion is geared toward individually held fixed income assets (ie, not bond funds which do not have an end date and therefore no guaranteed return).

thanks for the info.

I have roughly 90/5/5 taxable/ira/Roth split, with Roth equity, ira total bond, and taxable 50/50 equity/muni, and am retired

I could convert my ira to a TIPS ladder (I agree with you on TIPS funds), but it would not move the needle much at all, and I then have the ladder to deal with and to worry about matching income with RMD’s.

100% equities makes sense for me in Roth.

I cannot find the tools to help decide if moving some of my Munis (all funds) into TIPS is worthwhile. Munis have been beating Nominals for the last 10 years even before accounting for taxes, and they broke even with TIPS after taxes over the past 4-5 years. This is not a long time period to base a decision on.

My intuition of what it means to “break even” was that the expected value of the cashflows of the TIPS should be precisely equal to the expected value of the cashflows of the nominal bond. But I was having trouble making the numbers work out.

The key piece I was missing was this: it is not quite correct that the breakeven inflation rate is equal to the nominal rate minus the real rate, as one often sees stated. This is an approximation; the exact formula is (1+nominal) ÷ (1+real) – 1.

If you calculate the breakeven in that way, then, indeed, the expected value of the nominal will exactly equal the expected value of the TIPS, if observed inflation is equal to the breakeven.

See “Inflation-Indexed Bonds: How Do They Work?” by Jeffrey M. Wrase of the Philadelphia Fed (1997), and the Wikipedia page on the “Fisher relation”, for more detail.

Interesting idea, but the Federal Reserve itself (and almost all other sources) define inflation breakeven as nominal yield – real yield for the same term.

I grant you the St. Louis FRED numbers use simple subtraction, as you say, but if you try that definition out on actual cashflows, you will see it does not give an exact result—it’s a little bit off.

My goal is to be able to say with mathematical precision what it means for a nominal and an inflation-adjusted bond to be “the same”, such that we should be indifferent to the choice between the two. (The subject of this web page!)

My definition is that the expected values of the two bonds’ cashflows are equal. (Is there a better definition? I am no expert here, but this one seems intuitive.)

Here is a toy example, which is very similar to the one in the Philadelphia Fed paper I cited (see p.5). I’ll use made-up 3-year bonds that pay annual coupons. Let’s say the nominal interest rate is 5% and the real interest rate is 2%.

Then the cashflows of the nominal bond are $50, $50, $1050. The present value of those cashflows, discounted at 5%, is $47.62, $45.35, $907.03, which sum to $1000, as expected.

Now the inflation-adjusted bond. First let’s use the breakeven inflation rate that your formula would suggest: simple subtraction of 2% from 5% suggests that if inflation is 3%, we should break even. But do we? Let’s see!

The 3% inflation-adjusted bond has cashflows of $20.60, $21.22, $1144.58. The present value of those cashflows, discounted at 5%, is $19.62, $19.25, $962.82. This sums to $1001.68—so the inflation-adjusted bond comes out slightly better than even with the nominal bond.

Now, I claim that the breakeven inflation rate is about 1.05/1.02 – 1 ≅ 2.941%. If the bond is so adjusted, its cashflows are instead $20.59, $21.19, $1112.67. The present value of those cashflows, discounted at 5%, is $19.61, $19.22, $961.17, which sums to exactly $1000. Presto!—we broke even.

Looking at the charts at 30,000 foot level, it appears that even when the variance was at its worst from the standpoint of investing in TIPS it was never worse than 1%. I think of TIPS as an insurance product against inflation. If I wind up giving up a little bit on return– so what! If I want to take risk then I put my investment into equities with a greater historical upside. Most people allocate a portion of their portfolio to equities, and a portion in bonds. The bond portion is intended to be stable, but if you have to worry about inflation then it is not stable.

Just one person’s opinion.

I agree.

It’s sinking in more and more how TIPs are a “quasi” zero coupon bond … that is the inflation part compounds. One could “hack” a secondary market TIPs and create a sorta kinda Zero Coupon TIP by buying the issue with tiniest coupon (i.e. .125 or something like that). Is my thinking right???

With low coupon rate, it is similar to zero coupon in that you pay taxes on phantom interest every year.

Also, low coupon rate treasuries and TIPS are a great tax-planning tool (keeps MAGI down) to minimize current year taxes while maximizing I-bond redemptions for college and for tax-efficiency.

So many experts in this forum – please correct mistakes in my thoughts for everyone’s benefit!

Well my thought was that by leaning this way (lower coupon TIPs vs. higher), you’d avoid reinvestment risk.

You still pay taxes on the phantom income though so how would this lower MAGI? The MAGI would be based on the delta between the zero rate and the “correct” rate if it wasn’t a zero. You can’t defer the interest until maturity, unlike I’s and EE’s.

You are correct. So this applies as a tax planning strategy to lower current year taxable income ONLY when one purchases treasury notes and bonds that are sold at a deep discount as the coupon rate is near zero (0.125% 0.25% etc.) thanks to past decades of low interest environment.

Deep discount bonds are taxed on the portion of deep discount upon maturity or upon sale (which involves a calculation of discount amount prorated and capital gains, if any)

For TIPS it wouldnt make as much sense due to phantom interest taxation every year.

Feel free to correct any mistakes, please

Hi David, Thank you for the great site.

I’m planning on building out a ladder to cover the difference between my projected annual spending needs and Social Security during retirement.

Currently I estimate that SS will cover 60% of my basic expenses and want to build a ladder of Nominals/TIPS to cover the remaining 40%.

With TIPS yielding >2% for all maturities today, it seems like a no brainer to build out the ladder with TIPS. In your article above you state that TIPS typically outperform nominal when the breakeven inflation rate < 2%.

In the secondary, today's 10 year nominal is at 4.347 and the 10 year TIPS is at 1.985, so the break even inflation rate is 2.362.

Given this relatively high break even rate, would you still preer TIPS over nominals for this ladder?

If you are building a ladder to meet specific future spending needs, the breakeven rate becomes less relevant. Getting 2% above inflation across nearly the entire ladder is an excellent way to meet those needs. But yes, the 2.3% rate is on the high end, meaning that TIPS are “more expensive” versus nominal Treasurys of the same term. Until a couple years ago, we had gone through a decade-plus of very low inflation, so a 2% breakeven rate often mean TIPS lagged. Now, have we entered a new inflation era? I’d say probably, and 2.3% doesn’t look unreasonable. But you never know …

Great site and helpful comments. I wonder if anyone could comment on the following “thoughts”. I have a substantial amount in VMFXX but want to build a 15 year ladder at the right time (soon). This is for income – my stock portfolio will be untouched during those 15 years. I’m thinking that I’ll build a short term (5 yr?) ladder using nominals assuming interest rates decline then stabilize, and then start building a longer term (10 yr) ladder with TIPS once the stabilization happens by rolling over the short term ladder as they mature. I realize we have no way to be sure 🙂 on inflation.

VMFXX, the Vanguard Federal Money Market Fund, has been a nice holding and it currently has a yield of 5.24%. I’m not a financial adviser, of course. So … I do think this is an excellent time to build a nominal / TIPS ladder through purchases in the secondary market. You will be locking in decade-high yields. This is what I have been doing, gradually, since last summer. The difference for me is that I have been targeting the longer maturities, in the 2029 to 2043 range, to hold to maturity.

I use VMRXX Money Market Fund which, as of now, has 7 day Yield of 5.27%. Vanguard tells me that this Fund has the highest yield among their Money Market Funds. If you go with is, please keep in mind that this not a sweep fund, meaning you will need to sell its units to cover the cost of your buys, such as US Treasuries, a day before or the same day, as I do, as the settlement day. I am good with little incovenience for the extra yield.

An interesting thought exercise might be to compare the total return of TIPS to that of IBonds with the same maturity length. I suspect the initial real YTM on the TIPS is the primary factor with some impact provided by IBonds’ inability to go below zero for a composite rate. For example, the Jan 23 TIPS’ total return was slightly less than the equivalent length IBonds, while the July 23 TIPS’ will be worth slightly more (both IBonds have a 0% fixed rate).

These factors (plus having IBonds in a tax deferred space coupled with optionality on their maturity) have led me to hold both. Cheers.

Thought exercise … no time for that. However, I have been working on an article about the 10-year TIPS that will mature July 15. All the factors are already set, since the CPI adjustments were announced last month. That TIPS (with a real yield at auction of 0.384%) had a nominal annualized return of 3.055%. If you bought an I Bond in July 2013 with a fixed rate of 0.0%, it so far has had a nominal return of 2.64%.

I’ll note: 2.64% + 0.384% = 3.024%, really close to the actual result.

Other facts: A 10-year Treasury note issued in July 2013 would have earned 2.56% annualized. Vanguard’s Total Bond Fund ETF, BND, had an annualized total return (including dividends) of 1.47% over the last 10 years. The TIP ETF had an annualized total return of 1.93%.

Buying that TIPS worked out well.

Dave, I would also suggest including the numbers for the Jan 23 TIPS vs IBond in your piece as a counterpoint. Using the numbers from eyebonds.info, the matured TIP returned a total of $1229 / ~2.08% per year while an IBond purchased in Jan 13 returned $1263 / ~2.36%. It appears to me the reason is the TIP was bought at a premium at auction ($1075.06 for a face value of $1000) with a real YTM of -.630. The two subsequent auctions for this TIP also had negative YTMs.

The point of this is that TIPS bought with negative real yields will generally lag behind IBonds of the same maturity. This conclusion may be a blinding flash of the obvious, but folks should recognize the potential drawbacks when investing in negative YTM TIPS especially when another investment exists that can do virtually the same thing. Your site covers both very well. Cheers.

Yes, it is clear that when TIPS of your desired maturity have negative real yields, I Bonds are the superior investment, even with a 0.0% fixed rate. And I Bonds get superior deflation protection. (This assumes no redemption penalty.)

The TIPS that matured in Jan 2023 had an annualized nominal return of 1.96%, versus 1.86% for the 10-year Treasury note. It auctioned with a real yield to maturity of -0.630%. A $1,000 I Bond purchased in Jan 2013 and redeemed in Jan 2023 had an ending value of $1,263.60, which works out to an annualized compounded return of 2.37%.

Hi David, First, your comparing nominal and TIPS return tables are very helpful, thanks!! 2: I own TIPS only in my and my wife’s IRA accounts, in fact, I started owning them after I luckily found your website and learnet more about them; 3: I own nomibnals in our taxable accounts; 4: On stating the obvious, each tax situation is unique so returns from TIPS and nominals will vary for everyone.

Finally, I want to share an observation that I just made after reading Nick Timiraos of WSJ article posted at 2:24pm today. Interstingly, post panedemic, well debated, neutral rate, and contrary to my thinking, is expected to stay low. This means the Fed will need to keep rates high until inflation comes down from 4.9% to around 2%. Barring unexpected events, which happens more often than we want to believe, so far, the Fed seems to be quite successful in bringing down inflation from 9.1% to 4.9% by raising interest rates by only 5% (it’s all relative, I have 80s in mind). If the trend of inflation going down remains intact or recession happens (thought Q2 GDP growth of 2.2% is looking way better than Q1 1.1% growth), we have a limited time (6-9 months) to get a decent income from current rates. The challenge will be on how to reinvest when current nominals mature….ok, our daughter is right about my living way too much in the future, well, too late, she could not pick her biological Dad….:)..thanks again for all the posts and exchanges..best!!!

15-jan-19’s inflation breakeven of 0.12% seems like an anamoly (for lack of better words). Six months before the market was thinking of an inflation rate of 2.49% and six months after 1.58%.

So if someone bought TIPS at that time they were guaranteed a real yield of 2.245% which is PRICELESS!

So if the annual inflation was in the range of 6.5% then the equivalent nominal yield for holding that TIPS will be 8.745% correct?

Besides numbers, below is what I am thinking as guidelines to determine whether to invest in TIPS or not.

1) Lower the breakeven the more attractive TIPS gets.

2) A real yield of 1.5% for 10 year is really attractive.

3) Don’t buy TIPS if one does not want to hold it for maturity. Trading in TIPS is not for a simple minded investor like me.

In this listing, the Jan 2019 TIPS matured in January 2019 and was issued in January 2009. That was in the depths of the financial crisis and investors were selling off everything. So an inflation breakeven rate of 0.12% was an anomaly, as you note. Inflation over the next 10 years ended up averaging 1.7%, but even then this TIPS did quite well.

I agree with your points 1 – 3.

Hi David, I’m new to this but am coming around to the view that, vis-a-vis TIPS, nominal treasuries are essentially for those who want to speculate on future inflation rates. Buying TIPS and holding through maturity locks in a guaranteed pre-tax real rate of return whereas nominals lock in a guaranteed pre-tax nominal RoR, with the real RoR fluctuating based on how actual inflation turns out relative the the break-even expected rate at purchase. For the investor who has no interest in speculating on inflation, is there some other reason I’m missing as to why he would choose to include some nominals in his portfolio? Thanks!

Nominals protect against deflation, and are excellent short-term investments. I like to own a mix.

Thanks, but deflation doesn’t affect the TIPS real RoR, right? And, if living expense move reasonably in line with inflation/deflation, it’s real RoR that matters, yes? If so, it seems like “nominals protect against (unexpected) deflation” is just the flip side of “nominals leave one exposed to (unexpected) inflation”, which gets back to speculating. I may be missing something, but I’m still not seeing why I should prefer a mix if I’m not interested in speculating on inflation. Thanks!

Consider: Nominal bond pays 4%, at a time of 2% deflation your real return is 6%. TIPS pays 1.5% real. TIPS lose out in this scenario.

Oh, for sure. I’m not saying nominals can’t ever result in better real RoR over TIPS. It doesn’t even take deflation for that to occur, just lower than expected (i.e. breakeven) inflation will do that trick. But that’s just speculating on actual inflation vs. market-projected inflation and winning. I’m asking for the investor who doesn’t want to bet against the market expectation and speculate on inflation, if there’s any reason to not just buy TIPS.

I’m fascinated by this insight (declaration, idea, thought) by Vesuvius. I think the investor who “has no interest in speculating on inflation” probably does have interest (no pun intended) in diversification of the risk of their income from bonds, notes, or bills. One way to diversify one’s risk, would be to both speculate on inflation and not to, in order to get the only free lunch there is (namely diversification).

But yes, if you aren’t interested in diversifying, then TIPS would eliminate one source of risk, that of inflation. If you want to diversify risk–the only ‘free lunch’–then buying both TIPS and nominal bonds would be one way to diversify that risk (I’m curious if anyone has thoughts on whether one should “split” one’s inflation/deflation risk diversification and buy 50%/50% TIPS and nominals, or if there is some other (smarter?) way to understand how much to diversify inflation/deflation risk–I suppose anything other than 50/50 is just a bet on one or the other (a bet on inflation lower than expected / deflation, or on inflation higher than expected, over the term to maturity)…

So I would say, rather than that “nominal treasuries are essentially for those who want to speculate on future inflation rates” (true, to a degree), that I’d rather say, “a split other than 50% TIPS/50% nominals” is for an investor who wants to bet on either lower inflation than expected (all the way to include deflation), or who wants to bet on higher inflation than expected. For those who **don’t** want to bet on inflation or deflation, one should hold 50%/50% in TIPS & nominals.

Does that make sense David, or Vesuvius?

I know you asked David or Vesuvius, but you questions are worth contemplating and sharing. I think a mix of TIPS and nominals is a good think. I acknowledge that we cannot know for sure if yields on nominals will go up or down in the future and we cannot know if there will be deflation in the future. Deflation seems contrary to historical norms and contrary to human nature, but I am not willing to speculate that there could not be multiple consecutive periods of deflation nor how deep they will be, but it seems like there is enough greed so that deep consecutive deflation is unlikely. It is probably good to trade up as often as it makes sense to do so (as in purchase higher yielding nominals and higher yielding TIPS whenever the math involved in doing so is beneficial).

Here is a topic you may have covered but some people may not know about and it may not be a good idea. See https://youtu.be/bSoZJJypSAQ

Buyer beware:)

Thanks for the post. The detailed information in the tables above is very helpful.