Summary

- The U.S. Treasury will offer a new 5-year TIPS at auction Thursday.

- The real yield looks likely to come in around -1.21%, which is pretty awful but isn’t a record low.

- The only way to judge this TIPS is to compare it with other very safe investments of similar term. How does it measure up?

The U.S. Treasury on Thursday will offer $17 billion at auction in a new 5-year Treasury Inflation-Protected Security, CUSIP 91282CAQ4. The real yield to maturity and coupon rate will be set by the auction, but we already know, the terms are going to look fairly awful.

Real yields (meaning yields above the rate of inflation) have declined mightily in 2020, dropping from about -0.05% on January 2 for a 5-year TIPS to -1.21% at the market close on October 16. That’s a decline of a whopping 116 basis points from an already low starting point.

A TIPS is an investment that pays a coupon rate well below that of other Treasury investments of the same term. But with a TIPS, the principal balance adjusts each month (usually up, but sometimes down) to match the current U.S. inflation rate. So, the “real yield to maturity” of a TIPS indicates how much an investor will earn above (or below) inflation.

We can say with certainty that CUSIP 91282CAQ4 will auction with a coupon rate of 0.125%, the lowest the Treasury will go on a TIPS. Its real yield to maturity should be somewhere around -1.21%, meaning it will underperform official U.S. inflation by 1.21% for five years. And that 133-basis-point gap between the real yield and the coupon rate will mean investors at Thursday’s auction will have to pay a rather large premium above par value, probably somewhere around $106 for $100 of value.

So, as I said, pretty awful. But in the current environment of ultra-low interest rates for safe investments, this TIPS should be considered “above average.” Why? Because it provides a hedge against unexpected future inflation.

The Federal Reserve has openly committed to forcing annual U.S. inflation higher than 2% a year, for an extended period of time, as long as the labor market remains weak. The Fed already is holding short-term rates very close to zero, and is buying Treasurys in the open market to hold down longer-term yields. This is “quantitative easing,” which, in effect, increases the U.S. money supply. In the longer term, combined with trade barriers and stimulus spending by the federal government, it could force inflation higher.

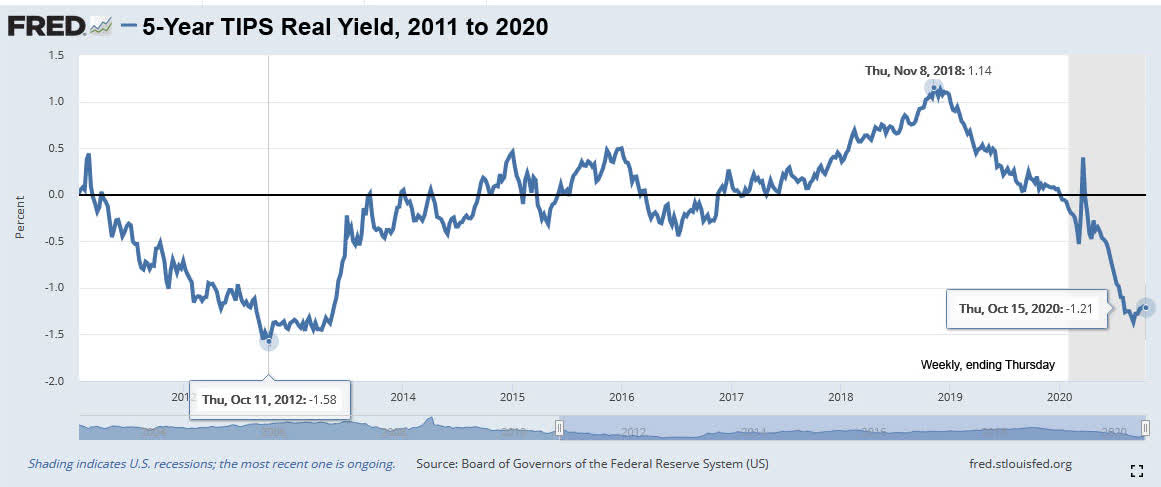

The Fed’s first phase of quantitative easing began in mid-2011, and that coincided with real yields dipping sharply negative for an extended period. Here is a look at 5-year real yields over the last nine years, a period of nearly continuous off-and-on Federal Reserve manipulation in the Treasury market:

Note that the current 5-year real yield of -1.21% hasn’t yet reached the lowest level of 2012, which actually dropped to -1.67% on September 14, 2012, according to Treasury estimates. So, could real yields continue declining? I’d say yes, but we could be nearing a bottom, unless the U.S. economy suffers a severe second phase of the pandemic.

Okay, what are the factors that make this TIPS offering attractive?

Inflation breakeven rate

With Treasury’s estimate of a 5-year Treasury note’s nominal yield currently at a woeful 0.32%, this TIPS with a yield of -1.21% would get an inflation breakeven rate of 1.53%, which indicates that the financial markets aren’t expecting inflation to rise higher than 2% anytime soon. The current U.S. inflation rate is 1.4%, and inflation over the last 5 years (ending in September) has averaged 1.8%.

Inflation expectations remain very low, and that’s surprising given the Federal Reserve’s adamant attempt to get inflation above 2.0%. And that makes this new 5-year TIPS an attractive investment, at least when measured against a 5-year nominal Treasury yielding 0.32%.

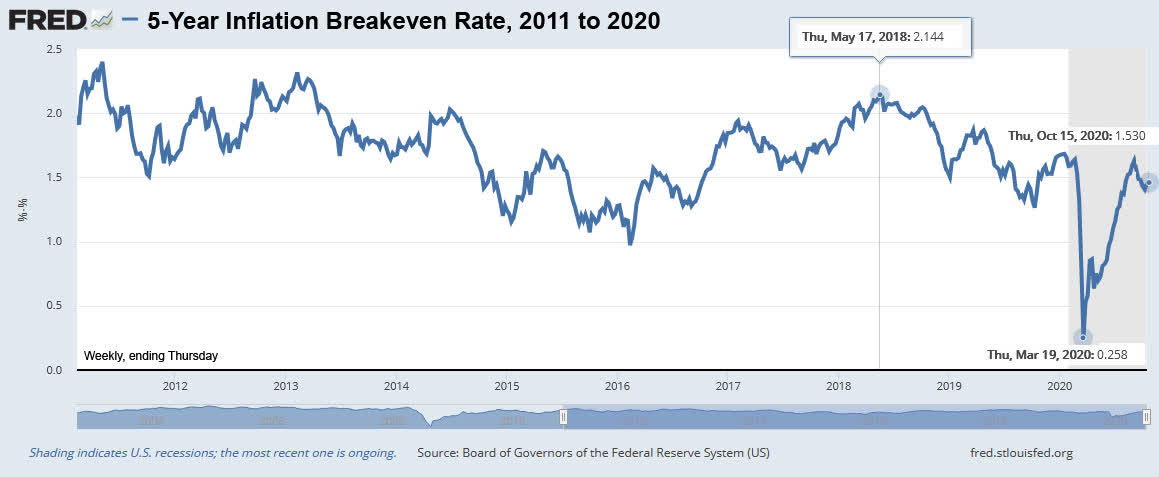

Here is the trend since 2011 in the 5-year inflation breakeven rate:

Despite the wild swing since February 2020, the current inflation breakeven rate is sitting in a range we’ve seen before, although fairly low. I think this should make the new 5-year TIPS attractive to big-money investors like central banks and pension funds. And even for a small-scale investor, this TIPS should look more attractive than the very low return of a 5-year nominal Treasury.

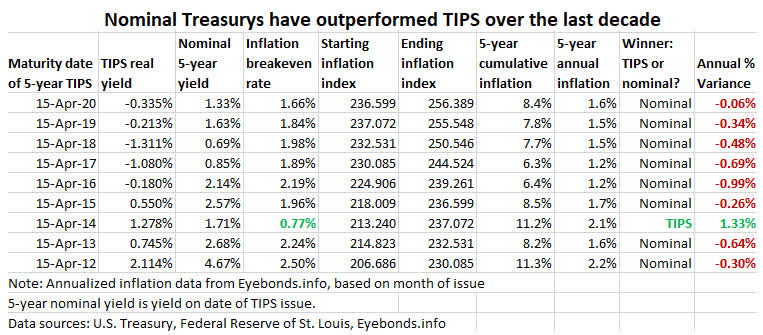

But I will point out that TIPS have under-performed nominal Treasurys for about a decade, because inflation dipped much lower than expected over that period. Much of that time, inflation expectations were hovering around 1.9-2%, while actual inflation only averaged 1.8% in the last five years. When inflation runs lower than expectations, TIPS underperform.

I track how each maturing 5-year TIPS has performed against its nominal counterpart, and the picture isn’t pretty:

However, keep in mind that today’s inflation breakeven rate of about 1.53% is historically low – and that indicates the potential for outperformance, especially if inflation begins exceeding expectations.

What are the alternatives?

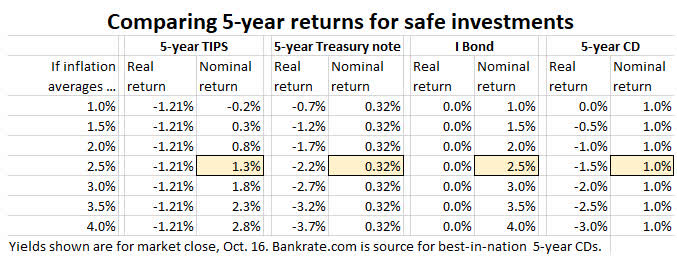

The five-year term opens up comparisons with several very safe alternatives, most notably the U.S. Series I Savings Bond, which currently has a fixed rate (equivalent to its real yield) of 0.0%. Because the fixed rate is combined with an inflation-adjusted variable rate, I Bonds will accurately track U.S. inflation and can be redeemed after 5 years with no penalty.

The I Bond’s real yield is 0.0%. This TIPS will have a real yield of about -1.21%. That means the I Bond has a 121-basis-point advantage over this new TIPS. The I Bond is clearly superior. But the problem with I Bonds is that the Treasury caps electronic purchases at $10,000 per person per calendar year, plus the opportunity for $5,000 in paper I Bonds in lieu of a federal income tax refund.

I Bonds are better than TIPS, across the entire maturity spectrum. But once you reach the purchase limit, what’s your next choice?

Another option is a 5-year insured bank CD, currently offering a yield of around 1.0% at several online banking centers. This is a significant improvement over the 0.32% yield of a 5-year Treasury note, and it pushes the inflation breakeven rate for this TIPS up to 2.21%, which I think makes bank CDs attractive despite the awful return.

If you look at the chart above, you can see that the I Bond is the clear winner in all inflation scenarios above 1%. The question then becomes: what is the second-best choice? For inflation scenarios below 2.21%, the bank CD is the best second choice. For inflation scenarios above 2.21%, the 5-year TIPS is the best second choice.

If you believe inflation could rise well above 2.21%, this TIPS is a clear second choice.

Conclusion

U.S. Series I Savings Bonds are the best choice for an inflation-protected investment, offering a yield about 121 basis points higher than this new TIPS, with a similar 5-year term (if you choose to redeem after five years).

Once you reach the purchase cap on I Bonds, however, this 5-year TIPS becomes relatively attractive as a super-safe investment offering insurance against unexpected future inflation.

Bank CDs will perform very well, even with yields around 1.0%, if we hit a deflationary spiral. However, I’d say that 1-year CDs, with returns around 0.70%, are more attractive than a 5-year CD yielding 1.0%. A lot can happen in five years.

CUSIP 91282CAQ4 isn’t attractive, but it could work for an investor looking for protection against strongly higher future inflation. The risk is out there, it’s true. And it is wise to plan ahead against that risk.

I’ll be posting the auction results after the close at 1 p.m. Thursday EDT. If you are interested in this TIPS, make sure to track the Treasury’s yield estimates, which are posted after the market closes each weekday. Yields dropped as low as -1.35% on August 26, so beware of falling leading up to Thursday’s auction.

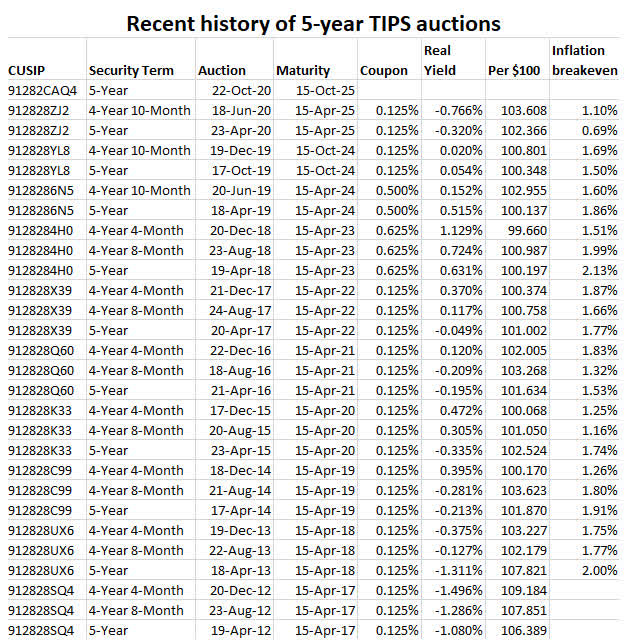

Here is a history of recent 4- to 5-year TIPS auctions, showing the rather wild fluctuations in real yield during this time of Federal Reserve manipulations:

The wait is over...one of the missing ingredients is the benefit of starting the minimum one year old for maximum…