By David Enna, Tipswatch.com

Any long-time reader of this site knows I try very hard to avoid political discussions and I discourage political rants in the comments section. This is a site about inflation protection and investing with a focus on safety.

Thursday night’s presidential debate was difficult to watch, no matter your political persuasion. Did we get actual policy discussions? No. The solvency of the Social Security system was raised by the moderators, but we got in essence, nothing of substance from the two debaters.

But I was interested to see a report Friday from Bloomberg that combined inflation and inflation protection into the debate analysis. This was the headline, and you can read the article free on Yahoo! Finance: “Barclays Says Buy Inflation Protection to Prepare for Trump Win.”

It is based on a research report from Barclays Plc. From the Bloomberg report:

With former president Donald Trump appearing more likely to unseat Joe Biden in the Nov. 5 election, the market should “be pricing in a considerable risk of higher-than-target inflation in the coming years, and this is from a starting point of our thinking they already offered structural value,” Barclays strategists Michael Pond and Jonathan Hill said in a note.

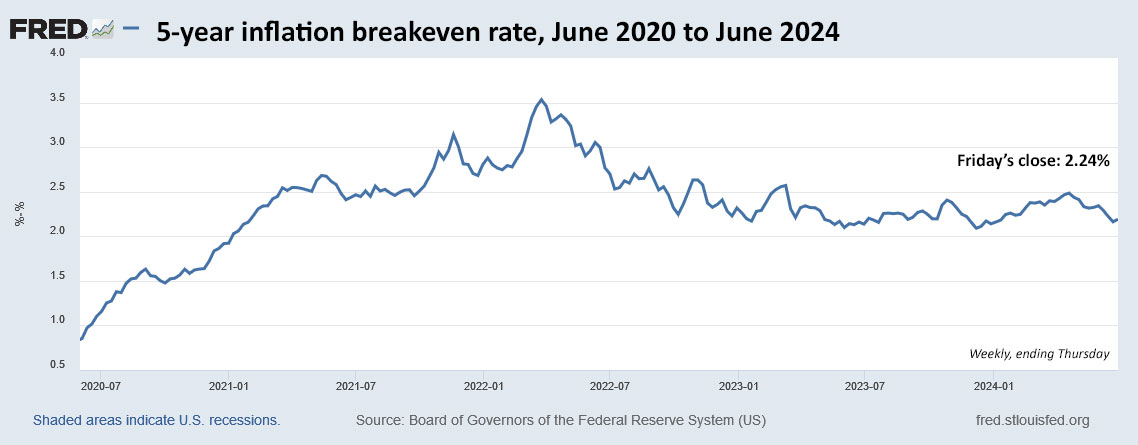

The simple trade, they wrote, is a wager that five-year Treasury inflation-protected securities, or TIPS, will outperform regular five-year Treasuries, leading to a wider yield spread between the two. That breakeven rate — representing the market-implied expectation for the average inflation rate of the consumer price index over the life of the securities — will widen to 2.5% from about 2.25% currently, Barclays projects.

The reasoning

The authors point to former President Trump’s proposed 10% tariffs on all imports, and likely even higher tariffs for imports from China. In addition, his plan for an aggressive effort to deport illegal immigrants could trigger labor shortages and wage inflation. He has also proposed across-the-board tax cuts, which would add to the U.S. deficit and potentially stimulate consumer spending.

(I)f the odds in the coming months continue to favor a second Trump term, “we would expect them to be embedded in the market via higher breakevens as the November elections approach,” Pond and Hill wrote.

A similar analysis was recently laid out in a letter published by 16 prominent economists, all Nobel Prize winners. They wrote, “The outcome of this election will have economic repercussions for years, and possibly decades, to come.” You can read that here.

You can read a detailed analysis of import tariffs imposed by Trump and continued by Biden in this report from TaxFoundation.org. From that report:

As of March 2024, the trade war tariffs have generated more than $233 billion of higher taxes collected for the US government from US consumers. Of that total, $89 billion, or about 38 percent, was collected during the Trump administration, while the remaining $144 billion, or about 62 percent, has been collected during the Biden administration.

Along the same lines, noted bond investor Bill Gross recently told the Financial Times that he believes a Trump victory would be “more bearish” and “disruptive” for the bond markets than the re-election of Biden.

“Trump is the more bearish of the candidates simply because his programs advocate continued tax cuts and more expensive things,” Gross said, although he noted that Biden’s presidency had also been responsible for trillions of dollars of deficit spending.

My analysis

I have been saying for several months that inflation breakeven rates seem overly optimistic, making an investment in a Treasury Inflation-Protected Security (current 5-year real yield of 2.09%) more attractive than its matching nominal Treasury (4.33%). And history is on my side. Inflation over the last 5 years, ending in May, has averaged 4.2%. And that is why we have seen a string of favorable returns from 5-year TIPS over the last several years:

I would add the possibility of Republicans controlling both houses of Congress and the presidency, which could — ironically — tamp down GOP efforts to control the federal deficit. Having a divided Congress can help control government spending and at least force compromises on policy.

In addition, Trump would likely name a new chairman of the Federal Reserve, potentially with a much more investor-friendly policy. In his first term, Trump consistently pushed the Fed to lower interest rates, and that would likely continue.

Both Trump ($2.2 trillion stimulus package) and Biden ($1.9 trillion) deserve blame for the recent surge to a 40-year high in U.S. inflation, along with Congress for approving massive deficits and the Federal Reserve for keeping interest rates too low for too long and then failing to end bond-buying quantitative easing.

The fact is, I believe that no matter which candidate is elected, we will see higher-than-expected inflation over the next four years.

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Comments on this article are now closed.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I am in favor of experimenting with tariffs to see how effective they are for raising government revenue as well as providing domestic companies a chance to compete. It’s true that tariffs are a wedge and could create inflation for some products but it isn’t inflation caused by erosion of the value of the currency. Any kind of tax deprives the consumer of disposable income.

Good points.

Those 16 Nobel Prize winning economists also said in a public statement in the Spring of 2021 that the $1.9 trillion Biden deficit plan was not inflationary. This happened after Larry Summers warned Biden not to proceed with the legislation.

This morning, I called Vanguard about the $100 fee and about what else may be happening there. Well, $100 fee is charged if all assets within an account are moved out of Vanguard, however, for partial asset transfer, they don’t chanrge the fee. You could, for example, leave $1 in the sweep account, they will not charge $100. Please double check on this before you believe my take on this.

If all assets in an Rollover IRA account are transferred, within 60 days, using Indirect Rollover then there is no $100 fee, In this case, you will be issued a 1099-R, but it will be nulified by the receipient plaform using cide G, and IRS will ignore the 1099. I believe that we don’t need to liquidate the assets before trasnfer, but I will double check before taking this route.

In the most unlikely event of Vanguard becoming insolvent, they have the standard SPICC Insurance plus additional, up to about $50M insurance. One of those instances when, for me, it’s good not be wealthy.

Their new CEO, first external candidate from Blackrock, starts next Monday, July 8th. Soon, we will hear more from him about Vanguard startegy etc. Independent of what may be happeing with Vanguard, I am trasferring our last account out of Vanguard. However, I will continue to hold lots of Vanguard products such as their ETFs, etc. …..this will require keeping an eye on them and others….best

Not sure why I see my typo error only after I post it…8(

I transferred my entire Vanguard account to Schwab. I can’t remember if I was charged a fee. I didn’t like some of the rules Vanguard has like the inability to buy inverse funds since its against their belief system. That should be up to me to decide. I also like Schwab’s tools much better

The general theme of your article is that a Trump win will cause higher inflation, labor shortages, wage inflation, higher deficits, and disruptive bond markets. Although you acknowledged that Biden has also contributed to inflation, supported trade war tariffs, and increased the debt, you emphasized that a second Trump term will be more disruptive than a second Biden term.

Particularly disturbing in the article is a link to a letter published by “16 prominent economists, all Nobel Prize winners.” You quoted from the letter, “The outcome of this election will have economic repercussions for years, and possibly decades, to come.” But, the quote is contextually deceptive because you did not say whether the Nobel Prize winners were referring to a Trump win or a Biden win. Clearly, they were talking about a Trump win.

The letter is an overtly politically biased and factually inaccurate hit piece on Trump. I am not a Trump sycophant, but the so called “prominent economists” detest and condemn Trump while heaping accolades on Biden and his agenda. Not a single criticism is leveled against Biden. The letter is short, shallow and devoid of any factual basis. Just because a person has been awarded a Nobel Prize is not evidence of high integrity, intelligence, or goodness. The six prize winners are equivalent to the 51 former “intelligence” officials who signed a letter saying that the Hunter Biden laptop “has the classic earmarks of a Russian information operation” despite the fact that the FBI had previously authenticated it.

You say that you are not interested in political discussions and political rants. But, your article and the included documentation show that you hold yourself above that policy. In summary, the article speculates on highly complex and unpredictable issues that are unknowable, and it engages in a cherry picking process that supports your biases. I thought you were better than this.

I disagree with your opinion. But thanks for the feedback.

With what do you disagree? Your sources are one-sided and biased. Balanced sources (and a subsequent balanced article) would judge the impact of either winner against the impact of the other. But I’m not sure we need that analysis — both candidates already have a record. Let’s look at the record and determine which policies have caused inflation to rise and which have not.

I second the comment above that you engaged in cherry picking sources to support your biases. A practice all too common today in journalism.

But most off-putting is your statement about deleting comments which you judge to be too political. If you write a one-sided political article you should accept the consequences in the comments. If you don’t want political comments then don’t write one-sided articles on political topics.

Tim, for any topic that touches on politics, the writer stands a high probability of being called biased. Fine. I want the discussion here to focus on inflation and Treasury yields and the policies that could affect them. This week, both Morgan Stanley and Goldman Sachs issued reports backing up Barclay’s contentions. The point is that there is potential for higher inflation with policies that supercharge trade tariffs, increase deficits and reduce the labor force. That’s my belief, but you do not have to agree.

You seemed to have touched a nerve with the radicals. David, you do a great job of being fair and balanced.

You and many other are confused on the terminology. “Radicals” are leftists that seek rapid change to society and “Reactionaries” prefer slower change. The author has already acknowledged in his words above “…the writer stands a high probability of being called biased. Fine.” Technically he is a radical; those that disagree are reactionaries. So be it. Since he already acknowledges in print that he is biased, how can you logically say “David, you do a great job of being fair and balanced.” You cannot have it both ways.

Sir, with all due respect, merely touching on politics did not inspire my comment. I would have withheld my criticism had you not sourced the letter signed by the sixteen disingenuous Nobel economists. The letter is propaganda and bears no resemblance to the truth. The truth is what your readers expect, and I encourage you to either justify the letter in detail, or simply admit that it should not have been referenced. I am happy to debate this with you privately by email if that is your preference. That said, your TIPS and I bond strategy advice is excellent. Your willingness to dedicate your valuable time and effort in order to provide this service free of charge is admirable.

Again, I appreciate the feedback. And now you see why I rarely venture into anything touching on politics. Comments on this article are have shifted to purely politics and are now closed.

I’m surprised no one has mentioned the most relevant data from Friday: according to the Treasury Department’s Daily Par Yield Curve tables, the yield on the 10-yr Treasury note went from 4.29 on Thursday to 4.36 on Friday (as I’m writing this on Sunday night, Bloomberg shows 4.39). The real yield on the 10-yr TIPS went from 2.03 on Thursday to 2.08 on Friday (as of Friday after hours, Bloomberg showed 2.11). The uptick in yields came on a day when the PCE report came in exactly in line with expectations and showed a continuation of the disinflationary trend. This looks to me like the bond market’s first reaction to the debate Thursday night, the inference being that the election could produce a higher-growth, higher-inflation outcome than was expected previously.

In case anyone has forgotten, it is instructive to review those tables to see what happened in November 2016. The 10-yr Treasury yield finished that month about 60 bps higher than it started, and the real yield on the 10-yr TIPS finished the month about 30 bps higher. At the time, this was called “reflation.”

RRC, this is just the sort of analysis I do almost every day, and then two days later, the entire trend gets reversed. It is definitely possible that the debate had an effect on longer-term yields, since higher yields are one potential result of a Trump victory. But we have a long way to go, along with potential Fed interest rate cuts. Monday will be interesting, and thanks for the heads up.

I’ve had this nagging little concern for a year or so that if the radical candidate in this election prevails, especially if his party takes full control of Congress, we may look back on discussions about diversifying among US-dollar stocks and nominal Treasuries versus TIPS as having missed the point. I think I recall Mr. Trump saying in the past that the best way for the U.S. to deal with its accumulated debt is to get rid of it by defaulting. It also worries me that a Supreme Court which seems to be on a roll of deciding that its own long-standing precedents don’t necessarily need to be followed. Could the Court muster five votes to agree that Congress, or the President by Executive Order, has the authority to change the terms of Treasury debt instruments?

Which is my way of saying that I wonder if we (or at least I) shouldn’t be looking at non-U.S. debt. I know that the U.K. issues inflation-indexed Gilts, and Australia and several of its states issue inflation-linked bonds. I think there are inflation-adjusted bonds issued by a variety of other national governments. I haven’t figured out a way for a U.S.-based individual investor to buy these in their native currencies. There are ETFs like the broad-based WIP or the single-country ILB, but I really don’t like bond funds; I prefer to buy individual bonds and hold them to maturity.

David, have you ever looked into non-U.S. TIPS analogs? Have any of my fellow Tipswatch followers actually invested in any of these bonds or funds? Anybody have any thoughts about the merits of foreign-currency bonds as a hedge against something dire happening to TIPS and I-Bonds?

I’m currently invested in Vanguard’s EM Bond ETF, VWOB, and it currently has a yield of 6.75%, but it’s total annualized return over the last 5 years has only managed a paltry 1.73%, but still above an even worse return of Vanguard’s Total Bond Index ETF at 0.29%. Now granted, 2022 was one of the worst year’s on record for bonds, which has really altered their long-term performance, but, as you were alluding to, is diversification outside of the U.S. really the best practice anymore, if U.S. TIPS are beating everything else? As all the pundits like to say, the U.S. is the “cleanest shirt in the pile of dirty laundry.” Debt-fueled spending around the world is excessive, and at some point, a day of reckoning shall come. I remember them talking about minting a trillion dollar coin during the debt ceiling debates, and poof, the debt is gone. Sort of like Biden is doing with student loans…poof, gone. The problem is, when you just start forgiving all of your debts, then you lower the value of everything, and consequently lower your national security. Currency valuations will be an interesting study going forward, for sure!

Last line about currency fluctuation is critical. Just to give you an example, I am geeting about 6- 7% interest on a CD like foreign investment product. However, their currency, relative to the US dollar, deteriorates around the same percentage, every year, so it’s a wash. And don’t forget the complexity with International taxes, Turbo tax can do only so much, especially with non-US TIPS. They are plenty complex just in the US. Also, in general, expenses are much higher when you invest international. Talking head promote it because they can not make much money in the US with zero transaction fee and ultra completitive expense ratio environment.

I am going to use the opportunity to get rid of my European and Far East ETFs, such as VGK , VWO (I think), …etc., as soon as their economies start to turn in the new rate cutting cycle.

Good idea…I “unbundled” my Vanguard International ETF’s (which included VWO), but I did stick with VYMI. I went with DBEF, XCEM, EWX, FLJH, DXJS, EPI, and SMIN. So far, so good, but yes, if the dollar weakens, then maybe I’ll move back into just one or two funds then. However, currency-hedged vs. non-currency-hedged funds perform about the same over the long-run. You are so right about fund managers pushing international with their higher expense ratios!

As you know, currency-hedged cost even more than non-hedged. Bid/Ask spreads are wider and most of the international funds, and they mostly have relativily limited liquidity. AUM for popular and well diversified US ETFs are over Trillions of dollars. So liquidity is great and they also have low tracking error relative to indexes. Now, my challenge is to find the right opportunities to sell them and not look back. The opportunity cost of missing on so many very attarctive investments here in the US is not worth considering international….I guess, I may be overly opinionated on this..but I don’t think so..:)

Another excellent thought and discussion provoking post, thanks David!! With rain and thunder storm underway here in Lexington, Massachusetts, I spent most of this afternoon reading all the 31, posted so far, comments. My actionable take aways, not in any priority, from all the reading:

Apologies for typos in my above post.

One thing a found a bit off. You’re all into the US and reducing international, but as far as equities go, the US has been the best game in town for many years. These things go in cycles. It looks like international equities are about to best US equities – IE the cycle may be reversing where you have a period where international equities will dominate US equities. Probably be a good idea to have some international equities in your equity allocation. US equities are overvalued too.

Thanks for your comment and input. Yes, valuations, such as P/E ratio and many other ratios, are lower for international equities than the US equities. ECB and a few other countries, such as Canada, have started cutting rates to help their economies grow, notwithstanding all the European political turmoil. I can go on and on on this but will spare you all. I am waiting for the cycle to show more life in International equities so that I can sell and get out of them. Medium to long-term, I believe staying within the US is the right strategy. I believe that the US economy will continue to outperform other econmies for a long long time.

You have to look at the whole picture, and not try to artificially remove what you don’t like. Politics is a big part of economics. Choosing a Fed Chair is a political decision, with big economic ramifications. Speaking of which, the Nobel economists David cites are predicting higher inflation under Trump, and some say that Trump will choose a Fed Chair who will lower interest rates. Uhh, that is not going to work. No Central Bank lowers interest rates in the face of rising inflation. (BTW, I attended a major university with some interest in economics. My conclusion is that economists are not scientists in any way, shape, or form, but are more like a lamer version of social studies teachers.)

As for my plan, I will stick with laddering T-bills (3 to 6 month). If inflation jumps higher, fine, T-bill rates will have to go up. If the Fed is reluctant to raise short-term rates in the light of higher inflation, inflation will rise even faster. Economics is sometimes called “the dismal science.” Well, it is dismal, but there is nothing scientific about it.

Regardless of who wins in November, our goal will have to be to do what’s best for ourselves and our loved ones. IMO, that means diversification. I have treasuries and CD’s with rates in the area of 5%. I also have TIPS with fixed rates ranging from about 1.6% to a bit over 2.2%.

All these people who pontificate on the future are no more knowledgeable than most of us here. In fact I would guess that the predictions of any 5 people here are probably more accurate in the aggregate than many of these experts.

My guess is that inflation will remain high but what do I know? I retired (early) 20 years ago. I”ve kept 17 years of my basic budget documents. At first I factored in 3% a year inflation, then 2% after the housing crisis, back to 3% recently.

How I was going to fund those increases was something of a muddle. But it has turned out that COLAs (pension and SS) and tax cuts (both Federal and local real estate taxes) have more than made up the 38% increase in my basic budget.

I would say, yes, use historical data to make your projections but more importantly, spend time understanding where your money goes and where its likely to be needed in the future based on your stage of life. Prepare to be wrong in your assumptions. I was concerned about health care costs before retirement but thankfully I have been healthy. Insurance of all types has turned out to be the biggest inflationary drag on my budget: it made up 14% of that budget 17 years ago, 24% today. Maddening because I almost never use it, no home or auto claims in 20 years.

I have been a long time Ibond investor and that’s about 11% of my portfolio. Not enough or too much? I don’t know, I’m interested mainly in the tax advantages and the fact that they are a stable savings vehicle for my grandchildren to inherit. At this point it would take Wiemar Republic type inflation to make any significant difference to me and worst case planning makes no sense, better to fret about nuclear war or climate change than inflation for me , personally.

My portfolio is 19% I-bonds, the rest CDs (which I have grown to dislike because of early withdrawal penalties which I knew about before buying) and laddered T-bills (which I now like). I shifted all my focus to buying T-bills, a few months before Buffet decided they were a good deal. Most of my I-bonds were bought when the fixed rate was about 3%, so those are looking pretty good. My total return on everything is 5.1%, completely risk-free, about a third in tax-deferred stuff. My annual income is more than it has ever been, thanks to higher interest rates. My expenses are not high, I don’t buy a lot of junk, so inflation affects me a lot differently than others.

You know what the average fed funds rate was in the last fifty years, 1971-2022, including the ZIRP years? Average was 4.86%, median 4.97%. If you look at the same numbers but exclude ZIRP years, the average 1971-2008 was 6.43% and the median 5.62%. There is a lot of volatility, remember Volker’s double digit rates. But my 5.1% return is very close to normal, historically speaking. That’s all I ask.

Patrick, you sound a lot like me … 1998-2001 era I-Bonds; some 5-year 5% CDs; GSE bond & CD ladders; an emphasis on Roth Conversions over the past 25 years; retired from my full-time job 20 years ago today! I also dislike substantial penalties for early withdrawal, so I started moving some RMD funds into no-penalty FDIC-insured 5+% CDs at Raisin.com.

William, those Raisin.com 5% and higher no penalty CDs have terms of 12 months or less, usually a lot less. Try 3 or 6 month T-bills which yield about 5.35% (higher than any no-penalty CD at Raisin.com). Also T-bill interest is state-tax free, important if you live in a high income tax state. If you buy a T-bill at auction (auctions are held once a week) and hold to maturity, I know Schwab will not charge any fees. You can also buy CDs at a broker which never have early withdrawal penalty fees, but you might win or lose some money on the secondary market if you sell before maturity. Also broker CD interest rates are almost always higher than any you buy through a bank. You need a brokerage account of course. I use Schwab. I hear Fidelity is good. I would avoid Vanguard as I have had a lot of trouble with their web site and people are complaining a lot about Vanguard’s new fees.

I am a big fan of 4 & 8 week, and 3 & 6 month US bills at Auction on Schwab, Fidelity, and Vanguard for the reasons you articulated. Yes, Vanguard website is not user friendly but it works once you know your way around.

I learned to buy T-Bills at Fidelity from watching Jennifer of Diamond Nest Egg on YouTube (I think she’s given a shout out to David from time to time too). She targeted 13 week T-Bills as being in the sweet spot, and explained how to stagger your purchases initially and then set them on auto-roll for monthly liquidity. So far, that is working wonderfully for me, and I have been enjoying rates in the 5.38% ballpark, almost 1% higher than my Capital One Money Market Savings Acct. And bonus: no State taxes!

Diamond Next Egg videos on YouTube are very good. As for Vanguard, I can only get so far in their website and I get a blank screen. I used all normal browsers, and it still happens. I complained about a year ago but they have done nothing. As of July 1 2024 Vanguard “Account closure and transfer fee: A $100 processing fee may be charged for account closure or transfer of account assets to another firm.” Two strikes and you’re out for me. I closed my account with Vanguard, and will never return.

Rolled my Roth from Vanguard to Fidelity and couldn’t be happier. Have it set up on recurring investments every Friday and it even buys fractional shares. Platform is much more robust than Vanguard too.

My guess is Vanguard is having serious problems. Not many successful business models suggest driving customers away. Unfortunately, Vanguard is privately held, so Vanguard customers won’t know what is happening until it is too late.

We know that Vanguard is known for low cost products and most of their popular products have been available on other, more user friendly, platforms. For the purpose of consolidation and simplification, I have moved all my accounts, except for one account, from Vanguard to Schwab and Fidelity. Your comment about the fact that they are private, which I knew, and their business may be in trouble, which I did not think about, is somewhat alarming. I did notice how unexpectedly and suddenly their CEO resigned. I did not know that they will start charging $100 to move assets to another platform; this is really bad. I will call them today to get a feel for all. Thanks for all the information.

Thanks Patrick, I’ll take a look at this.

Before I begin, I thank you for being one of the few altruistic people left in the USA. That being said, I believe you have entrusted your decisions to faulty sources. Yahoo is as far left as MSNBC. So you are starting with biased “facts”. The media is constantly citing xxx # of economists. Krugman and his Modern Monetary Theorists are propping up a myth that printing money can correct a recession. Definition of inflation is too much money chasing too few goods. Powell and Yellin are on the same page of the playbook when, in reality, they are supposed to be independent on one another. Additionally, 90+% of college professors donated to the party in power, a statistical abnormality. The economists mentioned have one thing in common with the Group of 51 influential “leaders” who signed a sworn testimony before the last election that the Hunter laptop was a political fraud – they are all lying to us (and show no shame for doing so). The greatest economist of all time, Milton Friedman is only mentioned in 8% of college classrooms. Notice any patterns here? Secondly, many of our long time allies are moving on in life because of our $35 Trillion debt. Saudi’s just announced a move away from petrodollars. BRIC nations are forming alliances without USA. Third, the actual basket of goods measuring inflation lacks many life essentials which skew inflation numbers downward. Plus, now that zero interest rates are gone, the government must borrow at higher rates and inflation will ramp up because entitlement increases will be forced upwards fueling more inflation. Fourth, most large banks are technically insolvent, foolishly holding a ton of 30 year low interest loans. Fifth, when the deck of cards collapses, we will have achieved the nations goal of equality- we’ll all be broke. Sixth, if anyone wants to read truthful economic or political analysis, I suggest you start looking for the people who have been silenced or banned for “misinformation”. One reputable source with regular scholarly articles is from Mises Institute (promulgating the philosophy of the Austrian School of Economics). Manhattan Institute also does excellent work. Many of the banned individual writers have moved on to Substack. Good reading.

Barclay’s isn’t the only one to make this prediction about higher inflation. Former Treasury official Robert Altman said so on Bloomberg’s Wall Street Week giving the same reasons.. In addition, the on-shoring of jobs and higher debt servicing (now more than $1 trillion annually) will lead to higher inflation.

The Fed’s 2% target for inflation is not realistic and by keeping it at that level delays the lowering of the Fed Funds rate and will likely lead to a recession. I expect the June employment report coming out this Friday to show the jobless rate ticking higher and a slowdown in job creation. The latest continuing jobless claims data from last Thursday showed it’s taking longer for workers to find new jobs.

Brent Fine

Chandler, AZ

I am with you, I try to keep politics out of my writing. However, it is important to notice that the Rs have not been the party of fiscal restraint in many years (starting wiith Reagan). while the Ds have not necessarily been good, (Rino Bush and Clinton actually were), they have at least tried. It is disingenuous to suggest that the Rs even attempt to “tapp down” deficit spending.

See https://shawnpheneghan.wordpress.com/2023/03/17/who-is-responsible-for-debt/

.

Clinton took us down the path of shorter term bond maturities to make his numbers look good because of the lower interest on the debt. That began the continuing path of America’s economic suicide. He also opened the door to China which made American companies show their true allegiance to money by producing there while devastating factory workers here and continuing to charge as if they were American made. Think of shoe companies. Then no politico had the backbone to force China to raise the value of its currency vis a vis the dollar to alleviate the imbalance of trade and keep everyone’s economy in the game. Ships are coming from China loaded to the gills and are going back to China virtually empty. That is unsustainable. John Deere this week just posted great numbers. Executives took a big chunk, shareholders too. Then they announced production is moving to Mexico harming innumerable American families. CEO of a major bank recently thought he deserved a severance of almost a billion dollars in addition to his regular monthly retirement income. The greedy keep getting greedier. Nothing is ever enough.

I think perhaps the only thing we can say about the future is that we’ll be entering a period of relatively high worldwide political, economic and environmental uncertainty. Inflation could return, but so could a rapid decline in economic activity or a liquidity crisis. Holding sufficient cash, plus a bit of gold, plus diversified financial and real estate assets (including TIPS) may be the most prudent approach. And maintaining a close network of trusted friends and family.

Be careful out there, everyone!

I have seen at least one research paper concluding that for the individual investor (but not necessarily for institutional investors), their bias should be strongly towards inflation protected bonds as opposed to nominal bonds, independent of the break even rate regime; or at best only weakly dependent on what the break even is.

Perhaps the individual investor’s preference should even be biased to 100% inflation protected and no nominal bonds at all. To the extent I could understand the research, this conclusion is due to the observation that only inflation protected bonds protect the individual investor against the risk of unexpected high inflation, which can devastate a retiree’s ability to consume in constant real dollars. E.g. inflation linked bonds protect against an inflationary “fat left tail” event in a way that nominal bonds simply can’t and don’t.

And on the other side of things, if the high unexpected inflation does not show up, worst case scenario for the retiree is perhaps a few percentage points less return over time, which is easily survivable.

Mr. Enna, I don’t know if you’ve ever blogged on this kind of research, but it would be great if you ever had a chance to do so, and give us your analysis of it.

Thanks.

The big risk of TIPS versus safe nominals like Treasury notes is severe deflation event. Nominals would greatly outperform TIPS in that scenario. In the more likely scenarios, I could lose out on a small amount of interest with TIPS if inflation is very low, and that is the price of my insurance policy against high inflation.

I agree with this as the risk for TIPS, but (personally) I place the odds of that event very low. At least in our current money system.

Since 1940, I count three years with negative annual deflation (1949: -1.0%, 1955: -0.3%, 2009: -0.4%). With many years you can count on inflation of >7%.

What about buying I Bonds? Seems five years should be likely to perform well.

I Bonds remain very attractive as an inflation-protected savings account, preferably held 5 years before redemption.

I know that most people my age (mid-50’s) that hope to see retirement on the horizon soon, have a seriously foreboding feeling when it comes to inflation, Social Security, and the deficits. Most of us feel as if we’ll never be able to stop working now, and not in jobs that we want because of ageism in the workplace (in fact, I heard yesterday that the share of workers age 75 and older will be growing). Neither candidate could articulate how to prevent Social Security from shortfalls. That fear is definitely causing me to look differently at my investment allocations and making me seriously consider recalibrating to more equity risk and bond-like proxies (such as real estate and utilities that pay good dividends), along with TIPS and shorter duration fixed income. My belief is if we have a divided Congress in 2025, that we’ll have another debt crisis and another downgrade and consequently weaker Treasury auctions, and thus higher and higher short-term Treasury rates. How else to you explain gold being at an all-time high right now? The entire world is aging and in debt (300 trillion +), but the world’s GDP is only (100 trillion +) and that will finally come home to roost at some point, perhaps sooner than later.

For what it’s worth, and I realize this is not possible for many people, I subscribe to the philosophy that money needed in 10+ years should be in a low cost S&P 500 fund, and money needed before then is in TIPS, held to maturity. I rebalance every year to keep this balance.

Yes, it definitely feels as if TIPS is the only intermediate-term bonds you should focus on right now. I’m probably 65/35 stocks/bonds right now, but will probably shift to more 75/25 with the extra 10% in stocks now being allocated to bond proxies with good dividends. I just don’t see how inflation could possible return to 2% when most of it is now coming from service-related sectors, due to the aging population needing more services (health care), travelling more, etc., and younger populations using services like Door Dash instead of saving money by cooking at home. A.I. will only be able to do so much in the services sector.

Hi Jason, if you feel the overall investing environment has gotten riskier, then a plan to increase your portfolio risk by increasing your allocation to equities is inconsistent with your observations. Increasing your portfolio risk increases your overall risk. It’s up to you what you do with your money, but selling bonds to buy equities–even so called “bond proxies with good dividends”–increases your portfolio risk and increases your overall risk.

Unless your overall risk tolerance has increased–and that doesn’t seem to be what your are saying here–if anything, you should sell 10-15% of your equities and buy intermediate TIPS or a TIPS fund with them.

Doing so will actually reduce both your portfolio risk and your overall risk.

Buying dividend stocks in place of fixed income does NOT reduce your risk. It increases your risk. And in a more normalized interest rate regime, with 5+% nominal and 2% (approximately) real rates in effect, there is absolutely no justification to do so.

Good luck.

Hi 500Madison, thanks for your reply, but I think you’re missing my underlying point, which is that the traditional approach to portfolio allocations should perhaps be reconsidered, because traditionally safe and less risky investments like bonds are becoming MORE RISKY when it comes to the prospect of higher inflation, higher debts, and higher taxes. Perhaps in the future, the only way to beat that is with riskier investments like stocks, but by leaning towards less riskier stocks. I respectfully disagree with you when say there is absolutely no justification to do so, when historically stocks have beat bonds (and inflation) over time (the great John Rekenthaler at Morningstar has published some good articles on this debate over risk in the long run, as has the great Jeremy Siegel of the Wharton School). Yes, I think TIPS SHOULD be part of the equation, but that is it, especially when you factor in that folks like me will most likely not have a “normal” retirement age now with Social Security shortfalls and longevity risk.

Jason, I did not mean to imply that you should not take more risk in your portfolio. That is a strategic asset allocation decision. However, the notion that high dividend stocks are a “proxy” for bonds in terms of their riskiness is simply wrong. It is not supported by the data. It was an idea floated by various talking heads, including Malkiel, when real interest rates were zero or negative on bonds.

It didn’t make any sense then, it makes absolutely no sense right now.

If anything, high dividend stocks may be a “proxy” for value stocks–but if so, they are a poor proxy. If you want to buy more equities and expose your portfolio to a different risk factor, you should consider buying small-cap value stocks. Not “high dividend” stocks.

If Siegel nor Rekenthaler ever stated that replacing bonds in your portfolio with high dividend stocks makes your porfolio less risky, those statements are not supported by history or research. I suggest you re-read what you think they said, and if you do, you will likely find their positions to be much more nuanced than at first glance. Certainly, if they did take such a position, I would imagine it was when real interest rates were very low or even negative a few years back, or more generally during the period following the Great Financial Crisis.

After 2022 we are in a completely different interest rate regime where investors can now easily get real returns on nominal and inflation protected fixed income at or exceeding 2%. That is a totally different scenario then when high dividend yield stocks were being touted as “bond proxies.”

Good luck.

500madison, you are twisting my words into a your more nuanced belief of what I’m actually saying. I never said “high dividend stocks,” I said stocks with “good dividends.” High dividend stocks are absolutely more risky, than say, stocks in the “dividend growers” factor. I should have been more specific there, and said to aim for stocks (or ETF’s like VIG) that are going to give you a decent dividend along with capital return too. Also, I never claimed that Rekenthaler or Siegel said to replace bonds with stocks. Their articles mostly compare all-stock portfolios vs. traditional stock/bond portfolios in regard to volatility over the long-run, and their research shows that stocks are clearly the winner if you can stomach the volatility. What my point was is that because of the current and potential future environments being more volatile in the sense of higher inflation, higher taxes, higher deficits, and “higher for longer,” rates, people living longer, etc., the traditional academic approaches may not be the best answer right now, and referring to folks like Rekenthaler and Siegel can help you make that decision. As for risk interpretation, that is in the eye of the beholder (and stomach, lol). You say that high dividends stocks are risky. Well, Vanguard’s High Dividend Yield ETF, VYM, has a total annualized return of over 11% for the last 5 years in a higher inflationary environment, while Vanguard’s Total Bond Market ETF, BND, has had a total annualized return of 0.29%, and the iShares ETF TIP, has had an annualized total return of 2.24% over the last 5 years. So obviously, the REAL RISK has been to be over-allocated to BONDS. Those are stark differences that should be given much higher consideration now when you’re talking about traditional approaches to allocation, which still should include TIPS. The real question is: how much TIPS is going to get the job done?

I find articles like recent Bloomberg to be of little value. Both sides of the political debate perform too much cherry picking of data and I find it to be dishonest.

There are dozens of variables that bear on inflation, and I have yet to see any one from academia model these correctly. (But, please keep trying!)

Permit me to play their game and cherry pick just a few inflationary varialbes to gaslight that turns their arguments around completely.

On the immigration impact on inflation, we cannot focus on the open border as being panacea for wage inflation. We have long ignored structural labor problems in this country that are highly inflationary (and difficult to measure). We need more skilled technicians and folks with BS degrees. The increase in illegal immigration certainly can hold down the cost of lower skilled service labor inflation; however, it does nothing to increase the supply of engineers, nurses, lab techs, HVAC techs, high school math teachers, airline pilots, plumbers, etc. Likewise, bringing in tens of millions of immigrants increases the demand for all of our essential services and safety net programs. Local governments, hospitals, schools, transportation systems, utilities, etc. are straining to assimilate our new residents– how can this not be inflationary. Our economy will have to provide some place to live for these folks– and we have real serious shortage of affordable housing in most parts of this country.

Weather we keep current Fed Reserve board or get a new one. They can take interest rates back to zero for another 12 years. Homeland Security can swing opens the border with open arms or shut it down like the Berlin wall—- whichever party is in power— I have little confidence we can find the needed skilled labor to build houses, keep our transportation and electrical systems efficient; or staff our medical facilities.

”Inflation over the last 5 years, ending in May, has averaged 4.2%.”

Although it’s factually correct, is it really fair or predictive to cite the average inflation rate for the past five years when included in that number is the post-pandemic spike in inflation to over 9% due mostly to supply chain issues, not government spending or policy? The latter had a nominal impact o inflation according to economists, with the former primarily responsible

Absolutely true. I would expect inflation in the next 5 years to run in the 2.5% to 3.0% range. Inflation over the last 10 years, which includes fives years of low inflation, averages 2.8%. It could be lower in the next five.

There are many economists who disagree with the notion that supply-chain issues were major contributors to pandemic related inflation. They believe that the likely culprit was a flawed discretionary monetary policy that was focused on stimulating the economy, when significantly restraining the money supply was the correct strategy.

I agree that either way, TIPS are a great call.

Neither the Dems or the GOP have shown any interest in debt reduction, and that is a huge problem. We know that Trump is the Republican nominee, but we do not know who will be the Democratic nominee. It could be Biden, Harris, Newsom, Whitmer, M. Obama, etc. Making unbiased predictions on what any of them might or might not do, or speculating on inflation and interest rates is extraordinarily difficult, if not impossible. I will ignore the noise and stay the course by maintaining a diverse portfolio.

We created the debt game and pay em off with value we create sometimes out of thin air. Somebody gonna foreclosecon the USA? As with the consumer borrowing was necessary for our high standard of living for most, not just the Lord’s and Ladies.

You need to change the debate to Thursday. You said “Focus on policy, like we didn’t get in Wednesday’s debate.”

Fixed, and thanks for the careful read, all the way to the last line!!

Oops! One other little typo – an extra “l” in the headline word Barlclay.

“Senior moment” … thank you