By David Enna, Tipswatch.com

We are halfway through the I Bond’s interest-rate-setting period, with the next reset coming on Nov. 1 — or more probably on Halloween Day, Oct. 31. On that day, the U.S. Treasury will announce both a new fixed rate and inflation-adjusted variable rate for the U.S. Series I Savings Bond.

The new fixed rate will apply to I Bonds purchased from November 2024 through April 2025. The fixed rate is crucial because it remains with the I Bond until it is redeemed or matures in 30 years.

The inflation-adjusted variable rate will apply to all I Bonds for six months, no matter when they were purchased. When combined with the fixed rate, it forms the I Bond’s composite rate. As things stand today:

- I Bonds purchased through October 2024 have a fixed rate of 1.3%.

- The current variable rate is 2.96%.

- And that creates an annualized composite rate of 4.28% for six months.

Now the bad news …

It’s early to make a projection, but after looking at the numbers I would guess that both the I Bond’s fixed rate and variable rate will be falling at the November reset. A lot will depend, of course, on where real yields (which are currently falling) and non-seasonally-adjusted inflation (also falling) end up in the next three months.

The fixed rate

The Treasury has no announced formula for setting the I Bond’s fixed rate. TreasuryDirect provides only this cryptic information:

The Secretary of the Treasury, or the Secretary’s designee, determines the fixed rate. The rate is based on market rates that have been adjusted to account for the value of components unique to savings bonds. These include the early redemption put option, tax deferral feature, deferred purchase feature, and Treasury’s administrative costs.

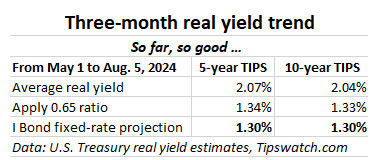

After years of monitoring this fixed-rate decision, (and getting help from clever Bogleheads) I have settled on a formula for forecasting what the Treasury is likely to do. The idea is to look at average real yields of 5- and 10-year TIPS in the six months leading up to the rate decision, and then apply a ratio of 0.65 to those averages.

The formula recently has been accurate when applied to the average for 5-year TIPS, but I like to look at the 10-year TIPS as a backup.

Just before the Treasury’s last I Bond reset on May 1, real yields were at annual highs for 2024, hitting 2.29% for both the 5- and 10-year TIPS on April 30. For the next two months, real yields remained fairly elevated, holding above 2.0% through the beginning of July. But then the decline began, which has accelerated in recent days as the Federal Reserve moves closer to cutting short-term interest rates.

On Tuesday morning, both the 5-year and 10-year TIPS were trading with real yields of about 1.74%, down 55 basis points from the April 30 high.

Interesting thing … if you look at just the three months from May 1 to Aug. 5, the I Bond’s fixed-rate projection holds at the current level of 1.3%.

But … what if real yields continue at this 1.74% level (or lower) for the next three months? If that happens, the I Bond’s fixed rate is likely to fall to 1.2%, or lower.

Conclusion. My feeling is that we are likely to see lower real yields in the next few months, so I am going to assume that the I Bond’s fixed rate will be reset in November to a rate lower than the current 1.3%.

The variable rate

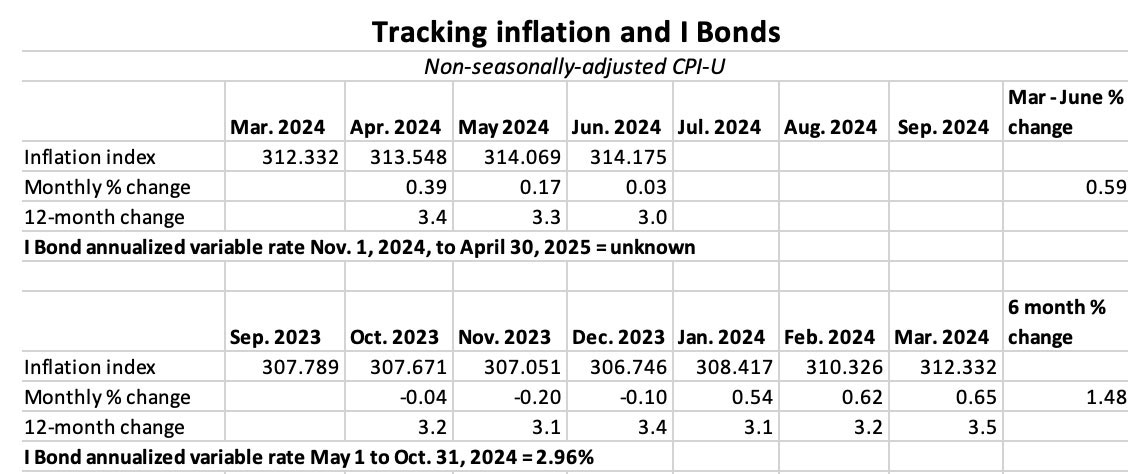

Inflation has been slowing in recent months, falling from an annual rate of 3.4% in April to 3.0% in June. (Inflation over the last six months ending in June was 2.4%, which is high for six months. But in the last three months it was up only 0.59%.) The slowdown can be seen in the three months of data we have so far for calculating the I Bond’s new variable rate:

So far, inflation from April to June would translate to a new variable rate of 1.18%, with three months remaining. Because of recent trends, I would guess inflation will average no higher than 0.20% a month for the last three months, and an even lower number seems likely.

Part of my reasoning is that inflation in August 2023 surged higher by 0.44% and then 0.25% in September 2023. I doubt we will see numbers that high this year, so keeping up with 2023 will be tough. Notice that inflation in June 2024 was up only 0.03%, compared to 0.32% in 2023. We could even see a month of deflation in July to September 2024.

Any way you look at it, the I Bond’s variable rate appears likely to fall from the current 2.96% at the November reset. Of course, inflation is full of surprises, so we can’t be sure.

Conclusion

At this point I’d guess that both the I Bond’s fixed rate and variable rate will be lower, creating a composite rate well below the current 4.28%, possibly somewhere around 3.0% to 3.6%.

What does this mean for I Bond investors?

The good news is that three months of high-ish real yields should hold the I Bond’s new fixed rate above 1.0%, even if real yields decline further. In my view, a fixed rate around 1.0% is attractive.

The bad news is that the potentially lower composite rate is going to scare off I Bond investors. It shouldn’t — because in the long term the high fixed rate is the goal.

By mid-2025 we could also see nominal T-bill rates falling to a range below 4.0%. If the I Bond’s fixed rate can hold at 1.0% or above, I would be a buyer in 2025, even with the lower composite rate. But I would also be likely to turn over some remaining I Bonds with very low fixed rates. Those could end up with a six-month composite rate around 2.0% to 2.4%.

Of course, I could be totally wrong. Nothing is certain. The good thing is that this is a very early, mid-term look at potential I Bond interest rates. So the real answer is to sit back and wait to see how things develop.

What do you think? Post your ideas in the comments section.

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Pingback: September ibond Interest Rate 4.28% | Keil Financial Partners

Pingback: U.S. annual inflation fell to 2.9% in July, lowest rate since March 2021 | Treasury Inflation-Protected Securities

1% real yield sounds pretty good considering how low rates were on cash savings prior to 2021.

I can’t just yeet $10,000 into I-bonds without sacrificing emergency fund liquidity…but it’s nice to know even if it’s 1% fixed and 3% composite, it’s still going to make more than my credit union’s money market account. So I’ll probably keep dropping a few hundred bucks into I-bonds each month as I’m able, maybe stack it up a little extra in October and skip the last months of the year if I can. Not the end of the world if I can’t though. It’s still pretty a pretty good deal.

Thanks for running this site! Very helpful!

I decided to follow your advice and increase my inflation investments (TIPS plus I-bonds to 10 or 15% of my investments. I was at 7% but that included only I-bonds. The first thing I did over the past year was to sell all my I-bonds that had a zero fixed rate and reinvested the max last year and this year into ones that did have a fixed rate. I then took some of my IRA money to buy a ladder of TIPS, – 10, 9 and 5-year on the secondary market, to get back up to 7%. I bought mostly the longer dated ones in June and early July to take advantage of the probable lowering of treasury rates. So far a good decision.

The question is what to do now – I-bonds or TIPS or more of both? I just turned 80 so I’m not overly concerned about long-term inflation.

It sounds like you are looking at a 10-year term for your investments, so both I Bonds and TIPS would work for additional purchases. If you think you would need to tap into that money in the future, then I Bonds might work better. In retirement, you might have to raise money to buy I Bonds, a problem you wouldn’t face in your IRA account if you just reallocate.

Thank you. I have enough savings outside of my IRAs to buy more I-bonds but I won’t be able to until next year, then we’ll know better where inflation and interest rates are headed. I will add more TIPS this year to my IRA to bring my allocation up to 10%

I would say the good news of the fixed rate staying at 1.0% outweighs the bad news – fewer I bond investors.

David – I see a lot of comments that investors are going to ‘roll over’ lower performing I bonds into the currently higher performing I bonds. But what if you are already fully invested for the year in I bonds? Should the lower performing and 0% fixed I bonds be rolled into something else? TIPS? Treasuries? Money Market? All of which could create tax consequences that the I bonds would not have in the short term.

People talking about doing roll-overs before November are probably planning to use the gift-box strategy, which requires a trusted partner. Once the new fixed rate is set in November it will be available for purchases through April 2025 and the purchase cap will reset.

But yes, a lot of people tell me they are selling out of low-fixed-rate TIPS and buying T-bills, which is a fine short-term strategy but possibly a bad long-term strategy, especially after the tax hit of redemption.

I was planning to buy more I Bonds next spring based on current real yields, but forgot about the gift box strategy. Now I’m debating whether to redeem my April 2023 bonds to purchase gift I Bonds with the 1.3% fixed rate. (I already bought my full allocation in April).

How long would it take to break even if I redeem 0.4% fixed rate I Bonds to buy more at the 1.3% rate? I may do a gift box purchase in October but wait until 2025 to redeem any 0.4% I bonds when the lower variable rates take effect.

Dave, I’ve been reading TIPSwatch for over 2 years. My question is this, is it wise to sell all my bonds with 0% interest and purchase bonds today with the existing rate or wait until the change in November? Didn’t want to think about it before because of tax issues I might incur by redeeming them since the 0% bonds are over 10 years old. Guess the other question is what’s the best solution so as not to incur more taxes than I need to pay.

This is always going to be a personal decision. One factor is if you are in the “accumulation” phase (before retirement) or “spending” phase (after retirement). I Bonds are a tax-deferred savings account and I plan to spend this savings before most of my I Bonds mature. My first targets would be I Bonds with 0.0% or other low fixed rates. But if you don’t need the money and don’t want to pay the taxes this year, just continue holding them.

Thanks for the advice. I’m in the accumulation phase right now with a 10 year window to retirement. Even if the rates keep dropping and your analysis holds true, I didn’t want to miss out on the opportunity of getting rid of the 0.0% and getting a better rate even at 1%.

If, as David observed, you are “accumulating” as partial protection against future inflation, then, since I Bonds continue to earn for 30 years (or until redeemed, whichever comes first), in my opinion there’s no particular reason to dump bonds with a 0.0% fixed rate unless (1) you need the cash for spending right now or (2) you need the cash from older I Bonds with lower fixed rates to buy new I Bonds with a higher fixed rate, i.e., you haven’t got enough dedicated money to hold both.

Meanwhile, although the 0.0% fixed rate on those old bonds is obviously nothing to get excited about, they do still include all the inflation earnings of the years since they were originally purchased, and are compounding accordingly.

My wife and I buy I Bonds every year, having also set up multiple accounts (individual, individual trust, joint estate planning trust) to increase the total potential annual purchase amount. But we continue to hold all our zero-fixed bonds as well, although, as David observes concerning his own approach, those will probably be the first to go when we eventually start redeeming.

A lot of people seem to think “I’ll redeem my zero-fixed I Bonds because I can do better in the stock market.” (Well, perhaps just a bit fewer people are thinking that during the past week of surprising stock market turbulence.) But the purpose of I Bonds and TIPS is not to beat stocks. It’s to accumulate a holding whose principal is guaranteed at all times by the national treasury, and whose earnings are guaranteed in advance to track a particular measure of “inflation”–neither of which can be said of stocks.

I’ve been accumulating I Bonds for the last 13 years. When I first started, we were in a deflation period which didn’t make much sense except to me. Having the backing of the treasury was a better bet for me to keep my principal intact. I made small purchases due to my personal circumstances so my holding was not substantial.

It was four years ago that things changed. Being in a better position, I’ve been able to increase my monthly purchases. I was convinced that redeeming the zero % bonds and getting a better interest rate was a good idea.

After contemplating your reply, you’ve made me realize something else. It doesn’t make sense to redeem them and having my earnings taxed versus having the earnings compound and increasing it’s worth. Redemption in retirement is a much better idea. Thank you for your insight!

People that buy I bonds are risk adverse so many are thinking, I’ll get rid of the 0% IBonds and get a good fixed income alternative. A short duration corporate bond fund will earn over 6% as the Fed cuts rates. 0% IBonds are weak underperforming assets. You might get under 2% for the next couple of years.

First: It’s seems a bit odd to be advocating short-term bonds when just a few years ago the Fed was suppressing interest rates to lows not seen in the lifetimes of many people. Short interest rates are quite pleasant right now, but that’s the whole point: their term is short. There’s no way of predicting their future course.

Second: If, for example, at the next Treasury reset, the fixed rate on I Bonds went to an all-time high of 5% (in our dreams) before inflation, there’s still a limit on the dollar amount of I Bonds that can be purchased in any calendar year. And a year passed without a purchase is a year lost, since it’s not possible to retroactively buy I Bonds for a previous calendar year. So people who are stockpiling I Bonds with an eye to LONG-term inflation protection, instead of SHORT-term gains from asset-hopping, will “take ’em as they can get ’em.” (I’m ignoring the gift box approach, which doesn’t radically change the dollar limit issue.)

Third, a grammatical note on an error frequently seen in chat forums: The correct word is risk “averse” (no d). It comes from the same root as “aversion,” meaning to have a distaste for something. For example: “He’s risk-averse because he just hates adverse outcomes.”

The strategy of I Bonds is to keep accumulating. The assumption is that US monetary policy cannot avoid high inflation. Therefore, having a large stake in I Bonds will capture that inflation.

I agree with your analysis of I-bond fixed and variable rates trending down. Of course, who knows. Oil could double and we’d all be in the soup.

As I still own 0% fixed rate I-bonds I will be looking to exchange them no matter what the rate is.

So it seems that a good strategy might be to purchase a large dollar amount in a gift box for a spouse at the current fixed rate and deliver it over the next few years. Is there a down side to such a strategy other than the (unlikely?

possibility that the fixed rate might go higher over the next few years?

Yes, the gift box strategy works best when the fixed rate is high, as it is now. The potential negative — if you stack too many $10,000 allocations — is that the fixed rate will rise in the future and stay high. So you might need to sit on those gift boxes until yields come down.

I’d recommend waiting until October to decide on using the gift box strategy. At that point you will have a lot better idea of where rates are heading.

From a long-term view, buying I Bonds before November 1, whether directly or through the gift box strategy to secure a 1.3% fixed rate, is definitely the thing to do. There’s not much reason for a short-term investor to do anything other than sell 0% fixed rate I Bonds.

Short-term investors won’t even be glancing at I Bonds if T-bill rates hold up. T-bills are a better short-term investment, in my opinion.

This is where I’m at. I’m mid-30s so I’m heavy into the stock market with about 13% of my new worth in cash equivalents as emergency savings that I’m trying to get a better return on. I jumped into I-bonds a few years ago with everyone else, never knowing about them before.

About half of my cash is now I-bonds, and when I considered increasing my investment a couple of months ago, I opted for T-bills instead because of the higher rates.

As long as they stay anywhere near 5% I’ll stay there, and will have to decide if I want to giftbox more I-bonds from my savings account in October.

James, for your purposes, and at your age, I think T-bills probably fit your needs better. I am not a financial advisor, of course, so that is just my opinion. The 5-year holding period for I Bonds (to cash out without penalty) limits their appeal as a short-term investment.

The penalty is a downside, although for a couple years there the returns were so high it was worth it even with the penalty! I’m happy to stick with the I-bonds I have long term, especially since (I hope) I’ll never have to actually spend the ‘second half’ of my emergency fund and build up that tax deferred savings.

What is the maximum that can be held in a gift box for a single person? I know only 10K can be given in a year, but could i buy more now and say give 10K in 2025 and another 10K in 2026? Always informative to read your analysis. Thanks.

There is no limit on gift box purchases for an individual (hopefully a trusted partner), but you can only distribute $10,000 of original value per year per person because of the purchase cap.

David, Thanks for all of the I-bond info, I find it very informative. My question is regarding gift box strategies. Is there a limit to the dollar amount that can be held in a gift box (e.g. for a spouse) at any one time?

Dennis, as I noted above, there is no limit to gift-box purchases. The limit applies to the year of delivery, when only $10,000 of original value can be delivered to the recipient each year.

You note the annual limit is $10,000 of “original value”. So if the I-bond has accumulated interest of $300 for example, would you be able to deliver the I-bond worth $10,300 without exceeding the annual limit? I also assume if you deliver prior to holding for 5 years, you do not forfeit 3 months of interest?

Thanks you for your reply.

Correct. The entire proceeds are delivered and the 5-year penalty isn’t triggered unless the recipient redeems.

Glad to have picked up $25,000 worth of I-bonds back in April ($10k was a gift-box by a trusted person). That strong fixed rate will be key as inflation subsides (unless it returns when rates are cut, though I think none of us want to see that)

I also did my first-time-ever gift box purchases in April. I *might* consider another set if real yields plummet before the end of October. I don’t think that will happen, though.