By David Enna, Tipswatch.com

If you’ve been overpaying estimated taxes all through 2024 with the intention of purchasing paper U.S. Series I Savings Bonds in 2025 … it’s time for a new plan.

Reporter Susan Tompor of the Detroit Free Press last week discovered a little-noticed press release from the U.S. Treasury declaring an end to the tax-refund issuance of I Bonds, beginning on Jan. 1, 2025.

The decision ends the Tax Time Savings Bond program, which was started in 2010 to give tax-filers the ability to buy paper I Bonds in lieu of a federal tax refund. The program was the last way to purchase any kind of paper savings bonds, which otherwise went all-electronic in 2012. Treasury listed several reasons for the change:

- “This option was costly and not frequently used.”

- “The mailing of physical savings bonds was also subject to fraud, theft, loss, and delays.”

- Only 35,000 tax filers each year bought paper I Bonds, representing 0.03% of tax filers, and less than 10% of Series I bond purchasers.

- Sales of paper I Bonds through this program made up less than 1% of all I Bond purchases.

Treasury also noted that taxpayers who received an extension to Oct. 15, 2024, on their 2023 tax filings will still be able to purchase paper I Bonds with a refund using IRS Form 8888. I am assuming very few people will qualify for that last-ditch opportunity.

And finally, it noted that despite the end to the tax-refund program, the $10,000 per person per calendar year purchase will not change.

You may continue to purchase up to $10,000 of series I bonds in a calendar year.

Reaction

I support this decision, but it should have been paired with an increase in the electronic purchase cap to $15,000, at least. Back in February 2022 I suggested that the Treasury raise the cap to $20,000 while also eliminating the paper I Bond tax refund.

When I Bonds were first created in the fall of 1998, the purchase limit was $30,000 per person per year, and the Treasury even allowed credit cards to be used for purchases with no fees. (Air miles!) However, the Treasury determined about 98% of all savings bonds were purchased in amounts under $5,000. This triggered a new policy in 2008: a $5,000 limit per calendar year.

The current limit of $10,000 per person went into effect in January 2012. If that $10,000 limit had been adjusted for inflation since 2012, it would be about $13,700 today.

I never used the paper I Bond strategy because in my opinion it wasn’t worth the hassle. But it was widely used by many people back in 2022 when the I Bond’s variable rate began the year at 7.12% and then rose to 9.62% on May 1, 2022.

As things stand today I doubt many people were planning on triggering the strategy in 2025, when the I Bond’s composite rate could fall to something like 3.4%, down from the current 4.28%.

Paper I Bonds are getting difficult to cash at many banks because of fear of fraud. So that means for ease of ownership, the paper I Bonds should be converted to electronic form, which is another hassle. Read this.

The gift box strategy continues

Instead of using the tax-return strategy, many investors have been using TreasuryDirect’s “gift box” to make additional electronic purchases in a calendar year, to be delivered later to a trusted partner. In its press release, the Treasury reinforced that the gift-box program is continuing:

Can I still gift someone a series I bond?

Yes. You can buy a series I bond as gift electronically in TreasuryDirect. Bonds bought as gifts are registered in the name of the gift recipient, and do not contribute to your $10,000 purchase limit (note: the $10,000 limit still applies to the recipient in the year they are delivered).

I added the bold text in the above quote as a clarification. Full instructions are here.

The gift-box strategy requires a trusted partner, such as a spouse or adult relative. So it won’t work for everyone. Investors can also add to their holdings with electronic purchases through trusts, or business-owner strategies.

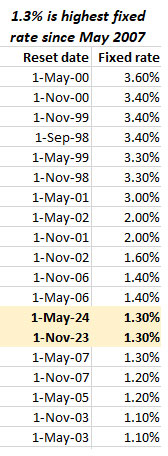

I don’t sense a lot of enthusiasm right now for investing in I Bonds and certainly the fervor is well below the mania of two years ago. But, because the I Bond’s fixed rate should hold above 1.0% at the November 1 reset — and 1.2% or 1.3% seems more likely at this point — gift-box purchases will continue to be potentially attractive, both before the November reset and into 2025. A fixed rate above 1.0% is sound, even if the variable rate is rather weak for six months. The fixed rate holds for the full 30-year term of the I Bond.

Today, the I Bond’s fixed rate is 1.3% and the 5-year TIPS has a real yield of 1.70%. That is a 40-basis-point spread, which is reasonable given the I Bond’s advantages of easy ownership, tax-deferred interest and rock-solid deflation protection.

If the 5-year TIPS yield continues to decline, the I Bond will look more and more attractive. But that is a topic for another day.

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep or the display breaks on the mobile site. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Pingback: Treasury is ending its Payroll Savings Plan for purchasing savings bonds | Treasury Inflation-Protected Securities

Pingback: Deciphering TreasuryDirect’s mysterious gift-box email | Treasury Inflation-Protected Securities

Who do we complain to about this decision. They couldn’t have waited until enacting the rule next year before people plan their withholdings?

When inflation was high, there was a bipartisan bill to increase the limit to $30,000 in the years when CPI was above 3.5%, but now that it has fallen below that, it seems to have died on the vine. https://www.congress.gov/bill/117th-congress/senate-bill/4952

I wonder if this shift will mean that the Treasury stops doing their calculations based on the $25(?) dollar bonds – I recall reading an article on this site about that being their likely methodology

I would guess not, since the tax-return paper I Bonds were issued in $50 increments, but the minimum for the electronic version remains at $25. Here is more on the calculation: https://tipswatch.com/2022/09/06/lets-try-to-clarify-how-an-i-bonds-interest-is-calculated/

We are from the government and are here to help you . . . . . .

You are, of course, quoting Saint Ronnie Reagan’s definition of “the most terrifying words in the English language”–which nevertheless didn’t stop Saint Ronnie from relishing his place at the top of that very same government.

But the national treasury offers inflation-indexed bonds–which it didn’t have to do, and which many countries don’t do–and for people wanting some kind of hedge against future prices, those bonds, whether in paper form or electronic alone, are indeed a “help.”

The current I-bond offer of 1.3% over inflation guaranteed for up to 30-years is still a good stash for cash

I see the “justifications” being offered by Treasury for discontinuing the tax-refund-as-paper-I-bonds option, but ever since I became aware of the option (and have used it for quite a few years), it was never clear to me whether Treasury was actually printing new bonds on a “made-to-order” basis for each taxpayer, or just trying to rid itself of a large inventory of paper bonds previously printed but never sold, after which the option was someday going to be discontinued in any case.

My wife and I have been overpaying our federal estimated income tax each year in order to get paper I Bonds in addition to our allotments of electronic bonds, but then each year we also file the TreasuryDirect paperwork to convert the paper bonds to electronic in our joint trust account. Because of the chronic understaffing/underfunding of the TreasuryDirect operation, this can take many months between paperwork submission and completion of the requested conversion. Just in the past couple weeks we were pondering, “Maybe we should stop buying paper I Bonds. $5,000 a year in extra bonds isn’t going to make a big difference in the future, and it just doesn’t seem worth the trouble.” . . . Well, no more back-and-forth debating that subject now, since Treasury has made the decision for us.

I don’t think the Treasury has been unloading stashes of pre-printed I Bonds over the last 14 years. But issuing electronic I Bonds through TreasuryDirect is a much more cost-effective enterprise. The paper savings bond was a relic of the past, and its days were numbered. I know all about this, since I worked for newspapers for 39 years.

Every paper bond has a Treasury secretary signature on it. In all the tax return paper bonds I have received up to 2024, I have never seen a signature newer than Geithner (2009-2013). He was secretary when paper bond sales were discontinued. My experience, at least, aligns with a story that they haven’t printed new stock since 2011.

Or either the program was continued to protect someone’s job or the printing department and now they have all retired. It’s hard to believe that this is being done to save money. Since when has the government been concerned about that? And something as trivial as printing and mailing a piece of paper.

I bought bonds with tax refunds too so I am opposed to this decision but I am pretty heavy in I bonds and my income is drastically reduced due to retirement so the government is probably doing me a favor for weaning me off more I bonds.

They will still need some employees to convert the outstanding paper bonds to electronic entry. Hopefully, they don’t get lost in the mail.

For those of us that took your advise and did the 3 mo / 6 mo TBill roll a couple of years ago…….What now? Continue with the program or transfer out? I’ve been trying to extend longer but the dip in yields has made the shift difficult since we’re use to plus 5%.

I am still rolling over staggered 13- and 26-week T-bills. I bought the 26-week last week at 4.865%. Still fine, in my opinion. Extending the duration won’t help much with the 1-year now at 4.38%.

Currently the 1-year Treasury is at 4.44%. Is that not worth locking in right now? And what is your opinion about locking in the current 4% 2-year Treasury rate? I’ve been rolling over 4-week Treasuries for two years, and don’t know what to do now! Thank you, David!

I bought some three year 5% broker CDs last month, but these are now being offered at only 3.9%. I will stick with T-bills for the following reasons. We have seen inflation head fakes before. Assuming the Fed has some impact on the economy, lowering rates will stoke inflation, leading to higher rates. If Harris gets in, the Democrats’ spend spend spend regime will stoke inflation. If Trump is elected, his tariffs will stoke infation. 5% is the average fed funds rate over the last fifty years. Arguing that the Fed is tightening at 5% is just plain stupid. It is a neutral rate. Volker’s 14% fed funds rate was tightening.

I actually bought $30,000 of I-bonds using a credit card at a bank in the early 2000s. I got a fixed rate of just over 3%. You cannot do any of that nowadays. I get the feeling the government is no longer much interested in the savings bond program. We seem to be witnessing a death by a thousand cuts. I would not be surprised if they ended all new purchases.

BTW, the $10,000 annual maximum is ridiculous. As David and some of his readers have shown, there are workarounds to exceed the $10,000 limit. But there should be no annual maximum.

There has to have some kind of limit or else the program will fail. The government isn’t under any obligation to the public to provide I Bonds.

I agree that the program needs a limit, and $15,000 a year would be acceptable to me. Savings bonds are for small-scale investors. TIPS are there for the more sophisticated investors, and many people invest in both.

Agree that, since the creation of Savings Bonds, they were intended for smaller investors. (Said with a smile: I’m old enough to remember receiving Savings Bonds as childhood gifts, an idea probably more psychologically attractive to the adult gift-giver than to a kid who might have preferred to have a new Superman cape or an extra caboose for the model train layout.)

I have no particular opinion about what the annual I Bond purchase limit ought to be, but I’ve always though it strange that the government issues these bonds automatically linked to a measure of inflation, but the annual limit itself is NOT automatically adjusted for inflation.

I understand the argument that mailing of physical savings bonds was also subject to fraud, theft, loss, and delays. But why couldn’t they have switched to allocating electronic bonds instead, which are in the words of the same press release, simple, safe and affordable?

Pingback: Treasury Direct Ending Tax Refund via Paper I-Bonds Option - Doctor Of Credit

As always, grateful to you, Enna, for sharing this. I’ve been using this strategy to shore off some additional $. I use a minuscule % just to keep up with inflation, not profit (as long term care savings). Bummer, Treasury is not going to allow this in 2025. I do concur that they need to raise the I-Bond amount we can buy to $15-20/year.

I did the paper option one year including conversion. Very cumbersome PITA. Was hoping to hold my purchases for at least 5 years but with the Trump tax cuts sunset at the end of 2025 and higher rates available in the current bond market may be time to cash out pay the taxes and move on. Small piece of the puzzle but hate to be earning squat right now.

Darn it! I was one of the 35,000…. 😦

Likewise. Only 0.03% of taxpayers is even lower than I thought. I purchased $15k of additional I Bonds with my tax refund over the last three years. Admittedly, I was starting to debate whether to continue that strategy next year. At least now I have one less decision to make.

Me too! I guess I shouldn’t be surprised that we are so few – every time I told people I used my refunds to buy paper I-bonds I was met with puzzlement

When the “great recession” struck, interest rates plummeted to near zdro for waaaay too many years,; then, rates came back to a much more investor pleasing level. Unfortunately, it appears the Fed is going to kill the goose that laid the golden egg.