By David Enna, Tipswatch.com

Reality is beginning to settle in on the U.S. bond market. Even as the Federal Reserve continues to cut short-term interest rates, longer-term yields have been rising in recent weeks as the market:

- Calculates the potential deficit risks of a Trump presidency.

- Figures the possible effect of tariffs on U.S. inflation.

- Observes a decently strong U.S. economy and labor market.

- Ponders why risky asset classes like Bitcoin have surged 34% higher in two weeks.

- And beyond all that, sees the U.S. Treasury continuing to borrow a lot of money.

As a result, mid- to longer-term Treasury yields have been rising over the last several weeks, as shown in a 56-basis-point rise in the 10-year real yield since mid-September. This surge could continue because the bond market is dealing with uncertainty. Bond investors don’t like uncertainty.

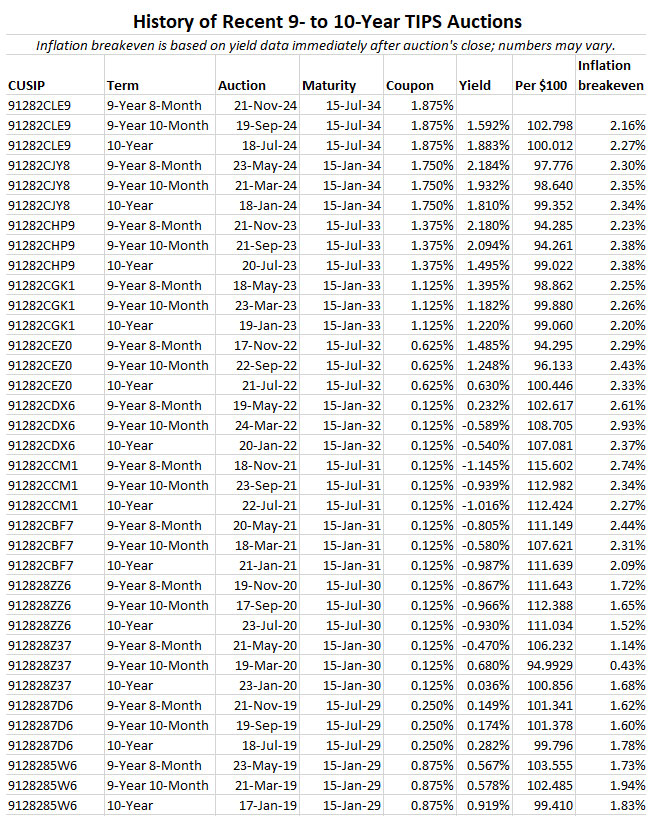

Amid this drama, the Treasury on Thursday will offer $17 billion in a reopening auction of CUSIP 91282CLE9, creating a 9-year, 8-month Treasury Inflation-Protected Security. Some history:

- July 18. The originating auction for this TIPS got a real yield to maturity of 1.883%, which set its coupon rate at 1.875%, the highest coupon for this term since July 2009.

- Sept. 19. The first reopening auction got a much lower real yield of 1.592%, the day after the Federal Reserve made a surprise decision to cut short-term interest rates by 50 basis points.

Now, two months later, the 10-year real yield has surged to 2.10%. CUSIP 91282CLE9 trades on the secondary market, and this weekend I am seeing price quotes right in the 2.10% range. Of course, things will change a bit before Thursday’s auction. An investor in this TIPS can also buy it at any time on the secondary market, of course.

Definition: The “real yield” of a TIPS is its yield above or below official future U.S. inflation, over the term of the TIPS. So a real yield of 2.10% means an investment in this TIPS would provide a return that exceeds U.S. inflation by 2.10% for 9 years, 8 months.

Here is the trend in the 10-year real yield over the last 15 years, showing that while yields are off the highs of October 2023, they remain in a historically high range:

As for the future, who knows? It’s in the realm of possibility that 10-year real yields could climb to somewhere around 3% (as we last saw in January 2003). That seems unlikely, but if deficits soar while the U.S. economy is surging it could happen. However, if the economy dips into recession, both nominal and real yields will decline.

In the 15-year chart above, note the tiny shaded area indicating the very brief pandemic-triggered recession in 2020. One brief recession in 15 years is rather amazing. So … are we due?

Pricing

At Friday’s close, this TIPS was trading with a discounted price of 98.02. It is discounted because the real yield of 2.10% is above the coupon rate of 1.875%. In addition, it will have an inflation index of 1.00473 on the settlement date of Nov. 29. With that information, we can estimate the investment cost of a purchase of $10,000 par value:

- Par value: $10,000

- Actual principal purchased: $10,000 x 1.00473 = $10,047.30

- Cost of investment = $10,047.30 x 0.9802 = $9,848.36

- + accrued interest = About $70.

In summary, the investor would pay $9,848 for $10,047 of principal and then receive inflation accruals plus an annual coupon payment of 1.875% for the next 9 years, 8 months. The accrued interest would be returned at the first coupon payment on Jan. 15. This is an estimate and conditions will change by Thursday.

Inflation breakeven rate

With the 10-year Treasury note closing Friday with a nominal yield of 4.43%, this TIPS currently has an inflation breakeven rate of 2.33%, higher than recent auctions of this term. Not a big surprise … this reflects the market’s uncertainty about future inflation. Over the last 10 years ending in October, inflation has averaged 2.9%, the highest 10-year rate since 1999.

A simple rule for me is that a higher inflation breakeven rate indicates that a TIPS is “more expensive” versus the nominal Treasury. In this case, I have to admit, a 10-year Treasury note paying 4.43% looks pretty attractive. But I’d still prefer to invest in the TIPS to get the future inflation protection.

Here is the trend in the 10-year inflation breakeven rate over the last 15 years, showing that the current rate of 2.33% is in the “highish” zone:

Some thoughts

I bought this TIPS on the secondary market on Oct. 29 with a real yield of 2.008%, so I am not in the market to buy more. I am now awaiting the auction of a new 10-year TIPS on Jan. 23, 2025. That TIPS will be my first (and possibly only) purchase for the 2035 rung of my TIPS ladder.

If you have a brokerage account, you can buy this TIPS at auction this week, or any time on the secondary market when you see a real yield you like. The advantage of the auction is that small purchases (the minimum is only $100 at TreasuryDirect) get the high real yield, but you won’t know the yield until the auction completes. The advantage of the secondary market is you can see the exact yield you are purchasing, but you may face a small penalty for buying in a small amount.

In my opinion, any 10-year TIPS with a real yield of 2%+ is attractive. It is a good target for investing. If you are buying at auction, you can follow the real yield of this TIPS on the secondary market on Bloomberg’s Current Yields page. Both the bond and stock markets are volatile right now, so things can change.

This TIPS auction closes Thursday at 1 p.m. EST. Non-competitive bids at TreasuryDirect must be placed by noon Thursday. If you are putting an order in through a brokerage, make sure to place your order Wednesday or very early Thursday, because brokers cut off auction orders before the noon deadline.

I will be posting the auction results soon after the close on Thursday. Here is a history of auction results for this term over the last 5 years:

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

David and anyone else who cares to respond:

What are your views on how far a TIPS ladder should extend out into the future in terms of the buyer’s age?

My wife and I are already retired, so 30-year TIPS, if held to maturity, would extend way beyond reasonable life expectancy. On the other hand, even brand new 10-years maturing in 2034 and later would be going pretty far “out there” in terms of our own age at maturity.

So far we’ve bought only I Bonds because of their ease of redemption at any time, and the fact that they’re non-marketable securities with stable principal regardless of when we eventually die. But keep thinking we should also be buying TIPS, especially with spare money in Roth IRAs.

In case it makes any difference in the answer, we don’t have a “bequest motive” to leave behind a lot of money to anyone else. Our primary goal is just to meet our own expenses for the rest of our lives.

Thanks.

It’s a great question. My TIPS ladder extends to 2043, when I will be 90 years old. I probably won’t make it. My wife probably will. I have thought about adding 2044, but my preference lately has been to focus on 2034 now, 2035 next year and so on. In other words, 10 years out. But the ladder does now include years 2040 to 2043.

FWIW I maintain a rolling 10 year tips ladder, assuming an S&P index fund is a reasonably good bet for a 10+ years timeframe. I’ll be buying the new 10 yr in January for this purpose. I’ll stop this approach once I sense the grim reaper is on my trail.

It’s really a personal decision based on how long you think you might possibly live. Fidelity projects to age 93. Some people would say if you have longevity in your family and don’t otherwise have serious health issues you might want to project into the low 100s or even beyond.

How long your TIPS ladder should extend into the future depends on how much risk you want to take that you will outlive the ladder. You can get an idea of what that looks like at this website, USA Longevity Illustrator

As an example, a 70-year-old couple, nonsmokers, in average health have a 50% probability that one will make it 22 years, a 25% probability that one will make it 26 years, and a 10% chance one will make it 29 years. Given these values a 30-year TIPS is not so far out for them.

Although it’s still early, it certainly makes it less likely that I will purchase my 2025 allotment of I Bonds in January as waiting until May, and taking advantage of the short term interest rates which so far are holding steady, may be the best option.

They way my 2025 maturities are spaced out, It’s likely I will buy in January and then again later in the year, possibly the July 2035 TIPS. The danger is that real yields start declining (which isn’t happening yet).

2% above inflation on US Treasury backed dollars is certainly good and safe by long term measures.

No one knows if rates will keep going up. If a trade war (or actual war, for that matter) sends us into recession, you may wish you had made all those tips purchases already. But maybe not…

Good point. No one really knows. I might just keeping moving forward with my purchases. I plan to do a few each day until I am done. Selling existing positions in stock as I go. Thanks!

I cannot thank you enough for the education. I have started building a tip ladder in my IRA that starts on my RDM year. I have purchased the first 2 yrs. I just learned that I can purchase the 2035 rung by waiting for the Jan 25 10 yr auction. I assume this is also a possibility for the 2036 and 2037 rungs.. just wait instead of following the tipladder created on the wonderful website you made me aware of.

Another question. Since long rates are rising, am I correct that I can take my time filling the rungs of my ladder (not purchase all at once)?

I maintain a 10 year TIP ladder and plan to add to it in the January auction. However, this jump in real yields make me wonder if I should buy now (or at the reopening) to lock in the current rate even though I will get 6 months less of the interest. I think we may be a peak uncertainty now, making this the opportune time to lock in the yield. Also, if these rates hold here, the new coupon could be higher and I am not interested in the current interest payments, so would prefer this coupon rate. Any thoughts on the tradeoffs of buying this week versus 2 months from now?

I understand, since I did buy the July 2034 TIPS two weeks ago. But I still plan to buy in January, and probably will do that even if real yields drift a bit lower.