By David Enna, Tipswatch.com

If you are an account holder at TreasuryDirect, one of your “duties” each January is to go on a hunt for your 1099s, the extremely important (and ruthlessly obtuse) tax forms the Treasury hides away deep inside the site.

You will get nothing in the mail, but you will get an email that is easy to miss.

The 2-minute video (which was produced several years ago) is actually helpful, and it plays on YouTube, so you can watch it right here:

Last week I was in TreasuryDirect looking for information and I saw 1099s for the 2024 tax year were now available. (I had not received an email as of yet, but it should be coming soon.)

As the video notes, if you are part of a couple with separate accounts, or if you have linked accounts from converting paper I Bonds, or child accounts, or separate trust or entity accounts, you will need to go to the linked accounts and get separate 1099s. In the case of a spouse, you will need to log out and re-login to that separate account to find the second 1099. Here is what TreasuryDirect says:

It is important to check ALL of your accounts, as a separate Form 1099 will be created for each one. If you have established Custom, Minor-Linked, or Conversion-Linked accounts, you must access each account to print the Form 1099 for that account.

However, if you use your TreasuryDirect account simply to buy savings bonds (I Bonds or EE Bonds) and didn’t redeem any or have any mature in 2024, there will be no taxable transactions and you won’t have 1099s. You will see this on TreasuryDirect’s ManageDirect page:

TreasuryDirect is NOT going to mail you these forms. You need to hunt them down.

Important: Once you are inside the account section of TreasuryDirect, never click on your browser’s back button. If you do, you will be booted out of TreasuryDirect and you will have to log in again. To navigate, either click on the top row of tabs or click “return” at the bottom of most pages.

Here is the basic step-by-step process for finding each set of 1099s:

- Log into your TreasuryDirect account on this page. Click “Next.”

- Enter your account number and click “Submit.”

- After you enter the account number, you will get a message that a verification code has been sent to the associated email address. Open the email, copy the code and paste it in the box. Click “Submit.”

- Enter your password and click “Submit.”

- Now you are on your MyAccount page on TreasuryDirect. From here you can click on your Investor InBox in the upper navigation to see further instructions. The message will be titled “Tax Statement Notification.”

Important tax information for the recently concluded tax year is now available. The Form 1099 may be accessed through the ManageDirect tab in your TreasuryDirect account. A Form 1099 will NOT be mailed to you.

- Next, click on the “ManageDirect” link in the upper navigation. Under the heading, Manage My Taxes, select the link for the 2024 tax year. Then click the link: “View your 1099 for tax year 2024.” (Make sure to select 2024, not 2025.)

- At this point, you may get a huge listing of all of your interest payments, savings bond redemptions, potential capital gains and original issue discount accruals for Treasury Inflation-Protected Securities.

- TreasuryDirect does not offer an easily printable .pdf version of this form. To print it, click anywhere on the browser page and hit CONTROL P on a PC or COMMAND P on a Mac. This should open up a dialog to print the pages. (Mine was 12 pages long.)

- Print the 1099. (Your computer may also give you the option to “print to .pdf” which will allow you to save the document before printing.)

- Don’t have a printer? You can copy the entire text of the 1099 and paste it into a text or Word document. Save that file for reference when you fill out your tax return.

- At the bottom of the page, click on “Return.” Repeat the process for any additional spousal or linked accounts.

One bit of comedy from TreasuryDirect: Once you open your 1099 page, there will be no top tabs and you will need to scroll all the way to the bottom (12 pages!) to get to the “Return” button. Do not click on the back arrow or you will get logged out of TreasuryDirect.

Examine the 1099

There is a lot to see here, and you don’t want to miss anything that needs reporting to the IRS. On a 1099 from any brokerage or bank, everything is nicely organized and summed up, with clear references to the proper boxes on your tax filing. Not so with TreasuryDirect. In fact, this 1099 is actually a collection of 1099 forms, each with special purposes.

Form 1099-INT Interest Income

If you invested in any T-bills, Treasury notes or bonds, TIPS or redeemed savings bonds in 2023, you are going to see all interest-paying transactions listed here. In 2024 I was rolling over staggered 13- and 26-week T-bills at TreasuryDirect, plus had a collection of TIPS, plus redeemed a couple 0.0% I Bonds, so my list was enormous: 33 items. Example:

At the bottom of this long list, way at the bottom, is the total. Scroll all the way back up to the top to see that this total is Interest On U.S. Savings Bonds And Treas. Obligations and it goes in Ref. Box 3 on the federal tax form when you are filling out the section for 1099-INT. Here is the definition of Box 3:

Shows interest on U.S. Savings Bonds, Treasury Bills, Treasury Notes, Treasury Bonds and Treasury Inflation-Protected Securities (TIPS). … This interest is exempt from state and local income taxes.

You want to make sure the interest gets recognized as coming from U.S. Treasurys, because it will be free of state income taxes.

If you had any proceeds withheld for tax purposes (highly unlikely) those totals will be listed in column 5 of this section.

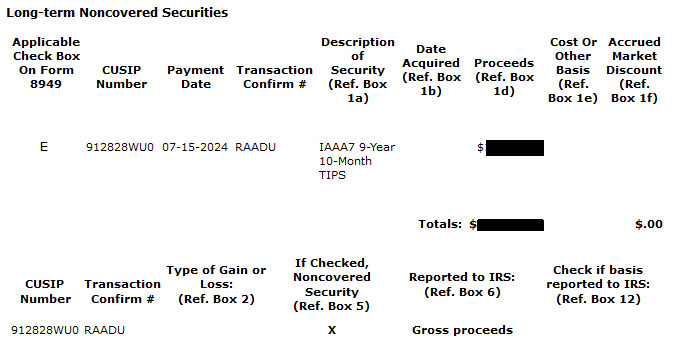

Form 1099-B Proceeds from Broker and Barter Exchange Transactions

There are several sections to form 1099-B and I generally have just a few transactions listed here. This seems like a relatively new part of TreasuryDirect reporting, which shows an Accrued Market Discount on longer-term investments that matured in 2024.

This is my only 1099-B item for 2024, and it is a doozy:

This is all for a single 10-year TIPS, CUSIP 912828WU0, that matured on July 15, 2014. The Treasury calls this a “noncovered security,” which I translate to mean, “We have no idea how much you paid for this.” The 1099 instructions note: “Generally, a noncovered security means: debt instruments acquired before 2014.” But I bought it in 2014!

The problem is that Treasury is reporting the “gross proceeds” to the IRS and so I will have to try to figure out a way to keep from paying taxes on that total amount, much of which was my cost basis. The 1099 instructions are not particularly helpful. My records show my initial discount at purchase was about $400, and that is probably what will end up being taxable.

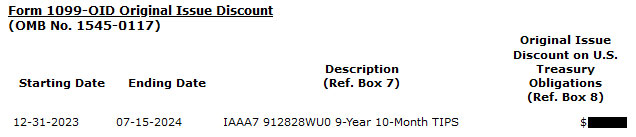

Form 1099-OID Original Issue Discount

This is a very important section for investors who hold TIPS at TreasuryDirect. The 1099-OID lists annual inflation accruals for every TIPS held in the TreasuryDirect account in 2024. These inflation accruals are federally taxable in the year they were earned, even though they were not paid out but just added to principal.

Long-time investors in TIPS are familiar with the 1099-OID, but new investors at TreasuryDirect need to pay heed to this section and report it on their federal tax return.

At the bottom of the list will be the total for all your TIPS holdings. TreasuryDirect notes:

Report this amount as interest income on your federal income tax return. … This OID is exempt from state and local income taxes.

Final thoughts

I am no tax expert, so nothing you just read should be considered tax advice. Still, getting these 1099s from TreasuryDirect is EXTREMELY IMPORTANT. And make sure you do this for every account where you had taxable activity (such as maturing short-term T-bills or redemptions of I Bonds).

You are going to get one email with a fairly cryptic message. That’s it. Nothing in the mail. Nothing you can download to Quicken. No .pdf. No easy-to-read tax summary like you receive from your broker. It’s up to you to go to TreasuryDirect, find the 1099s, print them, decipher them and report them on your tax return for 2024.

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Did you figure out how to reflect 1099-B on your taxes?

It seems difference between cost basis and proceeds amounts to zero.

The difference it the OID, for which we paid taxes on all these years.

Yes, in this case the Treasury did not report my original purchase price to the IRS, but I had a record of it and ended up having a very small capital gain on the tax form.

I can’t reconcile my TreasuryDirect 1099 income with what TreasuryDirect itself says it paid me for Tax Year 2024 (under “Recent Account Activity”). I have both Form 1099-INT and Form 1099-OID because I hold some TIPS. TreasuryDirect’s “Recent Account Activity” page shows that there were 5 interest payments to me in 2024, and those 5 payments match the deposit records for my banked account down to the last penny. But Form 1099-INT shows a different amount, which is less than the amount that was really paid to my bank account. Also, Form 1099-OID shows quite a large amount of this type of income, but it doesn’t show up in either TreasuryDirect’s “Recent Account Activity” page or my bank records. I get it that the Form 1099-OID reflects the increased value of my principal, but it still feels wrong. If I have shares of stock, or a mutual fund, that appreciate, I don’t pay tax on the gain until it is realized. In the case of my 1099-OID, it feels like I’m expected to pay taxes on an unrealized gain. How can that be? Also, forgetting about the 1099-OID for a moment, I’m STILL confused about why the numbers on 1099-INT don’t match what TreasuryDirect actually sent to my bank account. Last gripe: I emailed TreasuryDirect to ask about this and got back an auto-reply saying they’re swamped with inquiries and can only answer questions regarding open cases, with case numbers, which I don’t have. I haven’t opened a case, I’m just trying to file my taxes on time! What do I do? Thank you! Mary

I was confused by that, too. I think the answer is that even though the interest is deposited x-weeks before, the Treasury is assigning that interest to the maturity date. For example, I received $260.36 on 6/18/24 for a 26-week TBill. That amount shows up only once on my 1099 as of 11/26/24, the maturity date.

I’m interested in reading your advice on timing for purchasing I-Bonds this year.

I wrote about that here: https://tipswatch.com/2025/01/05/great-mystery-an-i-bond-buying-guide-for-2025/ …. At this point a purchase in late April looks most logical.

What, if anything, do you make of Paul Krugman’s repeated warnings on TIPS – that the current government may cook the numbers to understate inflation for political reasons, which would leave those holding TIPS (and I Bonds) undercompensated?

I hope you are enjoying your travels.

I get this comment pretty much daily. I’d say we have to stay alert.

Important: If you have both regular Treasuries and Converted paper bonds, remember that they are 2 separate TreasuryDirect accounts with 2 separate account numbers. So, you need to do ManageDirect(tm – Hilarious, as if someone would copy this awful interface) for your normal account, print your 1099 (to PDF preferred). And then Return to accounts, and switch to your My Converted Bonds account and repeat the ManageDirect procedure. So, you’ll get two 1099’s, and you’ll need both (assuming you earned interest both).

Of course, there won’t be a 1099 for the converted I Bonds unless you actually redeemed some in 2024. I have also chuckled over that trademark on ManageDirect. Pretty silly.

texgreen, if you’re tired of having to go to both your primary account and your conversion account to look for the 1099’s like I used to do. It’s really easy to transfer the bonds in the conversion account to your primary account and all of your bonds are in one place.

Go into your Converted Account; Click on Manage Direct and Manage My Securities and Transfer Securites; pick the ones you want and follow the instructions to move them to your Primary Account.

Wow. Had no idea. I’ll do this today. Thanks!

So, the Converted I-bonds were purchased through tax refunds, so they are co-owned by me and my wife. When I get to the final transfer screen, it warns about possible tax consequences. Essentially I’m transferring from a co-owned bond to a personally owned bond. Even though we are spouses, I’m not sure I know whether there are tax implications, so I’m hesitant to mass-transfer them.

If the social security number is the same, you’re probably okay, but I would call Treasury Direct 844-284-2676 with that question.

Thanks for this useful information. Having just retrieved and reviewed my TD 1099, though, I have one question maybe someone can help with. In January I purchased a 3 year Treasury note (CUISP 91282CJT9) that included a small amount of accrued interest, but I do not see the accrued interest paid reported on the TD 1099 as I have for brokerage 1099s and the interest amount reported on the TD 1099 is the gross amount paid (i.e. it does not subtract the accrued interest I paid on purchase). Will there be any problem if I include this amount of accrued interest on my tax return even though it is not documented on the TD 1099? The history detail for this security on the TD website does show that accrued interest was paid on the purchase. Thanks.

A reminder to deal with taxes for everyone who sold Series I Bonds in 2024 in a linked account for a minor. In my case, the interest income in the minor account was above $1,300 and I’m including that income in my own tax return with Form 8814. I thought TurboTax was doing a decent job guiding me through the process.

I wish the IRS people who took a year to straighten out my taxes had seen this post.

Question about entering TD interest on tax return:

As everyone mentioned the TD 1099 is a big mess with so many lines for interest.

Do you guys enter each line individually to 1099-B or just enter one line for the “total”?

Thanks.

One line for the total, for each category of 1099.

I enter after TD Ibonds for interest…the individual account amount of taxable interest in parenthese with the total in the right column

If you choose to report multiple items on one line you should use code “M” in column f on Form 8949. When you use code “M” you are supposed to attach a statement to your return showing the individual items. In practice, I have heard CPA firms not attaching statements and never getting a notice from the IRS.

I pulled my info yesterday. The Treasury could reduce their carbon footprint by decreasing spacing and putting more interest payments on one page, or even better, offering a summarized file showing just totals. The 13-page 1099 I printed is ridiculous.

I endorse this viewpoint! Of course, some people will want to see the detailed list. A brokerage could handle this info in 2 pages max, nicely formatted. The explanations will add to the page load, however, and they are important.

We redeemed a lot of I Bonds in 2024 (and then turned around and bought a bunch of new ones during The Great Gift Box Rules Confusion.

All but a few of the old ones had a zero percent fixed rate component, and all were originally paper bonds later converted to electronic. And, most tedious, all from the days when a person taking a federal tax refund of $5,000 as I Bonds instead of cash would get 12 separate I Bonds each year: six of $50, one of $200, one of $500, and four of $1,000, a denomination format which was retained by TreasuryDirect even after they’d been converted from paper to electronic.

So I had to perform 108 separate online transactions to redeem all of them, which I spread in computer sessions over multiple days, lest I go blind from eye fatigue, or go insane, at the screen. Aaargh.

And each redemption was listed individually on TreasuryDirect’s year-end Form 1099, with lots of white space between them, so when I printed the thing it seemed more like a small magazine than a tax form.

Early withdrawal penalties on CDs and I assume I-Bonds are deductible “above the line” and the payer should report that amount to the taxpayer.

I cashed in an I-Bond in 2024 that I had held for a little over 1 year, but I do not see any info regarding the amount of the 3 month interest penalty on the 1099 that just became available on the Treasury Direct system. Any thoughts?

Thanks!

Love your website!

I am almost positive the Treasury just reports the net interest paid out above the original purchase price. The penalty is already subtracted.

Yes, they did report the exact amount that I received in my bank account after the sale. What I am trying to find out is the amount of the 3 months of interest that I forfeited by selling before 5 years had passed. That amount can be taken as a deduction on my tax return if I knew what is was. The same would apply to the interest penalty for cashing in a bank CD before maturity.

Thanks!

I am no tax expert, but the interest the Treasury is reporting already excludes the 3-month interest penalty. So you can’t claim it again.

Yes, I agree. On a typical 1099-INT they report the interest you received say on your CD in box 1 and if you had an early withdrawal penalty that would be deducted by the bank from your principal when you cash the CD out and the penalty would go in box #2. This is much easier to understand if you think of the case where they pay you the interest every month to your checking account and you spend it. You have a $10k CD and you cash it out early and get $9,900. You have to report the total interest income you got and then the $100 penalty.

In the case of ibonds, TD does not give you nor report interest that has accrued but is not owed you yet. In other words, the amount owed you is always shown with the penalty included, so nothing would be reported in box two, as your interest earned is your payment less your original cost. As you will notice your monthly total is always less 3 months interest until you hit the 5 year mark.

Thank you for your explanation regarding the interest penalty!

I’m very happy with how quickly Treasury Direct completed the 1099 and provided it online. This is much faster than from my brokerage – apparently I still have to wait another couple of weeks for that. I always download all my 1099s electronically to be sure I have them (rather than relying on the US mail) and to save my entire tax returns electronically. It is easy to see the amounts for 1099-INT, 1099-OID, and 1099-B. For anyone not familiar with 1099s, David’s overview is excellent as always.

Just looked over all my 1099s for T-bills (13 pages). The amounts on the 1099s are different from the amounts deposited in my Bank of America checking account, sometimes a few cents off, sometimes up to $5 off. Why would that be? Thank you.

I just compared my interest received vs the 1099s, and I found that: 1) the interest paid out on TIPS matches exactly, but 2) the interest on T-bills doesn’t match. So why? I think it is because the T-bill is being reinvested and the purchase price is discounted. Let’s say 13 weeks ago you invested $9,800 for a $10,000 T-bill. At maturity, you get $10,000 to reinvest, but the new cost is $9,780. The Treasury sends you back the $220 excess, which doesn’t match the $200 interest you actually earned. (That’s my theory, at least.)

Thank you for the response! In so many ways TD is a PITA. I cashed out all my IBonds because I don’t want my kids to have to deal with TD at all when I pass. Now I only use TD for my two-year cash stash in Tbills that untimately will mature into my bank account. So my kids will never have to deal with TD – oh, except for getting the &*% 1099! Ugh. I may have to rethink this. I’m trying to really simplify everything for them. Thank you for all your info!

I was confused by that, too. I think the answer is that even though the interest is deposited x-weeks before, the Treasury is assigning that interest to the maturity date. For example, I received $260.36 on 6/18/24 for a 26-week TBill. That amount shows up only once on my 1099 as of 11/26/24, the maturity date.

Thank you for your wonderful “blog” and insights. I finally picked 2024 to experiment with TIPs…..couldn’t have picked a better year.

If you receive a second 1099 for a conversion-linked account, should that interest be reported as a separate line on Schedule B? Or is it acceptable to report the combined interest from each TreasuryDirect 1099 form all on one line? (assuming same taxpayer ID for both accounts)

It probably doesn’t matter as long as all the interest is reported, but wondering what is best practice.

You’re right, it probably does not matter as long as all interest is reported, but I would report on Sch B a separate total for each separate account. Also report OID separate from Interest if any. This may reduce your chance of getting an annoying letter from the IRS. I have been preparing tax returns for 26 years, so I have seen a lot.

Thanks for your perspective. I usually report the interest separately for my own record-keeping and to avoid the scenario you’ve described.

Thank you, Chris B! My wife is an ex-CPA and she agrees with you. So we will be listing those 1099-INT items separately.

This year will be the first where I have two 1099-INTs for the two accounts. I will probably combine them since the payee will be the U.S. Treasury for both. The 1099-OID and 1099-B are reported as separate categories.

Thank you very, very much for this info and detailed guidance. Invaluable! I never would have figured this out otherwise.

Very timely. Thanks! Maybe Trump can sign an executive order to simplify this mess.

It’s the time of the year again:

https://x.com/c0c0blanc0/status/1867984806187032954

On a more serious note, while I now got the Treasury Direct 1099, Treasury direct will likely cause delays for my Schwab tax forms. Because Treasury direct did not provide sufficient information / cost basis for an account transfer that I initiated last June and which completed in November. I talked with Schwab and they said they requested it, but it may take a long time for Treasury Direct to act on it.

Just as a warning for anyone planning an account transfer, you may want to start it in January to give it maximum time.

RE: Transfer out of TD

I mailed the form to transfer 5 notes/bonds from TD to Fidelity on Jan 17 received a email with case number on Jan 25. It noted that it could take up to 12 Months to process. They arrived at Fidelity on Jan 29! I was pleasantly surprised to say the least. Less than 2 weeks, with a Federal Holiday in between.