By David Enna, Tipswatch.com

I sometimes watch too much CNN (stop me!) and on Thursday I heard Republican members of Congress repeatedly state that the just-approved Big Beautiful Bill would eliminate the tax on Social Security benefits, fulfilling a campaign promise by President Trump.

And then in his celebratory speech in Iowa Thursday evening, Trump said:

“We’re making the Trump tax cuts permanent and delivering no tax on tips. No tax on overtime. And no tax on Social Security for our great seniors. Right?”

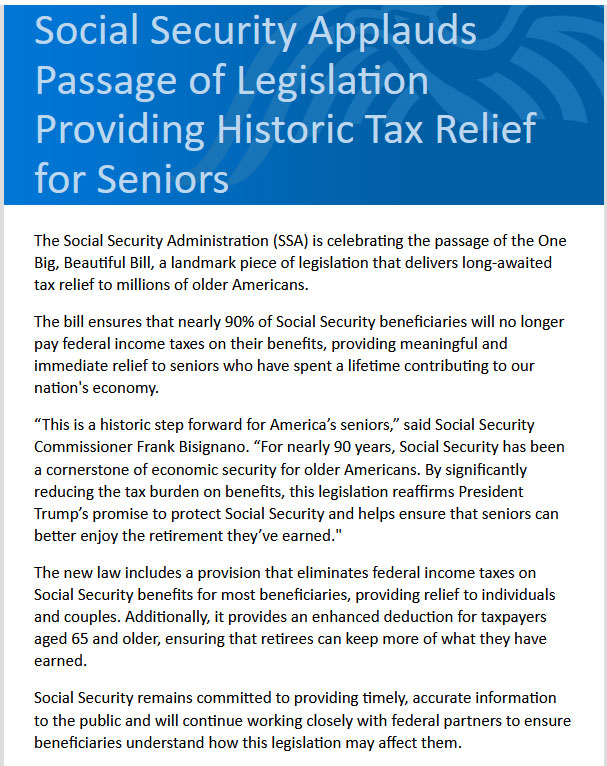

And I received this email from the Social Security Administration Friday morning:

The Social Security Administration (SSA) is celebrating the passage of the One Big, Beautiful Bill, a landmark piece of legislation that delivers long-awaited tax relief to millions of older Americans.

The bill ensures that nearly 90% of Social Security beneficiaries will no longer pay federal income taxes on their benefits, providing meaningful and immediate relief to seniors who have spent a lifetime contributing to our nation’s economy. …

The new law includes a provision that eliminates federal income taxes on Social Security benefits for most beneficiaries, providing relief to individuals and couples. … Social Security remains committed to providing timely, accurate information to the public.

A lot of this is not true, and whoever was responsible for that email should be embarrassed. What’s even weirder: There was no reason to fudge the facts here. The bill does provide meaningful (but temporary) tax relief for most seniors, and in fact will reduce federal tax bills for most seniors. But it does not eliminate the tax on Social Security benefits, which remains intact exactly as in pre-July-4 law.

What the bill does

The Big Beautiful Bill provides a $6,000 boost to senior citizens’ standard deduction from 2025 through 2028. The new tax break — $6,000 for individuals and $12,000 for couples — is for tax filers age 65 and older. It starts phasing out for those who earn over $75,000 ($150,000 for couples).

This provision is aimed at middle- to upper-middle-income taxpayers. People with very low incomes won’t benefit (they already pay near-zero taxes) and high-income people will see the deduction phased out completely. This is from a Yahoo Finance analysis:

To be clear, this provision does not eliminate taxes on Social Security benefits as Trump promised in the campaign. It is a temporary income tax deduction, not a cut in the Social Security tax. …

In addition, under existing law, people over 65 got an add-on to the standard deduction — $2,000 for a single person and $3,200 for a couple filing jointly. The White House has issued a fact sheet that clarifies those pre-existing add-on deductions will continue:

Under current law, about 40% of people who get Social Security must pay federal income taxes on some of their benefits, according to the SSA. The tax hit begins at low levels ($32,000 for couples) and eventually caps out at $44,000, when up to 85% of the couple’s benefits may be taxable. These levels were initially set in 1983 and have not been indexed to inflation.

Again, the current tax on Social Security benefits remains intact. But the boost of $6,000 / $12,000 to the standard deduction will provide a counter-balancing tax break, potentially eliminating the effect of the Social Security tax. People who rely solely on Social Security for income will likely not pay any tax at all.

However, people under the age of 65 who have already begun collecting Social Security will be subject to the full tax — potentially on 85% of benefits — with no increase in the standard deduction.

A couple over 65 with up to $96,950 in taxable income in 2025 is in the 12% marginal tax bracket. So a boost of $12,000 to their standard deduction would provide a potential tax break of $1,400, whether or not they are collecting Social Security. A similar couple with $150,000 in taxable income is the in 22% tax bracket, and would receive a potential tax break of $2,640. That is substantial.

A couple with taxable income above $150,000 would see the deduction phase out and it would be completely gone for a couple with $250,000 income. I am assuming these people would still be eligible for the current $34,700 standard deduction for couples over 65.

The $6,000 bonus deduction would be available to taxpayers whether they take the standard deduction or itemize.

Here is an analysis from Govfacts.org:

Primary Beneficiaries: The main group to benefit are middle-income seniors aged 65 and over. These are individuals whose total income is high enough to create federal tax liability but low enough to fall below the phase-out thresholds. The White House Council of Economic Advisers estimated the new deduction would benefit 33.9 million seniors.

No Benefit for the Lowest-Income Seniors: The poorest seniors, whose total income is already below existing deduction thresholds, pay no federal income tax on their Social Security benefits. For this group, an additional deduction has no effect.

No Benefit for High-Income Seniors: Wealthier retirees with incomes above the phase-out thresholds are ineligible for the deduction and see no change in their tax liability from this provision.

Harry Sit, creator of TheFinanceBuff.com, just posted a good analysis of this issue, including a chart compiling the income phaseouts:

Key takeaway: Note that some significant tax benefits remain even when a person or couple gets close to the $175,000 or $250,000 limits. Some smart income planning could result in a lower tax bill for 2025.

The new law also includes a deduction on charitable contributions, according to CNBC. The bill allows charitable taxpayers who don’t itemize to deduct up to $1,000 for single filers and $2,000 for married couples filing jointly. This begins for tax year 2026 and may also apply in some form to taxpayers who itemize.

Based on excellent information provided by commenters, it appears all the new deductions will be “below the line,” meaning they will not reduce adjusted gross income, which is used to determine Medicare surcharge levels among other things. But they will reduce taxable income.

Why this is good

The bill cleverly shifts the tax break to a 4-year increased standard deduction instead of eliminating the tax on Social Security benefits. Why is that good? Because the tax on benefits is intact and goes back into the Social Security “trust fund,” helping to pay future benefits. The trust fund is currently expected to run dry in 2032 to 2034, potentially leading to a 19%+ cut in payments to all beneficiaries.

The Committee for a Responsible Federal Budget estimates the higher senior tax deduction through 2028 would result in a loss of $66 billion in revenue over the four years. But most of that lost revenue would be outside the Social Security system.

And the downside …

Because many senior citizens will now be reporting lower adjusted gross incomes, they will in turn potentially be paying 1) less in taxes on Social Security benefits and 2) less in Medicare surcharges imposed through the Income-Related Monthly Adjustment Amount, or IRMAA. GovFacts.org says:

The nonpartisan Committee for a Responsible Federal Budget (CRFB) estimates that the “senior bonus” and other tax changes in the bill will lower revenue collected from benefit taxation by approximately $30 billion per year. …

The CRFB projects that this revenue loss is significant enough to accelerate the projected insolvency date for the Social Security OASI trust fund (which pays retirement and survivor benefits) from early 2033 to late 2032.

The IRMAA trigger levels are not directly affected by increasing the standard deduction, because IRMAA is based on adjusted gross income, before the deduction is subtracted. But with the expanded deduction, some retired people may be making smaller taxable withdrawals or stock sales to supply current income, making it easier to stay below IRMAA trigger levels.

Thoughts

No one is a “fan” of the tax on Social Security benefits, or the Medicare IRMAA surcharges for that matter. But I understand the need for these taxes and surcharges to keep these important programs going. Not every problem can be solved with a tax cut.

So, I support the tax on Social Security benefits. The problem with the tax is that the trigger levels are much too low and have never been indexed to inflation, after 42 years. Too many people at fairly low income levels are paying the tax.

The tax is crucial to help delay insolvency of the Social Security trust fund. That day is coming and a solution needs to be found. I don’t expect anything to be done in the next three years, so the problem will simply get more severe.

Trump promised “no tax on Social Security” — an idea I did not support. Congress came up with a solution to give seniors a temporary, 4-year tax cut outside of the Social Security system, adding to the federal deficit but not putting a great deal of additional strain on Social Security.

The Wall Street Journal notes:

Under the fast-track legislative procedure that Republicans are using to pass their bill, they aren’t allowed to touch the Social Security trust funds, which is where some income taxes on benefits go. Republicans devised the senior bonus deduction as a way to give tax breaks to many of the same people who pay taxes on their Social Security benefits. …

“I would welcome any relief on taxes,” said Trump voter Peter Sullivan, 67, a retired financial executive in Strongsville, Ohio. He added: “It’s still short of my Social Security tax nirvana of having it completely tax-free.”

The tax on Social Security benefits is intact and under current law will continue after the $6,000 bonus standard deduction ends in 2028. My opinion: This is a good thing. I am sure some of you disagree. Express opinions in the comment section, but please avoid political attacks or tirades.

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I agree with the the ideas that 1) the bonus senior deduction is beneficial to lots of middle-class seniors, that most would recognize as a good thing, and 2) the messaging is not only confusing, it’s blatantly false. I can guess why they communicated it that way, but it’s not important.

What is important is that the misrepresentation actually does a DISSERVICE to seniors. Imagine a SS-eligible individual that is trying to delay taking benefits in order to increase their monthly income. After hearing that “tax on SS is eliminated” they think, I may as well file now because I won’t have to pay any tax on that money. When in fact, doing so may increase their taxes and permanently decrease their benefit.

Another article on the $6000 deduction for 65 and older: https://www.yahoo.com/news/social-security-sends-incorrect-email-221025521.html

It states that the deduction is available for itemizers and is per person, like a personal exemption.

Mr Enna says “The tax is crucial to help delay insolvency of the Social Security trust fund. That day is coming and a solution needs to be found.” This tax actually goes into the general tax fund, and not into the Social Security trust fund.

Not true. From AARP (and many other sources): “Like your payroll taxes, the federal income taxes collected on benefits go into the Social Security trust funds. That means the money contributes to future benefit payments and helps shore up the Social Security system’s finances.”

Here is the link from the SSA website.

https://www.ssa.gov/oact/progdata/taxbenefits.html

The new $1000/$2000 deduction on charitable contributions for non-itemizers appears to be below the line, not above the line as some have reported in the press. This is written into law as a simple extension of the similar 2021 CARES Act charitable deduction which was below the line that final year. (Look at your 2021 Form 1040 tax return.) The confusion may stem from the fact that the non-itemized charitable deduction was above the line in 2020.

Incorrect. The charitable deduction is for Non-Itemizers, so it is above the line. If you do Itemize, there will be a 0.50% reduction in charity on Sch A.

There is no reason that deductions available only to non-itemizers cannot be below the line (do not reduce AGI). It happens. See: Year 2021, IRS Form 1040, Line 12b, which is an entry (below the line) for: “Charitable contributions if you take the standard deduction (see instructions).”

My expectation is that the IRS will interpret this law the same as they did in 2021. The new verbiage in the OBBB (https://www.congress.gov/119/bills/hr1/ … hr1eas.pdf) simply says:

SEC. 70424. PERMANENT AND EXPANDED REINSTATEMENT OF PARTIAL DEDUCTION FOR CHARITABLE

CONTRIBUTIONS OF INDIVIDUALS WHO DO NOT ELECT TO ITEMIZE.

(a) IN GENERAL.—Section 170(p) is amended—

(1) by striking ‘‘$300 ($600’’ and inserting ‘‘$1,000 ($2,000’’, and

(2) by striking ‘‘beginning in 2021’’.

(b) EFFECTIVE DATE.—The amendments made by this section shall apply to taxable years beginning after December 31, 2025.

The new charitable deduction simply expands and makes permanent the below the line version that was in place in 2021.

Since this charitable deduction for non-itemizers will be below the line, QCDs (which reduce AGI) will be a better option for those who can make QCDs. Also, the charitable deduction for non-itemizers is not available until the 2026 tax year.

Sorry about the broken link. Hopefully this will work:

BILLS-119hr1eas.pdf

Object’s link does seem to imply the additional deduction will not go into effect until 2026. “shall apply to taxable years beginning after December 31, 2025.”

On the topic of QCDs, isn’t it more accurate to say they have no effect on AGI? Except in the cases were they are reducing an RMD. So for people not yet taking RMDs, the $1,000 deduction would be beneficial.

What I meant to say is that when the source of the donated funds is from a traditional IRA, making the donation in the form of a QCD is better than using a below-the-line deduction (that increases AGI). Whether the donor is taking RMDs is not a relevant factor in this decision.

Object, definitely true. If you are at an age that is QCD eligible, and want to move that money from a traditional IRA, you go with the QCD. In other cases, if you just want an additional $1,000 deduction added along with the standard deduction, use a cash account to make the donation. But wait until next year.

Objectimportant above is 100% wrong about the charity. If you are itemizing, then any charitable deduction will be reduced by 0.50% and it is on schedule A, which is below the line. In 2026, the deal they are offering people that Do not itemize, is that they can deduct charity up to 2,000 per joint return and it is above the line. 100% fact.

This post in Bogleheads provides evidence that all the new deductions are below the line.

The new deductions are all below-the-line – Bogleheads.org

-Quote:-

26 USC 62 defines AGI and lists all of the above-the-line deductions. Section 62 has not been amended by the new bill.

26 USC 63 defines taxable income as gross income minus all deductions. It then proceeds to clarify how the standard deduction and itemized deductions work:

The question, then, is where the new deductions have been placed. None of them were added to Section 62, so they are not subtracted prior to calculating AGI.

The additional senior deduction was added to section 151, so it will be treated exactly the same as personal exemptions used to be treated.

The new cash charitable deduction was just an update to section 170(p), so that’s already there as a below-the-line deduction.

Finally, three new lines were added to 63(b): the overtime deduction, the tips deduction, and the car loan interest deduction.

Therefore, these new deductions are all below-the-line and available to non-itemizers.

-End Quote-

“Under the fast-track legislative procedure that Republicans are using to pass their bill, they aren’t allowed to touch the Social Security trust funds, which is where some income taxes on benefits go.“

Congress could NOT eliminate or change how SS is taxed because of rules in the Senate that apply to the RECONCILLIATION PROCESS that enacted this bill. Is the result perfect? NO, but my goodness it certainly makes a dent in the taxes paid by those 65 and older. In my mind it meets the SPIRIT of what the administration said they would do. Don’t let perfect be the enemy of a good result.

You just explained the situation perfectly, and accurately. This is a big win for the administration: A nice increase in the standard deduction that benefits middle- and upper-middle class people aged 65 and up, no matter if they are taking Social Security or not. It would be smart to promote what it is, and not what it is not. It is not “no taxes on Social Security.”

Regarding the sentence – “Some smart income planning could result in a lower tax bill for 2024.”

Wondering what some of the readership is doing or planning to do to reduce their upcoming tax bill?

@David, I assume you meant 2025 here.

Ah yes, I rarely know what day month or year it is. Today I thought all morning it was Sunday (not Saturday).

Well, in your brain’s defense, it is the second day of the weekend.

Great summary as usual. And I was pleasantly surprised to see a donation button at the end of the article, and happily sent in a contribution to help keep this highly valuable site running! Thanks!

Clark, your support and participation is greatly appreciated!

Hi David, Thanks for another excellent and timely article. I’ve got a question about IRMAA. Since it’s calculated based on MAGI and only the taxable portion of Social Security is counted for MAGI, would the increased “bonus” decrease the amount of taxable Social Security used to calculate MAGI for IRMAA purposes? It’s not that I’m against paying IRMAA but hate to go over it by just a few dollars. Thanks again for all the education you so generously share!

This came up in earlier comments (thank you Andrew and Sabine) which clarified IRMAA is based on adjusted gross income, before the standard deduction is subtracted to create taxable income. I edited the article to include this new sentence: “The IRMAA trigger levels are not directly affected by increasing the standard deduction, because IRMAA is based on adjusted gross income, before the deduction is subtracted.” …. Plus, “taxable Social Security” is totally unaffected by the Big Beautiful Bill. That calculation was not touched.

Perhaps you should start your analyses on a positive note rather than your typical Trump bashing. This is not the typical regressive taxation used by Democrats. Trump has done something decent for lower income people. Establishment politicians of both parties have abused the lower classes by lowering the capital gains taxes which benefits the people of means. Then they instituted Quantitative Easing lowering interest rates to 0% for 10 years which destroys any hopes for the poor who do not have portfolios. The house flippers and option traders should have contributed more to the national Treasury instead of buying estates in the Hamptons. Capital Gains taxes should revert to 70 years ago and progressively rise to 90% to balance the budget. Maybe you should expand your repertoire and consider other sources of “facts” beyond the perennial liars you seem to prefer. You might consider people such as Professor Thomas Sowell or Victor Davis Hanson of Stanford and others which would help balance your leftist indoctrination.

Joseph, I appreciate this opposing viewpoint. My feeling is that the White House had something excellent to talk about — a large increase in the standard deduction for people over age 65 with moderate incomes. Instead, it put the focus on “no tax on Social Security benefits,” which simply wasn’t true except in certain cases. The tax remains on the books exactly as it was pre-Big Better Bill.

You raise important issues about fairness in tax policy. But to clarify: David’s article isn’t bashing anyone politically — it’s pointing out that the claim made by President Trump about “no tax on Social Security benefits” isn’t fully accurate when you look at how the tax code actually works. That’s not an ideological judgment — it’s a fact-based correction, especially relevant for people with income from TIPS, RMDs, or other sources.

This isn’t a debate about Sowell, Hanson, or broader economic theory — just a clear explanation of how tax rules affect real retirees. Facts matter regardless of who’s in office. I thank David for this.

Very good reply. Joseph was off the reservation with a completely incorrect assessment.

Hear, hear!

Some examples.

https://www.whitehouse.gov/articles/2025/07/no-tax-on-social-security-is-a-reality-in-the-one-big-beautiful-bill/

In these examples, the White House is pointing to people whose income is ONLY Social Security and no other source. So sure, those people will not be paying tax on their Social Security benefits, and in fact won’t pay any tax at all. People who have other sources of income (part-time job, pensions, annuities, capital gains, interest, RMDs, etc etc) could still be subject to the tax. In other words, some percentage (up to 85%) of Social Security benefits will be counted as income and face federal taxes.

From my calculations (this doesn’t affect me yet so I don’t check it often) even under the current tax law, a single person earning the maximum benefit possible, around $61,000 in 2024, without any other income, would pay very little in income tax. $2,750 taxable income, About $275 in tax. Probably an unlikely scenario though.

Excellent write-up and explanation of this change in tax law. It’s ridiculous that the SSA sent a misleading and false email, which I also received.

I also received the SSA email and found it to be an insult to my intelligence. It’s bad enough when they lie to us through the media, but now they are sending the lies directly to us via personal email.

A (very) rough calculation shows that if the income limits had been indexed to inflation in 1993 they would presently be 50% at $56,000 and 85% at $75-79,000. And the estimate of $66 billion in lost revenue over four years is probably less than the cumulative loss would have been had indexing had been introduced.

Politically clever, most likely the party out of power will be in power when an opposition party takes over. Essentially ss will be running dry along with a tax increase. Republicans, in the 21st century, have been very clever at politics.

Excellent information. I am an Accountant and will have to understand all of details for the next tax season. Did not know anything about the changes with the new tax bill. This article was a great introduction. Thank you.

Let’s remember we are fortunate to have such high standard deductions. If we are want to tackle the deficit these high deductions should be eliminated. Can you imagine the press and social media’s outrage if that were to occur? The article seems to neglect the benefits and how they were put into the tax code.

No, I am a fan of the standard deduction, which truly helps lower the tax bill of lower-income people. A high standard deduction also discourages itemizing, which makes filing taxes a lot simpler.

Further, it seems even more beneficial to completely eliminate itemized deductions entirely. Eliminating schedule A and only having the standard deduction would:

(1) Make taxes fairer by eliminating special interest tax preferences that benefit only 10% of the population [90% of people use the standard deduction].

(2) Simplify complying with tax laws and take less time to file your taxes.

(3) Reduce record-keeping for taxpayers, financial institutions, and the local, state, and federal governments that produce tax documents .

(4) Reduce IRS bureaucracy for verifying itemized deductions for all itemized filers as well as resulting additional effort in audits.

Harry Sit of The Finance Buff makes a good point. This is a senior deduction, not a Social Security deduction or a Social Security tax decreaee. It actually has nothing to do with Social Security at all.

https://thefinancebuff.com/social-security-taxed-2025-trump-tax-law.html

Harry, as always, did a great job on this. I am using his phaseout information to replace the chart I originally posted.

Yes, he did, and always does. it’s up to you, of course, but I suggest deleting the word “quite” from the title of this article for accuracy’s sake. Even if someone is in the “Goldilocks” zone to maximize the senior deduction offsetting their SS taxes owed, SS is still taxed exactly as it was before, as Harry points out.

It feels like we are living in the world of 1984. These are odd dystopian-like times indeed when an email from the SSA, a government agency, seems like spam because it is filled with misleading information.

No, it does not eliminate SS taxes for 90% of recipients.

No, the SS deduction does not apply to all types of SS recipients. Those aged 62, 63, or 64 are out of luck.

Those aged 65+ who have low incomes and already pay no federal income tax get no benefit. This group comprises 20% of all SS recipients.

Those with higher incomes get a reduced deduction or nine at all.

The entire deduction is temporary and expires cynically just after the current presidential term expires.

Tax relief is popular but SS is even more popular. The program is not as solvent as it needs to be and there is nothing in this bill that addresses that issue. The fairest way to do that is to lift the income cap on SS taxation so the burden doesn’t fall the most on those earning below the cap. But god forbid Republicans ever agree to raise a tax (despite the fact that it was Ronald Reagan who enacted the SS tax in the form we have it today). I guess we will have to leave the hard decisions to a future president and Congress when their backs are against the wall and the impact will be more painful and costly.

Thanks for this nice summary. I plan to plagiarize it when I report to SSA that their account has been hacked and somebody is sending out political crap under their name.

Here’s a possible path to hard decisions: “Effective January 3, 2027, congressional salaries and benefits shall be paid exclusively from the Social Security Trust Fund. Any reductions in Social Security benefits or other payments from the said Trust Fund resulting from any funding shortfall shall apply pro rata to all congressional salaries and benefits.” (The effective date is to satisfy the 27th amendment.)

Great idea. We just need a new branch of government empowered to implement it. We can’t even get Congress to pass a law preventing their own insider trading.

You say that the new $6000 deduction would be an increase in the standard deduction, meaning it would not be available to those who itemize (which will be a larger number of taxpayers due to the SALT increase). I’ve seen other sources say this will be a new above-the-line deduction separate from the standard deduction, in which case it would be available to itemizers. Can you clarify? Which is correct?

Actually, my article contains this sentence: “The $6,000 bonus deduction would be available to taxpayers whether they take the standard deduction or itemize.”

I missed that, thank you!

The embedded quote from Yahoo Finance, which mentions the standard deduction amounts of $15,000/$30,000, may be out of date. I think that the standard deduction amounts are permanently bumped up by $750/$1,500 for 2025 to $15,750/$31,500, with future inflation adjustment made from that new base. https://www.nytimes.com/interactive/2025/06/30/upshot/senate-republican-megabill.html

Thanks, I added a paragraph of clarification. What I can’t locate precisely is if the current over-65 add-ons will remain in effect, or will the $6,000 bonus replace them?

That’s a good question. Everything I’ve seen seems to refer to an “additional” $6,000 deduction (e.g., https://finance.yahoo.com/news/tax-break-for-seniors-trump-bill-includes-additional-6000-deduction-204604211.html). Also, the current add-on is not just for over-65, but also for blind taxpayers, and I haven’t seen anything suggesting that this nonsense raises the taxes for under-65 blind taxpayers.

According to whitehouse.gov the total deductions for a senior couple below the phase out will be $46,700.

https://www.whitehouse.gov/wp-content/uploads/2025/03/The-One-Big-Beautiful-Bill-Delivers-On-President-Trumps-Promise-Of-No-Tax-On-Social-Security.pdf

Bob, thanks for pointing out that WhiteHouse.gov link. It does clarify that the previously existing $2,000 single / $3,200 joint add-on deduction will continue with this law. That add-on is not subject to a phaseout.

For those willing to make a really deep dive, the text of the new law can be found here: https://www.congress.gov/bill/119th-congress/house-bill/1/text/eas

Section 70103 is the new ‘senior’ deduction. Yes, it is in addition to the $750/$1500 bump up in the standard deduction for everyone and the previously existing ‘extra’ standard deduction for 65 or older or blind. This new $6000 senior deduction does not appear to be part of the standard deduction (i.e. it should be available to itemizers as well if they meet the income requirements). In fact, it appears that it was inserted into the tax law alongside the now permanent deletion of the person exemptions. It is also just for those 65 or older by the end of the tax year.

This is interesting information, but I’d say to hold off on making financial decisions based on the $6,000 being available to itemizers. We will need clarification.

You mention “…IRMAA is based on adjusted gross income…”

IRMAA, I believe, is based on MAGI (Modified AGI) and in the case of IRMAA, MAGI is calculated by adding to AGI any income from tax exempt municipal bonds.

Yes, this is true

Will be interesting to see the revised 2025 Form 1040 (and Form 1040-SR). Since the new deduction for seniors is also available to those who itemize deductions will it be an „above the line“ deduction that reduces AGI/MAGI? Also, anyone who is worried about the adverse effect of this new deduction on the solvency of the Social Security Trust Fund (it is expected to „speed up the exhaustion of the Social Security trust fund by about a year, the CRFB estimated last week“, exhausting it by 2032) can make a donation to Social Security: https://www.ssa.gov/agency/donations.html. For example, you could donate the savings in income taxes you have under the new vs. the old law.

I am assuming the deduction will be below the line, but keep in mind that high-income people will see the deduction phased out wherever it appears on the tax form. Those are the people most concerned about IRMAA.

Very true. And in general it’s the trigger of a (higher) IRMAA, not additional income tax liability, that prevents most upper middle class taxpayers from making larger Roth IRA conversions or taking larger-than-required distributions from traditional tax-deferred IRAs.

IBonds interest, not reported or taxed until the bonds are redeemed, may be preferable to munis for those hoping to reduce applicable IRMAA AGI.

It won’t have any direct impact on the Social Security Trust Fund. It won’t decrease Soc Sec revenues nor increase Soc Sec expenditures.

In their 2025 annual report, Social Security trustees estimated that the program’s trust fund would become insolvent in 2033. That was before Congress approved Trump’s bill.

The Committee for a Responsible Federal Budget, a fiscally hawkish group, ran the numbers on the Senate version of the bill, which the House approved without changes on July 3. It is headed to Trump’s desk, and he’s said he will sign it.

The group calculated that the changes from Trump’s bill will reduce Social Security tax revenues by $30 billion per year — meaning the trust fund would be exhausted several months earlier, in 2032 rather than in 2033.

The bill’s estimated impact on Medicare’s hospital insurance trust fund — which operates in a similar way to the Social Security trust fund — means the fund would run out mid 2032, not late 2033.

https://www.politifact.com/article/2025/jul/03/social-security-tax-break-impact-solvency/

Thank you. I didn’t know that income taxes on social security earnings were earmarked for the two trust funds. Sorry for the error.

Am I correct to think that for individual US taxpayers that are 65+ that also had no federal tax liability for 2024 and wouldn’t otherwise for 2025, that this OBBBA provision would allow for them to withdraw an extra $6,000 ($12,000 for couples) from a traditional retirement account above and beyond current withdrawals before they would hit the threshold for owing the first dollar in federal taxes?

I am not a tax expert, but this seems logical and will be a highly-used strategy.

Thanks so much for your commentary. I received the SSA letter yesterday morning as well and could see that it far from the truth. I’m glad that you and some other commentators (e.g., the Washington Post has a story on the subject) are trying to make everyone else aware of the facts.

David, great facts and analysis. However, AGI which triggers IRMAA goes on 1040-SR line 11. The standard deduction hits line 12 and reduces taxable income but does not help to reduce the IRMAA trigger level. Am I correct?

Yes, I believe you are correct. Thanks for this feedback.

I also received the email that stated the source was Social Security and I was wondering if it was a scam, knowing that the information was not correct. It is disconcerting to find false information from a government source.

With RMDs starting next year, I will not benefit from this boost to the standard deduction, unfortunately.

That’s what I thought, too, especially since my spam folder caught it! We are all used to politicians lying to us, but I can’t recall ever receiving a message from a government agency that deliberately misleads for political purposes.

“I understand the need for these taxes and surcharges to keep these important programs going.”

Do they? Or do those taxes just get spent by the government on other things?

The IRMAA surcharges help offset the costs of Medicare benefits for all participants, including those who don’t pay IRMAA. The taxes on Social Security mostly go back to the SSA, but some goes to Medicare.

I am an AARP volunteer tax preparer and this will be the number one topic for the coming tax season. I will have to deal with seniors that believe the email and the President. I forwarded the email to my Congressman and asked for hearings with the head of the SSA. Impeachment would be a fair outcome.

Thank you, David! This is just what I need to shut certain family members down at a picnic later this weekend.