By David Enna, Tipswatch.com

In two months, probably on Halloween morning, the Treasury will announce a new fixed rate, inflation-adjusted variable rate and composite rate for U.S. Series I Savings Bonds purchased from November 2025 to April 2026.

And I have bad news for I Bond investors: The fixed rate is likely to fall from the current 1.10% to 0.90% at the reset. Of course, this is still up in the air, depending on how real yields track over the next two months. But the path looks pretty clear.

The forecast

The I Bond’s fixed rate is its “real yield” — the yield above future inflation. It is important because it is permanent, staying stable for potentially 30 years. So if you bought an I Bond in 2014 with a fixed rate of 0.2%, it will continue to have a 0.2% fixed rate for the life of the bond. Purchases through October 31, 2025, have a fixed rate of 1.10%.

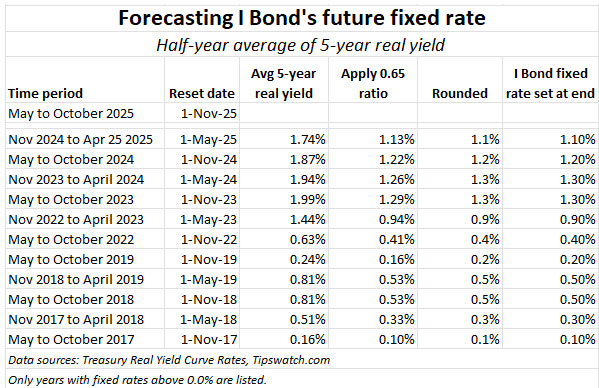

The Treasury has no announced formula for setting the I Bond’s fixed rate, meaning there is no calculation required by law or regulation enforcing the process. It is up to a decision by Treasury officials. However, I Bond watchers have settled on a forecasting tool that seems to work: Apply a ratio of 0.65 to the average 5-year TIPS real yield over the preceding six months. This formula has worked without fail at least since 2017.

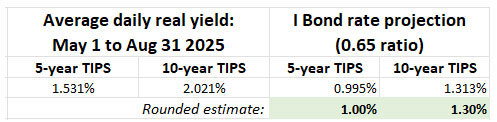

With two months to go, I looked at 5-year real yield data from the date of the last reset on May 1, 2025, to the close of Aug. 29, 2025. Looking at just that data, the forecast is for a new fixed rate of 1.00% at the reset.

I added the 10-year TIPS information just because it is interesting — using the 10-year real yield data you get an new I Bond fixed rate of 1.30%, much more attractive. The spread between the 5-year real yield (currently 1.21%) versus the 10-year (1.82%) is amazing. But it also probably irrelevant because the forecasting formula has only worked using the 5-year TIPS real yield.

So, with two months of data yet to come, the I Bond’s new fixed rate would be 1.00%.

Extending the forecast

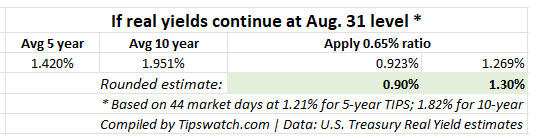

Now, let’s assume real yields hold steady at current levels through the month of October. That’s a bit iffy because the Federal Reserve is likely to cut short-term interest rates on September 17, and the 5-year TIPS real yield tends to move with those decisions. At this point, however, I think the rate cut is priced in.

In this chart, I added 44 days at current market real yields, which lowers the 5-year real yield average to 1.420% and in turn drops the 0.65 ratio to 0.923%, resulting in a new fixed rate of 0.90%. The forecast using the 10-year real yield remains at 1.30%, but I don’t believe it is relevant.

Keep in mind: The I Bond’s fixed rate is always rounded to the one-tenth decimal point. That means a further fall to 0.80% is unlikely.

As of today, I project a new I Bond fixed rate of 0.90%.

This chart demonstrates the accuracy of this projection method for every year back to 2017. (Of course, we can’t be sure the current administration will continue on this course.)

What this means

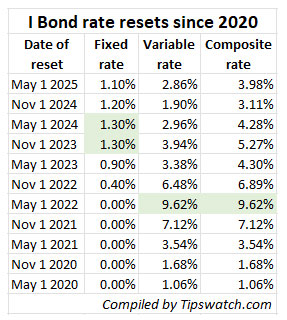

One immediate conclusion is that the I Bond’s current permanent fixed rate of 1.10% and composite rate of 3.98% for six months is attractive. I Bond investors who haven’t bought the full 2025 allocation ($10,000 per person per calendar year) should consider making a purchase before November 1.

Hard to say just yet, but the new variable rate could be around 2.8% to 3.0%, resulting in a new composite rate pretty close to the current 3.98%. But a higher fixed rate, which is permanent, is always preferable. Here is the trend in I Bond rates over the last five years:

In 2022, we got that gaudy 9.62% variable rate for six months, but it was tied to a fixed rate of 0.0%. After a year or two, investors were dumping that investment, which is currently yielding 2.86%. The fixed rate of 1.30% that came later was much more attractive, in my opinion, as a long-term investment.

In January, would I be buying I Bonds with a fixed rate of 0.90%? Not in January, probably, but later in the year, yes. I’d probably wait until mid-April to see the trend in real yields and inflation.

As the reset date approaches, I will be writing more on this topic. This article is meant as a heads-up for investors speculating that we could get a boost in the fixed rate, which is unlikely.

And, again, we can’t be sure the Treasury won’t simply ditch our much-trusted 0.65 ratio and set the I Bond’s fixed rate in a radically different way. (Not likely, I hope.)

FYI: I focused this article on future rates and didn’t attempt to explain the investing purposes of I Bonds or their intricacies. You can find a lot of that information in these links:

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Thank you for highlighting the idea of converting older fixed rate 0% to fixed rate 1.1% in Sep/October ’25 via gift boxing method. I am slightly embarassed I didn’t put this together when fixed rates were higher (but 110 bps in the right direction vs missing out on another 20 – that’s a win).

Appreciate the great info and expertise you share on this site!

I can’t decide whether to exchange an iBond from April 2029 with 0.5% fixed or one from January 2023 with 0.4% fixed (and forgo 3 months of interest). Any thoughts?

I haven’t rolled over any 0.4% I Bonds yet, and might not. Presented with your question, I would probably go with the January 2023 version since the tax hit would be much less.

The following is a copypaste directly from the Treasurydirect.gov site for I-bonds. It seems pretty clear (at least to me) that a gifted I-Bond counts toward the $10k annual limit for the person receiving the gift. There are other sections on the Treasury Direct web site that say the same thing as well. Bottom line is the annual limit of $10k includes both a persons own investments plus any gift box transfers to that person in the same year. Following is the copypaste:

Electronic Savings Bonds

Through your TreasuryDirect account which is established using your name and social security number, bank information, driver’s license and e–mail address – you can invest in electronic savings bonds (also referred to as book entry savings bonds) each calendar year by purchasing as much as:

Exceptions: Savings bonds you purchase as gifts aren’t included in your annual limit. The purchase amount of electronic savings bonds you transfer, deliver as gifts, or de-link to another TreasuryDirect account holder is applied to the annual purchase limit of the recipient. It is applied in the year the bonds are delivered to the recipient’s account.

Note: The three purchase limits above apply separately. That is, in a single calendar year you could buy $10,000 in electronic Series EE bonds and $10,000 in electronic Series I bonds.

Yes. Exactly. You have found TreasuryDirect’s bizarre loophole on gift-box purchases. Read the *exact* wording you have copied: “The purchase amount of electronic savings bonds you transfer, deliver as gifts, or de-link to another TreasuryDirect account holder is applied to the annual purchase limit of the recipient. It is applied in the year the bonds are delivered to the recipient’s account.”

What this apparently means: When you deliver $10,000 base-cost (plus interest) of I Bonds to a recipient, that recipient will no longer be able to buy I Bonds the traditional way in the year of the delivery. But … what is not stated but has been true for a year-plus … if recipients have already bought $10,000 the traditional way, they can still receive gift-box I Bonds, possibly to an unlimited amount. I and many other readers tested this approach. I didn’t expect it to work, but it did work and continues to work as far as I can tell. (Opinion: This loophole should be closed.)

“This loophole should be closed.” Be careful what you wish for. TD would also have to close out the transfer of ownership in currently delivered Ibonds. Reread your quote…it includes “transfers.” Therefore one would not be able to deliver ownership in whole or in part in one’s ibond portfolio in anticipation of death, etc. you name it! Everything is working as intended by TD!

Holding onto about $10k in I-bonds with a 0.4% rate from a couple years ago. Was planning on selling and buying bonds at a higher rate, but might hold onto it. Between HYSA rates falling to 3.25-3.5% by end of year and the preferred tax treatment of I-bonds, I-bonds with a low fixed rate might still outperform a savings account.

In addition to a bunch of more recent purchases–as much as we could afford using the gift box option–we also still have some I Bonds at 0.4% fixed, and others at zero fixed.

I keep debating whether to redeem those and buy more new ones. But the current value of those older bonds contains the “embedded” inflation earnings from the period after the worst of Covid, when the variable component of I Bond rates was up around 7%-9% annualized. So I keep thinking that if inflation (at least according to CPI) remains low in the next several years, then even a new I Bond at 1.1% fixed, or 0.90% fixed, combined with a low variable rate, will probably take quite a while to reach a “crossover point” with the value of older bonds with lower fixed rates but higher historic inflation earnings.

This is the kind of back-and-forth, “on the one hand/on the other hand” consideration that makes me feel like my head may explode, so we’ll probably end up leaving things just as they are and just keep buying whatever new bonds we can afford without redeeming older ones.

See my comments below at Doug

says:

September 5, 2025 at 7:51 am

It doesn’t matter if you have five 0% fixed interest $10,000 I-Bonds that have accumulated high variable interest in the past and now are worth, say $60,000. Or you cash them in and buy six $10,000 I-Bonds at 1.1% fixed interest. You still have $60,000 NOW earning 1.1% plus the variable interest that both bonds would earn.

Chat…And the difference is? In the noise level! And other alternatives provide? In the noise level! The caveat is your age and if you manage by managing expenses! It’s preservation time not accumulation time!

I tried to leave a comment and got transferred to WordPress. I had to log in and got this weird webpage about adding a site. Meanwhile, my comment has disappeared. Please advise.

Sounds weird, but this one worked. Try again and see.

I’ve already purchased my $10k for the year back in January so I am set and glad I did. The real decision for me will come next January… Like you said, waiting until April makes the most sense but that messes up my clean January purchase schedule for the past few years. I don’t know if I can handle the injustice of such a ‘messy’ spreadsheet.

One question, however. My oldest Ibond is from early 2020, at the 0% fixed level. I am tempted to cash that out early next year and buy a new one to keep a rolling 5 year ‘E-fund’ and/or bond tent for my recent retirement. I haven’t done the full math yet, but is ‘losing’ the compounded interest in the existing bond worth the ‘step up’ on a lower base amount in a new bond with a higher fixed portion?

Quick calculator tells me almost 13k at 3% (0 + 3) gives me roughly the same amount as 10k at 4% (1 + 3). The higher the fixed portion the more it makes sense but at the current/near future level, I am unsure. Whether I keep the bond and buy a new one with other savings, or cash it and roll it over, I will probably use them within the next 5-10 years.

You asked, “I haven’t done the full math yet, but is ‘losing’ the compounded interest in the existing bond worth the ‘step up’ on a lower base amount in a new bond with a higher fixed portion?”

I used the eyebonds.info website to estimate the hypothetical below.

Let’s say you have a $10k I-Bond bought in May 2020 earning 0% fixed rate plus inflation for a Composite rate of 2.86%. On Sep 2025, you will have earned $2,396 on the bond. In 6 months, you will have earned $177 on the bond.

You redeem the $10k I-Bond and buy a new $10k bond and receive 1.10% fixed rate plus inflation for a Composite rate of 3.98%. In 6 months, you will have earned $200 on the bond.

Use the gift bond process to buy another I-Bond for $2,000 (Amount left after paying tax on the sale of the redeemed bond) and receive 1.10% fixed rate plus inflation for a Composite rate of 3.98%. In 6 months, you will have earned $40 on the bond.

You will have to pay taxes on the interest on the redeemed bond. To me, if you can pay the taxes and use the gift bond advantage it looks like a win.

Doug, the real kicker is the next 4 years where there is the $6K or $12K added senior deduction to cover the taxes…also taking more IRA distributions too

Close.

The first bond was purchased in January 2020 with 0% fixed rate and will be redeemed in January 2025 when it matures and I will have no income. Forecast amount should be $12,736.

I will purchase $10k in Jan 2025 from the above cash in, using the $2,736 for livings expenses. OR I will leave $12,736 in at a lower rate.

If the expected fixed rate per the post is 0.9%, and, for ease of math, the variable rate is 3%. Yes, the variable will change in six months but the real comparison is the fixed rate which will not.

$12,736 for a year at 3% earns $382.08 if I keep the bond, the extra compound helping it out.

$10,000 for a year at 3.9$ earns $390. This is what I will probably do based on the other answer and realizing less money works harder for me. I just saw the number was so close so wanted other advice.

And no, gift bonds don’t work for me for reasons I won’t get into. I will also have no tax on the ibonds due to standard deduction covering all my ‘income’ from here on out.

When I roll over an I Bond for a higher fixed rate, I spend the excess money for travel or other needs. I generally don’t intend to hold I Bonds to maturity, but I will use them carefully for needed cash in the future. But if you don’t need the cash, you can re-invest the excess elsewhere.

Thank you! And this is why I asked. The numbers were about dead even but freeing up almost $3k to use or put elsewhere and earning about the same amount on a new one works much better.

I wonder if the real yield on the new 5 Year TIPS in October will be below 1.1% (the current I Bond fixed rate). October may be an I Bond gift box period for me if that happens.

Thanks for the forecast. I thought the fixed rate would continue to stair step down in 10-basis point increments (1.3 1.2 1.1 1.0).

Looks like I will buy my remaining $5k in late October. In hindsight I should have maxed out my 2025 purchase in April. However, I’m glad I used the gift box when the fixed rate peaked at 1.3%. Given uncertainty about the accuracy of future inflation reporting, I will probably pause new I Bond purchases as long as the fixed rate stays below 1.0%.

If one believes the 25 basis point reduction in the Fed Funds rate is the start of a series of rate cuts extending into 2026, then the I Bond could be an attractive short-term play as well. In mid-September, the Fed will likely lower interest rates to the 4%-4.25% range from the current 4.25%-4.5% range. This will likely make the rate of return from a newly purchased I Bond in mid-October comparable to t-bills, for the ensuing 6 month period, but a superior investment for 12 months if further rate cuts arrive in 2026. And if you believe the Fed will be cutting rates even as inflation ticks up from tariffs being passed along to the consumer, which I do believe, then the gap between nominal and I Bonds could grow larger. I think a lot of us will have to think hard before passing up an October purchase or gift purchase. Is there any data on how steep the gap has been between I Bonds and T-bills in the past? I think that would make for an interesting chart, with columns for a one year comparison and five year comparison.

Doing a side-by-side comparison of the I Bond composite rate vs the then-current 4-week T-bill seems easy. Maybe over the last 10 years? During that time, I Bonds were a screaming buy, at times, versus T-bills (near zero nominal yields) and TIPS (negative real yields). I do think, though, that the current Fed has learned a lesson from the surge in inflation. The next Fed, maybe not.

Of course, when comparing I-bonds to short-term t-bills, you must factor in the limitation of having to hold the I-bonds for 12 months and losing 3 months interest if you redeem before 5 years.

Yes, true, (and don’t forget the tax deferral with I Bondsl), but that’s why I compare them to a 52-week t-bill and a 5-year t-bill for comparison purposes on the short-term side. The 52-week is a good comparison once you know the I Bomd inflation rate in mid-October. You can see right now that the 52-week t-bill is returning a rate of 3.763%. I believe that will decrease by mid-October (possibly by 25 basis points long with the Fed rate drop expected in September) and the I Bond should return closer to 4% for the current and ensuing 6 month period inclusive of the current fixed rate. The difference could be 50 basis points by then. Of course, the five year t-note comparison is more difficult to make ahead of time. Today it is trading at 3.69%. But with the I Bond, you have the flexibility of cashing in at any time over the five year period (yes, with the 3 month penalty) whereas with the 5 year t note you do not and have to sell it on the secondary market. I just think the I Bond is going to look attractive by mid-October as a short-term fixed investment.

But wait! What if the Trump tariffs are deemed illegal by the supreme court and the treasury has to refund the billions collected? Note what’s happening in the bond market today… interest rates are surging. This could skew the I Bond fixed rate back up in the final weeks before the reset.

It’s absolute futility to try to predict things these days.

It is difficult, true. But the 5-year TIPS is trading at 1.17% this morning — lower than last week.

Thanks for the new projection on the I Bond fixed rate. Re gifting I Bonds, you alerted us last year that Treasury was sending notices that holders of gifts should deliver them immediately, even if the recipient had maxed out the 2024 purchase limit. Eventually I received those notices for our accounts. I have made some new gift purchases this year for my wife who has maxed out purchases, but I’ve not seen anything about this from Treasury. Have you heard anything indicating that it is still OK (or not) to release gifts this year when the recipient has already maxed out purchases? I expect that you would have reported if there was any clarity, so maybe the better question is, if you have made gift purchases, are you having them delivered this year, even if the 2025 limit has been reached? Thanks as always.

I will say I am annoyed at the Treasury for not giving us guidance on delivering gift-box purchases. So I think we stand where we were last year: Have the recipient buy the standard purchase first, then deliver the gift I Bonds. I am not sure there is any limit on doing this. I delved into the issue in January: https://tipswatch.com/2025/01/05/great-mystery-an-i-bond-buying-guide-for-2025/

I am off the “gift-box wagon” for now, just because we have a good amount of I Bonds in two accounts.

While gifting is still an option, TD also allows one to split the ownership of Ibonds, ergo, one could possess more than $10K that a direct purchase would allow, i.e. TD is “encouraging” two methods that allow possession of more than $10K and it is not merely the “gift” route! Any change should be a regulatory change and should call for a change/deletion of the other two avenues! And, that I submit, why TD has done nothing except by implied ratification!

By 5/31/25, I purchased 10,000 I-bonds. Then in June 2025, I purchased 3,000 I-bonds in the wife’s gift box and delivered them to my account about 7 days later. No Problem. Also delivered over the limit in 2024 with no consequence.

0.9 % is not as nice as 1.2 or 1.3 fixed rate but it’s still a whole lot better than those lean years of the teens when the fixed rate was typically 0, 0.1, 0.2 in that range. By waiting until mid -year to buy your allocation you lose out on several months of interest.

Any purchase between May and October pays the same interest for six full months. The only difference is when the one-year clock starts. (I bought before the May reset.)

can we still purchase gift I-bonds.

Yes, that option is still open for people with a trusted partner. There has been no clarification on delivery limits, so I assume that door remains wide open. My perceived rule has been: Deliver AFTER the recipient has completed a maxxed standard purchase. This is based on personal experience last year. I don’t know of any change.