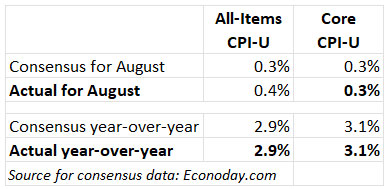

Annual all-items inflation rose to 2.9%, the highest level since January

By David Enna, Tipswatch.com

In what could be a crucially important report, the Bureau of Labor Statistics reported today that seasonally adjusted U.S. inflation rose 0.4% in August, higher than expected. The annual rate rose to 2.9%, up from 2.7% in July.

Core inflation, which removes food and energy, rose 0.3% for the month and held steady at 3.1% for the year. This matched expectations — meaning that overall this report should not raise market alarms. However, U.S. inflation remains too high.

The BLS noted that shelter costs rose 0.4% for the month, the highest monthly rate since January. The annual rate fell from 3.7% in July to 3.6% in August. More from the report:

- Food at home costs rose a troubling 0.6% for the month and are now up 2.7% year over year. The index for fruits and vegetables rose 1.6% for the month. Costs for meats, fish and eggs have increased 5.6% over the last year.

- Gasoline costs increased 1.7% in August after falling 1.9% in July. Gas prices are down 6.6% over the last year.

- Costs of new vehicles, which have been fairly stable throughout 2025, rose 0.3% for the month and are now up 0.7% for the year.

- Costs of used cars and trucks popped 1.0% higher for the month and are up 6.0% for the year.

- Medical care services costs fell 0.1% for the month but are up 4.2% year over year.

- Airline fares rose 5.9% in August, after rising 4.0% in July.

- Apparel costs rose 0.5% for the month but are up only 0.2% year over year.

Overall, this August report shows inflation continuing to run at a fairly high level, but so far there appears to be no dramatic “instant” effect from U.S. tariffs on imports. Here is the trend for all-items and core inflation over the last year, showing the steady march higher in all-items inflation since April:

What this means for TIPS and I Bonds

Investors in Treasury Inflation-Protected Securities and U.S. Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances for TIPS and set future interest rates for I Bonds. For August, the BLS set the inflation index at 323.976, an increase of 0.29% over July.

For TIPS. The August report means that principal balances for all TIPS will increase 0.29% in October, after rising 0.15% in September. Here are the October Inflation Index Ratios for all TIPS.

For I Bonds. The August report is the fifth of a six-month string that will determine the I Bond’s new inflation-adjusted variable rate, which will be reset November 1 and eventually roll into effect for all I Bonds. Inflation from April to August has increased 1.31%, which would translate to a variable rate of 2.62%. One month of data remains and we are probably looking at a new variable rate of 3.0% to 3.2%, higher than the current 2.86%.

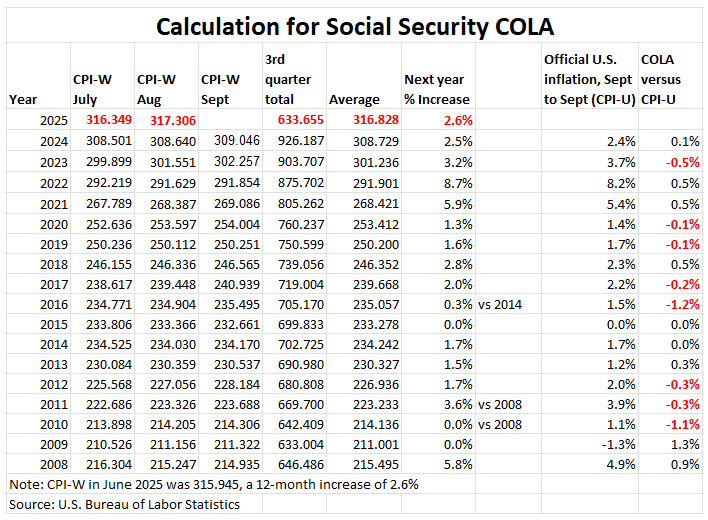

What this means for the Social Security COLA

The Social Security cost-of-living adjustment is based on an unusual inflation index – CPI-W – and is determined by averaging the indexes for July, August and September and comparing that number to the same average for the year before. For August, the BLS set the CPI-W index at 317.306, an increase of 0.30% over the June number.

With one month to go, here is where we are:

We are probably looking at a COLA of 2.7% once the September number rolls out on October 15. There is still a shot that my projection of 2.8% will work out.

What does this mean for future interest rates?

Although U.S. inflation remains too high, I believe the Federal Reserve will move forward with a 25-basis-point cut to short-term interest rates next week. A cut of 50 basis points should off the table. From this morning’s Bloomberg report:

While the report underscored that inflation remains above the Federal Reserve’s target, the reassurance that tariff hikes aren’t obviously sparking a generalized escalation in price pressures reinforced expectations for Fed policymakers to cut interest rates by 25 basis points at the Sept. 16-17 meeting.

From the Wall Street Journal:

In recent weeks, more Fed officials, including Chair Jerome Powell, have suggested that softer labor market conditions should give the Fed more comfort that they can assume price increases will be a one-off. … (T)he overall inflation picture in the first six months of the year wasn’t as ugly as many feared it would be in the wake of the tariff increases.

So it is highly likely that a rate cut is coming next week. What happens next will depend on the status of the U.S. job market.

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Supposedly the tariffs collected so far have been around $300 billion, which Trump and Bessent claim will be a “financial disaster” if forced to repayI’ve heard a number of reports that retailers have only been passing on a very small proportion of the tariffs, waiting for things to sort out, and taking the entire hit from the tariffs themselves so far. But once the “dam breaks” and any major retailer starts passing on the tariffs, the change in inflation could be abrupt and significant.

And as we remember from COVID, retailers often see opportunities to raise their prices when they have an “excuse.” I expect the excuse of “tariffs” will result in a larger increase than currently anticipated

This sounds accurate to me. As new products roll out, prices may increase. It was surprising that Apple seemed to hold the line on its new iPhones, but of course that company is cash rich.

Apple is exempt from tariffs.

Arthur, this is from NBC.com: “Apple hasn’t completely missed the tariff consequences. Cook said the company spent $800 million on tariff costs in the June quarter. … Apple warned it could spend $1.1 billion in the current quarter on tariff expenses.”

Normal international/domestic transactions for US Buyers would cover it by having the net price which may be adjusted up/down based upon an escalation clause..Buyers normally require any and all duties/taxes to be ultimately paid by the importers accounts! Exception is income tax of Buyer

Interesting anecdote in yesterday’s APM Marketplace interviewing a US manufacturer of bike parts. While the aluminum tariff is hurting them, changing their prices is very expensive and involves pushing the change through their resellers. As such they (and others like them) wait until they absolutely have to or have a natural breakpoint (like the calendar year, fiscal year, or industry-specific seasonality) to push through the price changes. An import-driven interviewee mentioned “how do I know what tariff I should price in? 15% 46% – it keeps changing.” Hearing things like this I think the tariff impact on inflation will be very drawn out in some areas (manufacturing) and more rapid in other areas (immediately priced items like fruit and veg).

35% of CPI is now imputed

The head of BLS was fired last month because Trump didn’t like the numbers

The CPI report today supposedly shows NO goods inflation due to tariffs

But we’re asked to believe the numbers are dependable

Keep in mind that nothing as really changed at the BLS, so far. The interim director is a long-time BLS official who has been interim director before. He is a “regular” and so I think up to this point, the BLS is doing its normal work (although with lower staffing). Trump’s appointee, EJ Antoni, will soon have a Senate confirmation hearing, which I predict is going to be very interesting.

I have two 0.4% fixed rate I Bonds. Would you recommend redeeming them to buy two of the current 1.1% fixed rate I Bonds? I feel like others will be facing a similar decision. Is there a way to figure out how long it would take to break even on that exchange?

I am doing the same thing you are considering. Redeeming 0.4% and buying 1.1% I Bonds. I haven’t calculated the break even time, but I plan to hold the 1.1% I Bonds for many years, so I know they will earn more long term. I have already factored the interest earned at redemption into my 2025 taxes, that is a consideration as well.

The difference is $7 per $1000 of bonds for each year held. I would lookup the value of the 0.4% bonds which will include the 3 month penalty if before 5 years along with the estimated tax you will pay for the redeemed interest and see when the $7 per $1000 addition breaks-even compared to just holding them. It has been my experience the break-even point typically ranges between 2.5 – 3.5 years.

Rick’s response gives a rough way to estimate. You can use the Savings Bond Calculator to determine the current value of those 0.4% I Bonds: https://www.treasurydirect.gov/BC/SBCPrice (It will not show the last three months of interest if the I Bond is less than 5 years old.) I am figuring these I Bonds were purchased in the Nov 2022 to April 2023 period, so they will have the three-month penalty.

If you purchased $10,000 in Nov 2022 the current value is $11,100 and the current composite rate is 3.27%. If you redeem you will owe taxes on the $1,100 — maybe around $250? And you will give up three months of interest — $92. But you will also have some extra money you can invest or spend.

If you reinvest $10,000 in a new 1.1% I Bond, you are going to earn about $70 a year in additional interest, compounding with inflation. So all in all it could take about 4 1/2 years to break even, given the tax hit and 3-month penalty. If this is a long-term holding, it makes sense.

Question, responding to David’s comment above about what “makes sense”: If the break-even time is reasonably predicted to be 4 1/2 years, then would the definition of “long-term” likewise begin around 5 years, when the interest penalty for early redemption of any 1.1%-fixed replacement bonds purchased during the current rate period before the end of October would also end?

Elsewhere in these comments there’s talk about great rates on 20-year TIPS, but based on current age and family longevity history, my wife and I are definitely not going to be alive in 20 years, maybe not even in 15. I continue to weigh the pros and cons of redeeming I Bonds which have a 0% or 0.4% fixed rate, and have high “embedded” inflation earnings from 2022/2023, and are getting close to the end of their five-year penalty period, just to buy new 1.1% fixed and thereby start a whole new cycle of redemption restrictions or penalties. But maybe it still makes sense if we expect to hold the bonds for at least five years or longer?

In 2024 and early 2025, using our multiple TreasuryDirect accounts and making extensive use of the gift box workaround, we did replace a lot of older 0% I Bonds with new 1.2% and 1.3% fixed, so that we no longer have any bonds older than 2021, and the 0% and 0.4% bonds that remain represent less than a third of our overall I Bond portfolio.

Based on this response, I think the better play is to hold the 0.4% Fixed rate I Bond until I need the cash or for at least the remainder of the five year period since it’s half way there, and just buy a new 1.1% fixed rate I Bond in October for the long-term if I decide to do so then. The 0.4% fixed rate I Bond will earn 3.0% to 3.2% + 0.4% = 3.4% to 3.6% for the ensuing 6 month period which is probably market value or netter than market value by the time the Fed is dine cutting rates. The 1.1% fixed rate I Bond will earn 3.0% to 3.2% + 1.1% = 4.1% to 4.3% and is the better long-term hold without needing almost 5 years to break even. Thanks fellas.

TipswatchChat, if you can reasonably hold 5 years, it would probably make sense to roll over. But maybe not with the 0.4% fixed rates. I’d keep those until the last-ditch roll over. (Then again, the fixed rate could be declining in the future.) I am 72 and I have now outlived both my parents. But I am in good health. I probably can live another year … or 20 years. No way to know.

You can still get 1.63% real yield on a TIPS maturing in January 2035, but is that really fantastically superior to an I Bond at 1.10%? My opinion: They are about equally attractive, because the I Bond has so many advantages: tax-deferred interest, flexible maturity, solid deflation protection, fully compounded interest.

The TIPS maturing 15 and more years out paying more than 2% over inflation look pretty good to me if there is going to be continued inflation on and on.

I agree. The 10-year real yield has dipped to 1.69% but the 20-year is trading at 2.32% today, historically attractive.

A belated but heartfelt thanks for focusing me on the 2%+ real yields available a while back. I was lucky enough to build a ladder from ’26 to ’35 and 40′ to 45′ all at yields greater than 2%.

Looks to me like to buy today the longer TIPS will cost about 5% more than a they did a couple weeks or so ago. Getting some TIPS bonds paying way over 2% above inflation locked in long term is what I did too.

Inflarion from the TTT (Trump Tariff Tax) is gradually leaking into the economy. From April, inflation has incrementally increased from 2.4% to 2.5% to 2.7% to 2.9% with core now holding steady at 3.1%. As Powell previously said, the Fed would’ve already cut interest rates had there been no tariffs.

This says it best. “When they cut next week, they will not be cutting because we have good news on inflation. They’ll be cutting because we have bad news on employment.”

With the likelihood of more rate cuts ahead, locking in the current I Bond in October with the 1.1% fixed rate at around 4% for the current and ensuing 6 month period seems like an even better decision now.

But goods inflation is “reported” to NOT have increased

Almost all of today’s increase is attributed to the shelter component

So either we’re being lied to, or inflation from TTT is yet to enter the economy

I’m definitely a skeptic of this regime but much more inclined to believe the latter point – inflation from TTT is a future event.

There has been a cycle of deliberate confusion on the effective dates of the tariffs, first with the April announcement, then various delays, proclamations that turned out to not be true, carve-outs and re-negotiations. Companies were not prepared to take price actions and their decisions were delayed by the intentional uncertainty.

Meanwhile, the supply chain is only able to work a tariff / tax increase of this kind into prices over several months to even years. When it nets out – the total of tariffs collected will represent money removed from free market economic activity. A ton of it will be in goods prices.

I’m not sure that’s the case. From The NY Times:

The issue for the Fed is that Mr. Trump’s levies have pushed up costs across a wide range of goods, upending earlier progress on bringing inflation down. Declines in other categories have limited the overall increase, helping to placate earlier fears that the resulting inflation surge would be much more intense.

One of those offsets had been energy prices but those costs accelerated sharply in August. Gasoline prices jumped 1.9 percent over the month, contributing to a 0.7 percent increase in the overall energy index. Airfares spiked 5.9 percent in August, following a 4 percent increase the previous month.

The impact of Mr. Trump’s tariffs on the automobile sector also showed through more notably in August, with prices for new and used vehicles rising after several months of more muted gains. The index tracking new vehicles increased 0.3 percent in August and is up 0.7 percent compared to the same time last year. Prices for used vehicles rose 1 percent and are up 6 percent from a year earlier.

Household furnishings also became more expensive in August, as did clothing. Shelter prices rose 0.4 percent, the largest contributor to the overall monthly increase. Food prices rose 0.5 percent over that same period, and 3.2 percent compared to last year. Coffee prices in particular have jumped significantly: They are up nearly 21 percent compared to August 2024, and in August alone, rose 3.6 percent.

“Tariffs are a tax. It’s a regressive tax that is causing a bifurcated retail community where only companies that have decent pricing and high quality are doing well,” said Nancy Lazar, chief global economist at the investment bank Piper Sandler. “Weak consumer spending is going to put downward pressure on certain prices.”