Are we entering an era of lower real returns?

By David Enna, Tipswatch.com

The U.S. Treasury on Thursday will auction $19 billion in a reopened 10-year TIPS, CUSIP 91282CNS6. This will be a notable auction because the real yield to maturity is likely to fall to a two-year low, a level not seen at auction since July 2023.

CUSIP 91282CNS6 had its originating auction two months ago, on July 24, when its real yield to maturity came in at an attractive 1.985%. The coupon rate was set at 1.875%. But in the last two months, real yields have dipped fairly dramatically.

This TIPS trades on the secondary market, where it closed Friday with a real yield of 1.69% and a price of 101.64. The price is at a premium because the real yield has dropped below the coupon rate. You can track the current yield and price on Bloomberg’s Current Yields page.

Definition: The “real yield to maturity” of a TIPS is its yield above official future U.S. inflation, over the term of the TIPS. So a real yield of 1.69% means an investment in this TIPS would provide a return that exceeds U.S. inflation by 1.69% for 9 years, 10 months.

One day before Thursday’s auction closes at 1 p.m. ET, the Federal Reserve is highly likely to cut short-term interest rates by 25 basis points and signal that future rate-cutting is coming in an effort to support a sagging job market. The 25-basis-point cut is already priced into CUSIP 91282CNS6’s yield, but comments by Fed chair Jerome Powell Wednesday afternoon could set the bond market roiling. In other words: Expect volatility in the hours leading up to the auction.

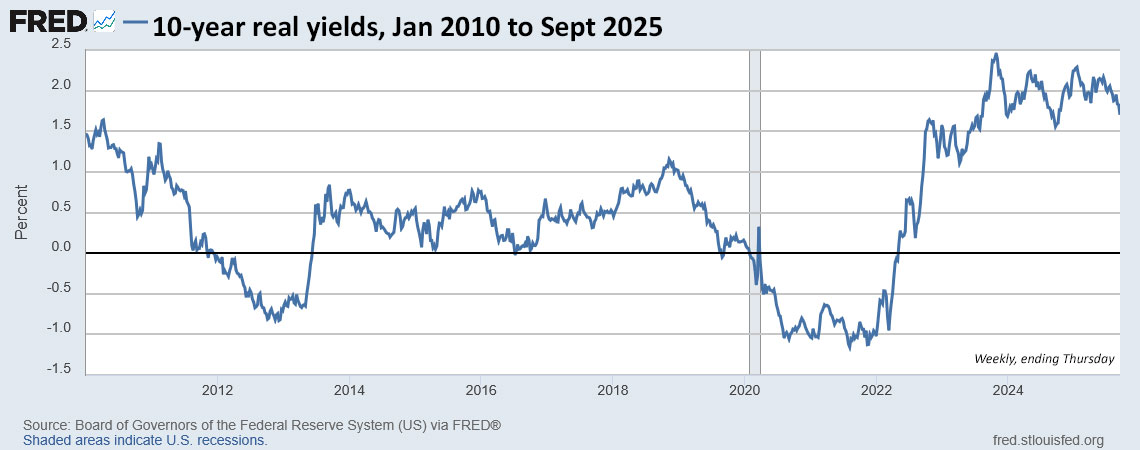

Here is the trend in the 10-year real yield over the last 15 years:

The chart shows that the current real yield of 1.69% remains historically attractive, but has fallen well off the October 2023 high of about 2.55%.

Pricing

At Friday’s close, CUSIP 91282CNS6 was trading with a real yield of 1.69% and a price of 101.64. In addition, on the auction’s settlement date of September 30, this TIPS will have have an inflation index ratio of 1.00602. With that information, we can estimate the cost of a $10,000 par value investment at the auction:

- Par value: $10,000

- Accrued principal on settlement date: $10,000 x 1.00602 = $10,060.20

- Cost of investment: $10,060.20 x 1.0164 = $10,255.19

- + accrued interest of about $39.47

Again, this is an estimate based on Friday’s closing price. In this scenario, the investor would pay $10,255.19 for $10,060.20 of principal on the settlement date, and from that point on would earn inflation accruals plus a coupon rate of 1.875% until maturity. Things will change before Thursday, but this gives you an idea.

Inflation breakeven rate

The 10-year Treasury note closed Friday with a nominal yield of 4.06%, giving this TIPS a current inflation breakeven rate of 2.37% –in line with recent auctions of this term. That means CUSIP 91282CNS6 will out-perform a nominal 10-year if inflation averages more than 2.37% over the next 9 years, 10 months. Inflation over the last 10 years, ending in August, has averaged 3.1%.

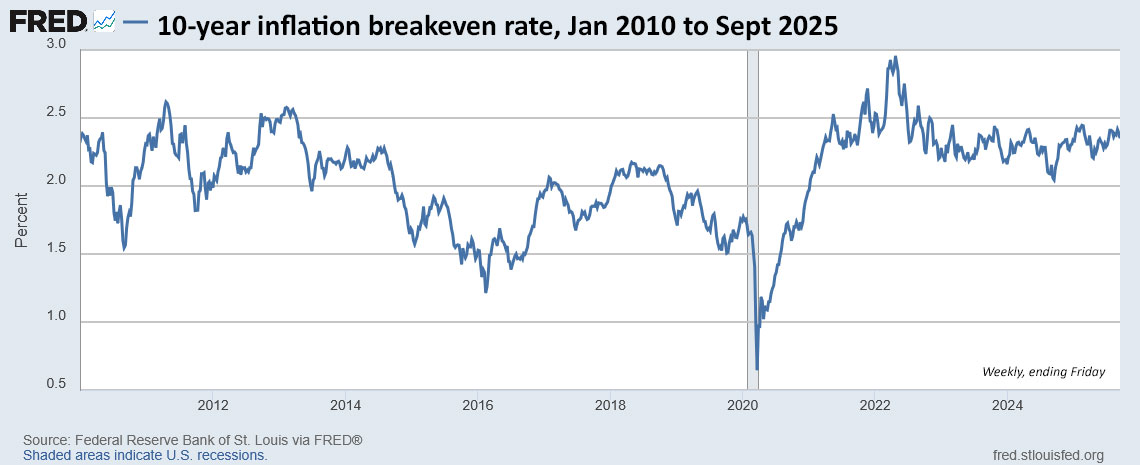

Here is the trend in the 10-year inflation breakeven rate over the last 15 years, showing the fairly stable pattern since the closing months of 2022:

Thoughts

Real yields for TIPS of short- to medium-terms have been falling over the last several months, in anticipation of future rate-cutting by the Federal Reserve. This could indicate a trend that will continue well into 2026, especially if the U.S. economy dips into recession. Or … it could be an overshoot to the low side. The Federal Reserve on Wednesday may help clarify this issue (but probably won’t).

I will not be a buyer at this auction because I have my sights on the January 2026 auction of a new 10-year TIPS, to add 2036 to my TIPS investment ladder. Will real yields be quite a bit lower by then? Maybe. I’ll wait it out.

Keep in mind that despite the boost from tariff revenues, the federal deficit is highly likely to continue increasing for years into the future. That will mean more borrowing and — potentially — higher yields. Note that the 20-year TIPS still has a real yield of 2.17% and the 30-year, 2.43%.

Relevant side note: This TIPS auction size of $19 billion will be the highest in history for any 10-year TIPS reopening. This is a 12% increase over last year’s September auction at $17 billion.

Also, note that if you have a brokerage account, there is no compelling reason to buy this TIPS at auction versus on the secondary market, unless you plan to make a small purchase at TreasuryDirect.

The advantage of buying at auction, especially through TreasuryDirect, is that even small-lot purchases will get the auction’s high yield. The advantage of the secondary market is that you can see exactly the price and real yield you will be receiving. The negative is that you may face a small bid-ask spread. Most of the time, it doesn’t make a huge difference, but if you see a real yield you like, know that you can probably get it on the secondary market without dealing with the auction’s uncertainty.

This TIPS auction closes Thursday at 1 p.m. ET. Non-competitive bids at TreasuryDirect must be placed by noon Thursday. If you are putting an order in through a brokerage, make sure to place your order Wednesday or very early Thursday, because brokers cut off auction orders before the noon deadline.

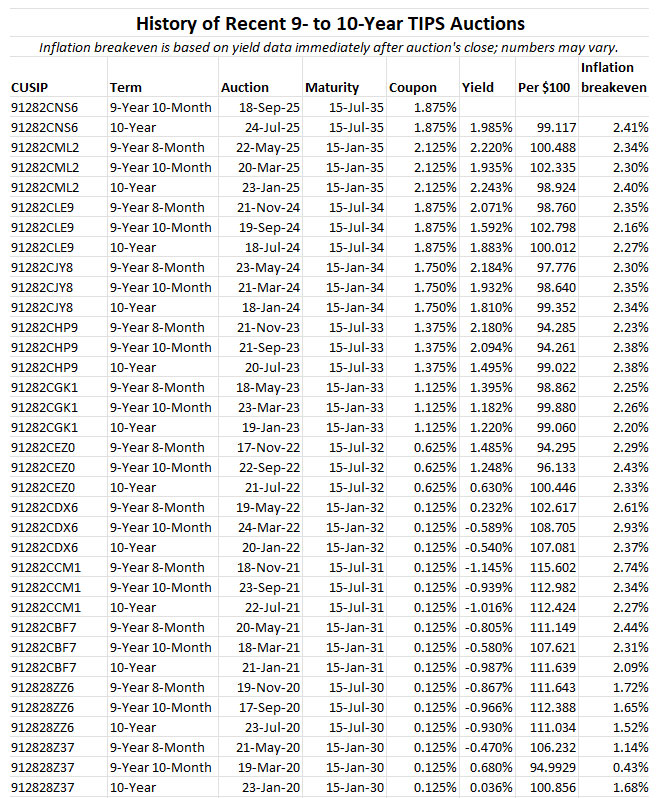

I will be posting the auction results soon after the close on Thursday. Here is a history of auction results for this term over the last 5 years:

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

You mentioned that you skipped this auction so you could focus on the 2026 auction to populate your 2036 rung. What are the chances that a whole lot of people and institutional investors will do the same causing such high demand that the resulting yield is very low for the 2036 TIPS?

Not likely. Sure. the yield could be lower (or higher) but I don’t expect outsized demand for that auction. This term is auctioned every other month.

Hi David,

I just read the following in WSJ with Greg Ip making a case for buying Gold:

…You could hedge against inflation with Treasury inflation-protected securities, or TIPS. But last month, Trump fired the commissioner of the Bureau of Labor Statistics after it reported unflattering jobs data, and nominated a partisan supporter to replace her. Investors must now weigh the risk the BLS will change the consumer-price index to lower reported inflation. That would undercut the protection offered by TIPS, which are indexed to the CPI. Gold isn’t….

I have many close friends who are Gold bugs who have tried for years to convince me to buy GLD or Miners….I have not done so. Your thoughts?

I’m not into gold but I can see the reasoning. It’s an investment I don’t understand. (Same for Bitcoin).

There is probably some kind of financial formula that could be devised to estimate the fair value of gold using the amount of fiat currency in circulation, the underlying economic value and the amount of physical gold in existence.

The 10-year nominal is still running close to your percentage, at 4.03%, and the 10-year TIPS at 1.658% in after hours. With a breakeven still at about 2.37%, what kind of a return could we be looking at in 10 years if say inflation is about 3%: close to a 4.65% return (1.658 + 3)? Thanks, David.

Yes. If inflation runs at 3%.

I heard something about an expansion in Euro Bond offerings, purportedly to fund increased European defense spending. Could be another investment avenue.

I’m a little confused by the difference between the numbers in the Bloomberg “Current Yields” page you linked to, and the numbers in the Treasury’s “Daily Treasury Par Real Yield Curve Rates” page:https://home.treasury.gov/resource-center/data-chart-center/interest-rates/TextView?type=daily_treasury_real_yield_curve&field_tdr_date_value=2025

It looks like you got the numbers in this sentence from the 9/12/2025 row of the Treasury’s page:

However, the Bloomberg page shows 2.32% in the Yield column for the 20 Year in the TIPS table (as of the evening of 9/15/2025). (The 30-Year number is much closer to the Treasury’s though at 2.41%.) Do you know why the numbers are so different in the Bloomberg page? Is it measuring something different?

Yes, they do show different things, and for potentially different points in time. The Bloomberg page shows real-time trading of the most recent TIPS on the market for each term. Since no 20-year TIPS are issued anymore, it is showing a 30-year that matures closest to that date, Feb 2045. The Bloomberg page updates constantly during trading hours. The Treasury page is showing its estimate for a full-term TIPS for each term and updates only at the end of the market day.

These numbers will usually be fairly close, but sometimes there are variations. The Bloomberg page is a good guide for purchasing a reopened auction TIPS or a secondary-market TIPS. The Treasury page is a good guide for new TIPS at auction.

One complication is that the secondary market 20-year always has a large inflation accrual (currently 37%) which puts a shift in its market value. The Treasury is estimating a “par value” TIPS, minus any inflation accrual. The 30-year on the Bloomberg page was issued this year so its market value isn’t skewed as much. Its inflation accrual is only 2.2%.

With the US dollar’s international trade value on a persistent path down, will TIPS or I-bonds protect cash assets value enough to compensate?

In theory, a declining dollar should result in somewhat higher inflation, which would be reflected in the I Bond and TIPS returns. As a frequent world traveler, I can say I have enjoyed the strength of the U.S. dollar over the last decade. But that isn’t true in 2025 — it is down more than 10% year to date.

Two recent articles on the decline in real yields:

https://www.dws.com/en-us/insights/cio-view/charts-of-the-week/2025/us-real-yields-is-the-trend-turning-downward/

https://www.reuters.com/markets/currencies/real-rate-dip-threatens-pull-down-dollar-2025-09-10/

Rising inflation expectations against the backdrop of Fed rate cuts seems to be pulling down real yields, especially the 5-year TIPS.

If real rates are falling like a knife, I guess the question you have to ask yourself is at what level of real rates do you reject the investment. You have a regular contributor that says he may no longer buy I-Bonds with a fixed rate below 1.00%. Is there a minimum acceptable real yield for TIPS?

I totally stopped investing in TIPS with negative real yields — what a downer that was. The problem is that when real yields decline, you also get more or less equal declines in nominal yields — T-bills and T-notes, bank CDs, money market funds, etc. Safe investments become less attractive. … On TIPS, it’s easier to accept lower real yields on the 5-year (it’s just 5 years). Harder on the 10 year, but anything above 1% would remain acceptable, in my opinion. The 10-year real yield fell below 1% from April 2011 to October 2018, more than seven years.

As a more recent TIPS investor this is helpful perspective David. I have never fully wrapped my head around negative real yields – except you lose out to inflation, but less than might be lost through nominal treasuries? Either way it doesn’t sound good and I hope I don’t have to deal with it.

Your opinion that anything above 1% real yield is acceptable for you is helpful and makes sense. We each have our own criteria and thresholds, while understanding that TIPS are primarily for preservation of buying power. 1% plus is good for me as well, hope it doesn’t become less, and more is always welcome.

David, thanks for the analysis. Very helpful. Last year around this time when the Fed cut rates, the 10-year TIPS real yield rose to about 2% and above for several months. Wondering if it would make sense to wait until the November reopening of this 10-year TIPS or like you said, maybe even wait for the new one in January. I purchase on TD so trying to avoid the premium.

Impossible to say. Real yields appear to be trending lower but often turn on dime.