Oct. 24 update: September inflation report sets I Bond variable rate at 3.12%

Oct. 12 update: I Bond fixed rate projection just fell to 0.90%

Oct. 10, 2025 update: The Trump administration has allowed the BLS to recall staff to prepare the September inflation report, which was due to be released Oct. 15. It will now be released at 8:30 a.m. Oct. 24, before the Federal Reserve meeting Oct. 28-29.

This is a wise move. The BLS noted: “This release allows the Social Security Administration to meet statutory deadlines necessary to ensure the accurate and timely payment of benefits.” The report will set the Social Security cost-of-living adjustment, Medicare fees and IRMAA levels, and the I Bond’s new variable rate.

By David Enna, Tipswatch.com

With the U.S. government on indefinite shutdown and the Treasury market showing signs of unease, the November 1 rate reset for the U.S. Series I Savings Bond is looking mighty unpredictable. It’s reasonable to ask: Will they call the whole thing off?

Time will tell. Naturally, I would love to see a resolution to this shutdown crisis in the next week, well before crucial release of the September inflation report on October 15 at 8:30 a.m. If we get that report before the end of October, a lot — but maybe not all — of the unpredictability will fade away.

Also read: TreasuryDirect email is an omen of coming changes

The basics

The Series I Savings Bond is a unique inflation-linked U.S. Treasury issue that earns interest based on combining a fixed rate and an inflation rate. All these rates will change November 1 for purchases between November 2025 and April 2026:

- The I Bond’s current composite rate is 3.98%, annualized, for a full six months for any bond purchased through October.

- The fixed rate will never change. Purchases through October will have a fixed rate of 1.10% for the 30-year life of the I Bond.

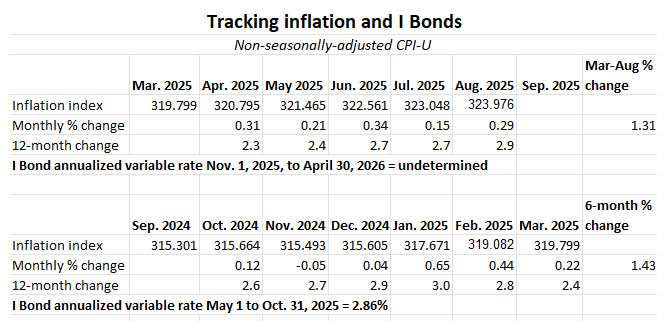

- The inflation-adjusted rate (often called the variable rate) changes each six months to reflect the running rate of inflation. That rate is currently set at 2.86% annualized. It will adjust again November 1. Each new variable rate applies to all I Bonds, no matter when they were purchased.

The problem: Variable rate

Without the release of the September inflation report, there is no way the Treasury can accurately set the I Bond’s new variable rate or composite rate in any traditional way. The same is true for the updated composite rates for all I Bonds ever issued. We need that September inflation report.

The new variable rate will be based on inflation for the six months of April to September 2025, which through five months has totaled 1.31%. That translates to a variable rate of 2.62%. If non-seasonally adjusted inflation for September runs at 0.3% (seems possible), the six-month inflation number becomes 1.61% and the variable rate rises to 3.22%, higher than the current 2.86%.

Without the September number, this calculation becomes impossible. So what will the Treasury do on November 1 if the shutdown continues? Regular reader and commenter Patrick found a potential answer in the Code of Federal Regulations.

If the CPI-U for a particular month is not reported by the last day of the following month, we will announce an index number based on the last 12-month change in the CPI-U available. Any calculations of our payment obligations on the inflation-indexed savings bonds that rely on that month’s CPI-U will be based on the index number that we have announced.

The I Bond regulations don’t give any further information on the process or formula, but inflation analyst Michael Ashton wrote about this in a September 2023 article on TIPS titled: What Happens if CPI Isn’t Released?

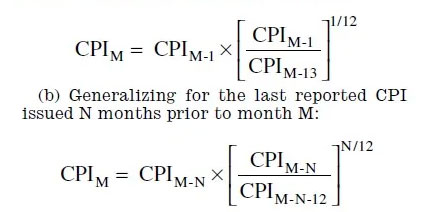

Title 31 of the Code of Federal Regulations spells out what would happen if the BLS didn’t report a CPI by the end of October. In a nutshell, the Treasury would use the August CPI index, inflated by the decompounded year-over-year inflation rate from August 2022-August 2023.

Today’s relevant calculation would be for inflation from August 2024 to August 2025. And look out, here comes the formula:

I find this to be gibberish (I’m just a journalist) but Tipswatch reader D did post an attempt at the calculation:

September 2025 = August 2025 * (August 2025 / August 2024)^(1/12)

= 323.976 * (323.976/314.796)^(1/12) = 324.753

If the fabricated September number ends up being 324.753, you get non-seasonally adjusted inflation of 0.24% for September, a six-month inflation rate of 1.55% and a new variable rate of 3.10%. My guess is that could be slightly underestimating current inflation, but we won’t know until the true September inflation report is issued.

One thing remains unclear: Once it has the correct number, would the Treasury immediately update the composite rates for all I Bonds ever issued? This isn’t a huge factor in the short run, since I Bonds assign interest at the end of each month. Any redemption in October would get an accurate payment based on the September total. But I would hope the composite rates would be updated to be accurate.

Another problem: The fixed rate

Now we have a quandary that has nothing to do with the government shutdown: What will be the I Bond’s next fixed rate? This is important to investors because the fixed rate is permanent and creates the “real yield” — the yield above inflation — for the I Bond.

The Treasury has no announced formula for setting the I Bond’s fixed rate, meaning there is no calculation required by law or regulation enforcing the process. It is up to a decision by Treasury officials. However, I Bond watchers have settled on a forecasting tool that seems to work: Apply a ratio of 0.65 to the average 5-year TIPS real yield over the preceding six months. This formula has worked without fail at least since 2017.

With less than a month to go, I looked at 5-year real yield data from the date of the last reset on May 1, 2025, to the close of Oct, 3, 2025. Looking at just that data, the forecast is for a new fixed rate of 1.00% at the reset.

I Bond fixed rates are always set to the tenth decimal point, so that means the projection has to be rounded. If you look at the top of the chart, you can see the 0.65 ratio results in 0.9539%, a razor-thin margin to round to 1.00%. So at this point, with 18 market days remaining, the fixed rate would “likely” be 1.00%.

But what if the 5-year real yield continued at the current level — 1.34% — for those 18 market days? If that happened, the 0.65 ratio results in 0.9421% and rounds down to a fixed rate of 0.90%. Again, this is a razor-thin margin.

My “guess” is that we are heading toward a fixed rate of 0.90% but that won’t happen if real yields begin to climb for the next few weeks. We have already seen the Treasury’s estimate of the 5-year real yield climb from 1.17% on Sept. 16 to 1.34% at Friday’s close. That could be caused by unease over future Federal Reserve rate cutting or the government shutdown causing a distaste for U.S. Treasury investments, or both.

Whatever happens, I feel confident the Treasury will set the fixed rate at either 0.90% or 1.00% at the November reset, as long as it continues following practices of the last decade.

What’s the strategy?

Will the Treasury call the whole thing off? No. It looks like it has a backup plan, even if it is a lousy backup plan.

My thinking: I Bond investors who haven’t purchased their full allocation ($10,000 per person per calendar year) should consider making a purchase before the end of October — I’d suggest Oct. 28 to give a margin of safety. An I Bond purchase late in the month earns a full month of interest. But don’t cut this too close to Oct. 31.

Buying in October locks in the current fixed rate of 1.10%, which is likely to go lower for purchases after November 1. It also locks in the current composite rate of 3.98% for a full six months, and then a potentially higher composite rate in the next six months. That sort of yield should be competitive with T-bills if the Fed continues reducing interest rates this year and next.

More aggressive I Bond investors could also look to bypass the purchase cap by making “gift box” transactions in October, which require a trusted partner. More on this. Additional purchases can also be made through trusts or business-owner strategies.

Is a fixed rate of 0.9% to 1.10% still attractive? I say yes, if you consider I Bonds to be a secondary store of emergency cash, always adjusting higher for inflation. Hold for five years and then redeem when you need the money.

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

“The Labor Department will bring back staff to work on a key consumer inflation report despite the ongoing federal government shutdown, CNBC has learned. The department’s Bureau of Labor Statistics will “promptly resume” work on September’s consumer price index data, a White House official said. The report will come out at 8:30 a.m. ET on Oct. 24, nine days after it was originally scheduled, according to the BLS.” -CNBC.

It looks like we’ll get the CPI numbers to calculate the variable rate for I-bonds on Oct. 24, and, I guess, Social Security COLA too.

It’s painfully obvious at this stage that the people running the Treasury Department, and particularly the I Bond program, are idiots.

How else to explain the utterly confusing emails that are still to this day being sent out? They’ve had a year to figure out what to say. All they are doing is making work for the poor souls that answer customer calls – and they don’t even give them a consistent explanation.

Not to mention the World’s Worst Website. They haven’t even figured out how to incorporate the back button!

Hiring more people won’t fix this. Firing those in charge and hiring better people will.

This is the first time I have received an email from Treasury Direct. Thoughts?

“Dear TreasuryDirect Customer,

Treasury is always looking for ways to enhance your experience. This includes simplifying the gift bond delivery process. Our records show that your account holds undelivered gift bond(s). To best prepare for coming changes, we recommend delivering your gift bond(s).”

I also received the same email today that had the following paragraph:

“While there may be changes to the gift bond program to help streamline the process of investing with the U.S. Treasury, there is no impact to your participation in the gift bond program at this time. Stay tuned as more information becomes available on how we’re enhancing the TreasuryDirect customer experience.”

I pretty sure we got this same email a year ago to clear out our gift boxes. It stirred a lot of speculation of pending changes, but nothing was ever changed.

The key words this year seem to be … “To best prepare for coming changes.” Have to wonder what that means.

If TD or the government was at all interested in the public to best prepare for…then it would provide more due process, public notice of “proposed” changes, use the Federal Register (minimum of 60 days notice), solicit and consider public inputs before any implementation. Otherwise non-compliance with the Administrative Procedure Act could dampen a “best prepare” experience!

If “Treasury is always looking for ways to enhance your experience,” Treasury could, of course, employ enough people so that I Bond buyers won’t have to wait half a year or more for Treasury to convert paper bonds to electronic bonds in a trust account, or to process a medallion-guaranteed Treasury form required to move eectronic bonds from an individual account to a joint trust account–both of which our household has experienced, more than once in the case of the individual-to-trust transfers. (Our latest submitted paperwork was acknowleged by Treasury in early May, and we’re still waiting.) Multiple threads on the Bogleheads forum, among others, have cited this issue, a particular headache for anyone serving as executor for a deceased person with TreasuryDirect holdings.

But, of course, that’s not the kind of “enhanced experience” the issuers of the memo had in mind, i.e., services being rendered by human employees to human customers, as opposed to tweaks to online customer SELF-service. And no one should expect things to improve in the current atmosphere regarding federal hiring.

Received another email today from TreasuryDirect advising me to deliver gift bonds.

In case anyone is wondering the gift procedure is still working. I had already made our regular purchase beginning of the year. Plus, bought and delivered 2 sets of gifts bonds in April. I bought another 2 sets last week and delivered them Monday. All went thru no issues. Not sure why I still received the email.

Dear TreasuryDirect Customer,

Treasury is always looking for ways to enhance your experience. This includes simplifying the gift bond delivery process. Our records show that your account holds undelivered gift bond(s). To best prepare for coming changes, we recommend delivering your gift bond(s). Delivering gift bond(s) enables your recipient to experience the full benefit of your gift.

Grows Investments and Financial Awareness: Delivering gift bond(s) to younger recipients can give them a head start on financial literacy. These bonds may also serve as valuable resources for tuition costs or other important life expenses down the road.

Promotes Timely Access and Ownership: Maybe you’re waiting for a certain milestone to gift your bond or simply haven’t gotten around to it. Remember, the registered recipient is the sole legal owner of the bond as soon as you purchase it. Delivering the gift bond promptly ensures the smoothest gifting process.

I got this too, and just after having posted here. I wonder if they’re watching :-0

I jest, of course.

>than the 10K limit works?

Thanks so much for all your good info. It has been of great help in the run-up to retirement. Thanks in part to the education you’ve given me, Spouse and I purchased several years worth of gift-box iBonds for each other this year as part of our transition to retirement planning. We successfully ran the experiment with annual purchases followed by delivery of one year worth of gift box last year but don’t plan to double up like that in the future unless prompted by TD. We plan to stop purchasing this month and deliver our birthday presents to each other over the next few years.

Hi, looking for some help in purchasing I Bonds this month …

In 2024 Spouse and I purchased 40k of I Bonds … 10k each personally and then 10k to each other via gift box (which were delivered shortly after purchase). Can we purchase more this year (2025) and if so how?

Would we be able to purchase for ourselves individually (10k each), through gifts to each other (10k each), or both for another 20k each?

Sorry I’m kind of confused by this

For what it’s worth, I think I Bonds look attractive for our investment plans as we bridge to Social Security over the next 10 years. Treasury rates are dropping and I could see inflation increasing over that time frame.

All the anecdotal evidence, including my experience earlier this year, is that you can buy I Bonds the traditional way in 2025, as long as you did not deliver any gift-box purchases this year. https://tipswatch.com/2025/01/05/great-mystery-an-i-bond-buying-guide-for-2025/ It also is highly likely you can make additional gift-box purchases, although I haven’t done that. Others have. My best advice is to go into TreasuryDirect and make the purchase. Let us know if they fails for any reason.

Holding for 5 years is ideal, but in some cases it makes sense to redeem early and repurchase at the higher fixed rate. If you are in a lower tax bracket and are strategic about the timing of redemptions, you can minimize the early redemption penalty and recoup the lost interest in less than a year.

I decided to redeem $5,000 in principal of April 2023 I Bonds with the 0.4% fixed rate in order to buy another $5k with the 1.1% fixed rate. Due to the recent low 1.9% variable rate, the early redemption penalty for April ’23 bonds redeemed this month is at its lowest point since first issue (only $6 per $1,000 in October vs. $6.40 in September, $6.80 in November and $8 in December). I figured a $30 penalty was acceptable to earn an additional $35 of annual interest going forward.

Anyone considering swapping 0.4% fixed rate I Bonds for the 1.1% fixed rate before October 31 (and resetting the 5-year clock) might want to follow this strategy. It makes the most sense if you are in a low tax bracket and plan to make the new higher fixed rate I bonds a long-term holding.

Do we know what happened when the gov’t shut down for 35 days during 2018-2019? What did Treasury do then?

This is interesting, because the shutdown started on Dec. 22, and the November inflation report was released on Dec. 12. So no effect there, and a December report is no way as important as the September report for its effect on I Bonds, Social Security, Medicare levels, etc. The December inflation report was released on schedule on January 11, during the shutdown. (The shutdown was over border wall funding.) The BLS was funded during this shutdown, which is different from our current crisis. https://www.bls.gov/bls/shutdown_2019_empsit_qa.pdf

Yes, the best course of action seems to be maximum buying of the 1.1% fixed rate I-Bonds before 11/1, because that could be your last chance to get a fixed rate above 1% for a long time.

Great post. Very informative without a hint of politics!

Aiming for that as often as I can.

So as you go to press for above article, the forecast would be 3.1% + 1.0% or a composite of 4.1% at November 1st reset for new ibonds…is that what we are reading?

I’d say the fixed rate is more likely to be 0.9%.

This is very helpful and obviously timely information. Unless there is a huge surprise to the upside (or downside) waiting in the September CPI Report, the formula, should it be used as described, seems to approximate what we can expect if it wasn’t needed. A buyer of this I Bond will get 3.98% for the first 6 months and should get 4.2% for the following 6 months.that averages out to just under 4.1% for a year. The current 52-week rate is 3.64%, so the delta in buying this I Bond from a nominal treasury is just under a half a percent, which makes it a short-term buy. And the 1.1% fixed rate makes it a mid-term and a longer term buy. Add in the fact that the Fed is expected to lower rates again this month (and again in early 2026), despite slowly rising inflation and tariffs still percolating through the economy, and this I bond seems like an attractive buy no matter how you look at it.

Good analysis

You said, “The current 52-week rate is 3.64%, so the delta in buying this I Bond from a nominal treasury is just under a half a percent, which makes it a short-term buy.”

If you redeem just after the 12 months hold on the I-Bond it works out 4.1% divided by 12 months x 9 months of interest = 3.07%. I’m not sure it would be a “short-term” buy. But I will be buying it for the longer term.

short-term buy, not short-term buy and sell.

Doug, I will write about this later this month, but I Bonds do not make sense as a one-year investment, given the 3-month interest penalty. T-bills are likely to do better. Investors in I Bonds should look at stacking up holdings for 5 years, to avoid the penalty. Or … if a very attractive fixed rate comes along … redeem and invest.

I would not buy iBonds for a year either, but note that buying late in a month and selling early in a month can make it close to 3% for 10 months for a motivated saver.

Actually, it works out to 11 months.

I use I Bonds as an emergency fund and will sell them before 5 years as needed. The inflation protection is worth the potential downside of 3 months lost interest to me.

It’s great that you are going to write about this soon. I look forward to the article.

I assert that there are times when selling an I Bond held for less than five years absolutely makes financial sense, and not just because you have a need for the cash.

For example, I bought a $5,000 I Bond on 10/1/22 (0% Fixed Rate) and sold it on 7/1/25 for $5,694. These were the interest rates it earned over that 2 3/4 year time period (so just a little more than half of the 5 year holding period): 9.62%/6.48%/3.38%/3.94%/2.96%/1.90%.

I chose the timing of the sale intentionally to be 3 months into the 1.90% rate to minimize the 3 month penalty, which turned out to be $8, $10, and $8. To summarize, I lost $26 worth of interest as the penalty, but still earned $694 in interest, which, if my math is correct, averaged 4.68% (instead of 4.84% had I not had to forgo that penalty but still sold at that time).

I put that $5,000 to work in a 13-week T-Bill that is currently earning 4.351% (it matures later this month). I could’ve chosen any term I wanted and earned slightly more or slightly less of an interest rate, but that was the one I chose. As a result, I will earn $236 in interest over that 13 week period, $210 more than the penalty.

Now, it’s true that I have to pay federal income tax on the $694 because I cashed out the I Bond. I would argue that you have to pay tax regardless of when you sell the bond, so it’s not really part of the math, but let’s factor that in anyway. Assuming an effective tax rate of 20%, I have to pay $138.80 in federal tax on the $694 of interest. I’m still ahead by $97.18, or $71.18 if you factor in the $26 penalty.

I apologize if I made any math errors, but the moral of the story, and the point I’m trying to make, is that if you can sell an I Bond in less than five years when the variable inflation rate applied to the bond has decreased substantially, and there’s an equally safe alternative investment offering greater yield, it actually can be profitable and sensible to do so.

Sure, I have redeemed 0.0% and 0.1% I Bonds before 5 years, mostly to upgrade to higher fixed rates. Mostly I want to keep my level of inflation protection intact. I wouldn’t look at short-term T-bills as a replacement for an I Bond with a fixed rate of 1.10%, however.