By David Enna, Tipswatch.com

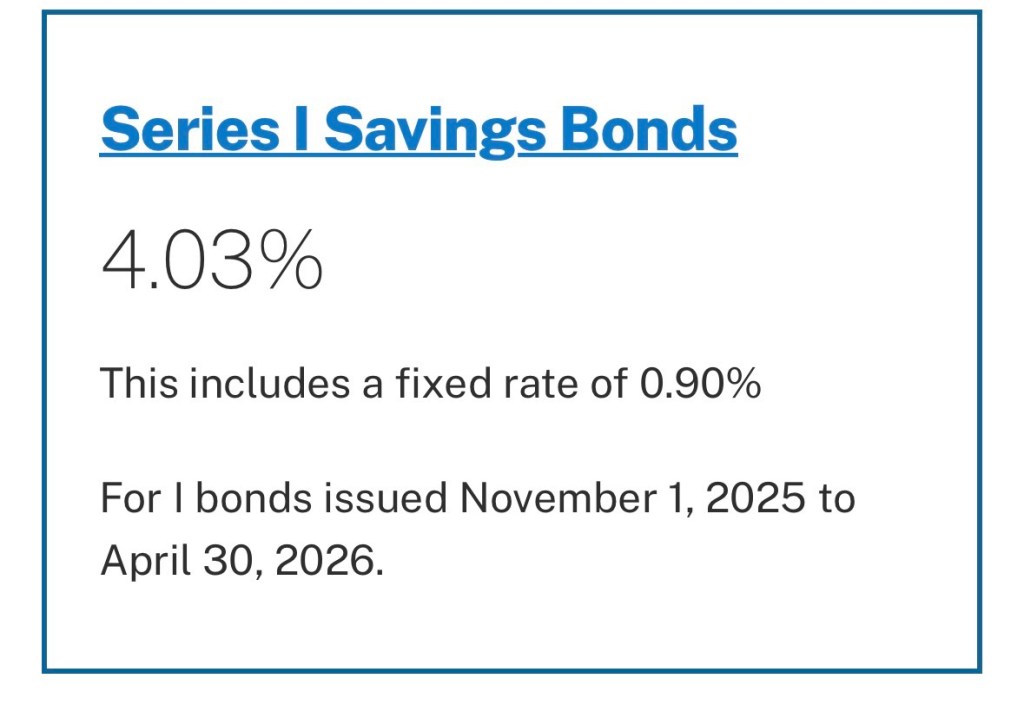

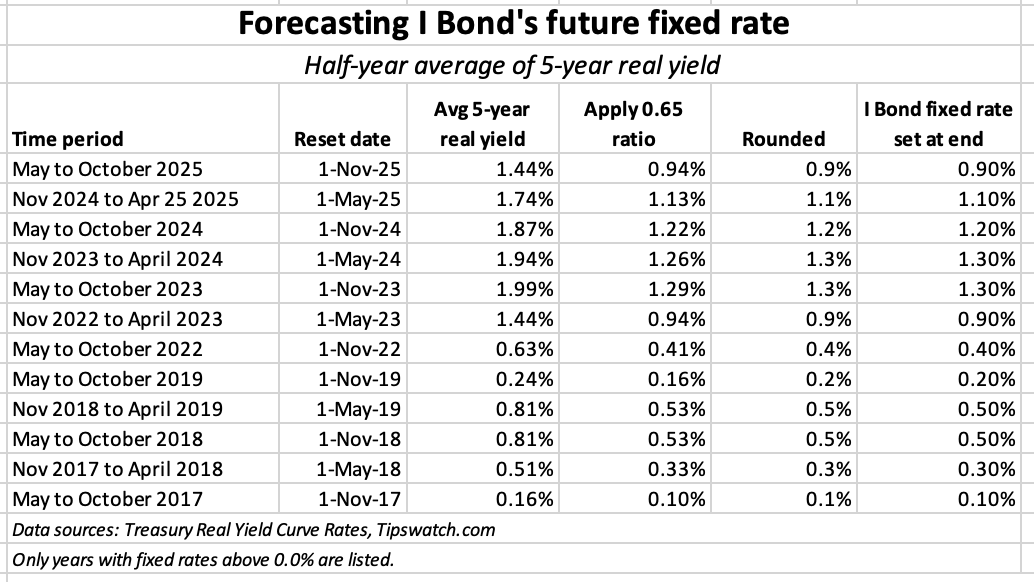

There were no surprises in this morning’s announcement of the new fixed and composite rates for U.S. Series I Bonds purchased from November 2025 to April 2026. Treasury followed its past practices, setting the fixed rate at 0.9%, as I projected.

This is a very good thing.

It is important because the Trump administration’s Treasury department continued to follow our “perceived” formula for the fixed rate: Applying a ratio of 0.65 to the average real yield of the 5-year TIPS over the last six months. This formula has worked, without fail, for 12 fixed-rate resets since November 2017.

Can we be sure this will continue to work? No, but it is reassuring to see past practices continued.

The fixed rate is permanent for the life of the I Bond, so it is a key factor in the attractiveness of this investment. While the fixed rate dropped from 1.10% to 0.90% at this reset, getting a guaranteed return of 0.90% above inflation will remain attractive for investors heading into 2026, as short-term Treasury yields continue to decline.

The composite rate

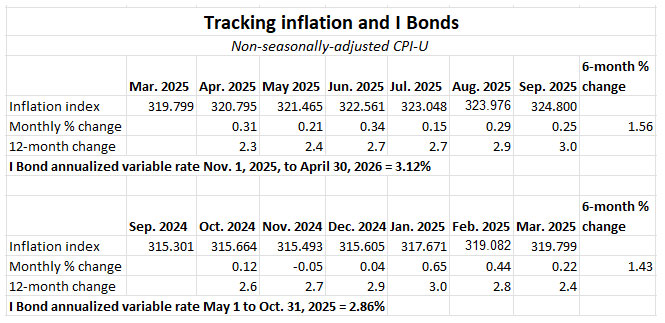

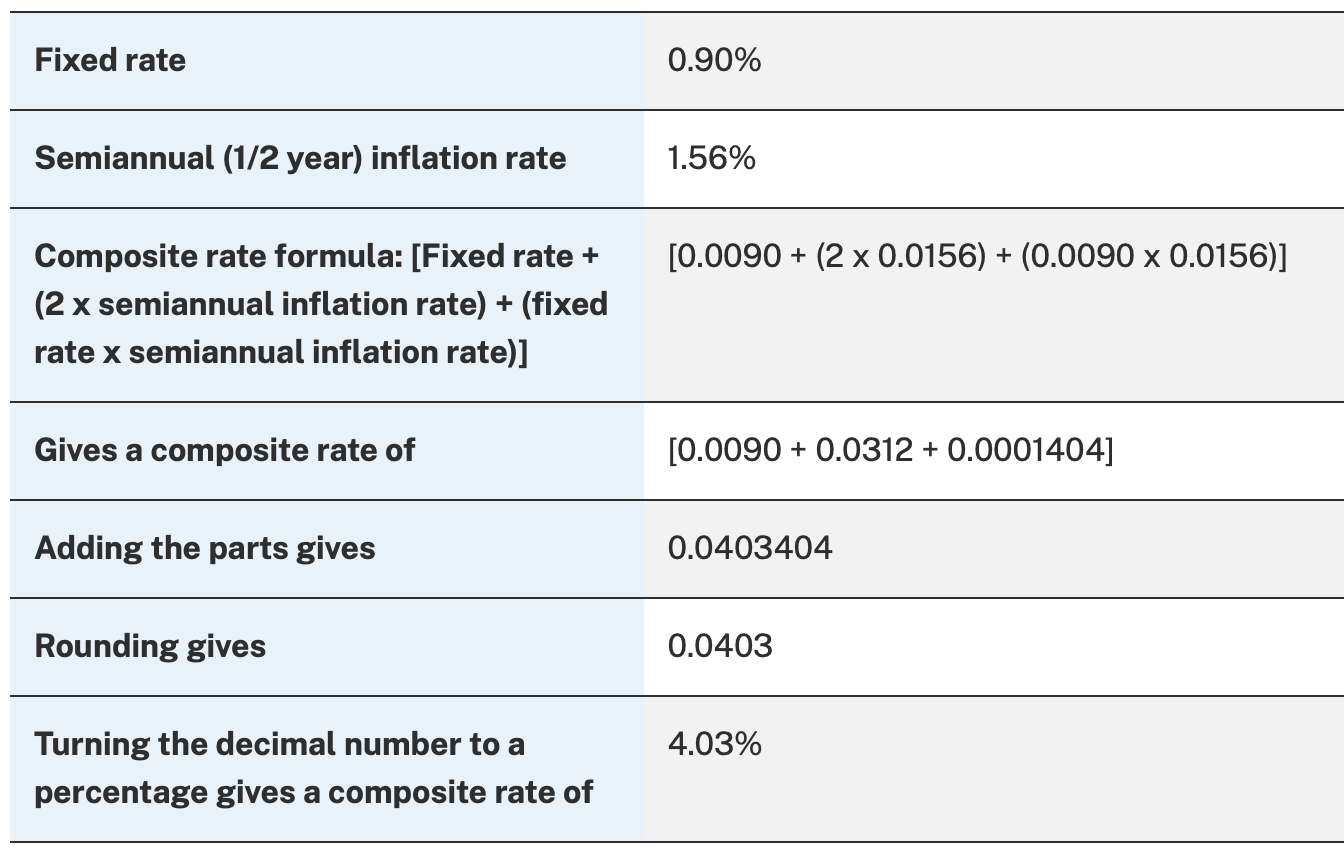

The I Bond’s composite rate is created by combining the fixed rate with an inflation-adjusted variable rate set by inflation over the last six months, in this case for the months of April through September. The current variable rate of 3.12% will apply to all I Bonds, no matter when they were issued.

Here is how the Treasury calculates the composite rate in a formula that combines the fixed rate and current variable rate.

This calculation is for I Bonds issued from November to April. For investors who purchased I Bonds earlier this year with a fixed rate of 1.10%, the new composite rate will be 4.23%. The new rates roll in for six months, depending on the month of the original purchase.

I Bonds remain attractive

New investors through April 2026 will be getting a six-month annualized return of 4.03%, which will be competitive with short-term Treasury bills, with yields that have already fallen below 4% and are likely to continue to decline as the Federal Reserve cuts short-term rates into 2026.

Of course, I Bonds must be held one year (technically about 11 months) before being redeemed, and any redemption before 5 years gets hit with a 3-month interest penalty. For I Bonds with an attractive fixed rate — and 0.90% is attractive — I suggest holding for five years and then redeeming when you need the cash.

Yes, your older I Bonds with fixed rates of 0.0% or 0.1% are less attractive. But even with these you will be earning above 3% over the six months.

I Bonds work well as a secondary emergency fund, constantly adjusting to inflation. There are no state income taxes, and the value of the investment can never decline with “market trends.”

EE Bonds

EE Savings Bonds purchased from November to April will have a fixed rate of interest of 2.5%, down from 2.7% for purchases in October. But Treasury continued is terms that double the value of EE Bonds if held for 20 years:

For EE bonds you buy now, we guarantee that the bond will double in value in 20 years, even if we have to add money at 20 years to make that happen.

At this point — unless short-term rates decline drastically — it is hard to argue that EE Bonds are an attractive investment. You can get about 4.64% on a 20-year Treasury bond.

Travel update

I am writing this from the Atlanta airport, about to get on a 14-hour flight to Seoul, South Korea. I will be “out of pocket” but feel free to discuss these developments in the comments section.

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Non-partisan thoughts on this? Implications?

White House says October jobs and inflation data may never be released because of the shutdown

https://www.cnbc.com/amp/2025/11/12/white-house-october-data-release.html

No actual data were collected, so any October CPI report would be suspect. The BLS will end up setting a “calculated” CPI rate, probably around 0.25% for the month.

It is very worrying, actually. The government decides through some mechanism who is required to work during a shutdown. Inflation data is critical to TIPS, I Bonds, social security and all sorts of tax items. Despite it being central to such items that impact everybody, the government decided not collecting inflation data isn’t important. Though later measures might “catch up,” they might not, or might provide an excuse (yeah, inflation was high in November but that was really October inflation and November was low, low, low). The path of economic statistics is very important. And all transactions in the absence of statistics are subject to greater uncertainty. Put yourself in the shoes of the Fed – how do you act in the absence of information? Do you act based on guesses and even less information than usual? Do you not act?

Jobs are a different matter as jobs numbers are very squishy. They are subject to large revisions due to delinquent reporting, and many companies simply don’t report. It does not bother me that they won’t be reported because they are not very reliable, nor have they ever been. With jobs you really have to look at a plethora of jobs statistics to have an idea of what is going on much more than you do with inflation. People think jobs statistics are hard, factual numbers, but many, if not most, are not.

Sadly, I suspect most people believe inflation numbers are soft, but jobs numbers are real, when the reverse is true.

Jobs numbers are real?

https://www.npr.org/2025/09/09/nx-s1-5527000/bls-us-job-growth-numbers-revised

Congrats on nailing the I Bond interest rate. (I’m thinking the Feds can save money by just reading your blog and acting accordingly)

One disagreement – K Pop Demon Hunters is great! You should take the opportunity to buy some swag in Seoul for the kids back home.

At this point — unless short-term rates decline drastically — it is hard to argue that EE Bonds are an attractive investment. You can get about 4.64% on a 20-year Treasury bond.

Is it really that attractive when a 20-year treasury bond returns the same basic yield?

He’s saying EE bonds are not an attractive investment because 20-year treasuries have a higher yield.

“Hard to argue” is a negative modifier. Also, 20-year STRIPS would be the best equivalent to an EE bond.

Like I bonds, EE bonds have the advantage of tax deferral. A 20-year strip would require payment of the imputed taxes. But as has been said before, they really only make sense if you can hold them for 20 years to get the doubling of value at that milestone. And that’s a long time to wait. Will I live that long?

Gotcha. Thanks for the clarification.

Pingback: New I-Bonds Rate Projection: 4.02% APY (Variable 3.13% + Fixed .9%) - Doctor Of Credit

At least the shutdown has not yet affected this. Let’s hope that our braindead, corporate lackey so called elected representatives can get the government running properly again.

Congratulations David on another spot on prediction.

David, your formula for predicting the next I Bond fixed rate has proven so accurate for so long that I sometimes wonder if you’re just tracking what Treasury has done, or if Treasury (which has never explained its own procedure) has begun to follow you. (“Hey, here’s this week’s new Enna column. He’s saying it’ll be 0.9%. What the heck, that sounds pretty good.”) 🙂

Wishing you safe and (in the best way) interesting travels.

+1! I remember when I started buying I-bonds, how hard it was to plan on when to buy. Now I just follow tipswatch …

I agree! Two or 3 years ago this was all new to me and David’s detailed and clear blogs along with this discussion forum helped me learn enough to feel comfortable deciding how I want to invest in TIPS and I Bonds. Very informative and appreciated!

I think it’s actually a little more tricky to know when to redeem them to minimize the 3 month penalty (if holding less than five years) and David has addressed that issue as well.