For me, definitely. But it’s a personal decision.

By David Enna, Tipswatch.com

Something unique is coming this week: The first-ever Treasury Inflation-Protected Security to mature in the year 2036. For that reason, and the fact that real yields remain attractive, I will be a buyer.

This is CUSIP 91282CPU9, a new 10-year TIPS that will auction Thursday. The coupon rate and real yield to maturity will be determined by the auction results. I have targeted this TIPS for a long time as the 2036 addition to my ladder of TIPS investments that stretches to 2043.

No TIPS were ever issued with maturities in years 2036 to 2039 for two reasons: 1) the Treasury stopped issuing 20-year TIPS in November 2009 and 2) the 30-year TIPS auctions were halted from October 2001 to February 2010. That left investors with gap years.

As a compulsive ladder builder, I want to fill those 2036 to 2039 years and I have set up my traditional IRA to allow purchases in January 2026 to 2029 — as long as real yields remain attractive.

This January auction size, by the way, is $21 billion, up from $20 billion for a matching auction in January 2025, but holding steady with the size of the new TIPS issued in July 2025. This marks a break in the Treasury’s recent practice of raising the size of its January TIPS auction.

Real yields

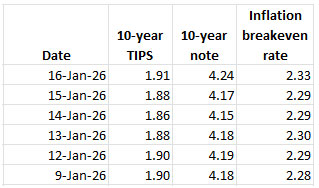

At this point, the 10-year real yield is about 1.91%, according to the Treasury’s yield curve estimates. However, the most recent 10-year TIPS trading on the secondary market closed Friday at 1.88%, so we have a bit of fuzziness.

The Treasury market was shaken last week with news that the Justice Department served Federal Reserve Chairman Jerome Powell with subpoenas in an apparent criminal probe. Powell responded with a strong statement criticizing the action as threatening Fed independence.

My initial reaction was that this kind of controversy should cause inflation expectations to rise, since an independent Fed has a key role in controlling inflation. While it might not seem logical, when inflation expectations rise, the real yield of a TIPS is likely to fall, at least compared to a nominal Treasury of the same term.

And that is what happened in the last week:

The Treasury’s estimate of the real yield of a 10-year TIPS rose only 1 basis point over the last week, while the nominal yield of a 10-year Treasury note rose 6 basis points. This isn’t a huge deal, but does indicate that real yields could continue shifting this week. (The bond market will be closed Monday for Martin Luther King Jr. Day.)

So far, I’d say the market isn’t pricing in a threat to Fed independence. But investors interested in this auction should watch real yield trends through the week.

Definition: The “real yield to maturity” of a TIPS is its yield above official future U.S. inflation, over the term of the TIPS. So a real yield of 1.91% means an investment in this TIPS would provide a return that exceeds U.S. inflation by 1.91% for 10 years.

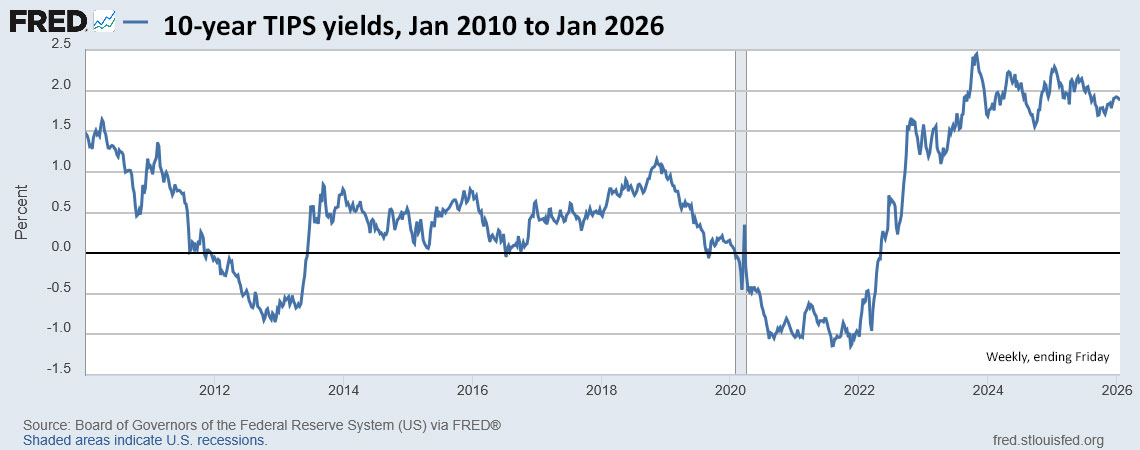

Is an above-inflation yield around 1.90% attractive? Yes, historically. Of course, we can’t predict where real yields will be heading into the future. They could be much higher if U.S. deficits continue to soar and the world loses trust in the U.S. dollar. Here is the trend in the 10-year real yield over the last 16 years:

Update: In the wake of turmoil over Greenland and the threat of additional tariffs on European trading partners, the Treasury’s estimate of the 10-year real yield surged to 1.97% at Tuesday’s close. See this.

Update No. 2: After the U.S. reached a potential deal over Greenland late Wednesday, real yields fell sharply. The Treasury is showing 1.92% as the prediction, but the secondary market closed at 1.86%. Just another “normal” day.

Pricing

Since this is a new TIPS, its coupon rate will be set to the one-eighths mark below the auctioned real yield. (For example, a real yield of 1.90% would result in a coupon rate of 1.875%.)

For that reason, the unadjusted auction price will be slightly below par value and investors will get the TIPS at a discount. Plus, this TIPS will carry an inflation index of 0.99779 on the settlement date of January 30. That guarantees the investor will get a discounted price, but also get less than par value of principal as of January 30.

For example, a $10,000 par value investment will be priced slightly below $10,000, but the investor will be getting only $9,977.90 of principal on the settlement date. My reaction: No big deal, but no one should be surprised.

If you find all this confusing, read this: Q&A on TIPS

Inflation breakeven rate

As I noted above, the Treasury’s estimate of the nominal yield of a 10-year Treasury note closed Friday at 4.24%. If you assume this new TIPS will get a real yield of 1.91%, its inflation-breakeven rate would be 2.33%, as things stand today. That is more or less in line with recent auctions.

Historically, an inflation-breakeven rate of 2.33% is high, and it indicates that the nominal Treasury at 4.24% may also be a fair investment. I favor the TIPS because it provides protection against future unexpected inflation. Also, consider that inflation over the last 10 years has averaged 3.2%, through December 2025.

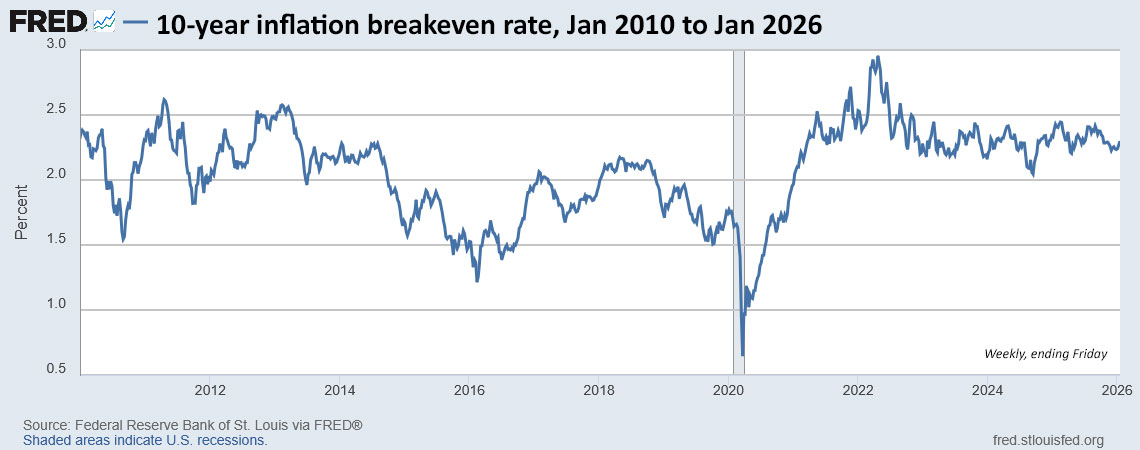

Here is the trend in the 10-year inflation-breakeven rate over the last 16 years, showing remarkable stability since late 2021 in the 2.2% to 2.4% range:

Auction thoughts

It’s impossible to predict demand for inflation-protected investments at a time when inflation reporting is being questioned and the independence of the Federal Reserve may be at risk. My view is that TIPS should get a bit of a “risk premium,” meaning slightly higher real yields. So far, that’s not happening.

I will be investing in this new TIPS unless real yields fall off in the next week. I could purchase CUSIP 91282CPU9 later in the year, easily, and possibly get a better yield at some point. Again, no big deal for my overall investment strategy. A real yield of around 1.90%, or even a little less, will be fine.

If you want to track this potential investment, you can use the Treasury’s Yield Curve estimates, which are posted at the market close each day. This is an estimate of the yield of a full-term TIPS at par value. The estimate will be close, but not perfect, and things can change on the day of the auction.

You can also monitor Bloomberg’s Treasury Yields page to see real-time updates of secondary market trading in the most recent 10-year TIPS. Consider this a rough guide; the auction result often varies.

This TIPS auction closes Thursday at 1 p.m. EST. Non-competitive bids at TreasuryDirect must be placed by noon Thursday. If you are putting an order in through a brokerage, make sure to place your order Wednesday or very early Thursday, because brokers cut off auction orders before the noon deadline.

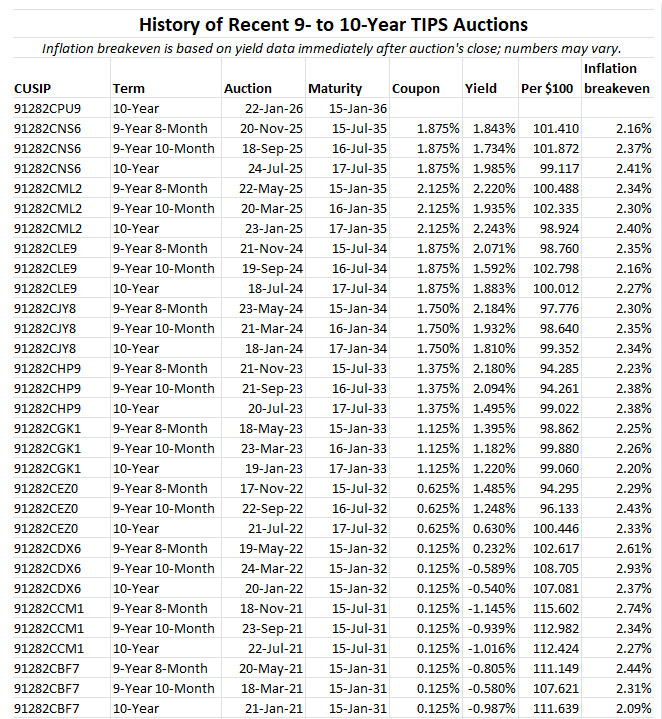

I will be posting the auction results soon after the close on Thursday. Here is a history of auction results for this term over the last 5 years:

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Note: Comments on this article have been turned off because the direction has turned entirely political.

If you did any amount of retrospective research you would find consensus that the monetary and fiscal policy at the time contributed significantly to the “demand surge” and “supply chain issues” that you attribute as the cause of inflation. Even if I accept your premise that the “pandemic reopening” was the sole cause, one must them examine the cause and necessity for the “closing”

The point of my post however is there was research at the time that indicated as such, but in addition to that not being addressed in any blog article, any suggestion that current (at the time) monetary or fiscal policy was contributing to (or caused) inflation was immediately shut down as “political”

That post should have been a child or a different post — not sure why it is standing alone

I’m curious. Is there an advantage to buying the 10 Year Tips in January at the initial auction versus waiting and buying when the reissue occurs in March? Seems like waiting would allow for more data to base the buying decision on. I’m very new to TIPS but I do need to fill out my 2036-2039 rungs as I’m otherwise covered through 2045 currently.

There is no advantage in buying in January versus March. Real yields could move either way.

Like most (but certainly not all) Americans, I am appalled that my government is shattering international norms and democratic institutions as if there are no repercussions. Then I read this article, which opened my eyes to the potential for political and economic destabilization that could be caused by EU retaliation against the ridiculous, unnecessary, and aggressive bellicosity of this administration against Greenland. In addition to shattering the NATO alliance that has maintained at least some world order since its inception, an invasion of Greenland (which my rational side still views as unkikey) or an escalating trade war (which I views as a near certainty) could cause the EU to start selling its massive holdings of U.S. treasuries. I realize this is unprecedented, but could you address whether such actions could trigger a stock market crash and a period of hyperinflation? What would this do to the bond market and how would it impact holdings in TIPS, treasuries, and I Bonds?

Europe can wield this $8 trillion ‘sell America’ weapon as Trump reignites a trade war over his Greenland conquest ambitions

https://finance.yahoo.com/news/europe-wield-8-trillion-sell-174459640.html

My view is that there is always “risk” in the US financial system and not addressing that risk well, or jumping in blindly, has led to the Great Depression, high inflation of 1970’s through 1980’s, Dot.com Bust and the Great Recession. Fortunately the last two were short and equities in U.S., Europe and Asia did relatively well during the high inflation era. A diversified portfolio, with dollar cost averaging did well through those storms.

In retirement, I reinvest interest and dividends and use rebalancing plus maturing income investments to set aside the money I need to live on. This is an attempt to imitate the dollar cost averaging when I was working. It has again helped smooth out the volatile market with 3-5% (annualized) being reinvested monthly in a diversified portfolio. Mine now includes TIPS because my greatest risk is inflation or stagflation (as I do believe cutting Social Security benefits will lead to a Gray Revolution).

I do not believe, and there is little evidence, for lay people and even most professionals picking investments and outperforming the market long-term unless you have relatively deep pockets like Berkshire Hathaway and the like who can be very patient (i.e., have very long term horizons) can follow the vice versa of Warren Buffet’s advice and “Be greedy when others are fearful.”

The Treasury webpage you provided has the following absurd message at the top. We’ve become a banana republic.

Since when has the abnormal become the normal? No one dare file a compliant with CFPB? For example, how/why can any credit reporting agency state whether a particular credit “pull” is hard/soft whereby it may impact your credit score (which is issued by an unrelated entity)?

Yes, this is embarrassing (and unnecessary) for a supposedly non-partisan department like the Treasury. I appreciate that the Bureau of Labor Statistics has not posted any similar message.

While the Biden administration was unconstitutionally trying to buy young voters with student loan forgiveness, the Dept of Education used to spam borrowers with emails about how great the Biden/Harris administration was (saving the world from student debt) and how terribly wrong Republicans and the Supreme Court were trying to stop them. They also put banners on the DoE web page. Was it embarrassing then?

One of the differences between now and then is your did not allow political comments on your posts. Now your posts are filled with them and the political comments follow.

I don’t like using US tax dollars for political gain. Either party.

Can you point to just one article during any period of Democrat control that was critical of such actions? Or one comment that might have suggested as such that you didn’t shutdown for being “political”?

I recognize this is your blog and you can write how you wish, but your blog is not politically objective –not now, not before.

I’ll be buying to fill in an important gap in my ladder as I plan to start QCDs in 10 years if my portfolio return and budget permit.

I too, planned to buy this coming Thursday barring a crash in the Real Yield. However, I must admit, the deterioration in the rule of law starting with our capricious Dear Leader and those he has empowered to enforce his whims (without any check by Congress or the Courts) has me seriously questioning “the full Faith and Credit of the United States Government” for the future. When our government has been seemingly co-opted by a “personality”, especially one as erratic and unstable as Trump, the writing may be on the wall. All of our European allies are now questioning their trust in America, South Americans have been duly warned by his aggressive behavior and the SEATO nations have to be looking askance at as well. I think Gold, silver and precious metals may be the canary in the coal mine announcing the world’s distrust of the US dollar (and fiat currency in general) and US debt loads. Can we trust economic data that comes of a government where everyone employed owes fealty to Trump? He reminds me so much of Juan Peron, and we know how well that turned out.

So, I’m vacillating a bit, between wanting to fill in a gap in my RMD bond ladder and a genuine concern that the payout I’m expecting will actually be made 10 years down the road.

What do you think about buying a 2046 TIPS on the open market instead of 10 year at the current auction? The 2046 TIPS currently has a real yield of about 2.5%. My intention is somewhat speculative, so I would have to sell it on the open market in about 10 years…or opportunistically sell before then during a period when real rates drop and prices rise. My understanding is that people avoid TIPS with maturities longer than 10 years because they are generally not as liquid as shorter maturity ones. However, in 10 years, the 2046 TIPS should be just as liquid as a10 year TIPS sold in 2036.

My other reservation is about the selling price on small lots of TIPS. Since I am an individual investor laddering my TIPS, my individual purchases tend to be in the $10-20K range. Should I expect to have to sell at a discount if I sell before maturity?

My recommendation is always to invest a TIPS with the intention of holding to maturity. That Feb 2046 TIPS currently has a real yield to maturity of 2.5%+, which is attractive. You will get it at a nice discount (76.13) because the coupon rate is only 1.0%, but you will also be buying 37% additional principal because of inflation since 2016. Overall, it would cost you over par value but with a lot of additional principal. It’s going to be pretty volatile over the next 10 years. I have never sold a TIPS so I can’t give you any idea on the liquidity or price spread.

While I am a buy and hold TIPS/income, I have bought in the after market on Fidelity platform and the bid/ask has been reasonable. Sometimes a little challenging in volatile markets. You may find bid/ask on your platform to see.

I have some that mature when I’m in my early 90s and may liquidate early if necessary (or some executor may) and the haircut seemed to me worth the real yield. And, I’m indifferent to the volatility.

I already invested in 91282CJY8 since a CUSIP wasn’t available for 2036. Can you walk us through the decision making process of whether to keep 91282CJY8 or sell the 2036 portion and invest the proceeds in 91282CPU9? Thanks.

91282CJY8 matures in Jan 2034, so I assume you were stacking TIPS to cover the missing years. My personal opinion: Just hang on to it. But if you did sell, you’d be getting a price just under 100, so no problem there. It could work out. These are going to end up being very similar investments.

I am in the same boat. Presumably the new TIPS will have a bit higher, real YTM and a similar interest rate, possibly a tick higher. So you get extend the maturity a bit and get a bit of a kicker.

I have also contemplated selling the 2036 portion now, and waiting to reinvest at the reopening.

One thing I will not do is buy the new TIPS without selling the excess in my 2034 TIPS. I am not considering increasing my exposure.

Future inflation expectations do not include the diverse and growing economic impacts of Climate Change. Higher property insurance rates are “top of line “ with agricultural impacts next. Both tropical products and domestic agriculture. Then odd changes like the restriction on the Panama Canal.

Climate induced inflation tips the balance (pun intended) towards investing in TIPS.

The inflation expectations also do not seem to include the possibility of significant deflation caused by automation and artificial intelligence. I don’t think that is a significant risk in the short term, but going out 15-30 years? It is within the realm of possibility.

I don’t recall a period in world history where significant, broad deflation was caused by automation (i.e., increased labor productivity). There is certainly short and long-term disruption. The best examples I can think of are the dramatically reduced relative cost of food, water, fuel and light as a share of income, but no net deflation. In U.S. history, the only relatively long-term deflation was during the Depression.

My concern with A.I., like many technologies, is that they tend to advantage the adaptable, often educated whether self or otherwise, in terms of both productivity and income. A.I., however may be different as factory-floor automation displaced “laborers” while A.I. displaces entry-level accountants, software developers, management consultants, call centers, …

I think I‘ll advise my grandchildren to become plumbers, electricians or HVAC technicians/installers. Even in bad economic times folks need these things to work.

I have 4 open ladders from 2037-2040. I may also be a buyer. That will complete my TIP ladder until I am 84. It starts at my RMD age 72. I was hoping for a breakeven of over 2% so we will see. Thanks for reminding and sharing. This site is my ‘go to for honest information” on inflation, tips and bonds in general. I have learned so much.

What are the theories to why the market has tuned out inflationary policies and acts that would normally undermine faith in the US financial system? My current uninformed guess is that it is a form of TINA. Gold and similar are already very expensive, traditional investors (and myself) are skeptical of cypto, and overseas systems make be even more vulnerable to the fallout of US systems issues. US equities are also quite expensive by the usual measures.

Each day seems to bring new threats to trust in the U.S. financial system. Or am I over-reacting? The stock market continuing its climb indicates investors are optimistic, or very complacent. I agree on gold and crypto speculation; that’s not my style. That leaves the U.S. and international equity markets, combined with safe-as-possible fixed income.

I think we’ll only know if we’re overreacting in hindsight.

I know that’s not very helpful right now.

Per Warren Buffett, as I recall: ”Be fearful when others are greedy…”

Threats to trust in any system come from many places. One of the places is journalists who selectively repeat every rumor and innuendo during some periods, and ignore or rationalize during others. The Biden administration and the Democratic congress were responsible for almost double digit inflation in 2021/2022 — but there were no critical articles of their actions or policies and any comment that suggested as much was shutdown and censored for being political.

No, Biden and the Democratic Congress were not responsible for inflation. If that were true, you wouldn’t have seen inflarion soar anywhere else in the world, and yet it did everywhere Your take is a partisan narrative that completely ignores the pandemic reopening ,demand surge, and supply chain issues which you did not mention that actually caused world-wide inflarion. Correlation does not mean causation.

I am a journalist, and I can’t speak for “all” journalists. When I started Tipswatch in 2011 Ben Bernancke was Fed chair, then Janet Yellen and now Jerome Powell. My consistent focus has been 1) safety-first investments in U.S. Treasurys, 2) lower federal deficits, and 3) keeping inflation under control. I was not a fan of quantitative easing, which began to ramp up in 2011 and set the stage for higher inflation. I was not a fan of stimulus checks sent out by both Trump and Biden, which certainly contributed. And I wasn’t a fan of Biden’s Inflation Reduction Act, which was in fact, inflationary.

I stand for lower inflation, lower federal deficits and Federal Reserve independence. I support keeping interest rates at a level above inflation, because I am a saver and want protection from inflation. This site isn’t supposed to be about politics, at all, and until we started getting a “two crises a week” I was a lot happier.

@marce607c0220f7 If you did any amount of retrospective research you would find consensus that the monetary and fiscal policy at the time contributed significantly to the “demand surge” and “supply chain issues” that you attribute as the cause of inflation. Even if I accept your premise that the “pandemic reopening” was the sole cause, one must them examine the cause and necessity for the “closing”

The point of my post however is there was research at the time that indicated as such, but in addition to that not being addressed in any blog article, any suggestion that current (at the time) monetary or fiscal policy was contributing to (or caused) inflation was immediately shut down as “political”

Platinum is possibly undervalued. It is around $2,350 per ounce yet it is said to be scarcer than gold which is at $4,600. But at the end of the day it comes down to what willing buyers will pay for something.

Platinum is up from around $1,000 9 months ago where it hovered for years.

My simple theory is that people lack imagination. They believe it can’t happen here, it can’t happen because it would be catastrophic, it won’t happen because saner heads will step and and prevent it…all the while watching it happening.

Another theory is people simply do not understand how things work. Run the govt like a business, the post office is losing money so we should sell it, employment data should be spot on because it comes from paycheck data, etc.

There is certainly some TINA – what are you going to do if you believe the US financial system is at risk?