After-auction update: 10-year TIPS reopening gets real yield of 1.896%

By David Enna, Tipswatch.com

The U.S. financial markets have had an interesting two weeks, to say the least. An active war in the Mideast has sent oil prices soaring, the stock market tumbling, and the U.S. bond market into turmoil.

U.S. inflation is very likely to rise in the short term, and possibly for the longer term. Billions of new borrowed money is flowing into attacks on Iran, causing longer-term Treasury yields to rise. Then, add in the cost of billions of upcoming tariff refunds to corporations. At the same time, the U.S. economy appears to be slowing and the Fed’s favorite inflation measure — core PCE — has risen to a too-high 3.1% as of January. The markets have a new fear: “stagflation.”

That’s the backdrop for Thursday’s Treasury auction of $19 billion in a reopened 10-year TIPS — CUSIP 91282CPU9 — creating a 9-year, 10-month TIPS. This TIPS had its originating auction Jan. 22, 2026, which generated a real yield to maturity of 1.940% and set its coupon rate at 1.875%.

For a while, that January auction looked like a big win for investors, as the 10-year real yield dipped to as low as 1.72% on February 27, one day before the U.S./Israel attack on Iran. Now two weeks later, CUSIP 91282CPU9 is trading on the secondary market with a real yield of 1.90%.

Definition: The “real yield to maturity” of a TIPS is its yield above future U.S. inflation, over the term of the TIPS. So a real yield of 1.90% means an investment in this TIPS would provide a return that exceeds official U.S. inflation by 1.90% for 9 years, 10 months.

In times of international strife, you would expect to see a “flight to safety” causing investors to pour into U.S. Treasurys. In addition, we could expect TIPS to be in higher demand because of the fear of future inflation. So far, that is not happening.

You can track CUSIP 91282CPU9’s real yield and price on Bloomberg’s Current Yields page, which updates in real time when the bond market is open. It closed Friday with a real yield of 1.90% and a price of 99.82. I would expect to see a lot of volatility leading up to Thursday’s auction.

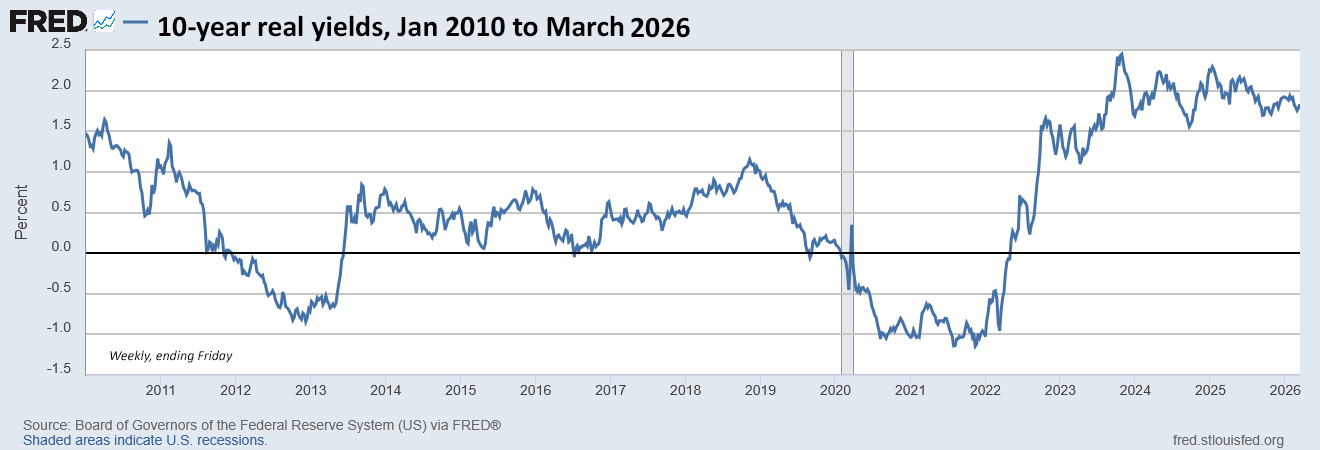

Here is the trend in the 10-year real yield over the last 16 years:

I start this chart in 2010 for a reason: It is a year before the Federal Reserve began aggressive quantitative easing in mid 2011 and then again in 2020 in the aftermath of the COVID shock. Today’s 10-year real yield of about 1.92% (the current Treasury estimate for a full-term TIPS) is attractive from this longer-view perspective. But investors should be aware that real yields could certainly rise from this point.

Pricing

If we assume the auction’s real yield will be 1.90% (things will change by Thursday) this TIPS is likely to auction at or near par value, since that yield is a bit above the coupon rate of 1.875%. The Bloomberg yields page shows a Friday closing price of 99.82. Plus, this TIPS will carry a minimal inflation index of 1.00086 on the settlement date of March 31. Let’s look at how that works out for a $10,000 par value investment:

- Par value: $10,000.

- Principal purchased on settlement date: $10,000 x 1.00086 = $10,008.60

- Cost of investment: $10,008.60 x 0.9982 = $9,990.58

- + accrued interest of about $33.88.

Things will change by the auction, but this one is likely to cost near par value. The accrued interest will be returned at the first coupon payment on July 15.

Inflation breakeven rate

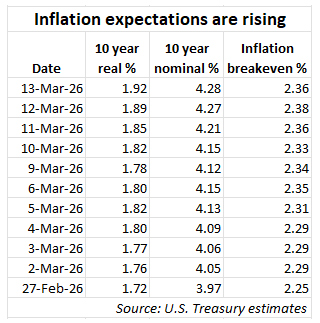

I have been assuming that inflation expectations would rise because of the current oil shock, but possibly not so much for 10 years out. This chart shows the 10-year inflation breakeven rate has increased 11 basis points since the outbreak of war.

An inflation breakeven rate of 2.36% is high by historical standards, meaning that the TIPS is getting expensive versus a nominal 10-year Treasury note. However, it seems in line with current conditions. Inflation has averaged 3.3% over the last 10 years, ending in February.

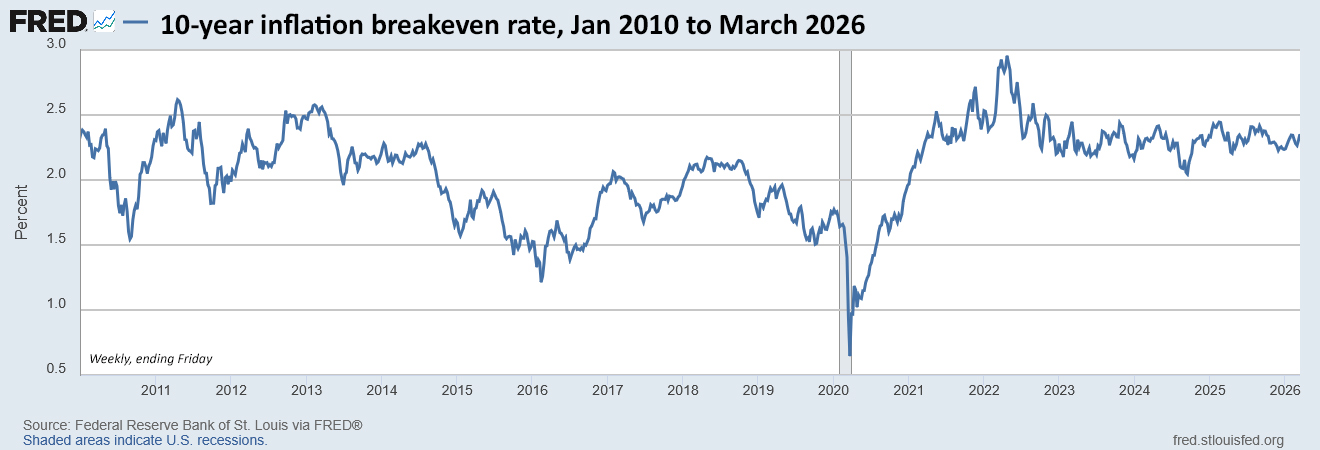

Here is the trend in the 10-year inflation breakeven rate over the last 16 years, showing the relative stability of expectations since fall of 2022:

Thoughts

I was a buyer of this TIPS in January, purchasing my entire 2036 allocation at that auction. So I won’t be a buyer this week. For investors, a real yield hanging in the 1.90% range looks attractive, in my opinion. But this week will be volatile, and any investor would be wise to watch the Current Yields page for updates.

This TIPS can be purchased at any time on the secondary market, which gives investors the option to target a desired yield.

The advantage of buying at auction, especially through TreasuryDirect, is that even small-lot purchases will get the auction’s high yield. The advantage of the secondary market is that you can see exactly the price and real yield you will be receiving. The negative is that you may face a small bid-ask spread. Most of the time, it doesn’t make a huge difference, but if you see a real yield you like, know that you can probably get it on the secondary market without dealing with the auction’s uncertainty.

This TIPS auction closes Thursday at 1 p.m. ET. Non-competitive bids at TreasuryDirect must be placed by noon Thursday. If you are putting an order in through a brokerage, make sure to place your order Wednesday or very early Thursday, because brokers cut off auction orders before the noon deadline.

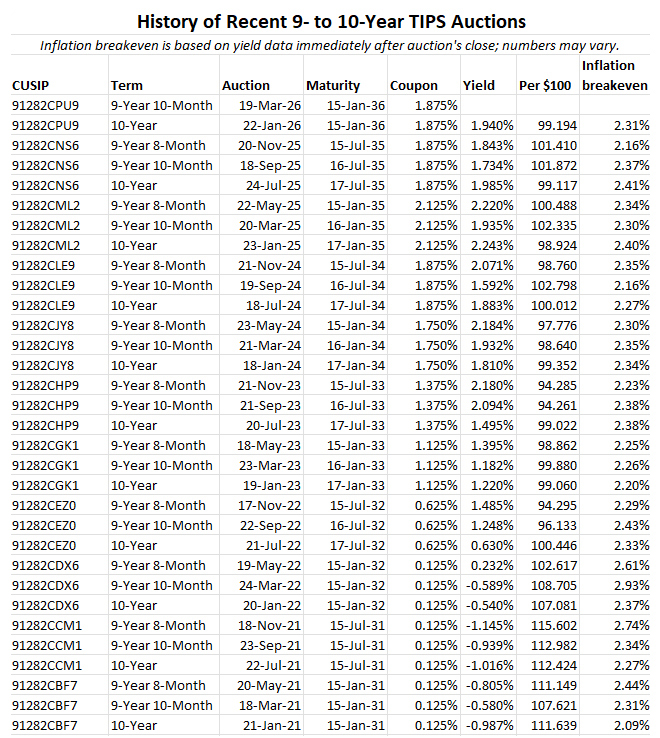

I will be posting the auction results soon after the close on Thursday. Here is a history of auction results for this term over the last 5 years:

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

One commenter mentioned that the social security tax system is not progressive, which is technically correct but very misleading, as the benefit is progressive. Basically, the benefit is calculated as a % of one’s highest 35 years of income, adjusted for inflation, with the % declining as average income increases. The steps for 2026 are:

90% of the first $1,286 of monthly income.

32% of the block between $1,286 and $7,749,

15% of the amount over $7,749.

So it is, in effect, a progressive system.

And the low “payback” from higher earnings is why increasing or removing the social security cap is so effective.

https://www.ssa.gov/oact/COLA/piaformula.html

To my old self, it appears like Uncle Sam is going to be needing to sell a whole lot more of bonds to cover costs of never-ending wars, tariff refunds and all compounded by low rates of tax collection on revenue of all the money makers (profiteers?).

On that Bloomberg ‘Current Yields’ page: Are the GOV yields shown just a ‘copy-paste’ of the Treasury’s website (for auctions), or are they estimating those by looking at the 2ndary market?

Thx

Larry

That Bloomberg page reflects real-time trading for the most recent issue for each maturity.

To avoid the tax filing hassle, I’m thinking about buying the IBIL ISHARES IBONDS OCTOBER 2035 TIPS ETF instead of the TIPS. Will it get the same real return, minus the expense ratio? https://www.ishares.com/us/products/342148/ishares-ibonds-oct-2035-term-tips-etf

This would be in a taxable account? Might be a good option. I wrote about IBIL back in March 2025, which means a 2036 version (JBIL) should be launching very soon (and I will probably write about that one, too). These funds are designed to be held to maturity and the asset value will rise and fall with market trends through maturity, just like any other bond fund. Expense ratio is fine at 0.10%. The inflation accruals are paid out in the current year, which solves the phantom tax problem but means the accruals don’t compound. https://tipswatch.com/2025/03/30/ishares-unveils-new-etf-holding-exactly-one-tips-for-now/

IBIL currently holds only two 10-year TIPS. In 2030 that fund will purchase new 5-year TIPS issues (assuming current issuing scheme holds) at whatever yield market dictates at that time. These new 5-year TIPS will likely be roughly half of the total fund holdings, possibly more. So no, the return of the fund diluted with these new TIPS issues will definitely not be the same as what you would get if you bought 2035 TIPS today and held them to maturity.

Nothing that I consume every stopped at the official inflation rate. Upper middle class budget. I did have an eye opener the other day, reminded me I did not really make it. I had lunch at a regional airport and was a steady stream of families schaufered up boarding small personal jet taxis. Uber for the 1%er nextdoor. Food was good. I got a few Ibonds only. This might be the end of the petro dollar so I expect banana republic rates.

In response, I point you to this New York Times article (gift link): https://www.nytimes.com/2026/03/15/business/billionaire-income-tax-loopholes.html?unlocked_article_code=1.TVA.0V_U.IKxkvnTd46Qy&smid=url-share

Payroll taxes are capped because benefits are capped. It was not set up as a progressive tax system and policy makers have been trying to avoid that from happening. Dividends and Capital Gains are taxed differently because they are, and in theory were once taxed as wages, so taxing again as wages would be pure double taxation. Estate taxes are unpopular even with liberals, many of whom have substantial estates.

I think everyone tends to forget that the estate tax exemption would be lower now had Trump not been elected.

The payroll tax system used to apply to a large percentage of U.S. wages, 90% in 1983. Wages above the cap have grown dramatically faster than what the rest of us earn. In 2021, the amount had dropped to 81% (and this is only wages, not capital gains, dividends, etc.). The Congressional Budget Office has estimated that the cap would have to rise to $305,000 to restore the 90% ratio. (Those people are still upper middle class, I know.) But we do need a solution.

I suspect comments are from a bean counter. No logic there, only numbers.

Yes, somebody better start counting beans. Social Security is in trouble

Depends on how old you are. Nobody makes a billion dollars nest egg on tax savings, but you can keep it on tax savings and inheritance laws to fund future arm chair billionaires.Im a boomer its someone elses problem. Wonder what Elons estates plan is looks like? Retired in Fl, 6person golf carts in breeder neighborhood,I see $$$.

I know that the software of the Tipswatch website only allows a certain “depth” of replies, so I’m using the only still-active “Reply” link available in this sequence involving the financing of Social Security, which means that my post will appear out-of-sequence with others on that subject.

Such discussions are always a good time to bring up a report of the Senate Committee on Aging (Senate Report 111-187, now almost 16 years old), which explored various ways to address the solvency and benefits structure of the Social Security program.

And, among the many options, the report projected that eliminating the cap on earnings subject to the payroll tax which currently finances Social Security would, by itself, in the absence of any other changes in the program, eliminate Social Security’s deficit for the following 75 years.

See p. 46 of the PDF version here:

https://www.congress.gov/committee-report/111th-congress/senate-report/187/1?outputFormat=pdf

Another way, of course, would be to apply the Social Security tax to all “income,” regardless of source, instead of just wages and salaries.

The 2010 Congressional report also included raising the tax by 1.1 points from 6.2% to 7.3%. Maybe a lower increase combined with an increase to the cap on earnings and a lesser increase in the benefit maximum would gain some traction? I think you would at a minimum need Democratic control in Congress and Presidency.