Investor demand might have been a bit weak.

By David Enna, Tipswatch.com

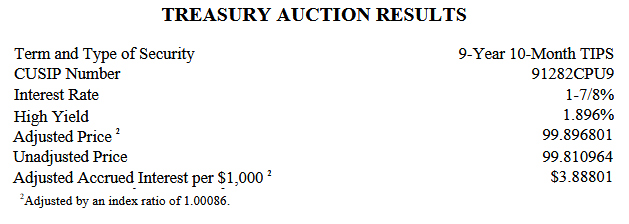

The Treasury’s offering of $19 billion in a reopened 10-year TIPS – CUSIP 91282CPU9 – generated a real yield to maturity of 1.896%, a bit higher than the market was expecting.

The reopening auction created a 9-year, 10-month TIPS. The coupon rate of 1.875% was set by the originating auction on Jan. 22, 2026.

This TIPS trades on the secondary market, and through the morning its real yield was inching higher, from about 1.85% around 8 a.m. to 1.88% right before the auction’s close. The “when-issued” yield prediction used by bond traders was 1.88%, so the resulting yield of 1.896% indicates relatively weak demand. The bid-to-cover ratio, however, was strong at 2.47, the highest for the last six auctions of this term.

Definition: The “real yield to maturity” of a TIPS is its yield above future U.S. inflation, over the term of the TIPS. So a real yield of 1.896% means an investment in this TIPS would provide a return that exceeds official U.S. inflation by 1.896% for 9 years, 10 months.

It’s been a volatile week for Treasury issues in a market roiled by potential price shocks from a war in the Mideast, and then contradictory messaging by Federal Reserve Chairman Jerome Powell on Wednesday. So overall, this auction result looks pretty solid.

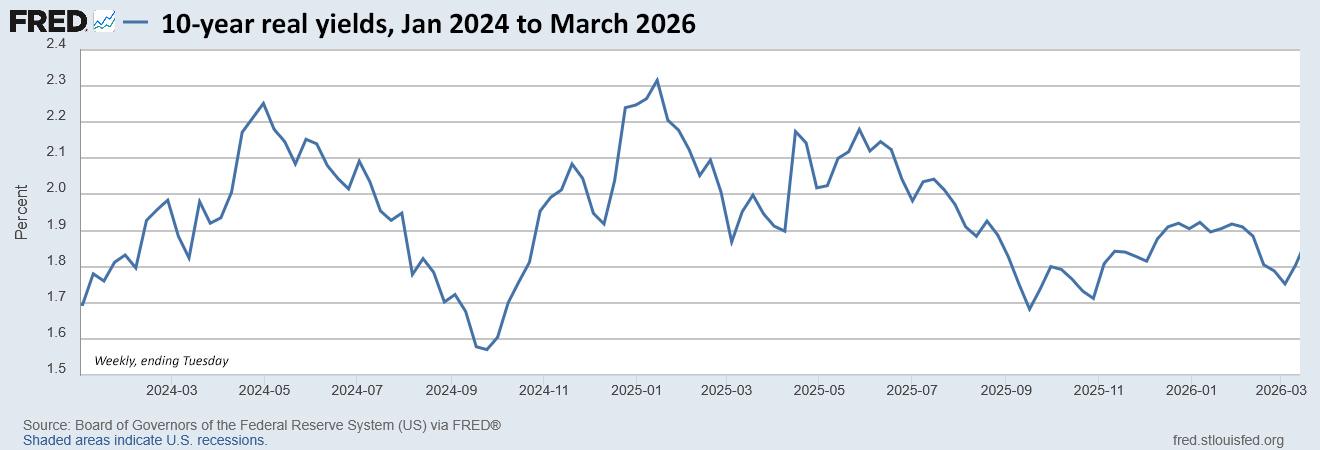

Here is the trend in the 10-year real yield over the last two years, with this auction’s yield falling just below the mid-range of yields:

Pricing

Because the auctioned real yield was slightly above the coupon rate, investors got this TIPS at a discounted unadjusted price of 99.810964. In addition, it will carry an inflation index of 1.00086 on the settlement date of March 31. With that information, we can calculate the exact cost of a $10,000 par investment at this auction:

- Par value: $10,000.

- Adjusted principal on settlement date: $10,000 x 1.00086 = $10,008.60.

- Cost of investment. $10,008.60 x 0.99810964 = $9,989.68.

- + accrued interest of $38.88.

In summary, an investor purchasing $10,000 in par value will pay $9,989.68 for $10,008.60 of principal on the settlement date of March 31. From then on, the investor will earn accruals matching future inflation plus collect an annual coupon rate of 1.875% on adjusted principal. The $38.88 in accrued interest will be returned at the first coupon payment on July 15.

Inflation breakeven rate

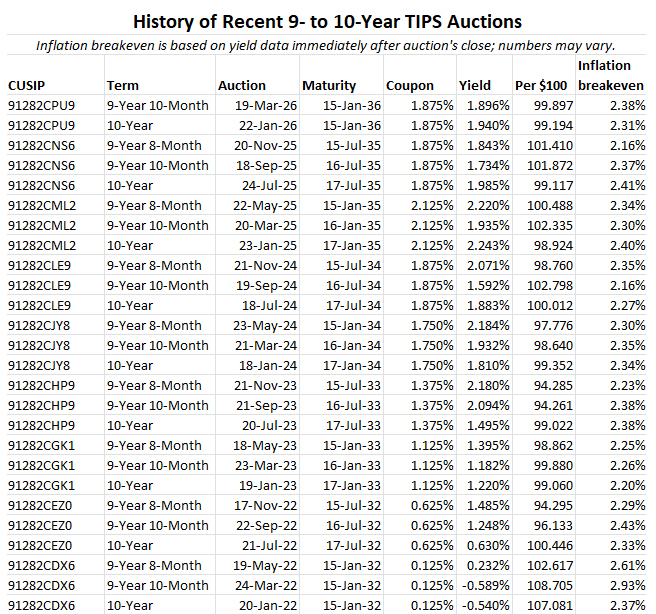

At the auction’s close, the 10-year Treasury note was trading with a nominal yield of 4.28%, giving this TIPS an inflation breakeven rate of 2.38%, a bit high but in line with many recent auction results. This means the TIPS will outperform the nominal Treasury if inflation averages more than 2.38% over the next 9 years, 10 months. Inflation has averaged 3.3% over the last 10 years, ending in February.

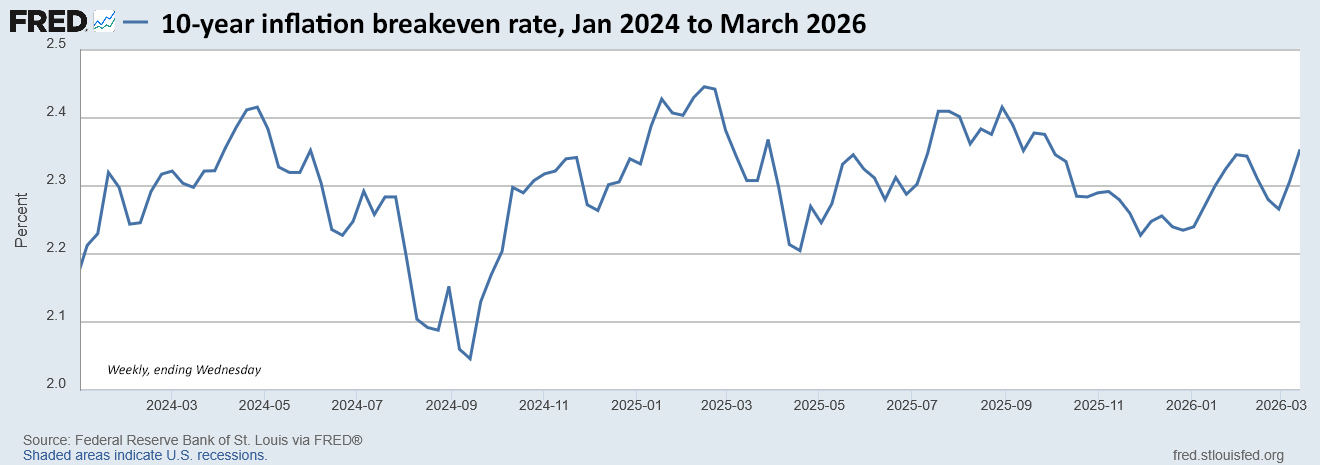

Here is the trend in the 10-year inflation breakeven rate over the last two years, showing that this auction ended in the trend’s higher range:

Thoughts

This looks like a solid result for investors. The yield of 1.896% was below January’s originating auction at 1.940%, but still attractive when compared to auctions over the last 15 years. For investors, the Treasury market is highly uncertain. The White House appears to be asking Congress for an additional $200 billion to support the war with Iran (and potentially to restock dwindling weapon supplies.) This would add to the Treasury’s heavy load of borrowing and potentially drive medium- and longer-term interest rates higher.

Inflation definitely is a concern for the near term and possibly longer. And then what will be the effect of an oil-price-shock on the U.S. economy? In his press conference Wednesday, Powell used the term “don’t know” 17 times (Forbes did the counting), including this quote on the current oil crunch:

The economic effects could be bigger, they could be smaller, they could be much smaller or much bigger. We just don’t know.

The Fed doesn’t know, and neither do we. And for that reason, investors should set aside some allocation to protect against inflation.

CUSIP 91282CPU9 will get one more reopening auction on May 21 and then a new 10-year TIPS will be auctioned on July 23. Here is the history of auctions for this term over the last four years:

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Apologies for being off topic (i.e. TIPS) but this feels like a proper bear market for stocks and bonds. Both stocks and bonds (domestic and international) had a great 2025. But now gasoline has gone up close to $1 per gallon in Michigan and the cost of things derived from oil (fertilizer, wheat) has also begun to rise. My rent renewal lease has a 6% rise. I bond holders (myself included) may need to wait until the November reset for all of these things to be fully baked in.

Historically the stock market tends to go down in the second year of a presidential term and now we’re in the midst of a war with an uncertain outcome. The question is does one seize the opportunity of cheapened asset prices or wait it out anticipating further declines? The investment professionals always say don’t try to time the market, it’s a fools errand. But these are distinctly unsettled times. I suppose the big question on the horizon is will central banks be forced to raise interest rates to contain anticipated inflation?

I am posting an article on this topic Monday morning. At this point, the stock market hasn’t even entered a correction. If we get to a true bear market, I would probably look to rebalance. The problem is that both stocks and bonds are moving lower, which means the market is doing the rebalancing.

Real YTM for 5 year TIPS had a sharp increase from 1.17 on 3/17/26 to 1.38 on 3/20/26. It was looking like the I-bond fixed rate was going to decline to 0.80% on the 5/1/26 reset, but now with this uptrend, we are likely to see the I-bond fixed rate remain at 0.90%.

I checked this yesterday and it could still go either way, but 0.9% is still in the lead.

The real yield sure shot up today

Investors don’t want to hold anything over the weekend, I’m guessing.

Chaos breeds opportunity.

I decided roll my 1/15/27 0.03% real yield tier (which I won’t use due to continued employment) to 2047-2056 and bump up the real yield to 2.7%.

I do plan to hold to maturity. Could the yields go higher? sure. I think it is also very likely that they will go lower at some point in the next 10 years and provide a nice exit opportunity.

If I see 2.8% I’ll probably do another set.

I opted the other way in my wavering, deciding that a tenth of a percent or so less was close enough to the original yield to finish my 2036 rung with funds that have become available since the January auction. The difference was closer than I’d hoped and I’m fine with the results. It keeps the allotment ahead of official inflation whatever may come.

I hemmed and hawed but finally decided last night that the Real Yield result wouldn’t make me happy in this highly inflationary environment, so I opted out. In another two months, real yields may go higher. I’ll add to my small January purchase in May if they do.

Agreed, I also sat this one out waiting for a better return: at least 1.95 at auction and 2+ in the market. This has caused me to sit out the last few 10 year TII sales. Maybe May rates will be more to my liking.