CUSIP 91282CCA7 had one of the ugliest TIPS auctions in history. And yet … it did well versus a nominal Treasury.

By David Enna, Tipswatch.com

Back in April 2021 I was out-of-my-mind frustrated by ultra-low real and nominal yields that offered little chance to surpass inflation. In those days, elite money market funds were yielding about 0.01% as the Federal Reserve held short-term interest rates near zero.

So I was intrigued (more out of boredom than financial sense) by the Treasury’s auction on April 22, 2021 of a new 5-year Treasury Inflation-Protected Security, CUSIP 91282CCA7. At the time, I was interested in “nibbling” into TIPS auctions after a long spell on the sidelines.

But I decided against a purchase. In my preview article for that auction I noted:

As of Friday’s market close, the Treasury was estimating the real yield to maturity of a 5-year TIPS at -1.73%, meaning an investor would be willing to receive a return that trails official U.S. inflation by 1.73% over the next five years.

Investors are going to pay a premium of about 9% above par for this TIPS, and then will receive coupon interest of 0.125% plus accruals to principal matching inflation over 5 years.

In closing, I noted that I Bonds were the superior investment:

You can purchase a U.S. Series I Savings Bond today and get a fixed rate of 0.0%, which means its real yield is 0.0% and your investment will very closely match future U.S. inflation for as long as you hold the I Bond. That is a 173-basis-point advantage over a 5-year TIPS.

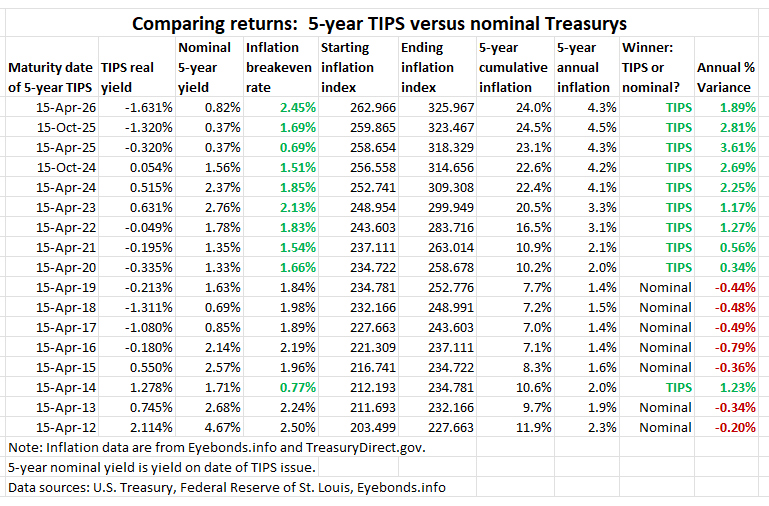

At its originating auction, CUSIP 91282CCA7 got a real yield to maturity of -1.631%, which at the time was the lowest real yield at auction for any TIPS in history.

How did CUSIP 91282CCA7 do?

The February 2026 inflation report, issued March 11, closed the books on this TIPS. It will end with an inflation index of 1.24296 on the April 15 closing date. That reflects cumulative inflation of 24% over five years.

CUSIP 91282CCA7 ended up providing a nominal return of 2.715% over the next five years. At the time, a 5-year Treasury note had a nominal yield of just 0.82%, an incredibly low number. So the TIPS ended up outperforming the nominal Treasury by an annual rate of 1.89%.

Why did the TIPS outperform? When it was issued, it had an inflation breakeven rate of 2.45%, a very high number coming out of a decade of low inflation. But by April 2021 inflation had already started surging higher, with the annual rate rising from 1.2% in November 2020 to 4.2% in April 2021 — eventually reaching a high of 9.1% in June 2022.

In the five years after April 2021, inflation averaged 4.3%, well above the inflation breakeven rate of 2.45%. And that resulted in the TIPS outperforming the nominal Treasury. This result continues a six-year string of out-performance of TIPS over nominal Treasurys.

I Bonds were the winner

If you purchased an I Bond in April 2021, it had a fixed rate of 0.0%, much more attractive than the auctioned yield of -1.631% for this TIPS. By April 2026, the value of the I Bond had increased 24%, for an annual return of about 4.3% — easily exceeding the 2.7% for the TIPS or 0.8% for the nominal 5-year Treasury at the time. (Source: Eyebonds.info).

How about bond funds?

Vanguard’s Total Bond Fund (BND) has had a total annual return of 0.25% over the last five years, according to Morningstar. That poor performance was caused by the beating it took in 2022, when its annual return was -13.1%.

The iShares TIPS ETF (TIP), which holds the full range of maturities, has had a total annual return of 1.25% over the last five years, also under-performing CUSIP 91282CCA7.

Vanguard’s Short-Term TIPS ETF (VTIP) has had a total annual return of 3.46% over the last 5 years, better than CUSIP 91282CCA7’s performance. It benefits from a shorter duration and counter-acting gains from higher inflation.

There’s a lesson here

Two very important takeaways: 1) An I Bond with a fixed rate of 0.0% will be a very attractive investment any time the Federal Reserve decides to repress interest rates through quantitative easing. And 2) Even a TIPS with a negative real yield can be “relatively” attractive if the inflation breakeven rate is lower than seems likely.

Side note: I eventually did make a small purchase ($5,000 par) of CUSIP 91282CCA7 at the June 17, 2021 reopening auction when it got a real yield to maturity of -1.416%. The investment amount was $5,480 — a steep premium because of the negative yield.

This June 2021 version had a slightly better nominal return of 2.767%. The payout on April 15 will be $6,214.80, plus one final, very small coupon payment.

Notes and qualifications

My TIPS vs. Nominals chart is an estimate of performance.

Keep in mind that interest on a nominal Treasury and the TIPS coupon rate is paid out as current-year income and not reinvested. So in the case of a nominal Treasury, the interest earned could be reinvested elsewhere, which would potentially boost the gain. For certain, we don’t know what the investor could have earned precisely on an investment after re-investments.

In the case of a TIPS, the inflation adjustment compounds over time, and that will give TIPS a slight boost in return that isn’t reflected in the “average inflation” numbers presented in the chart.

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Thanks for doing these reviews of maturing TIPS. It’s instructive to see how past investing decisions played out. I was wondering how this 5 year TIPS would have compared with simply doing a rolling reinvestment into 4 week treasury bills over that same interval. When I questioned AI, it suggested a return of somewhere in the 3-3.5% annualized range, similar to VTIP.

Looking ahead to the 5-year TIPS auction scheduled for April 23, right now Bloomberg’s US bond table shows the 5-yr bond with a 3.98% yield and the 5-yr TIPS at 1.30% for a breakeven of 2.68%. Things will no doubt change over the next few weeks (for instance, depending on developments with Iran, the next CPI report, etc), but a breakeven that high seems a little dicey. I’ll be very tuned into your comments about that auction!

I’m trying to summarize this outcome in a simple statement:

TIPs vs I Bonds

TIPs are a worse investment than I bonds if the real yield is negative (I Bond fixed can’t be lower than 0%).

Said another way, I Bonds are a better investment than TIPS if the real yield is negative.

Of course, none of this works in a deflationary scenario.

It is 100% true that I Bonds are the better investment when TIPS real yields are negative. That would even work in a deflationary scenario, since the value of the I Bond would stay stable (beating inflation) but the value of the TIPS would decline toward par value as inflation accruals are eaten away.

I Googled the SEC Yield and Duration for BND for 3/21. They were supposedly 1.2% and 6.9 years.

I am still skeptical, but I am told that bond funds reliably pay close to their SEC Yield if held for a period equal to their duration.

You noted that BND paid 0.25% annually over the 5 year period. Perhaps BND will yield enough over the next 2 years to bring up the average to 1.2%? That would require about 3.58% for each of the next 2 years. The CURRENT SEC Yield is 4.28% so that goal is actually achievable for a 7 year hold.

I still own BND as a core fund in a retirement account, despite the poor performance. The SEC yield can be misleading, but as of April 1 it was 4.3%, which reflects the fund’s longer-term and corporate holdings: https://investor.vanguard.com/investment-products/etfs/profile/bnd Duration is 5.8 years. Its 3-year total return has been 3.53%, so it has been doing better as interest rates have normalized.