By David Enna, Tipswatch.com

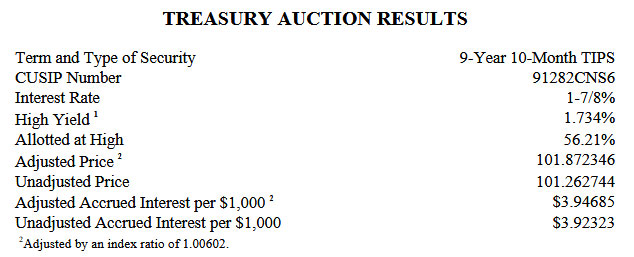

One day after the Federal Reserve acted to lower short-term interest rates, the Treasury’s offering of $19 billion in a reopened 10-year Treasury Inflation-Protected Security — CUSIP 91282CNS6 — drew surprisingly weak demand from investors.

The auctioned real yield to maturity for this 9-year, 10-month TIPS ended up at 1.734%, well above the “when-issued” market prediction of 1.684%. This TIPS had been trading on the secondary market with a real yield of 1.69% just before the auction’s close.

Also, the bid-to-cover ratio was a weak 2.20, the lowest in three years for this term. Conclusion: investor demand was lousy.

So the auction goes down as a flop for the Treasury, but a good deal for investors, drawing a real yield to maturity about 4 basis points higher than market trading.

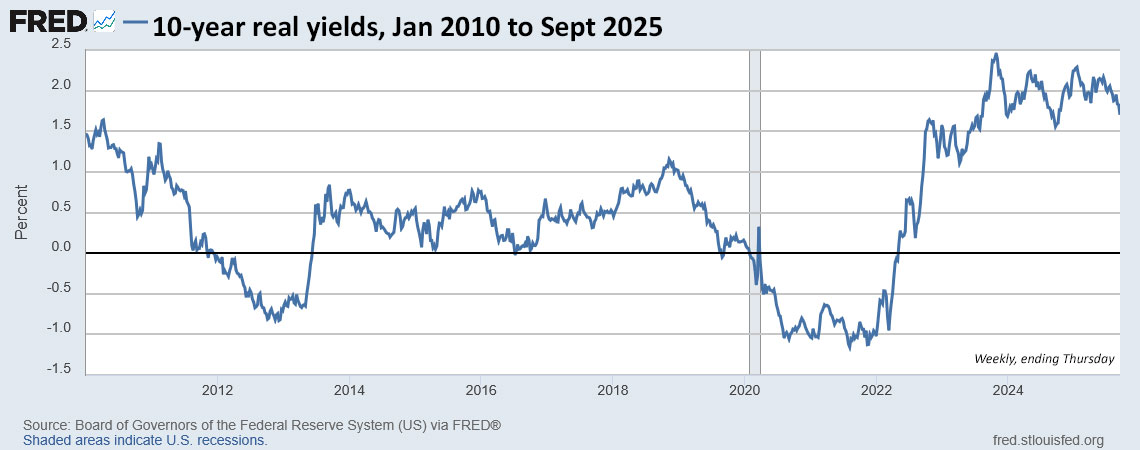

Nevertheless, 10-year real yields have fallen sharply through much of 2025. The originating auction for this TIPS got a real yield of 1.985% on July 24. Its coupon rate was set at 1.875% by that auction.

Definition: The “real yield to maturity” of a TIPS is its yield above official future U.S. inflation, over the term of the TIPS. So a real yield of 1.734% means an investment in this TIPS would provide a return that exceeds U.S. inflation by 1.734% for 9 years, 10 months.

Here is the year-to-date trend in the 10-year real yield, showing the steady downward trend since early summer, as expectations grew for Fed rate cuts:

Pricing

Because the auctioned real yield was below the coupon rate of 1.875%, investors paid a premium unadjusted price of 101.262744. In addition, this TIPS will carry an inflation index of 1.00602 on the settlement date of Sept. 30. With that information we can calculate the cost of a $10,000 par value purchase at this auction:

- Par value: $10,000

- Actual principal purchased: $10,000 x 1.00602 = $10,060.20

- Cost of investment: $10,060.20 x 1.01262744 = $10,187.23

- + accrued interest of $39.47

In summary, the investor paid $10,187.23 for $10,060.20 principal on the settlement date of Sept. 30. From that point on, the investor will earn accruals matching future inflation, plus an annual coupon rate of 1.875% for 9 years, 10 months.

Inflation breakeven rate

At the auction’s close, the 10-year Treasury note was trading with a nominal yield of 4.10%, giving this TIPS an inflation breakeven rate of 2.37% — down from 2.40% before the auction’s close. The result is more or less in line with recent results for this term.

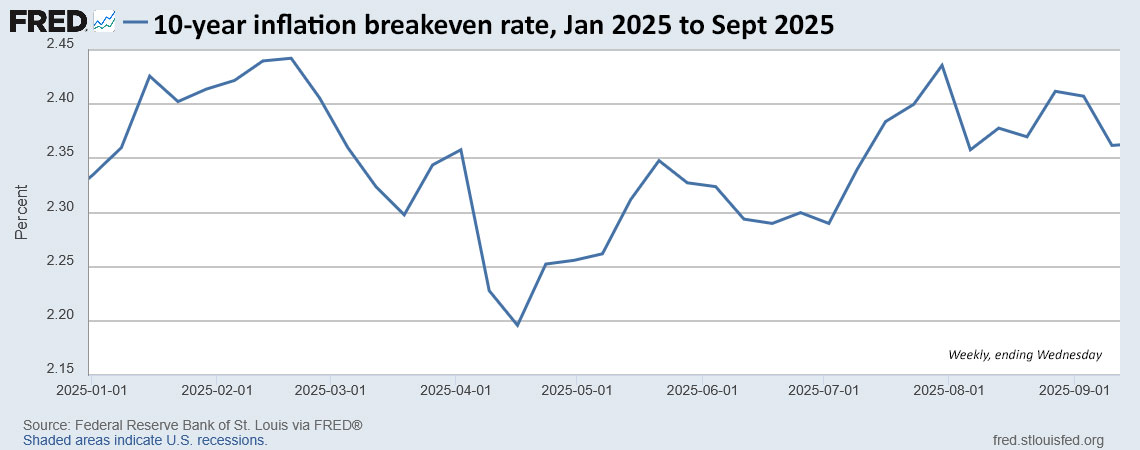

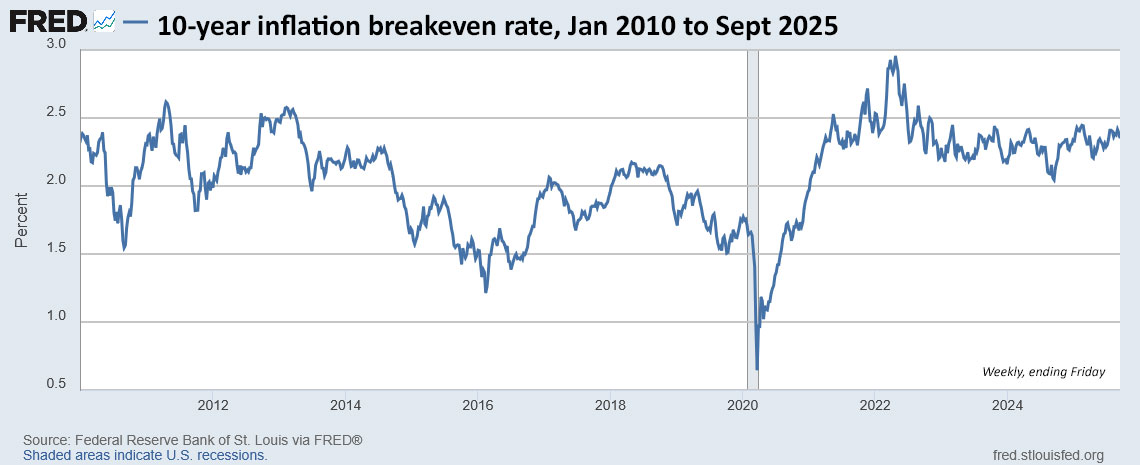

Here is the trend in the 10-year inflation breakeven rate year-to-date. Inflation expectations have been rising since tariff disruptions complicated things in April:

Reaction to the auction

While the auction result wasn’t way out of line, the lack of demand was surprising. Investors could be trying to calculate the effect of future Federal Reserve rate cuts on bond yields and potential inflation? Or maybe investors aren’t interested in inflation protection? (I’d say that would be odd as the Fed launches rate cuts while U.S. inflation is running at 2.9%.)

I suspect that investors are trying to sort out what will be coming in 2026, as the Federal Reserve moves to new leadership. This is from a follow-up Bloomberg article:

The TIPS drew 1.734%, about five basis points higher than their yield in pre-auction trading. By that measure it was the worst 10-year TIPS auction — of which there are six per year — since 2017.

Interest-rate strategists expected the auction to benefit from perceptions that Fed independence is at risk, which could stoke demand for inflation protection. The auction result suggests that the threat has peaked, said Gang Hu, managing partner at Winshore Capital Partners and a specialist in inflation markets.

The auction also drew ridicule from investors on X:

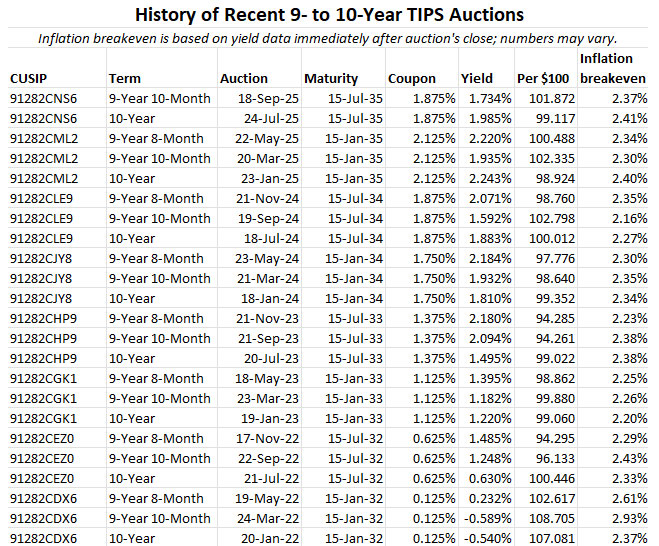

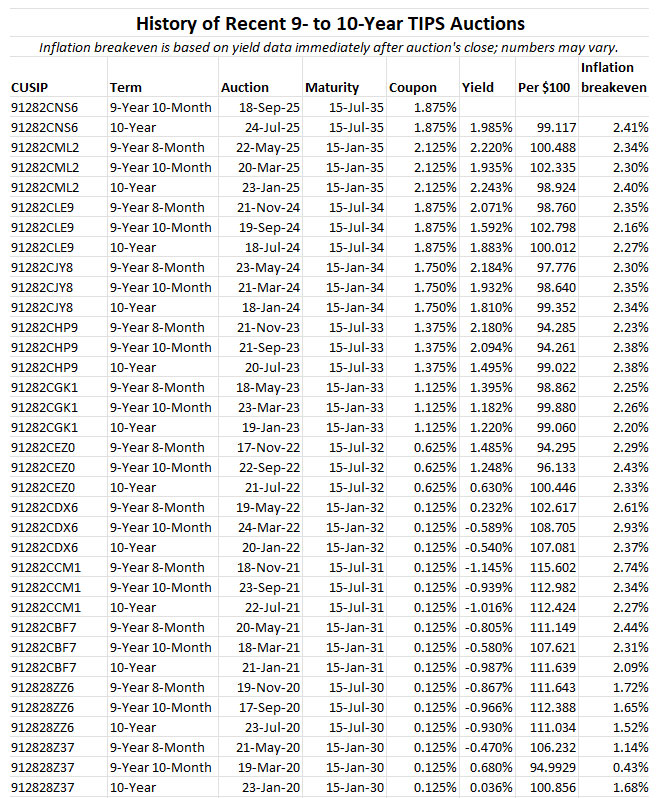

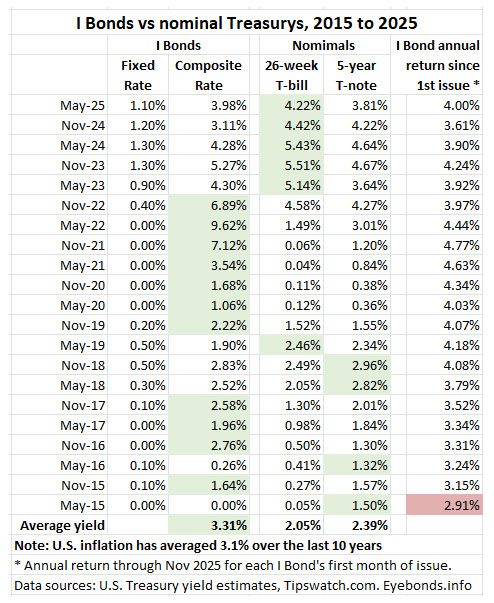

CUSIP 91282CNS6 will get one more reopening auction on November 20, and then a new 10-year TIPS will be offered at auction in January. Here are results for recent auctions of this term:

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

That's a sensible idea, especially if you fear the chance of prolonged deflation. I tend to use nominals for investments…