The Treasury will announce this tomorrow, but as usual it let some details slip out. On Feb. 21, it will auction a new 30-year Treasury Inflation-Protected Security, CUSIP 912810RA8. Update: Here is the announcement.

The Treasury will announce this tomorrow, but as usual it let some details slip out. On Feb. 21, it will auction a new 30-year Treasury Inflation-Protected Security, CUSIP 912810RA8. Update: Here is the announcement.

The coupon rate and yield to maturity will be determined at auction, but we can guess that the coupon rate will come in around 0.50% or 0.625% and the yield to maturity might be somewhere around 0.59%, based on today’s market.

The longest-maturing TIPS currently on the market, maturing Feb. 15 2042, is trading at a yield of 0.576%. This new issue, which adds a year and increases supply, should get a better rate.

(Some definitions: ‘Coupon rate’ is the actual interest rate the TIPS pays each year, based on a growing principal balance. ‘Yield to maturity’ is the true interest rate a buyer gets. This is set at the auction. Buyers ‘pay up’ when the yield is lower than the coupon rate, or ‘pay down’ when the yield is higher than the coupon rate. In addition to that yield, buyers of TIPS see their principal balance rise with inflation until maturity.)

Deal or no deal? My strategy with TIPS is to buy them and hold them to maturity. I don’t ever look at their prices on the secondary market, I don’t care. Viewed this way, TIPS are a very conservative, very predictable, and very boring investment. The problem with a 30-year TIPS is: Will I live long enough to see it mature? I am 59. I could live to 89.

Or … somewhere in my 80s, I might need to sell this TIPS. If that is the case, I am likely – I’d say extremely likely – to receive a secondary market price well below my original investment. I am going to lose money on a very boring investment. Not nice.

Why will I lose money? The Federal Reserve for the last two years has aggressively bought Treasuries to force down interest rates. At the same time, that Fed action has raised the fear of inflation. Both of those factors have driven TIPS yields down to record lows (although TIPS are now trading a bit above those lows).

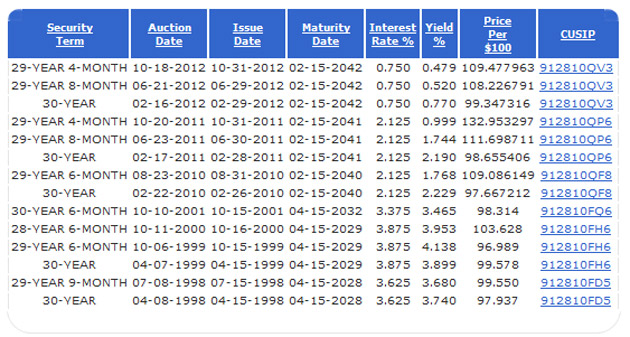

I can only point to history, and here is the history of every TIPS 30-year issue and reissue (make special note of the yield column):

The history of 30-year TIPS is short because the Treasury halted 30-year auctions from October 2001 to February 2010.

Maybe we live in a ‘new world,’ but when I look at this chart, I see 30-year TIPS issued at 3% to 4% above inflation. OK, that was the ‘old days’ of the Internet boom. Today’s rate is 0.59%. Even in this new world, I would expect 30-year TIPS to be paying at least 1.5% to 2% above inflation — the historical return of all U.S. Treasuries.

Someday – maybe soon, or maybe not – 30-year TIPS will again be yielding 1.5%, or 2%, or more. When that day comes, the secondary-market value of a long-term TIPS yielding 0.6% is going to be crushed.

Example: The October 2012 reissue of CUSIP 912810QV3, a TIPS maturing in February 2042, auctioned with a record-low yield of 0.479%. Because its coupon rate was 0.75%, buyers paid more than $109 per $100 of value for this issue. At one time, the yield on the secondary market dipped to 0.335%, but today, it is selling on the secondary market at $104.20 and yielding 0.576%.

So my advice is, traders beware. TIPS yields have already risen above record lows. This could be the beginning of a long-term trend. (Or not, who knows?)

Buy and holder? I can’t deny the attraction of a positive yield on a TIPS, and it might be a nice addition to your TIPS ladder. If you are sure you can buy and hold, and you are sure you will ignore the secondary market, and you truly fear future inflation … have at it.

Another strategy would be to park your money, or buy a 5-year TIPS, and suffer through a yield that lags inflation. Eventually, you could roll over into higher interest rates.

Why do people buy 5-year TIPS paying -1.34% less than inflation? Because it’s for five years. And then they can reinvest. Thirty years is a mighty long commitment.

Thank you Fred Bloggs for this coherent analysis, without undertones of personal agendas... a rarity on the modern www. It…