- The Part B premium will increase to $148.50 in 2021, up from $144.60 in 2020. Congress held down this cost in a spending bill passed earlier this year.

- The annual Part B deductible is increasing to $203, up from $198 in 2020.

- Many Medicare beneficiaries are unaware that higher income levels can trigger possibly lofty surcharges added to their premiums. It takes planning to keep these costs down.

Any day now, if you are on Medicare, you will get a letter from the Centers for Medicare & Medicaid Services informing you of your new premium and deductible costs for 2021. If you planned well in 2019, your costs should be going up only slightly.

But if you planned poorly, you may be meeting up with IRMAA, the Income-Related Monthly Adjustment Amount, which adds a surcharge to your Medicare Part B and D premiums. These surcharges can be lofty, so it’s smart to plan ahead to limit these costs.

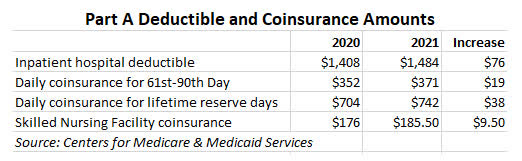

Part A: Hospital insurance

Most people who reach age 65 go on Medicare Part A, even if they are still working. Medicare Part A covers inpatient hospital, skilled nursing facility and some home health care services. About 99% of Medicare beneficiaries do not have a Part A premium since they have at least 40 quarters of Medicare-covered employment.

Although coverage is generally free, Part A has some sizable deductibles and coinsurance costs, and those will be rising slightly in 2021:

Keep in mind that most people on Medicare have a Medigap or Medicare Advantage plan that will cover all over most of the Part A deductible and coinsurance amounts. For example, all standardized Medicare Supplement (Medigap) plans, A through N, provide coverage for Part A coinsurance, and most also cover all or most of the Part A deductible costs.

Part B: Medical Insurance

Medicare Part B can be described as covering “outpatient services,” things like doctor visits, some lab tests, an annual wellness exam, flu shots, diabetes screenings, etc. Medicare Part B generally pays 80% of approved costs of covered services, and you pay the other 20%. Some services, like flu shots and a wellness visit, may cost you nothing.

Part B deductible. Before Medicare pays anything, you have to meet your Part B deductible each year. For 2021, that deductible is increasing to $203, up from $198 in 2020. Most Medigap plans do not cover this deductible and as of Jan. 1, 2020, Medigap plans sold to new people were not allowed to cover the Part B deductible. But once the deductible is met, Medigap plans will cover some or all of your Part B costs.

Part B premium. The Part B monthly premium, paid by all people on Medicare, is rising to $148.50 in 2021, up from $144.60 in 2020. This increase would have been higher, but Congress put a cap on the increase in one of its COVID-19 spending bills.

So, for most people in 2021, Medicare Part B is going to cost $148.50 a month for the premium, plus the cost of the $203 deductible. That’s a total cost of $1,985 a year, up from $1,933 for 2020, an increase of 2.7%.

If you want a quick estimate of your 2021 Medicare Part B costs, you can use a simple calculator developed by Alex Wender, founder and CEO of Bluewave Insurance, an independent Medicare Supplement insurance agency.

IRMAA can make things expensive

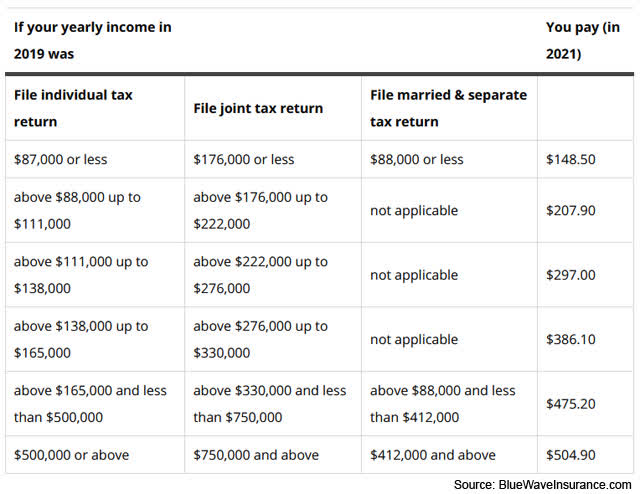

Since 2007, a beneficiary’s Part B monthly premium is based on reported income, known as MAGI, or modified adjusted gross income. According to the Social Security Administration handbook, for Medicare’s purposes MAGI is adjusted gross income (line 8b of the 2019 federal income tax form) plus tax-exempt interest.

Here are the 2021 Part B total premiums for high-income beneficiaries:

These income-related monthly adjustment amounts affect about 7% of people with Medicare Part B. And it’s important to note that people on Medicare Advantage plans continue to pay the Part B premium, and are also subject to the IRMAA surcharges.

CMS just announced these 2021 IRMAA levels last week, but they are triggered by income you reported on your 2019 federal tax return. In other words, when you filed your return earlier this year, you could not know the income levels that would trigger the surcharges. And a tiny mistake can be very expensive.

“The main issue I come across is 99% of people are completely surprised by the IRMAA, they had no idea they would pay extra,” said Wender of Bluewave Insurance. “It’s also tough on folks because it comes at a time when they are usually transitioning to a fixed income, so every dollar counts.”

Part D: Drug coverage

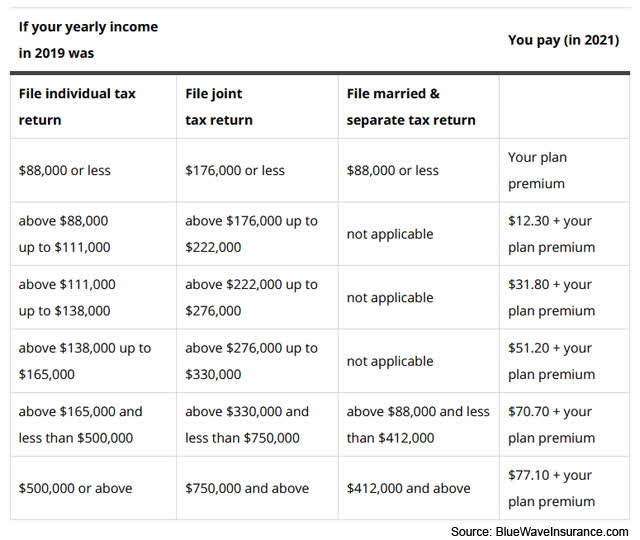

These IRMAA surcharges also apply to Medicare’s Part D premiums for drug coverage. There is no “standard” Part D premium — the cost you pay depends on the Part D insurer and plan you choose. The IRMAA cost, if any, is added on top of your base premium. People in Medicare Advantage plans don’t pay a separate Part D premium, since those plans include Medicare Advantage Prescription Drug (MAPD) coverage. But Part D is built into Medicare Advantage, and the IRMAA surcharge still applies.

“Yes, folks in MAPD plans pay IRMAA on Part D as it’s included in the coverage,” said Wender. “Even if you enroll into a $0 premium MAPD plan or one that returns part of your Part B premium, you will pay the IRMAA if one is assessed.”

However, if your Medicare Advantage plan does not include drug coverage, there will be no IRMAA surcharge, Wender said. (This is rare.)

Here are the Part D IRMAA levels for 2021, based on reported income in 2019:

The high cost of messing up

The IRMAA penalty isn’t a “progressive tax” that ramps up as you go over an income level. Instead, going $1 over the limit is the same as going thousands of dollars over the limit, and incurs the same surcharge.

Here is a look at the annual costs of Parts B and D, plus IRMAA, in 2021:

For example, let’s say a married couple decided to do Roth conversions in 2019 and it left them with a MAGI of $222,100, just $100 over the limit of IRMAA’s second tier. That means their total annual cost for Medicare Parts B and D would rise to $8,371, up from $5,765 if their income had stayed in tier 2. That’s a $2,606 penalty for $100 of extra income.

Financial planning implications

It’s worth noting that the first IRMAA tier for both singles and couples is not too daunting. It adds just $860 to the annual costs for a single filer, and $1,720 to the annual costs for a couple. But the next tier up starts to get pricey, increasing annual costs by $2,163 for a single filer and $4,372 for joint filers.

So I think people looking to take capital gains, buy a boat, make Roth conversions, etc., could feel comfortable in hitting that 2nd IRMAA tier. In fact, anyone planning on doing major Roth conversions over a period of time should probably shoot for that level, but not higher, if possible.

Anyone reaching age 63 this year, and everyone already on Medicare, should be paying careful attention to income levels each year. That means tracking capital gains distributions, dividends, pension payments, annuity income, Roth conversions, IRA withdrawals, Social Security income, etc. It’s a lot of work, but can avoid financial pain.

“To stay under I recommend working with a CPA and financial planner,” Wender said. “Most folks are completely unaware of the IRMAA charge until it’s too late. Sometimes it’s relatively easy to avoid or delay a transaction that may trigger a large capital gains tax and thus cause an IRMAA adjustment down the road.”

Another key consideration is that Required Minimum Distributions are required from traditional tax-deferred accounts beginning at age 72. If you have sizable holdings in these accounts, you could be facing years of higher Medicare premiums triggered by RMDs. And if one spouse dies, and the surviving spouse inherits tax-deferred holdings, the problem magnifies. The surviving spouse now will file a single tax return, pushing IRMAA costs much higher.

So making some Roth conversions, within reason, before reaching age 72 makes good financial sense. Plus, it’s wise to use tax-deferred accounts for charitable giving, beginning at age 70, when qualified charitable distributions are allowed.

You can appeal an IRMAA ruling

The Social Security Administration has very specific rules that will allow you to get a waiver of the IRMAA surcharge, if you meet certain criteria for a “life-changing event” in 2019, which include:

- Work stoppage

- Work reduction

- Employer settlement payment

- Death of spouse

- Divorce

You’ll need to fill out IRS Form SSA-44 to request the waiver.

“IRMAA appeals are very hit or miss, I have had clients win and others lose,” Wender said. “I will say that it’s always worth trying.”

A closing thought

Anyone who has been on a high-deductible, too-complex corporate health care plan will appreciate the simplicity and low costs of Medicare. It’s true that Medicare is not free, and for some people it can even be relatively costly. But the coverage is much superior to traditional corporate health insurance.

People on Medicare paid into the system for many years, and as a reward get good health care insurance. Griping is allowed, but Medicare should be appreciated.

It definitely caused at least a small reduction in six-month inflation. What's amazing is if the United States didn't attack…