By David Enna, Tipswatch.com

Just about every week, I get a comment or question from readers worried about the dangers of buying a Treasury Inflation-Protected Security on the secondary market with a high (or even not-so-high) inflation index.

Why is that a potential problem? Because TIPS come with a deflation-fighting guarantee: At maturity, you cannot receive less than par value, even if the nation goes through a prolonged period of deflation. Buying a TIPS with a high inflation index means part of your investment is not guaranteed to be returned at maturity.

Here is what I think: It’s possible a period of low or negative inflation could mean your TIPS investments are going to under-perform nominal Treasurys. But, under most circumstances, you are highly unlikely to lose money on that investment if held to maturity.

Some things to consider:

It has never happened. TIPS have been issued since 1997 in 5-, 10-, 20- and 30-year maturities (the 20-year was discontinued in 2009). Over that time, no TIPS has matured with an inflation index of less than 1.000, meaning par value. So the “deflation guarantee” has never been triggered for a TIPS purchased at auction.

Inflation is the norm. Since 1971, the lowest average annual inflation for any 5-year period was 1.4%, for the 5 years ending in both 2017 and 2018. For 10-year periods, the lowest was 1.6%, for the years ending in 2017. For a 30-year period, the lowest was 2.2%, for the years ending in 2020.

So if you are buying a TIPS on the secondary market with a high inflation index and 5 years remaining to maturity, you can be fairly confident you won’t be struck by a 5 year period of deflation, eating away at your original investment.

The deflation risk is more pronounced if you buy a TIPS with a very short period (meaning months) remaining to maturity. The longer the term, the lower the potential risk.

Long-term deflation is rare. The United States has not recorded a single year of December-to-December deflation in 70 years. The last deflationary year was 1954, when prices declined by 0.7%. The lowest since then was 2008, when inflation increased 0.1.%

In this chart, I have recorded 1) at the top, deflationary years going back to 1929 along with corresponding Gross Domestic Product changes in each of those years, and 2) at the bottom, the years with positive inflation but negative GDP rates.

The most devastating period of deflation came in the Great Depression years of 1930 to 1933, when prices fell a cumulative 24% from January 1930 to December 1933. That decline was matched by a similar drop in GDP.

But since 1954, inflation continued to increase even when GDP growth was negative, resulting in some classic years of stagflation in 1974, 1975 and 1980. Since the 1980s, the Federal Reserve has taken a greater role in trying to tamp down recessions, possibly easing the effects of economic downturns and holding inflation higher.

In the Great Recession years of late 2007 to mid 2009, inflation continued climbing: rising 0.1% in 2008 and 2.7% in 2009, despite negative GDP growth in 2009.

And in the brief COVID recession of 2020, inflation still managed to climb 1.4% even as the economy faltered. The next year, in 2021, annual inflation rose to 7.0%.

Short-term deflation is a risk

As I noted, the shorter the time to maturity, the more a TIPS is at risk of deflation because TIPS inflation accruals are based on non-seasonally adjusted inflation, which often dips into deflation in the later months of the year.

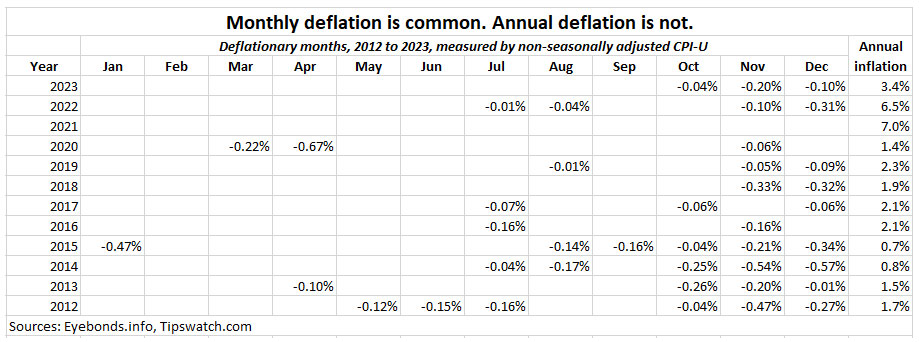

This chart shows month-over-month declines in non-seasonally adjusted inflation, going back to 2012. Note that minor deflation is common in nearly every November and December, and is fairly common in July, August and October. But also note that the annual inflation rate for every year is positive, overcoming the late-year swoons.

So if you are looking to buy a TIPS maturing in April 2025, with just a few months remaining, realize that the TIPS is likely to be hit by deflation in at least two or three of the remaining months. Its final inflation index will be set by inflation in February 2025.

The market knows what’s likely ahead for the April 2025 TIPS, and its real yield is currently higher (3.576%) than that of a similar 5-year TIPS that will mature in October 2025 (2.739%). In other words, deflation presents more of a risk for the April TIPS than it does for the October TIPS, and the market has adjusted prices to reflect that.

Is the October 2025 TIPS (with an inflation index of 1.207) safer than the April 2025 TIPS (inflation index of 1.212). Who knows? Because both are short-term investments, they both have some deflation risk. The April issue has a bit more risk and is priced accordingly. More on this here.

I Bonds have an advantage

U.S. Series I Savings Bonds pay out a composite interest rate based on a permanent fixed rate (currently 1.3%) and a six-month variable rate (currently 2.96%). No matter what happens with the variable rate, the I Bond’s composite rate can never go below 0.0% and the principal can never decline. So I Bonds have rock-solid protection against deflation.

In addition, while TIPS lose principal during spells of deflation, the I Bond never loses value. When inflation starts rising again, the TIPS has to make up lost ground. The I Bond starts increasing from where it left off, a nice advantage over TIPS.

But, on the flip side, the I Bond’s fixed rate of 1.3% (equivalent to its real yield) is well below the 2.0%+ real yields currently found on all TIPS maturities.

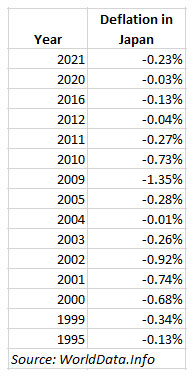

Worst case scenario: Japan

I can’t claim to understand anything about Japan’s complex economy, but I know that both inflation and interest rates have been very low for more than two decades in that country. This is from the World Economic Forum:

Between 1960 and the late 1980s, Japan’s economic growth was double that of the US. But in 1989, there was a stock market crash and a banking crisis in Japan. Inflation in Japan has remained low ever since, and turned into deflation in the 2000s, and again during the pandemic.

After two decades of extremely accommodative monetary policy, Japan is now moving to bring interest rates out of the ultra-low (or negative) range. Annual inflation rose to 2.8% in May 2024, considered a positive trend.

In Japan, rising inflation is considered a positive, which isn’t true in the United States. It’s hard to say if this is an omen for the U.S., or just a singular problem for Japan.

Final thoughts

If you want to build a ladder of TIPS stretching out 20 to 30 years, you are going to have to accept buying additional principal that is not protected against deflation. The TIPS maturing in February 2040 has an inflation index of 1.448, meaning the investor will be buying about 45% of additional principal. Is that actually risky? Sure, there is a very slight possibility of deflation striking across the next 16 years. But not enough to worry about, in my opinion.

If you have been holding any long-term TIPS for many years, they all have inflation accruals that aren’t protected against deflation. I could be wrong, but I don’t think the deflation risk is high enough to abandon these investments.

For example, I own CUSIP 912810FH6 in a taxable account at TreasuryDirect, a long-ago 30-year TIPS purchase that will mature April 15, 2029. It has a coupon rate of 3.875% and an inflation index of 1.90508, meaning it has accrued principal 90.5% above par value.

Do I lose sleep at night worrying about deflation eating away at my principal? No. This TIPS is a great asset. (But today, if I were looking on the secondary market for a TIPS maturing in April 2029, I would not buy this one. I’d prefer the April 2029 TIPS that just had a reopening auction with a much lower inflation index.)

Accepting some deflation risk is part of investing in TIPS. That risk, as I have noted, is fairly minor in most scenarios.

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• Upcoming schedule of TIPS auctions

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I’ve been a long time reader here, and my wife and I have lived on TIPS for income almost exclusively for the last 17 years (built-in COLAs!), and are laddering for the next 50.

When I encourage TIPS to our older couple friends who normally use CDs, I explain that TIPS will preserve your future buying power (along with the extra interest payments), riding the ups and downs of prices (if CPIs are figured fairly), as someone else here alluded, but it takes a while for them to understand it. The par value floor is an apocalyptic plus (you come out further ahead the lower it goes, strangely!), but admittedly not as good as I Bonds (which is why my wife and I are holding our 3.4 and 3 percent 2001/2002 I Bonds to maturity, from back when you could buy $60K per person). One other advantage against apocalyptic market collapse is the Fed is likely to use their nuclear option to protect the economy by rolling out their printing press, and unlike other investments, TIPS holders can ride that out too (just pay a lot of taxes, but be the envy of your friends!)

I think someone also mentioned my idea of, in addition to buying new TIPS at auction, of buying heavily discounted TIPs valued below par and hold them; I think currently a 2028 and a bunch of offerings from 2032 to 2054 qualify as such.

Thank you for the monthly inflation chart history – very useful. I assume its because TIPS use non-seasonably adjusted inflation. The fact they are a few months in appears has to be factored in too, as you alluded to.

I end with a question from the back of my mind – with all the causes of expected future inflation rightly mentioned here, I wonder if the inevitable crash in hyper-inflated rent prices (and maybe housing eventually), which makes up a big part of the CPI and inflation index ratios, and then comes down to earth, will that do some deflationary harm to all of us, which our non-TIPS peers and high prices for other goods doesn’t see?

Lastly – I am a fellow hold-to-maturity guy, but the one time I had some Jan 2025 TIPS to sell a few months early for cash flow this year, their yields skyrocketed, causing a 2 percent+ haircut if I sell them just a few months early, justifying me getting a lot of 0 percent credit cards for 12 months to avoid paying the 2 percent discount (I know, I just hate taking even a modest haircut on principle (excuse the pun)). If you have money on the side, those Jan 2025 TIPS are paying 4 percent annual interest + inflation – no CD should match that!

Thank you for this interesting commentary. You probably know more about TIPS than I do, and that is rare. On the January 2015 TIPS, the last inflation accrual month will be November 2024, which could be negative. But yes a 4% real yield looks enticing. One negative is the inflation index of 1.662, which means the investor is buying 62% additional principal at a slight discount. To outperform a nominal 6-month Treasury at 5.36%, you’ll need half-year inflation of about 1.4%, which is probably about right. The pricing seems fair.

I notice that the 2026 TIPS have quite high YTM’s. They also have high inflation factors. For instance, the 7/15/26 is at 2.37% with a factor of 1.31. Is this a good deal or is there a catch I am missing?

I’ve looked at a lot of these shorter-term TIPS, and my impression is that they are fairly priced versus a short-term nominal Treasury. The two-year Treasury note is yielding 4.71%, so inflation is going to have to average higher than 2.34% over the next two years for this TIPS to pay off. Could happen. This one, though, has a coupon rate of just 0.125%, so it is selling at a discounted price of about 95.6, which helps, but the adjusted price would still be about 124.9, so you’d be buying a lot of additional principal. Like I said, it’s probably priced correctly.

The price only matters when you sell or mature. I suspect most buy these bought for the long term with cash like money to be held forever. Worrying about short term events with long term money seems counterproductive.

Excellent analysis and charts. I worry about a lot of things, but deflation isn’t one of them. Deflationary periods were more common in the 1800s before the Federal Reserve was established in 1913. The greater risk is that failure to address our unsustainable debt could cause sustained higher inflation in the coming decades. I’ve also long believed that climate change will increase global inflationary pressures as commodity prices rise and population shifts create imbalances in supply and demand. An article on this topic was just published today: https://www.washingtonpost.com/business/2024/06/23/climate-change-warming-economy-impacts/

If someone bought a TIPS at a discount (below Par value), then the U.S. had deflation, he would lose $ because only the Par would be returned to him. Correct? Kind of an extreme case, but a lot of the TIPS issued a few years ago are trading at large discounts now I assume?

If you bought a TIPS at a discount and and your investment cost was below par value, you would be guaranteed to get par value back at maturity. So you’d have a potential gain. The older TIPS trading at a discount also potentially have large inflation indexes, so even with the discount you could pay more than par value because of that additional principal.

Sorry, I did not understand this comment. Can you kindly elaborate on your admission?

I edited my wording to make it clearer. … New wording: (But today, if I were looking on the secondary market for a TIPS maturing in April 2029, I would not buy this one. I’d prefer the April 2029 TIPS that just had a reopening auction with a much lower inflation index.)

We might add the fact that the Fed’s target for inflation is 2%, not 0%. One would assume they would take actions to increase inflation if it falls below that target, but who knows what could happen.

With all this in mind, one might wonder why hold nominal Treasurys at all. I think it’s been pointed out here that TIPS are intended to protect against inflation that is above expectations. Knowing that the future is always uncertain, the breakeven point tells us what the market thinks inflation will be, right? (As opposed to the iBonds rate, which is set by the Treasury and doesn’t tell us anything.)

If you hold a 5-year TIPS and a 5-year Treasury, you have some protection against inflation coming in above expectations and some protection against deflation. We should consider the portfolio as a whole, not just individual investments. Would you agree?

Yes, I agree.

Can you comment please on ETFs like VTIP and TIP? Since these funds never “mature,” is the deflation risk too high to buy right now? I prefer the convenience of ETFs, just not sure if they are a good investment right now. Thank you.

My quick reaction is that the deflation risk for VTIP and TIP is about the same as it is for any individual TIPS. You could see some short periods of deflation, which will minimize your returns. Because these funds have no maturity date, there is interest-rate risk if you need to sell at a certain point in the future.

Seems you made a typo

(two actualy)

here…. from January 2030 to December 2033

Thanks for the heads up and this is fixed. (I appreciate careful readings!)

Another excellent analysis and information……I was concerned about buying TIPS from the Secondary market with a high accrued principal….now I have a much better understanding if there are additiional potential risks or not…thanks!!!

All things being equal, no deflation risk would be better than even a small amount. With that said, since less than half of my expenses will be covered by TIPs/I-bonds, I wonder if the relatively small deflationary losses I might experience would be more than offset by my reduced overall expenses. It seems like barring an overall economic meltdown (perhaps a big if), I might even come out ahead relative to continued inflation. Am I missing something?

This is a good point. If you have a year of 10% deflation, your purchasing power will have increased 10%, so a reduction in TIPS principal would leave you more or less even. I Bonds would do better, losing no value. Stocks would likely be down 30% or more, so they would lose value. A nominal Treasury with a 5% yield would gain 15% in buying power. (This is a scenario we don’t’ want to see.)

Curious as to why we are even concerned with deflation, given the present environment we are in. We even dignify deflation with an article?

The reason, as I noted, is that is a very common concern voiced by TIPS investors. And as you note, it probably isn’t something to worry about in our current economy.