Update July 1, 2026: Although this article was posted in August 2023, the logic of ladder building holds true today. According to Tipsladder.com, investors today can build a 30-year TIPS ladder with a composite real yield of 2.6% and a safe withdrawal rate of 4.7%.

By David Enna, Tipswatch.com

For years, I was the “buy at auction” guy when it came to Treasury Inflation-Protected Securities. I’ve written a preview article about every auction since April 2011, so that made sense. I was tracking trends, and figured “I’m on top of this.”

But buying at auction limits you to 5-, 10- and 30-year TIPS maturities, and there are only 12 auctions a year. In the last few years, I began the process of building out a ladder of TIPS investments through the year 2043. I realized “this isn’t working.” At times, real yields weren’t attractive. Other times, they were very attractive. Limiting purchases to one maturity a month didn’t make sense.

Why buy at auction? A TIPS investor can make a purchase of just $100 at TreasuryDirect (or $1,000 at most brokerages) and be guaranteed to get the auction’s high yield, the same yield a million-dollar investor gets. On the secondary market, smaller purchases — usually meaning less than $100,000 — get a small penalty in real yield. A typical rule is that the bigger the investment, the higher the real yield. But the differences aren’t dramatic.

One negative of buying at auction, though, is that you can’t predict exactly the real yield you will receive. The auction sets the yield. A year ago, a string of TIPS auctions got higher real yields than expected. But that has reversed in recent months as demand for TIPS seems to be growing.

Why buy on the secondary market? 1) You can choose your preferred maturity date (which is ideal for building a TIPS ladder), 2) you can see the exact real yield you will receive and 3) you can see the exact cost of the investment before you hit “submit.” At the big brokerages — Vanguard, Fidelity and Schwab — secondary Treasury market purchases incur zero commissions.

One negative of the secondary market, as I noted earlier, is the bid-ask spread and sometimes lofty minimum purchase requirements. There will be times you can’t find any seller willing to accept a $10,000 purchase. The solution: Come back the next day and things can change.

Buying on the secondary market can be confusing. Every existing TIPS has a set coupon rate, sells at a discount or premium to par, and has some level of inflation accruals that you will be purchasing in addition to par. All those factors will affect the price you pay, and an investor needs to understand the ins-and-outs.

If you have questions, consult my TIPS In-Depth page for more detailed answers. Also, read this: TIPS on the secondary market: Things to consider.

Why now?

This chart, showing TIPS real yields from 2011 to 2023, pretty much tells the story:

I started this chart in 2011 because that was the first year of truly aggressive quantitative easing by the Federal Reserve, which by the end of the year pushed 5- and 10-year real yields deeply negative to inflation. Oddly enough, that session of QE was triggered by a downgrade of U.S. Treasurys by Standard & Poors on Aug. 6, 2011, which set off a severe decline in the U.S. stock market.

Less than a month ago, Fitch Ratings matched the S&P move of 12 years ago, downgrading U.S. debt to AA+ from AAA. While the 2011 move by S&P set off a rally in the bond market (presumably triggered by the Fed) this year’s downgrade has sent both nominal and real yields rising. The Fed can’t and won’t come to the rescue — and in fact is probably fine with higher bond yields.

What’s remarkable about this chart is the fact that real yields across the spectrum of maturities are aligning close to 2%, traditionally an attractive yield above inflation for any Treasury investment. It’s highly unusual to see that sort of alignment for maturities ranging from 5 to 30 years.

Here is the 2023 trend in real yields across popular TIPS maturities:

A ladder-building opportunity

The investment world — which rarely pays attention to TIPS and real yields — is starting to take notice. A Bloomberg article posted on Yahoo Finance this week had the headline: “Lesser-Known Treasury Yield Is on Brink of Historic Breakthrough.” The article noted:

The yield on 30-year inflation-protected Treasuries is on the cusp of exceeding 2% for the first time in more than a decade. … For some, a 2% “real yield” is a screaming buy … For others, uncertainty about whether inflation has peaked — combined with the US government’s growing borrowing need — means that all types of long-term yields may need to be higher still. …

“Our message is get into bonds, both nominal and real,” said Rob Waldner, chief strategist fixed income at Invesco.

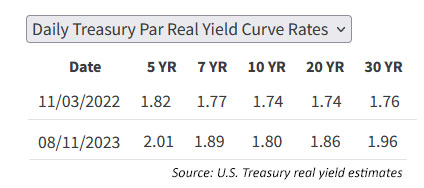

Real yields certainly could continue to rise, but in mid-August 2023 an investor can jump into the secondary market and purchase TIPS of most maturities and guarantee a return of 1.8% above inflation, or higher. So a ladder could be assembled in a few days, as financial adviser and author Allan Roth demonstrated in his October 2022 article: “The 4% Rule Just Became a Whole Lot Easier.”

Roth wrote that article as real yields were hitting a high for 2022, but those yields quickly declined later in the year in the wake of several mild inflation reports. Note that today’s real yields have now surpassed the 2022 highs across all maturities:

My TIPS ladder is complete through 2043, but I’ve gotten into the habit of checking the secondary market every day for issues with real yields close to or surpassing 2.0%. I still want to make additions. (FYI, I do my trading on Vanguard’s site — where I have a traditional IRA — but I believe the Fidelity bond platform provides more complete information.)

On Sunday, I found these TIPS with real yields above 2.0%, but the results vary day to day. Some days you will find none. I limited the search to TIPS maturing from 2028 to 2043:

The bond market is closed on Sunday and all of these TIPS had minimum purchase requirements of $50,000 or higher. Normally, but not always, the minimum purchases get lower when bond trading is active. On Vanguard’s site you can click on the “Show more” link to see the potential offerings. In recent months I have had few problems finding potential purchases in the $10,000 range.

Note that these TIPS yielding higher than 2.0% have maturity ranges dating from 2028 to 2043. But for 10-year TIPS, the yields are likely to be around 1.8% at this point, which is still attractive. (The auction of a new 10-year TIPS last month got a real yield of 1.495%, about 30 basis points lower.)

Final thoughts

I am not suggesting pouring all your investable money into a TIPS ladder, all at once. But if you are currently building a TIPS ladder, or want to start one, real yields in August 2023 offer a unique opportunity, with yields high across all maturities.

Remember, though, that real yields could go higher. My suggestion is to determine an asset allocation for TIPS and invest in them with the intention to hold to maturity. If you are happy with the real yield you are getting, don’t worry about future market fluctuations. Or … reserve cash to buy more at a future date.

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• Upcoming schedule of TIPS auctions

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Thank you for this outstanding web site. With current events in the US government, are you concerned enough about future Treasury credit ratings (or solvency) to consider diversifying your TIPS holding with inflation-protect bonds from other countries (or, err, perhaps with gold)?

Thank you again.

Concerns about the U.S. debt are legitimate, in my opinion, but I would not consider trying to find inflation-protection overseas. There are limited products for that. I’ve never had an interest in Bitcoin and never invested in gold. So I am sticking with U.S. Treasury investments (and a few brokered CDs) for individual holdings in my fixed-income portfolio.

Thank you so much for this outstanding web site. Can you say a couple words about last month’s TIPS yields? Is it correct to say that obtaining a real YTM of 2.5% is terrific, but not any kind of world record, since TIPS yields above 4% could be had in the year 2000?

I moved about a fifth of my life savings into TIPS last month, and am contemplating whether to move more, because I am concerned about the stability of the equity markets. Is it fair to say that current yields around 2.3% are terrific, and while we can imagine higher yields in the future, they are unlikely to occur, and if they do occur, it would be relatively transient?

And then one more question. This is kind of from left field but you have such an incredible perspective that I would be interested in your view: with current events in the US government, are you concerned enough about future Treasury solvency to consider diversifying your TIPS holding with inflation-protect bonds from other countries (or, err, perhaps with gold)?

Thank you again!

Yes, 2.5% real yield is quite good, but yields could certainly go higher. I think a real yield of 3% on longer-term TIPS could be a possibility, but 4% isn’t likely. But no one knows. Last month, the yield curve was pretty steep, with longer maturities getting higher real yields. That has narrowed down in February, with the 30-year down to 2.35%.

Pingback: Now is a great time to build (or improve) a long-term TIPS ladder | Treasury Inflation-Protected Securities

Pingback: For the right investor, this week’s 30-year TIPS auction looks attractive | Treasury Inflation-Protected Securities

Is anyone concerned about a TIPS bond ladder in their IRA not being enough to meet their RMD? It seems likely that as the principal builds each year by inflation that the balance of the IRA may increase so high that the RMD will exceed the TIP maturity for certain years.

It’s possible, certainly. In my traditional IRA ladder, I have 40% of the money in more conventional bond and stock index funds. I will use those to help withdraw RMDs as needed.

Thank you for the timely post. I primarily starting visiting your site in 2020 when I purchased some I-Bonds. I tried to read some of the posts on TIPS but back then however since the yields were negative I did not invest the time to truly understand them.

Also, timely I recently read William Bernstein’s new release of The Four Pillar’s of Investing which in this 2nd edition release he advocates to have 25 years of financial needs (what he calls RLE, or residual living expenses) invested in TIPS.

Reading your post “Now is an ideal time to build a ladder of inflation-protected TIPS” and William Bernstein’s book resonated with thoughts I had. I read this post and your TIPS In-Depth, and other articles to educate myself on TIPS. They were very helpful!

Since I already purchased 5-years in RLE in CD’s in April, in August I purchased a TIPS ladder from 2029 through 2049. Since there currently no TIPS available from 2034 to 2039 I added what I need for these years to my purchases for 2032 and 2033.

Thanks again for all the valuable information on your site…

After reading this blog (and the Bogleheads forum) in depth, I have taken the plunge and purchased my first TIPS ladder (inside my IRA). Most of my IRA is Vanguard Total Bond Index fund (VBTLX). Based on very conservative assumptions, I figure that the dividends from VBTLX will cover about one-third of my RMD (which is due to begin in a few years). My TIPS ladder will cover the rest of the RMD through 2033. This is intentionally a fairly small, short ladder: I wanted to learn the nuts and bolts of building the ladder on Vanguard and to learn more about filling in the the gap years when no TIPS mature.

I used the tipsladder website to help build the ladder – it seemed to work well and is simpler to use (at least for me) than the spreadsheet from Bogleheads (written by “Cruncher”, I think).

I’m not a fan of the Vanguard website in general, and buying the ladder was more complicated that it should be, but I have no experience with other investment companies, so don’t know if Vanguard is any better or worse than others.

Since you are building to 2033, you didn’t need to worry about the complexities of the gap-year purchases and tipsladder.com is a good resource. On Vanguard … I also do all my purchases there. I have learned the ins and outs; the negatives are more about the clunkiness of the presentation. I think you are on the right track — similar to mine except my ladder goes to 2043 — but of course we don’t know what the future will bring.

I’m growing increasingly dissatisfied with Vanguard’s clunkiness also. I’ve been slowly shifting assets to Fidelity, a much more robust and user-friendly platform.

David….why would you worry about deflation? Real return is all that matters in terms of spending power, and you are guaranteed to get at least the yield to maturity quoted when you buy the bond, regardless of inflation or deflation.

You could do even better in real terms if deflation is extreme.

Consider this very extreme example:

Instead of buying a house for $500K today, you decide to invest the $500K in TIPS maturing in one year at a YTM of 1% real.

Over the course of the year there is 99% deflation.

So at maturity the cost of the same house is only $5K.

When the TIPS matures you receive $500K.

You can now buy 100 similar houses with the proceeds.

Even if you paid a whopping $5M for the TIPS that originally sold for $500K on the secondary market, you could still buy 90 more houses than you could have bought a year ago had you not invested in the TIPS.

True, if you invested in a 1 year nominal Treasury at 5% instead of TIPS you would receive $25K more at maturity and you could buy 5 more houses. But if inflation exceeded 5% you could no longer buy the house that you could have bought a year ago.

Buying power is all that really matters. So when people speak of “deflation risk” with TIPS, am I missing something?

I don’t spend a lot of time worrying about deflation, but it has always bothered me when I have to pay a premium price for a load of inflation-adjusted principal. But this year I have done that, several times. As I have noted, I own a lot of TIPS with a lot of inflation accruals and I don’t lose any sleep about the potential risk of deflation. (On the other hand, as you note, if years of extreme deflation set in, a 20-year nominal Treasury paying 4.48% is going to be a big, big winner. Also, I Bonds with a fixed rate of 0.9% are going to do very well, since their principal balance never declines.)

Is your plan to live off matured bonds or roll over? This all seems like a structured savings plan more than a ladder.

As I have noted previously, the plan to fund future required minimum distributions beginning in 2026. But it’s possible some of the TIPS could be rolled over to fill in the TIPS “gap” from 2034 to 2039, when there are no TIPS on the secondary market. But there is no getting around the RMDs, so money is coming out of the traditional IRA from 2026 onward and maturity TIPS will be the primary source.

Got it. I’m doing same thing with STRIPS since current income not necessary.

Pingback: Experiment: Let’s try out a very short-term TIPS | Treasury Inflation-Protected Securities

Now that I have a nice TIPS ladder from 2026 to 2033, I started looking at how to keep rolling that forward – i.e. to find a treasury I can invest in at the end of 2023 which matures in 2034. I knew about the TIPS “gap” but I was surprised to see that the only bond (via Vanguard) maturing around the start of 2034 is a STRIPS bond with YTM of 4.44. I do not need income from this bond and the return seems pretty good over 10.5 years. Any words of wisdom on this and STRIPS in general would be appreciated.

It’s a problem. The general advice for income-matching TIPS ladders is to buy an oversupply in 2033 and also in 2040. There will be a new 10-year TIPS issued in Jan 2024 and as long as real yields hold up that should be an oversupply buy. You could also look at using I Bonds to help fill those years, if you actually will need to produce income. Or look at nominal Treasury bonds to fill part of the gap (available in years 2036 to 2039, with nominal yields about 4.3% on the secondary market). I don’t understand STRIPS, so I have no opinion.

“When this bond is stripped, the principal payment and each of the 20 interest payments becomes a separate security.”

I almost stopped reading after this sentence, but it is kind of intriguing – if this was an automatic process, I can see some benefits. But, since this has to be done through a financial institution, what’s the point? Maybe for large institutional retirement plans it is worth it – but again sounds like extra complexity. Large plans have all kinds of constant transactions going on, why not just rebalance periodically.

STRIPS are pretty cool, but a niche product. It’s a nominal future payment, with no interest along the way, so it’s sold at a discount which represents your return. Basically TBills, but for longer term. I bought a strips ladder to pay my 30 year mortgage, years 18-30 when nominal rates on them were 5.4% (avg) versus my mortgage of 2.8%. Pure arbitrage. Even with the tax wedge, I’m ahead. I need $22k/yr in nominal dollars for my annual mortgage payments, and buying the ladder was cheaper than paying off the mortgage. Since the mortgage is fixed, I knew exactly how many nominal dollars I needed, but no clue how many real dollars that will be.

Thank you as always for such a thorough explanation of all things TIPS and I-Bonds. I was not a fixed income investor (aside from cash) until the summer of 2022 when inflation was hitting new highs, and now I own I-Bonds, Bills, Notes, TIPS, and Agencies all in the 1-10 year timeframe thanks to your insightful articles. The language of bonds was a foreign language to me before reading your posts. Thanks again for everything!

I see there is a 30 year TIPS offering next week. Those longer term fixed rates are looking really nice and are very tempting.

However, given the change in inheritance rules for retirement accounts (per SECURE 2.0) to a 10 year period rather than over the life span of the (non-spouse) person who inherits it, I have been contemplating the terms of my fixed income assets. To date, I’ve been going out no longer than 10 years.

I spoke with Fidelity about this — what happens to those fixed income assets that have remaining terms longer than 10 years? The inheritor can sell them off or they can be moved into a non-retirement account any time within the 10-year time liquidation time frame.

Given that TIPS (from a tax standpoint) are most easily handled in a tax sheltered account, I am reluctant to have the inheritor have to deal with them in a taxable account (the hassle of dealing with an adjusted basis along with the usual tax hassles). That then requires selling them, perhaps at a time that would result in a loss.

I’d be interested in what other people have to say.

It’s an interesting question. I am no longer investing in 30-year TIPS because they go beyond my lifespan, and very likely my wife’s. One immediate reaction is that someone inheriting an investment portfolio is going to be better off with it, even after taxes. Nice problem to have. Inheriting any investments (including stocks) in traditional IRAs creates similar issues, except that the market for those is more clear cut.

Good points. And, I suppose, those longer dated TIPS could also become more valuable and sold at a premium if future rates are lower. One can only see so far down the road, but good to understand the possible pot holes.

First, thank you for the very informative post! This is my first (attempted) TIP purchase in the secondary market. I searched on Schwab for a TIP maturing in 3/2032 – 10/2032. The plan was to purchase face value $3,000. I received the following trade details:

Buy $3,000 CUSIP912810FQ6 @ 110.351 Limit, Fill or Kill

Settlement Date: 08/21/2023

Underlying Quote Information US Treasury TIP 3.375% 04/15/2032

Detailed Info

Maturity: April 15, 2032 (8 years, 7 months and 28 days from today)

Quoted Price $110.351

Yield to Maturity YTM 2.062%

Coupon Rate 3.375%

Market Price:$3,310.53

Estimated Markup: Estimated Markup Help$0.00

Principal Amount:$3,310.53

Accrued Interest:$60.80

Estimated Total Cost: Estimated Total Cost Help $5,744.85

I canceled the order because I cannot understand why the estimated total cost is $5,744.85.

Can you explain this number?

Thank you!

This is a great example of why buying TIPS on the secondary market can be confusing, and also why it all makes sense if you understand the factors involved. First off, this TIPS (originally issued in October 2001) is highly unusual. It matures on April 15, 2032, making it a 30 1/2 year TIPS, the only one ever issued of that term.

1) The Schwab summary doesn’t show it (probably it was on an earlier page) but this TIPS has an inflation factor 1.71643 which reflects inflation rising over the last 22 years. That means if you buy $3,000 par you are actually buying $5,149 of accumulated principal.

2) Also, it has a coupon rate of 3.375%, way higher than the current market rate of about 2.06%. So to get that coupon rate you need to pay $110.35 per $100 of value. So for $5,149 of principal you will be paying about $5,682, plus $61 of accrued interest, so you end up at $5,744, as Schwab quoted.

3) The accrued interest will be returned to you at the next coupon payment, so your actual investment cost is about $5,682 for $3,000 of par value. But remember, you are receiving $5,682 in principal, not $3,000.

And if that TIPS is just too confusing, there are two others that mature in 2032 with smaller inflation indexes and lower coupon rates, meaning they sell at a discount instead of a premium.

Thanks to you and others for increasing my understanding from all that’s written here. I built a ladder yesterday from 2026 to 2033 (my chosen period) with real yields all above 2%. However, there is one thing I can’t wrap my head around. I bought cusip 912828N71 which currently has an index ratio of 1.28644 meaning that every $1,000 par principal is now worth $1,286.44. However it cost me $1,221 to purchase. I must have this wrong. Please correct me.

Just figured it out. I was reading the ratio for dates ahead – i.e. 9/30

Real rates 2.2, nominal 10 year 4.3.

Bond market knows something

… or is afraid of something and that something isn’t a recession, apparently. This reminds me of a fast upsurge in rates in October-November last year, until mild inflation reports sent everything lower. I think the Fitch ratings downgrade opened some eyes to the poor shape of U.S. finances. A lot of borrowing is coming, even as the Fed winds down its balance sheet.

US has no choice but to keep monetizing the debt.

There is a serious risk of continuing inflation.

also, EU & UK rates are going up…Japan, a big buyer of US treasuries, is expected to flex its 10 year JBG yield control policy making Yen a bit more attaractive, US economy expectations have moved from recession to no-landing to soft-landing to almost robust to growth ( with improved productivity as a big kicker), and the Wednesday Fed minutes show their hawkish stand….so plenty of reasons for yields to go up. I want to add duration but greed of waiting for higher rates is making it hard…words of wisdom will help?

Today I bought two TIPS maturing in 2029 and 2030 when both had real yields surpassing 2.0%, the first time I had seen that for those years. But I am still gradually buying in, no major “swoop-in” purchases.

I hit a snafu placing an order on TD Ameritrade for TIPs trading on the secondary market. Yesterday after the market close, I placed an order for 5 x $1000 of the April 2027 TIPS, but the trade was auto-cancelled today because something about a “price limit”.

So, I had to place the order all over again today. This time the trade did execute.

TD really makes it really complicated to trade TIPS on the secondary market.

I don’t think it is a good idea to place after-hours bond orders. The price will change overnight and that is probably what happened. The bond market begins trading at 8 am ET so I think it is safe to place orders then.

Yes, it’s been my experience with Schwab that if you place an after hours bond order, by default it’s put in as a limit order at the listed price. If the price is above your limit at opening the order is cancelled. It’s possible to change it to a market order but why would you take that chance…

I bought the April 2028 maturity TIPS today, coupon 1.25%. Real YTM was around 2.1%.

1k v. 100 k of par, only had a YTM difference of 0.1 bps. Essentially nothing. So, you don’t necessarily need large purchases to get a good price.

Also, this maturity also had a 3.625% coupon. But the yield was only 3 bps higher. I don’t think 3 bps higher is worth it since your deflation floor will be significantly less favorable. So, you can protect well against deflation (I know it’s unlikely) and not sacrifice much yield.

Purchasing on secondaries seems like a very good option currently. I could have waited until the 5 year auction in October, but who knows where real yields will be at that time.

Pingback: TIPS Actual Yields ~2% Throughout All Maturities; 4.4% Assured 30-Yr Withdrawal Charge — My Cash Weblog - My Blog

I added to my TIPS ladder today. Schwab really is a better place to purchase TIPS on the secondary market than Fidelity, as has been discussed in the comments.

Lower minimum purchase+higher yield

Thanks David for your informative articles on TIPS. You mention you are “building out a ladder of TIPS investments through the year 2043”. But unless I am mistaken, there are no TIPS available with maturities of 2034 thru 2039. Am I missing something?

No, that is correct. The ladder has to skip those years for the time being. To compensate, I have tried to build up holdings in 2033, which is easy, and 2040, not so easy. Next year I will add 2034 and advance a year each year after that.

David, thank you for your great columns and to the sharing my fellow readers provide. I look forward to your insights and new comments — both have provided me with a lot of useful insights and guidance.

I am in the process of converting IRAs to Roths for a number of reasons, one of which is the IBonds I bought in the early years when the fixed rate was +3%. Those bonds, when they mature, along with RMDs and Social Security, etc are going to cause problems with IRMAA. So, I want to trim down my IRAs (and future RMDs). And right now, I have a spouse and better tax rates; once the first of us dies, that goes away. The tax man is going to collect one way or the other, and I have chosen to take my lumps now.

You like your TIPS in IRAs, but I am preferring them in a Roth (along with my other fixed income assets) as I like the tax equivalent boost in yield especially now that interest rates have improved. I understand the general preference for stocks in a Roth given the historically higher returns that are sheltered. But, in this whacky world we are living in now, I am no longer increasing my share of stocks.

A silver lining to the lower fixed rate TIPS in my IRA (which have been eclipsed by today’s higher rates and thus show a paper loss) — I will convert them to Roths and take advantage of the fact that the paper loss will now be a guaranteed non-taxable gain in a Roth.

Many people face this same problem, including me. Too much money in 401ks or traditional IRAs, not enough in Roths. Still, it is better than “not having enough money.” If you have a good reason to hold TIPS in a Roth, I see no problem with that.

David, Why are you sticking with CDs and nominal Treasurys to fill in the years up to 2028? TIPS on the secondary market that mature before 2028 now all have real yields above 2%, mostly above 2.5%, and some as high as 3.8%. Also, I have accounts at both Fidelity and Vanguard. Do you know if there is any difference at all between these two firms when buying secondary TIPS in terms of pricing or what is available? I’ve made over 30 purchases using Fidelity and I don’t ever recall a time when there wasn’t an option to purchase even as little as 1 bond ($1K face value.)

I’ve still been investing in TIPS in 2028 this year. Shorter-term nominal yields are very attractive in the 4.5% to 5.5% range and I think TIPS and nominals in the near term will perform about the same. I’m just trying to line up a set amount of cash in a traditional IRA to pay for RMDs in 2026, 2027 and 2028. I already have TIPS maturing in all those years.

Schwab occationally has a better yields. Today, they were offering a 1K TIPS at 2.06% and Fidelity was offering it at 2.031%. That 2.06% was the going rate on Bloomberg at the time. Of course, now that the TIPS yields are over 2%, I don’t have any dry powder left. Who would have thunk this would be happening in August? I was happy to get stuff over 1.5%. Now, not so much!

This is why, being a cautious investor, I was nibbling into individual TIPS starting last summer, first selling off my holdings in SCHP and then working on VTIP. I still have some VTIP left. I did buy a few “dog” TIPS with very low yields (compared to today), but they will do fine when held to maturity. I keep looking for yields “close” to 2.0%. Then I heard on Bloomberg today that one expert sees the 10-year Treasury topping out at 6%. Yikes. I’d want that, too.

I just looked at auction rates for 10 year TIPS and prices at auctions going back to 1997. Don’t understand why any normal human would accept negative real rates or near zero rates starting around 2011. And this lasted for more than 10 years!

The reason: Nominal rates were also incredibly low, often dipping below 2% during those years and hitting 1.46% in July 2016 and 0.64% in April 2020. The inflation breakeven rate was often about 1.5% and fell as low as 0.60% in April 2020, so a negative-yielding TIPS actually did end up out-performing the nominal Treasury. But it was an awful time to buy either.

When you look at the screen shot you posted of the tips on the secondary market… You see how the yield to maturity of all these are somewhat similar. But the coupon rate and the actual bond price can be very different. Being math challenged, is there a benefit/downfall to having a the bond price or the interest rate higher/lower?

The real yield you get and the maturity date you want are the keys. The prices do balance out. I always hated buying a big inflation accrual at a premium price, but I had to do that to fill the 2040 year in my ladder. It has an inflation factor of 1.40 and a premium price of about 102.5. I bought it recently and got a real yield of 1.8%. Now the yield is higher so I may buy more.

You say the prices balances out. Let me just clarify my question again. The secondary tips available to me at my broker. They are all close in the worst case yield. The question is about whether the higher coupon with high premium could out preform TIPS with a low coupon? Looking at available tips, we have a 3.375 coupon and a .125 coupon. Isn’t the coupon rate going to be applied to everything the bond has earned? So it is compound interest? Wouldn’t a very high coupon and a high premium out preform a low coupon rate and a low initial bond cost…. assuming that we had an environment of escalating inflation?

The coupon rate and the price you pay set the real yield to maturity. So the coupon rate is already factored into the price. If you buy at a discount, you are getting extra principal at a discount and a lower coupon rate. If you buy at a premium, you are paying up for principal but get a higher coupon rate. It’s all reflected in the price. However, I do believe a higher coupon rate could give you a bit extra protection against deflation, since the coupon rate will always be paid, all the way to maturity.

Totally agree David. I logged in this morning and saw the 20-year yields over 2% and attractive yields everywhere. The first thing I did was e-mail my buddy saying “I need money” because I’d like to put a bunch to work with these great yields. The second thing was checking in here. I think it is time to cash in some cash holdings to lock in yield+inflation protection.

Do you factor in the inflation accrual? It’s my understanding that certain TIPS would be exposed to deflation, but others less so.

This is true. A large inflation accrual could be threatened by extended deflation, because only par is guaranteed to be returned at maturity. Buying a new issue reduces that risk. It is a minor risk, in my opinion. Also, every TIPS you are currently holding has the same risk.

Thank you David for your continued great articles. In case this is useful for your readers: I have found at Vanguard that I can consistently get a purchase/quotes for less than $10,000 if I try a few times within a few minutes, refreshing the quotes. Sometimes if several quotes are listed at a low minimum, the higher yield purchase will not go through, but always the lower ones seem to work (which are only a few hundredths of a percent lower in yield). Finally, when I spoke with the fixed income group @ Vanguard on the phone, they noted they can always supply a quote (and do the purchase) down to 1 bond, and when I went that route, the yield they gave me was better than what was displayed on line.

CDs have higher short term interest rates. What is the difference in final gains between a CD ladder and a TIPS ladder?

I admit to knowing very little about either, so any thoughts would be appreciated. Thanks!

I didn’t mention this in the article, but I have been using CDs and nominal Treasurys to fill in the years up to 2028, because I want to set up available money for paying RMDs, which will begin for me in 2026. It makes sense to hold both nominals and TIPS.

Why does it make sense to hold TIPS and nominal Treasuries? While I don’t see a contradiction, I don’t see an obvious reason for. (That said, I did but a Treasury Zeros ladder, annual rungs maturities equal to my also nominal mortgage payments so I could arbitrage that.)

The key factor is safety, for a portion of your portfolio. TIPS offer the advantage of a known inflation-adjusted return, with a certainty that some years in the future, you will receive that protected cash. I personally use nominals for shorter-term goals, and TIPS for longer-term goals. But both of these are part of an overall portfolio that includes U.S. stock funds, international stocks and total bond funds, which give exposure to corporate bonds.

For help constructing a ladder from the secondary market you could use the free tool at https://tipsladder.com

fyi, the minimum qtys are much lower on Schwab

As I noted, Vanguard doesn’t show smaller lots until the market is open. Today it is showing lots as low as $1,000.

In my experience, when the bond market is open, Vanguard and Fidelity have very similar bid-ask spreads.

Based on comparisons of the same issues, Schwab tends to have better bid-ask spreads than either Vanguard or Fidelity, especially when buying a quantity of one.

I prefer to buy on TIPS secondary market. I plan to hold them for long periods of time, and often the issues that are not on the run have better yields than the ones that have been recently auctioned. For example, compare real yields on TIPS maturing in the mid-2040s with the yields of the last few 30-year TIPS from the early 2050s.