Interesting article today in the Wall Street Journal, with the enticing headline: ‘TIPS Investors Rush for Exit.’ Here’s the premise:

A surprise drop in gasoline prices has jolted a corner of the bond market, easing investors’ inflation fears and triggering an exodus from a popular form of Treasury securities. …

The move was triggered by a deterioration in the economic outlook. “People are feeling less positive, so they’re taking that out in inflation expectations,” (said Chris McReynolds, head of U.S. Treasury trading at Barclays).

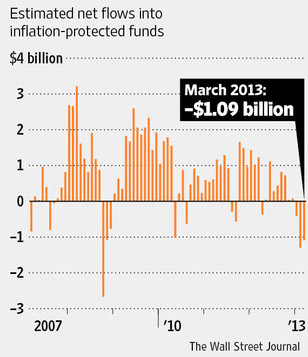

Before we get to rooting for inflation, let’s look at the article’s premise, that investors are suddenly pouring out of TIPS and into stocks, traditional Treasurys or high-yield bonds. This Wall Street Journal chart does show that TIPS mutual funds have been seeing net outflows for the last three months. These outflows have been fairly rare, and we haven’t seen three consecutive months of outflows since the financial crisis of 2008, when TIPS yields skyrocketed upward, and TIPS values plummeted.

Before we get to rooting for inflation, let’s look at the article’s premise, that investors are suddenly pouring out of TIPS and into stocks, traditional Treasurys or high-yield bonds. This Wall Street Journal chart does show that TIPS mutual funds have been seeing net outflows for the last three months. These outflows have been fairly rare, and we haven’t seen three consecutive months of outflows since the financial crisis of 2008, when TIPS yields skyrocketed upward, and TIPS values plummeted.

It’s also true that TIPS breakeven rates have been trending down, which was long overdue. As of Tuesday, for example, the nominal 10-year Treasury closed at 1.75%, and the Jan 2023 TIPS closed at -0.699%, putting the breakeven rate at 2.449%, still rather high but a drop from the 2.531% of Jan. 1, 2013.

But overall, I’d say the TIPS market had a pretty mild reaction to this week’s inflation news. In fact, I’d say it was remarkably mild. Here’s a chart of closing prices of the TIP ETF over the last month, versus the AGG (aggregate bond market ETF):

The TIPS market has outperformed the overall bond market in the last month. And look at the volume bar below the chart. Not much action this week. So there’s not much evidence that TIPS investors are fleeing for the hills … yet. Possibly today’s Wall Street Journal article will change that trend. It certainly will get some TIPS investors thinking.

So, do TIPS holders root for higher inflation? The answer is ‘no’ if you have a sensible asset allocation, divided among stocks and fixed-income investments, with maybe 20% of your assets in TIPS and I Bonds. I don’t endorse putting 100% of your investments in TIPS, especially now with yields so low.

TIPS and I Bonds are insurance against inflation, while at the same time providing modest, super-safe returns. Insurance is something better left uncollected. If your house burns down, you don’t say, ‘Wow! I got to collect the insurance!’ Not when your belongings are smoldering in front of you.

TIPS and I Bonds are often described as a hedge against unexpected inflation. If inflation continues in the 1.5% to 3% range, TIPS holders have a boring, safe investment.When the TIPS matures, the investor collects the money and reinvests. That’s how a super-safe investment works.

If inflation suddenly rises to 6% or 7% or 20%, TIPS holders have a safe, protected investment. It won’t be a time to cheer, because your other investments (stocks, bonds and fixed pensions) might be smoldering in front of you.

You’ll never cheer for inflation. But you will be able to say, ‘I did a very smart thing.’

Pingback: Friday Reading: Home Office Deduction