Summary

- U.S. Series I Savings Bonds purchased from May to October will pay a composite rate of 1.06%, annualized, for six months.

- EE Bonds will continue to double in value if held for 20 years, creating a tax-deferred, compounded rate of return of 3.5%.

- Both of these savings bond investments remain superior to better known alternatives offered by the U.S. Treasury.

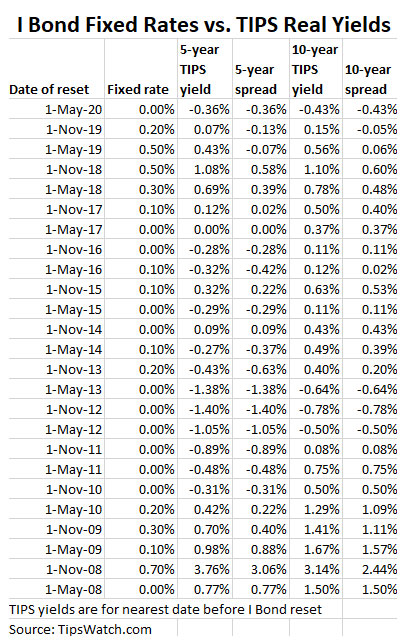

The U.S. Treasury just announced it is cutting the fixed rate of U.S. Series I Savings Bonds to 0.0% as of May 1, a move that was widely expected and won’t dampen the appeal of these inflation-protected savings bonds.

Read my full analysis on SeekingAlpha.com

Can Debt Be Inflated Away? is Paul Donovan’s report from May 7, 2020.

https://www.ubs.com/global/en/wealth-management/chief-investment-office/about-us/meet-the-experts/paul-donovan.html

My last post didn’t work and I don’t know how to delete it. On “WordPress” I am instructed to upgrade to Gravatar. My brain doesn’t have space for another task this morning, so I won’t.

I follow UBS Chief Economist Paul Donovan’s daily update. He has a Nobel Prize, that’s a biggie! Anyway, lets see if this url works. Otherwise, visit his main page and download the PDF.

*Can (Government) debt be inflated away? *

Click to access can-debt-be-inflated-away-en-1493405.pdf

This link worked for me, and thanks for the heads up.

He makes the case for inflation in the out years. I have heard “the noise” of warnings about printing money since I was a teenager and I tire of their lugubrious malaise. But there is something to this:

“…Similarly, Mathieu Savary of the Bank Credit Analyst contends that “Covid-19 has generated an inflationary shock in the medium term.” In addition to the wartime-style budget responses, funneling cash from central banks directly to consumers will be more inflationary than the quantitative-easing programs undertaken to respond to the financial crisis, he argues.

The bottom line: Brace for higher inflation. That means eschewing bonds, which Savary says “display rock-bottom real yields, inflation protection, and term premia” (the extra yield for the risk of holding long-term securities). Similarly, Brigden thinks the only refuge for fixed-income investors is in “inflation break-evens” (the difference between the nominal yield on Treasury notes and TIPS, or Treasury inflation-protected securities). …. ”

27 March 2020 _

https://www.barrons.com/articles/expect-the-unexpected-after-the-crisis-inflation-51585323090

If the issue is that you want the money that you put aside to be available after you are past your “earning years”, maybe you want the I-bond or a TIPS. An eighty one year old “you” won’t look back and say that you took a foolish chance.

Another issue is: Will Congress and the Fed have the courage to turn off the spigots once the economy stabilizes? The stimulus has already caused a gigantic recovery in the stock market, even though unemployment rates will remain high. When unemployment begins dropping, will the stimulus end. Both the Fed and Congress haven’t shown courage in the past to be strong against the “you’ll destroy the economy” criticism and resulting stock market swings lower.