By David Enna, Tipswatch.com

May 3 Update: I Bond’s fixed rate holds at 0.0%; composite rate soars to 3.54%

—————————

If you’ve been reading my posts over the last decade, you know I generally don’t advise jumping right into an investment in U.S. Series I Savings Bonds at the beginning of the year. Most times, there’s a better strategy: Wait until mid-April or mid-October to make a purchase decision.

Why April and October? Because in the middle of those months, the Bureau of Labor Statistics releases a key inflation report that determines the I Bond’s new inflation-adjusted variable rate, to go into effect on May 1 or November 1. After that report is issued, you will then know the I Bond’s new variable rate, and you will have a better idea if there will be a change in the I Bond’s fixed rate. You have two weeks to decide to buy before May 1 or November 1, or after.

It’s a good, sensible strategy. And … I am going to ignore it this year and buy my full allocation of I Bonds in January. In my case, I have a 10-year TIPS maturing on January 15 and I can reinvest those proceeds in I Bonds. Since I will have the cash available, I’ll just go ahead and make the purchase.

The key reason to set a purchasing strategy for I Bonds is to maximize your chance of getting a higher fixed rate, which is always desirable. By waiting, you can scout out the financial markets and take a guess if the fixed rate is going to rise. If it looks likely to rise, wait to invest. If it looks likely to fall, invest before the reset. If it looks likely to stay the same, compare the before-and-after variable rates and decide which one you want for your first six months.

If you are interested in using this wait-and-see strategy, these are the key dates:

- At 8:30 a.m. ET on April 14, 2021, the BLS will release the March inflation report, which will then lock in place the new variable rate for I Bond purchases from May to October 2021. Both the variable rate and fixed rate will be reset on May 1.

- At 8:30 a.m. ET on Oct. 13, 2021, the BLS will release the September inflation report, which will lock in place the new variable rate for purchases from November 2021 to April 2022.

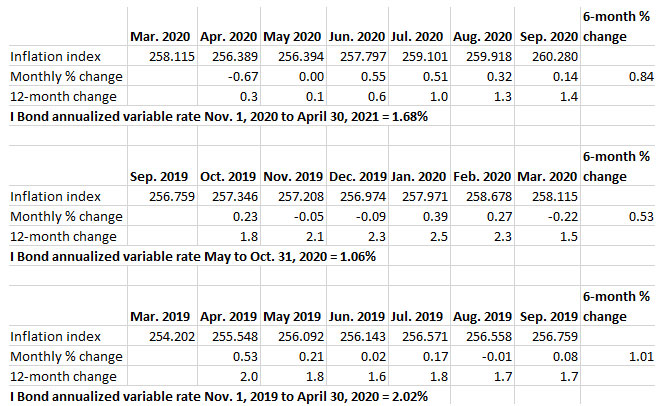

Here are how those inflation numbers have added up to create the I Bond’s variable rate in the last three rate resets, based on non-seasonally adjusted U.S. inflation:

What about the I Bond’s fixed rate?

The I Bond’s fixed rate is currently 0.0% and my thinking is that this fixed rate is highly likely to remain at 0.0% throughout 2021. The Treasury isn’t going to raise the fixed rate above 0.0% when real yields of 5-year and 10-year Treasury Inflation-Protected Securities are well below zero. At this point, these are market-determined real yields:

- 5-year TIPS = –1.63%. I Bonds have a 163-basis-point yield advantage.

- 10-year TIPS = -1.07%. I Bonds have a 107-basis-point yield advantage.

- 30-year TIPS = -0.36%. I Bonds have a 36-basis-point yield advantage.

Because the I Bond’s fixed rate seems likely to remain at 0.0% my recommendation is this: Buy whenever, but I definitely endorse an investment in I Bonds this year, up to the purchase limit of $10,000 per person per year.

What is an I Bond and why is it appealing?

A U.S. Series I Savings Bond is an investment that offers a composite interest rate that combines two elements: 1) an inflation-adjusted variable rate that is reset in May and November based on official U.S. inflation, and 2) a fixed rate that stays with the I Bond until maturity. The fixed rate for I Bonds purchased today is 0.0%, and that means I Bonds in effect have a real, after-inflation return of 0.0%.

OK, a real return of 0.0% sounds awful, but it is actually excellent in today’s environment of negative real yields, across all maturities of U.S. Treasurys and insured bank accounts.

An I Bond with a fixed rate of 0.0% will accurately match U.S. inflation until it is redeemed, earning interest that is tax-deferred and offering excellent protection against deflation. In times of deflation, an I Bond never loses any value. This is not true for a TIPS, which sees its principal balance fall after deflationary months.

Because of its above-market returns and insurance against unexpectedly higher future inflation, I believe the I Bond is the most attractive very safe investment available to small scale-investors today.

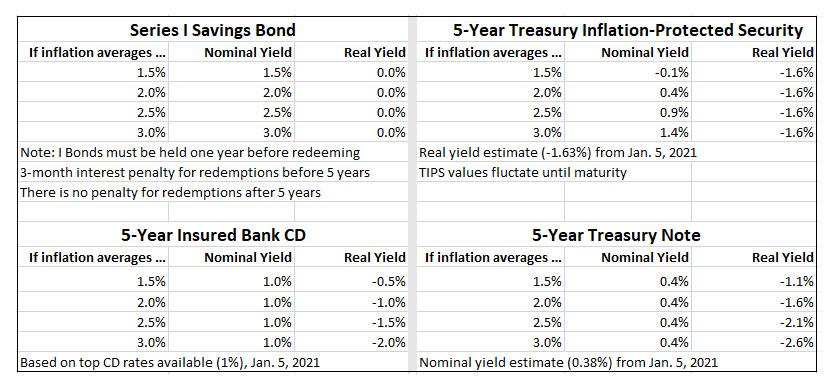

An I Bond can be redeemed in one year with a penalty of three months interest, and after five years with no penalty, or just held for 30 years, tax-deferred, before redemption. These terms make the I Bond comparable to a 5-year TIPS, 5-year nominal Treasury and 5-year bank CD. So let’s take a look at the returns of these investments under varied inflation scenarios:

If inflation averages 1.5% or higher over the next five years, the I Bond easily out-performs similar safe investments, which would all have negative real returns. Because of the added benefit of inflation protection and the above-market real return, an I Bond is a strong investment in 2021.

So … consider an investment, up to the purchase cap, anytime it works for you in 2021.

Who should be interested?

I Bonds are an investment for capital preservation, for protecting a portion of your portfolio from unexpected future inflation. I Bonds won’t make you rich. They make sense as an asset allocation as part of a overall financial plan.

I Bonds can also make sense as a short-term investment, as I explained in a recent article: “Unique Opportunity: I Bonds As An 11-Month Investment.” But, because of the annual purchase limit, I suggest buying an allocation every year and holding them until you need to cash.

—

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he recommends can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Are you allowed to use your S corp to get another 10k? You max out individually, use your S corp or LLC to obtain more.

TreasuryDirect says that a corporation can buy I Bonds electronically, but cannot receive paper I Bonds in lieu of a tax refund.

Mr Enna, Read your article about investing in I bonds today. I have been buying these for about 4 years now. The last 2 were 0% fixed rate. I have looked on the treasury web site and don’t see how to upgrade these bonds when they renew at a higher fixed rate. Is the only way is to sell and re-buy at the higher rate. I really did not want to claim the interest as income. Thanks John Mallard

It’s correct that you can’t upgrade the fixed rate because when you purchase an I Bond, the fixed rate is permanent for as long as you hold it. So, in the future, when the fixed rate does rise above 0.0%, you could sell some of your holdings and buy new I Bonds (the tax is only on the accumulated interest, so it may not be onerous) or just buy the new I Bonds outright, capturing that higher fixed rate and keeping the bonds with the 0.0% rate.

Glad to have found you again Mr. Enna, followed you for a long time on that other site & always enjoyed and learnt something new from your writings. Happy new year & thank you.

Thank you for your articles! I’ve been recommending you to others for years.

We haven’t purchased I-bonds since they went to online only. I just didn’t want to deal with the hassle of another account and password.

Is there information somewhere on the actual purchasing process and what one needs to do? Such as link a checking account, etc?

Excellent! Been following your iBond and TIPS advice for years over at the other site. Happy to follow you here! Thank you for taking the time and posting these articles. Much appreciated.

Here’s to a happier 2021!

Did not work when I attempted this a couple years ago. Estimated taxes are supposed to be paid in approximately equal amounts quarterly is the only explanation I received.

Can you file a tax return extension request with an extra $5000 payment, just to turn that into i-bonds when you file your real tax return? It is worth the effort?

I believe you can still pay estimated 2020 taxes through January 15, so you could pay $5,000 in estimated taxes now and collect the refund in I Bonds later in the year when you file your return. (I don’t use this method, so you’ll want to do some checking.)

Use online IRS Direct Pay with form 4868 to overpay $5K plus what you owe if you’re not getting a return. I’ve been doing it for years. Easy process.

A good way to start the new year is to thank David for his work. So far as I know this sort of analysis is simply not available any where else. (Because you can buy I bonds and TIPS with no one making a buck off of you.) So thank you David and best wishes for the new year. 👍

Thanks again Mr. Enna for the analysis on this important subject. I like the advice and will follow it. Have a great year!