By David Enna, Tipswatch.com

As expected, U.S. inflation surged 0.4% in February, triggered primarily by rising gasoline prices. But the overall February inflation report from the Bureau of Labor Statistics, released this morning, is a bag of mixed messages. One interesting detail is that offers some good-looking data for the next interest-rate adjustment for U.S. Series I Savings Bonds.

The BLS reported that the Consumer Price Index for All Urban Consumers increased 0.4% in February on a seasonally adjusted basis. Over the last 12 months, the all-items index increased 1.7%. Those numbers exactly matched the consensus forecasts.

But the core inflation numbers, which remove data for food and energy, came in at 0.1% for the month and 1.6% year over year, below the consensus estimates. So while gas prices are forcing overall inflation higher, core inflation continues to slumber along at a moderate level.

The BLS noted that gasoline prices surged 6.4% in February and accounted for more than half of the overall increase in CPI-U. Gasoline prices are now up 1.5% year over year, after falling deeply negative throughout 2020. Prices for fuel oil were also up a sharp 9.9%. The electricity and natural gas indexes also increased, and the energy index rose 3.9% over the month.

Food prices were up 0.2% in February and rose 3.6% over the last 12 months. The index for fresh fruits increased 1.8%, the largest increase in that index since March 2014. But the index for dairy and related products declined 0.2% in February after falling 0.4% the previous month.

Some other highlights from the report:

- Apparel prices fell 0.7% and are now down 3.6% year over year.

- The index for used cars and trucks dropped 0.9% in the month but is up 9.3% year over year.

- Shelter costs increased 0.2% in the month and are up 1.5% for the year. But keep in mind that eviction moratoriums are holding down rent costs. That could change in coming months.

- The cost of medical care services increased 0.5% and are up 3.0% year over year.

- The index for airline fares continued to decline in February, falling 5.1% following a 3.2% decrease in January.

Here is the overall trend for all-items and core U.S. inflation over the last 12 months, showing the deep decline after the pandemic erupted in March 2020, and the gradual climb higher in all-items inflation, even as core inflation has remained relatively stable:

What does this mean for TIPS and I Bonds?

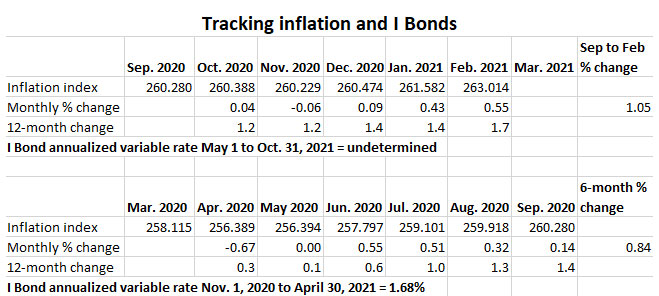

Investors in Treasury Inflation Protected Securities and U.S. Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances on TIPS and set future interest rates for I Bonds. For February, the BLS set the inflation index at 263.014, an increase of 0.55% over the January number.

For TIPS. February’s inflation report means that principal balances for all TIPS will increase 0.55% in April, following a 0.43% increase in March. This is welcome news for TIPS investors, but keep in mind that in this case, non-seasonal adjusted inflation was slightly outpacing adjusted inflation, and eventually those numbers will balance out over a year.

Here are the new April Inflation Indexes for all TIPS.

For I Bonds. The February report was the fifth in a six-month series that will set the future inflation-adjusted variable rate for U.S. Series I Savings Bonds. At this point, five months in, inflation has increased 1.05%, which translates to an annualized variable rate of 2.10%, higher than the current rate of 1.68%. Because gasoline prices are continuing to rise in March, we should see that variable rate climb even higher. But … inflation is highly unpredictable.

After the March inflation report, to be issued April 13, we will then know the I Bond’s new variable rate. I’ll have more to say about this after that report, but here’s a hint: I Bonds are going to be a very attractive investment in our current low-interest-rate environment. Could they get as popular as Bitcoin? Er …. no.

Here are the numbers, with one month remaining:

What does this mean for future interest rates?

The weaker-than-expected core inflation numbers give the Federal Reserve a lot of leeway to continue easy money policies, but those policies were going to continue anyway, no matter what this report said. I am expecting short-term interest rates to continue at near zero through 2021. Longer-term interest rates have been rising recently, but this report shouldn’t push them higher.

Inflation should rise at a higher pace in the next few months, as gas and other prices continue climbing, and the Fed knows this. It won’t be a surprise. Inflation numbers for March, April and May will be compared with very weak numbers from a year ago, so “surprisingly high” increases seem likely, and won’t actually be a surprise.

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Just thought I’d throw this out there:

Because the CPI-U is used unseasonalized (for I-Bond purposes) and yet is quite heavily influenced by seasonal factors, it is often possible to use those seasonal factors to make stronger statements about what the reasonable range of sixth-month effects might be (once the first five months are known) because seasonality explains a lot of the variance. I have used this idea with some success in the past.

I’d be interested in hearing more about this. The seasonal versus non-seasonal factor definitely affects sales of shorter-term TIPS, and can slightly skew 5-year TIPS auctions.I think the next six months (after March) are going to be extremely difficult to predict. The summer is always zany, inflation-wise. All-items inflation year over year is highly likely to soar in the next few months, just because of the suppression of prices a year ago because of the pandemic. Then you add in hurricanes, turmoil in the Mideast, etc.

On March 20, 2017, in a comment on your SA post “Inflation Rose 0.1% in February…”, I noted:

“I looked at the data going back to 2006 and—even though there were extended deflationary cycles within that period—March unadjusted CPI-U has never been below February unadjusted CPI-U.”

Well March<February happened for the first time (since 2006) last year (pandemic), but it remains true that unadjusted inflation tends to run *above average* between February and March. In the 61-month period from Feb 2015 to Mar 2020, average monthly unadjusted CPI-U rose 0.163%, but the average of the six monthly increases from Feb to Mar in each of those six years was 0.280%. Go back to 2010 and it’s 0.158% overall (121 months) vs. 0.430% Feb to March (average monthly increase over the 11 years).

This is—of course—a gross oversimplification of a complex subject. And pandemic exit effects loom large at this time. But naively, it is reasonable to assume that the March 2011 unadjusted CPI-U number will likely show an increase over February that is greater than 1/12 of the annual inflation rate.

I bought an I-bond in January. Did I buy too soon?

I also bought my full allocation in January, and I feel fine about it. It means you’ll get 1.68% (annualized) for six months and then 2.0% (possibly less, more likely more) for six months, for a combined interest rate of 1.8%+. I’m happy with that. The only way the “too soon” issue arises is if the Treasury raises the I Bond’s fixed rate above 0.0% later this year, which seems very unlikely.

Thanks for explaining.

Thanks for posting this. Although I was expecting a positive print I had hoped it would actually be larger. I need to study what they use in their formulas and how they weight the categories. Certainly fuel costs contributed less than I thought. My spot check last month throughout the country indicated much higher than the 6.9% they said happened.

The Texas winter event driving up natural gas, electricity and gasoline prices in a big way before February ended. Locally, gasoline is up almost 20% since the beginning of February. On a monthly basis I seem to have nearly always lived in places that seem to have higher inflation than the Fed posts. My bad…