By David Enna, Tipswatch.com

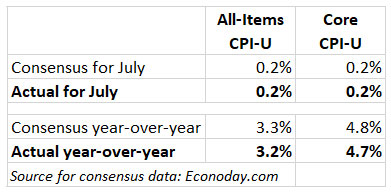

Markets got fairly positive news today with the release of the July inflation report: The Consumer Price Index for All Urban Consumers rose 0.2% on a seasonally adjusted basis, the Bureau of Labor Statistics reported. Over the last 12 months, the all items index increased 3.2%.

Core inflation, which removes food and energy, was also up 0.2% for the month and now has increased 4.7% over the last year. Both annual numbers came in slightly below expectations.

While annual all-items inflation ticked higher from last month’s 3.0%, that was expected because of deflationary numbers a year ago. So markets are likely to greet this inflation report as a positive sign that inflationary pressures are continuing to decline.

The recent rise in gasoline prices wasn’t fully reflected in this July report, with gas prices rising just 0.2% in the month and down 19.9% over the last year. Gas prices are likely to be a much larger factor in August’s inflation report.

The BLS noted that shelter costs were by far the largest contributor to the monthly all-items increase, accounting for more than 90% of the increase. Shelter costs were up 0.4% for the month and 7.7% over the last year. Here are some other highlights:

- The costs of food at home rose 0.3% in July and are up 3.6% year over year.

- The natural gas index increased 2.0% over the month, following five consecutive monthly decreases.

- Costs of motor vehicle insurance also increased 2.0% in July.

- Costs of used cars and trucks fell 1.3% for the month and are down 5.6% over the last year.

- Costs of new vehicles also fell slightly, down 0.1%.

- Costs of medical care services fell 0.4% and are down 1.5% over the last year.

Overall this looks like a fairly mundane inflation report, with few examples of exaggerated increases or falls. Here is the trend in all-items and core inflation over the last year, showing a steady trend lower, despite the uptick in all-items inflation:

What this means for TIPS and I Bonds

Investors in Treasury Inflation-Protected Securities and U.S. Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances on TIPS and set future interest rates for I Bonds. For July, the BLS set the CPI-U index at 305.691, an increase of 0.19% over the June number.

For TIPS. The July inflation report means that principal balances for all TIPS will increase 0.19% in September, after rising 0.32% in July. Here are the new September Inflation Indexes for all TIPS.

For I Bonds. July’s inflation report is the fourth of a six-month string that will set the I Bond’s new variable rate, which will be reset on November 1 based on inflation from April to September. So far, with two months remaining, inflation has increased 1.28%. Based on current trends, it looks like the new variable rate could be in the range of 3.2% to 3.4%, but two potentially volatile months of data remain.

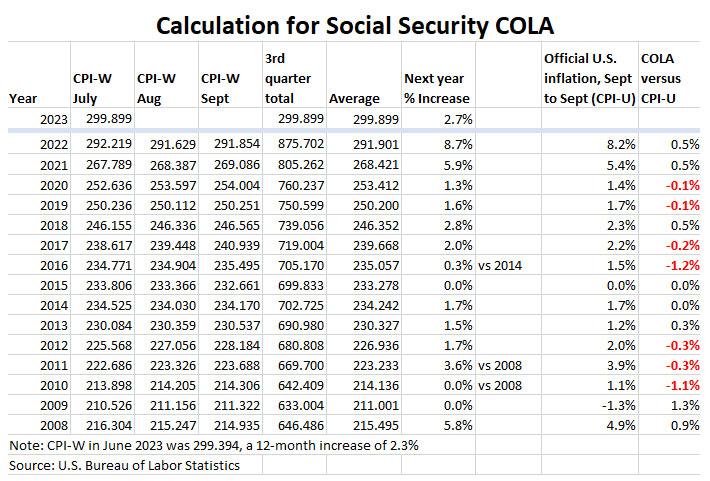

What this means for the Social Security COLA

The Social Security Administration uses a different inflation index — CPI-W — to determine the next year’s cost-of-living-adjustment. And it looks only at the average of three months of data, from July to September. For July, the BLS set the CPI-W index at 299.899, an increase of 2.6% over the last year.

For the COLA, the only 2022 number that matters is the three-month average from July to September 2022, which was 291.901. July’s CPI-W index was 2.7% higher. Two months of data remain and I have been projecting an increase in the range of 3.0% to 3.2%, which still seems on target.

What this means for future interest rates

This was a positive inflation report, although it didn’t fully reflect the recent surge in gasoline prices. Both annual all-items and core inflation came in slightly lower than expectations. I’d say all of this gives the Federal Reserve some room to pause near-term increases in short-term interest rates. Could the July increase end up being the last?

Bloomberg’s report this morning called this inflation report “subdued,” a good word. The Wall Street Journal noted the uptick in all-items inflation, but predicted the Fed would now consider holding rates steady:

The core CPI, in particular, could encourage the Fed to hold its benchmark interest rate steady at its September policy meeting. The new numbers lower the three-month annualized rate of core inflation to 3.1%, the lowest such reading in two years.

It’s good to look back on an amazing year in the U.S. economy. In June 2022, annual inflation peaked at 9.1%. At that time, the 4-week Treasury was yielding 1.21%. Today, the 4-week yield is 5.51% and inflation has fallen to 3.2%. I’m going to give the Fed credit for sticking with this difficult inflation fight.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I’ve read that you decided to utilize the gift box strategy to purchase IBonds later this month. I’ve also seen that you have speculated that the fixed rate may increase at the next reset. Understanding that the window opens up again in January for new purchases and you may be planning on utilizing the gift box strategy again come November but is there any particular reason as to why you didn’t wait until Nov for the possible higher fixed rate? I have yet to make any purchases this year and am debating on now vs November given real yields and the possible higher fixed rate. Plan to hold long term….Any opinion?

UPDATE: After thinking this over, I decided to cancel the late August purchase and delay it at least until October. As you noted, it probably makes sense to see the mid-October conditions before making a decision. It may be wiser to wait until November.

True I bonds are taxed but at least you can defer the taxes for up to 30 years if you keep them to maturity. I think that the idea of I bonds is not wealth creation but liquidity (better than TIPS) and inflation protection. (generally not as good as TIPS)

If you time horizon is 30 years, you might as well invest in an index fund.

I never said that.

However, a balanced approach to investment has 3 buckets (one of them is cash or cash equivalents) Another is Stocks and the third one is fixed income.

Where do the Ibonds fit? Its just a cash equivalent to me. Only have two buckets, stocks and everything else.

Cash or cash equivalent. After 15 months they are very liquid.

No matter how high the fixed rate will be, I-Bonds are still taxed as you must keep them at Treasury Direct. Much better is to buy TIPs in a Roth IRA.

Our Roth IRAs are 100% in stock index funds because that will be the last money we’d spend. I buy TIPS now in a traditional IRA, and the money will be taxed when withdrawn (including state income taxes). An I Bond is also tax deferred and won’t be taxed at the state level. In my case, I Bonds have a slight advantage when it comes to taxes.

You do it all wrong. Stock should go in a Traditional IRA, TIPS in a Roth IRA.

Or even better yet, index fund in a 401(k), TIPS in a Roth IRA (after conversion).

I have some TIPS in my Roth but I wouldn’t want to have only TIPS in the Roth. I don’t see TIPS as a particularly aggressive investment to maximize the benefit from a Roth.

If that’s the way you want to go, fine. Stock funds are already tax advantaged, so I go with fixed income in the traditional IRA, stocks in taxable accounts.

In all honesty, it really depends on your personal situation.

If you are still working and have access to a 401(k), then that would be your number one investment account. Depending on your salary you could have access to a Traditional IRA or Roth IRA as well.

For those that are retired, the options and strategies are probably different.

He is not doing it all wrong. You will never pay taxes again on Roth account, you should seek the highest growth possible, stock index fund is perfect.

On the other hand you will be pay income tax on trad IRAs (20-30%) so if you must hold fixed income (most of us should) and trad IRA is a great place to do so.

I you only had a Roth IRA, what would you invest in: index fund or TIPS?

I have I bonds in my cash equivalent taxable bucket for probably heirs. All IRA generation for me. Conversion makes no sense for me.

I will exit all I bods as soon as the interest rate of 6.49% finishes for them. I still have a bit of April 23 and May 23, but I will not buy more, unless the fixed rate goes at least to 1.0%. David have you thought about explaining FRN’s as an inflation protection investment?

So you’re okay with a 1% fixed rate, but not the current 0.9%? On a $10K I-Bond purchase the difference is $10/year.

I bought a fair amount when the fix rate was 0.9% I’m just not buying more at that rate. My time horizon is not a couple of years and I don’t see I Bonds/ Tips as wealth creation but as a defense against inflation. They are a component of my investment not _my_investment.

I got some old fixed 3%, Ill keep em. These are not trading vehicles

Are real rates still in an up-trend, indicating the Nov 1 fixed rate for I Bonds is likely 1.00% or more????