Do you believe inflation will average more than 2.12% over the next 5 years?

By David Enna, Tipswatch.com

The U.S. Treasury on Thursday will offer $21 billion in a reopened 5-year Treasury Inflation-Protected Security, CUSIP 91282CKL4.

The result will be a 4-year, 10-month TIPS with a coupon rate of 2.125%, which was set by the originating auction on April 18, 2024. The auction size of $21 billion is the largest for any 5-year TIPS reopening in history, up from $20 billion in December 2023 and $19 billion a year ago in June 2023.

I was a buyer at that originating auction, which generated a real yield to maturity of 2.242%, the 2nd highest at auction in 15 years for any 4- to 5-year TIPS. As of Friday, CUSIP 91282CKL4 was trading on the secondary market with a slightly lower real yield of 2.12%.

What makes this auction interesting is the sudden shakeup of both real and nominal yields, triggered by a soft inflation report released Wednesday. That report caused speculation the Federal Reserve would cut interest rates several times in 2024, but then the Fed tamped down the euphoria with a prediction of “one … or maybe two” rate cuts this year, depending on the data it sees. This set off a shakeup in bond yields:

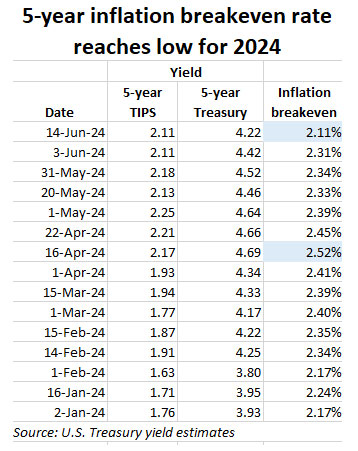

- Nominal. On Monday, the 5-year nominal Treasury note closed with a yield of 4.48%, which fell to 4.22% by Friday, a drop of 20 basis points.

- Real. The 5-year TIPS real yield closed Monday at 2.21% and fell to 2.11% at Friday’s close, a drop of only 10 basis points.

The difference means the 5-year inflation breakeven rate — a measure of future inflation expectations — fell by 10 basis points in a week. And in fact, the breakeven rate of 2.11% hit a low for 2024. I heard a commentator on Bloomberg this week mention the “collapse in breakevens” as a significant event. I wrote about this wild yield trend back on June 9: Read that here.

A lower inflation breakeven rate indicates a TIPS is “cheaper” as an investment versus the nominal Treasury of the same term. Here is the trend in the 5-year inflation breakeven rate so far in 2024:

In just two months, expectations for inflation over the next five years have fallen 41 basis points. That is a remarkable move lower, and potentially makes the 5-year TIPS an attractive investment when measured against a nominal Treasury.

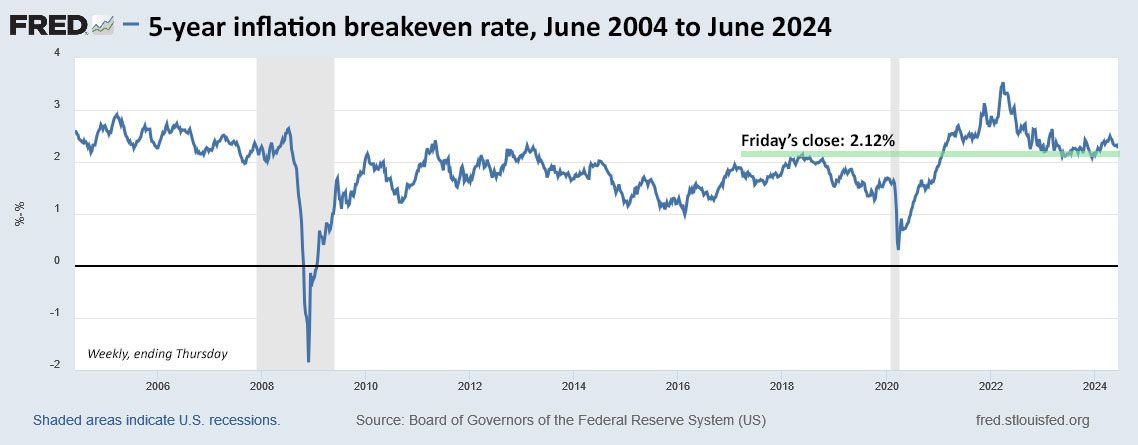

Here is a 20-year look at the 5-year inflation breakeven rate, showing that 2.12% is in a historically high range, but well below recent trends. In my opinion, the risk of under-performance for this 5-year TIPS (versus a nominal Treasury) is small.

The real yield

CUSIP 91282CKL4 trades on the secondary market, and you can track its real yield on Bloomberg’s Current Yields page, which updates in real time. It closed Friday at 2.12%, just slightly below the coupon rate of 2.125%. Here is the trend in 5-year real yields over the last 20 years:

A lot can change this week, especially with the high volatility we’ve seen in the last month. Just based on reasonable inflation expectations, it seems like the yield should be more in the range of 1.95% to 2.00%. That’s not a prediction, just an observation.

Pricing

Bloomberg shows a price very close to par value, 100.02, given that the current real yield is close to the coupon rate of 2.125%. This TIPS will have an inflation index of 1.01332 on the settlement date of June 28. So that leads to this estimate of the potential cost of $10,000 par at auction:

- Par value: $10,000

- Principal purchased: $10,000 x 1.01332 = $10,133.20

- Cost of investment = $10,133.20 x 1.0002 = $10,135,23

- + about $43.54 of accrued interest.

This calculation is an estimate and is highly likely to change in the next week.

Thoughts

It will be interesting to see if the real yield of this TIPS holds above 2.0% over the next week. It could be that bond-market turmoil left real yields a bit out of sorts on Friday. Or … investors really have decided that inflation could average less than 2.12% over the next 4 years, 10 months. If yields hold, this TIPS is attractive versus the nominal Treasury.

Last week, you could find best-in-nation 5-year bank CDs yielding 4.50%, which moves the inflation breakeven rate up to 2.38%, a more reasonable number. But we could see those bank CD rates fall if the downward Treasury yield trend continues.

I won’t be a buyer because I already own this TIPS and the 2029 rung of my TIPS ladder is fully stocked. If you are considering a purchase, watch Bloomberg’s Current Yields page during the week. The 5-year quote there is for CUSIP 91282CKL4. (And of course you can buy this TIPS at any time on the secondary market.)

This TIPS auction closes Thursday at 1 p.m. EDT. Non-competitive bids at TreasuryDirect must be placed by noon Thursday. If you are putting an order in through a brokerage, make sure to place your order Wednesday or very early Thursday, because brokers cut off auction orders before the noon deadline.

I will be posting the auction results soon after the close on Thursday. Here is a history of auction results for this term over the last 7 years:

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• Upcoming schedule of TIPS auctions

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Pingback: 5-year TIPS reopening auction gets a real yield of 2.050% | Treasury Inflation-Protected Securities

David, thanks for your though-provoking post. I was seriously considering placing an order for this TIPS today, but I decided to purchase a Federal Home Loan Banks 7-year 5.62% bond instead that’s call protected for one year. I expect this will be called next year once interest rates decline. One of the main factors for me was that I have a sizable amount of I-Bonds with 2028 to 2031 maturity dates. Thanks.

Those are the “dream” I Bonds. A fantastic asset over the years. Plan for the taxes, though.

I have never bought GSE bonds myself but have been looking into them lately. Will love to get your take on them. They do provide higher interest, and yes many of them are callable. But if I can get high rate for 3,6, 9, or 12 months and are then called, I am good with that. In fact, they may be even better than US bills. Back in 2007-8 financial crises, my portfolio was maanges by a so called “Boutique Financial Management Shop” and they had a lot in GSEs and did not work out well. I know GSEs are not like Treasuries and are not FDIC insured but they are almost top rated. Your thoughts will me most useful for me…thanks!!!

I don’t invest in these and I don’t track them carefully. For my individual bonds and CDs, I want “ultimate safety.” The callable issue doesn’t bother me, though, if the yield you get is high enough for the initial period.

thanks!!

Federal Home Loan Bank, Federal Farm Credit Bank and Tennessee Valley Authority GSE bonds are AAA-rated and state tax exempt. While they are not explicitly backed by the U.S. Government, and therefore may not be as safe as FDIC insured CDs, Treasury bonds or U.S. Savings bonds, many people think they have the implicit backing of the Federal Government. That said, we have 1/4 of our financial assets in GSE bond ladders and the rest in home equity, FDIC/NCUA insured CD ladders and I-Bonds, nothing in stocks. 57% of our GSE bonds and CDs are in a Roth IRA ladder; 38% in a Traditional IRA ladder; and 5% in taxable account ladders. 2/3 of our taxable account funds and 1/3 of our Roth IRA CDs are in no-penalty CDs. So, we have a lot of liquidity, fixed income diversification, plus tax diversification. I’ve decided that we could survive an unlikely problem with GSE financial stability since it only makes up 1/4 of our assets, especially with their AAA-rating and implicit Federal Government backing. I don’t think the Federal Government would sit by and watch the TVA go out of business, but if they do, we’ll still be OK.

Thanks much for your perspective and sharing asset percentages in your portfolio. The fact that 1/4 of your portfolio is with GSEs speaks to your comfort with them, I am going to add them in my fixed income part of the portfolio. You are the second person on this blog who has shared the fact that you do not have any stocks. The other person, sorry I don’t remember his name, has 100% of his portfolio in US Treasuries. I will be 68 in August and have a lot in stocks for growth (hopefully), but I am tempted to further stabalize and simplify our portfolio, especially for my wife of 40+ years, who has very little interest or patience for managing finances. I have been working on engaging her more. Thanks again for your response!!!

Note: Bloomberg 5-yrTIPS quote not using 91282CKL4 but rather higher coupon, higher yield, issue that also matures 4-15-29. CNBC is tracking the 2.125 TIP. https://www.cnbc.com/quotes/US5YTIPS

When I look at Bloomberg’s listing here: https://www.bloomberg.com/markets/rates-bonds/government-bonds/us I see a 5-year TIPS with a coupon rate of 2.13% (rounded from 2.125%) so that is the correct TIPS. It shows the real yield as 2.13% (also rounded) at 12:11 pm while CNBC shows 2.142% at 12:15 pm. It’s the same TIPS but it looks like the CNBC number isn’t rounded and is updated more quickly.

There is another TIPS that matures on April 15 2029 but it is a long-ago issued 30-year with a coupon rate of 3.875%. (I own that TIPS in a taxable account, purchased at auction in 1999!)

Hi David, are my assumptions correct? If I get 10K of the upcoming 5-year TIPS to hold to maturity and the coupon rate is 2%, and inflation in the next 5 years is 2% per year, should I expect the following:

I realize the upcoming TIPS auction is for 4 years and 10 months. Just rounding up for simplicity.

This is approximately correct. Keep in mind that the coupon rate of 2.125% will be paid on rising principal, as long as inflation rises, so that amount would grow over time. Plus, the accrued principal will also rise and compound, so that number also will likely be larger.

Thank you, David. I got inspired by you to learn how TIPS work. I think I am finally ready to jump in. It seems the yield fell down from 2.12% to 2.07% in the last couple of days. I hope it doesn’t dip below 2% tomorrow at the time of the auction. Do you still find this TIPS attractive with what we know today?

Anany, don’t focus too much on the decline in the real yield. At this point it is minor and any real yield above 2% is historically attractive. But of course things can change on Thursday.

I’m coming around to TIPS but I don’t fully understand them enough to jump in. I’m 70, retired, and 100% fixed income (MM, CD, Treasuries). My Social Security covers 50% of my expenses, so wouldn’t that mean I have adequate inflation protection? Many thanks for your updates and explanations for all these years!

TIPS aren’t for everyone. They are an investment aimed at capital preservation, to preserve buying power over time. You have a nearly risk-free portfolio, but it may or may not grow enough to match U.S. inflation. That is your one remaining risk. Social Security’s COLA definitely helps, and we can all hope benefits won’t be slashed in the future.

Thank you for your response! I use New Retirement software for long-range planning. I have inflation assumption set at 4% (pessimistic) and 2% (optimistic). Does that seem realistic to you? My annual expenses are 20k. The software indicates that even if I only made 3% interest rate on my portfolio, and with those assumed inflation rates, I’d have an 84% chance of having $ to leave my kids if I pass at age 83 (which I chose because of cancer history). Maybe I’m being naive about the effects of inflation? Thank you!

Reader in CA, I feel like an inflation range of 2% to 4% looks highly plausible. But you never know.

Also possibly noteworthy: the low end of the real yield curve has been inverted since roughly early May.

Whatever an IYC is supposed to mean….

Real yields have often been inverted since September 2022. For some reason, the 10-year TIPS tends to have the lowest yield, and then the 20-year was often higher than the 30-year. The 30-year moved to the top in Dec. 2023 and has continued to be highest, by a bit.

Question is whether the Fed will 1) allow inflation to gyrate and continue (1970s) or 2) raise rates to curb inflation (and the economy) as done in the 1980s.

If 1), then own TIPS; if 2) rollover 30-day notes (bonds, stocks, TIPS get crushed)

For ref – Federal Reserve Act as amended states: “…promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates.”

Also, how politicized vs independent is the Fed?

My money is mostly on #2 with some hedging via TIPS/I-bonds. I see zero case for me to own nominal bonds. Not sure if our blog author owns nominal or not.

Yes, as I have often noted, I do own “some” nominal Treasurys and CDs maturing in less than 5 years. And in our household’s combined portfolio, we use total bond fund as a core holding in traditional retirement accounts.

Looks like a good opportunity to me as well. Highest 5 year CD at Vanguard brokerage today ( 16 June) 4.45 % . Happy Father’s Day

Sent with Proton Mail secure email.

I ended up grabbing a 4.80% 5-year CD on Friday from the Bank of Montreal’s (BMO) new online bank- BMO Alto.

That is attractive, in my opinion.

Fidelity has a nice calculator that shows tax-equivalent yields based on security type. I find it useful when comparing yields from different security types.

https://digital.fidelity.com/prgw/digital/taxyieldcalc/

I’ve been reading your commentary on iBonds and TIPS for years, and it’s been incredibly useful. I did purchase this 5-year TIPS in the April auction and more in the secondary market on 6/10 (I believe real yield then was 2.174), but I might buy again this week. I’ve been wondering, though, how you determine when one rung of your TIPS ladder is full. Naturally, I’m not looking for dollar figures, but do you aim for a percentage of a projected year’s expenses? Or do you use part of that 15% target of the portfolio total mentioned in your 6/3 post and pro rate that over a certain number of years (you said the 15% included iBonds). This is my first RMD year, and info along these lines would be very helpful. Thanks!

I have my ladder set up with two things in mind: 1) Fairly equal amounts maturing in each year through 2043 that should come close to matching needed RMDs beginning in 2026, but with a larger amounts maturing in 2033 and 2034 because of the TIPS gap years, and 2) I have some nominal Treasurys and CDs mixed in through about 2028, with the idea of getting new 10-year TIPS maturing in years 2035 to 2039, if real yields remain fairly attractive. This is all in a traditional IRA account and is backed up by investments in Vanguard Wellington and Total Bond fund, which I could also use to pay RMDs or give to charity.

Thanks for those details. Much appreciated!

Yes, thx … money and mouth are aligned (as we knew)!

Sounds like limited funds in limited-duration nominal bonds awaiting the move to TIPS. I like it.

I like the predictability of nominal Treasurys (and CDs) of less than 5 years, even if I might give up a little inflation protection.