By David Enna, Tipswatch.com

We knew this day would come, after enjoying 5% nominal yields on very safe investments for more than a year. But that era ended Wednesday when the Federal Reserve cut its federal funds rate by 50 basis points, to a range of 4.75% to 5.00%.

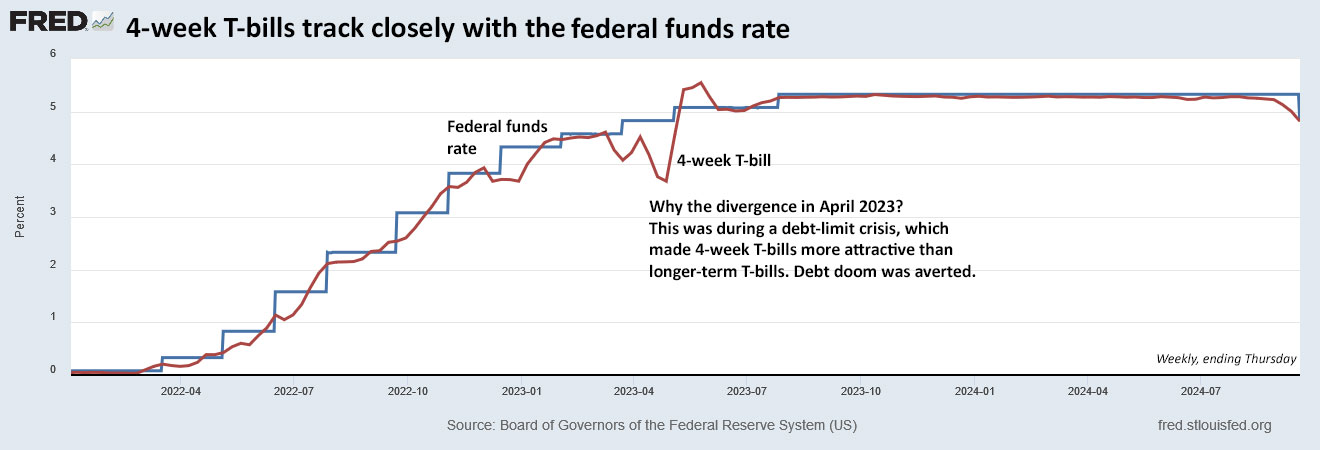

Today, the effective federal funds rate is 4.8%, and that means almost all safe investments already have or will soon follow the trend below 5%. Look at this chart to see how the 4-week Treasury bill — the base rate for Treasury money market funds and high-yield savings accounts — follows closely with the federal funds rate.

The yield on a 4-week T-bill hit a 2023 high of 6.02% on May 25, 2023, and then a 2024 high of 5.56% on May 24. Thursday, it reached the low for the year, 4.87%. And that yield will continue to decline as the Federal Reserve embarks on a course of rate cuts, probably through much of 2025.

For me, 5% is a magic number. When I was young, my neighborhood Savings and Loan offered a passbook savings account paying a flat 5% and that continued for years. This was the “routine” yield on savings in the 1960s. I remember an episode of the Beverly Hillbillies where banker Mr. Drysdale yelled out, “We’re holding the line on 5% interest!”

I was probably the only kid in America who laughed at that line. More proof I was, and still am, a nerd.

The trend is down

Over the last couple years, I’ve gotten a lot of feedback from readers who were choosing T-bills paying a nominal 5% over TIPS and I Bonds with inflation-protected returns. “Great choice,” I said, if your investment target is short term. But if the goal is longer term, “These rate won’t last forever.”

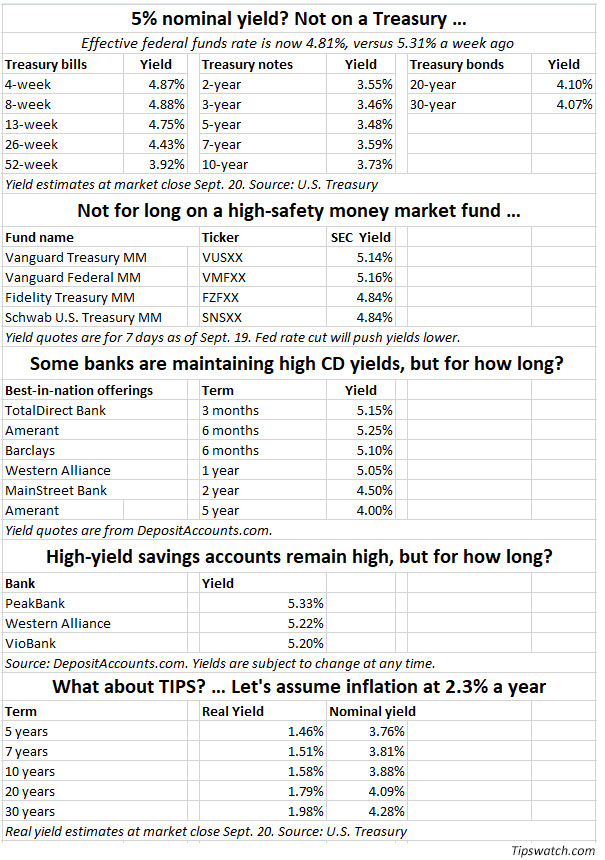

Here is a look at current yields of safe investment choices, both short- and longer-term. Yields across the board have already dropped below 5% or will soon get there.

A new strategy?

Instead of new strategy, maybe investors need new expectations.

“If you haven’t locked into a 5% yield yet, it’s probably too late for terms over one year,” said Ken Tumin, founder of DepositAccounts.com. “But 4%-plus mid-term and long-term CDs are still available. If interest rates keep falling, these too will soon be gone.”

Tumin advises looking for “add-on” CDs, which allow you to continue depositing money into the existing CD at its current rate.

“In addition to standard CDs at online banks and credit unions, there are a few 4%-plus add-on CDs and no-penalty CDs still available. Moving some cash into these can at least help you maintain 4%-plus yields for a few years into a low-rate cycle.”

I have been a strong proponent of investing in T-bills as part of a 2nd-level cash reserve, setting money aside to be used when needed. Back in July 2022 I suggested staggering investments in 13-week and 26-week T-bills, with some maturing every four weeks and then being rolled over. I followed my own advice and was able to ride T-bill rates from about 1.7% in 2022 to 4.87% on a T-bill I reinvested last week.

At this point, I don’t see any need to abandon this strategy. I need this cash reserve for potential spending in retirement, and I don’t want to increase risk in my portfolio. My potential returns will be smaller, but not drastically smaller for the next year, at least.

On the flip side, my core longer-term bond holding — the Vanguard Total Bond Fund ETF (BND) — has recovered nicely since the disastrous performance of 2022, when it was down 13.1%. BND had a total return of 5.66% in 2023 and is up 4.85% so far in 2024. It’s current SEC yield is 4.03%.

While short-term interest rates are almost certain to decline, there’s no certainty about longer-term rates. So there could be future opportunities to extend duration and lock in safe interest rates of nearly 4.0% — either with CDs or Treasury notes. The bond market has to settle down and adapt to the Fed’s actions.

This time around, most probably, short-term interest rates aren’t heading to zero. A more likely “neutral” level will be in the range of 3.00% to 3.50%. Annual U.S. inflation is currently running at 2.5%, and my goal as an investor would be to maintain yields above the rate of inflation. That should be possible over the next year.

Rather than extend my 3 year treasury bond ladder, I have switched to a bond fund (for example, VGSH, maturity 2 years, duration 1.9 years). As the trend of falling interest rates is clear (though not guaranteed) I might as well catch the upside of interest rate risk and add some capital gains on top of the yield.

The two year was a lackluster 3.520% today (Sept. 24). But maybe in a year that will look good.

This result was interesting, because I would expect the federal funds rate to be reaching 3.5% sometime next year, but then … will it go lower? The 2-year Treasury note often reflects the future of short-term rates.

I agree with your approach of using T-Bills as a second tier savings. As I get older I seek more simplicity in my portfolio, and am considering SGOV etf as an alternative. Any feedback/opinions? Are there any tax reporting complications (I.e. reporting tax-exempt income on state tax returns)?

SGOV is a fine alternative, recognizing that the share price gradually increases throughout the month until it discharges its monthly distribution at the end of the month. Thus, there will be a small capital gain or loss when you purchase or sell. No tax complications other than deducting the interest from US government obligations on your state tax return, as you would T-bills or Treasuries held directly.

SGOV is a 0-3 Month Treasury Bond ETF, so you won’t have Tax-exempt income, and the income from this should be exempt from a state income tax return. Many people opine that you are better off buying the treasury securities directly rather than a bond ETF, where performance will likely lag.

I have also had 5.5%+ callable CD’s being called… fortunately when CD rates were higher, I mostly stayed away from the “callable” CD’s and took a little cut on promised return for the fixed rates for 5 to 10 years.

One option not mentioned: Add more i bonds in the gift box before November. At the 2.3% assumed inflation in this post, that’s 3.6% nominal. This compares well to T-bills, favorably IMHO when you consider the <5 year flexibility. For me it is also competitive with CDs b/c of higher state taxes that take a bite out of CDs. There are limits to how deep you want to get into this strategy (you can only move so much out of the gift box each year). Close to 5 year TIPS, which are also of some interest to me.

Thoughts?

I agree on I Bonds, except this is more of a long-term investment because of the 3-month interest penalty on redemptions before 5 years. I may post some thoughts on this later this week, on rolling over low-fixed rate I Bonds to buy the current 1.3% I Bonds, for people who can use the gift box.

Finally, I caught up on reading over 40+ Tipswatch posts, certainly an exercise in joyful learning. Since the drop in rates, I have been looking for ideas beyond I Bonds, TIPS, CDs, and Treasuries, Whoever care to read my comments, most likely, they know that I am not a fan of buying bond MFs or ETFs, this inculdes BND. So far, I am considering the following (new for me) ideas:

I have never done 3. or 4. but have done a lot of reading and analysis. Yes, my goal is to never lose money on fixed income, so I tread for the fixed income part of our portfolio super super cautiously.

Your shared wisdom will be greatly appreciated…thanks!!!

Oh, and I got one coupon payment, which increased my total yield by .06 %🤷♂️

Amortization of the discount is 2.39% YTM based on first purchase, 2.19% based on last purchase price. Plus overcompensation of inflation – the purchase price was discounted by 46% on first purchase but the inflation adjustment is not discounted.

Here is an interesting “toy” going back to 1209 for UK data.

Inflation calculator | Bank of England

“Average” annual inflation comes out to 0.9% between now and back then.

But, the last couple hundred years seem to be higher than the first 600 years.

Of course, all this is pointless. What matters to most is what will the inflation do in 5-10-20-30-40 years – that is unpredictable.

2.3% is a reasonable assumption, but extremes are not impossible either.

Thanks for sharing this. Over 800 years, that’s a much lower average inflation rate than I would have guessed. Historically, periods of deflation were more common before the advent of modern central banking in the 20th century. Here’s an excerpt from a 2015 WSJ article:

From the U.S. Revolutionary War to World War II, inflation swung around much more dramatically than it does today. Especially in periods of war, prices would surge, to be followed by long periods of deflation. Over long periods of time, these dramatic swings tended to balance out, but it was a far cry from what anyone today would likely consider “price stability.”

One could argue that periods of deflation counteracting inflation surges actually creates better “price stability” in the very long term (decades to centuries). However, I can see how prices surging 10% annually, then falling by the same amount a few years later would seem erratic and unpredictable to the average person or business.

When David wrote earlier this year about the low risk of deflation, I commented that deflation barely registered on my list of concerns. While I still believe that high inflation is the much greater risk, I’ve started wondering if this is partly due to recency bias. It’s not inconceivable that significant technology and productivity gains from AI in the coming decades could cause an aggregate drop in prices even if the economy is still growing. The U.S. experienced a combination of economic growth and deflation in the late 1800s.

It’s hard to see this repeating in the modern era, though. A more likely outcome is that unsustainable U.S. fiscal policy could drive up inflation. As others have commented, climate change may also increase global inflationary pressures as commodity prices rise and population shifts create imbalances in supply and demand.

If there is some slight risk of deflation in the next 20-30 years, however, that would seem like a good reason to hold I Bonds over TIPS.

Justin,

Thank you for pointing out the differences between TIPS and I Bonds in deflationary environment. Got me thinking.

From that perspective CDs and regular Bonds might do even better – the deflation will be subtracted from fixed I Bond rate, but the rate will stay the same for the life of CD or regular Bond.

Five per cent we hardly knew ye. Didn’t stick around very long. It feels like a pay cut but one percent is not that meaningful to me and reaching for a point or two of yield in riskier products is usually a bad idea. I will just rummage around, looking under the (metaphoric) sofa cushions of my account, looking for funds that have not been efficiently deployed.

Interesting that the financial media, present company excepted, refuses to take what seemed like a pretty confident Fed at face value. Two columns in the WSJ today touted recession risks. One guy said the Fed is “flying blind”. The first person CNBC interviewed after the Fed decision was Jeffrey Gundlach, the current “Bond King”, who predicted recession. As he did in 2022. And in 2023. No mention that his funds which are doing well this year have a less than regal long term performance.

Re: your previous post on Bob Brinker and your stock portfolio. You might find this academic study interesting (https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4897069). They calculated compound returns for 29,078 common stocks from 1925-2023. The majority of stocks 51.6% had negative returns. Nvidia which you held led the 20 year return category but the overall winner was Altria (formerly Phillip Morris) which returned “265 million per cent” over 98 years. That’s $2.65 million dollars for a dollar invested in 1925. Not that that anybody alive has likely held the stock for that long but certainly a fun number to think about.

A few weeks back I suggested moving T bills to30 year treasuries for capital gains; wonder. if that worked? Additionally, I’m looking move tbills to high yield etfs, thoughts?

My first buy of 1/8 % coupon, 2052 TIPS are up 15% after holding less than six months.

Held in my IRAs so I do not have to pay taxes on phantom income from inflation adjustments.

Alan, your example shows the extreme volatility of 30-year Treasurys, which can work for you or against you. That 2052 TIPS has a duration of somewhere near 28, meaning a 100 basis-point swing in yield will push its value up or down by about 28%. Six months ago, a 30-year TIPS was yielding about 2.4% and earlier this week that was down to 1.84%, a drop of 56 basis points, which would swing the value of your TIPS higher by about 15%, as you reported.

And deliberately so.

Part of investing success is “Buy Low”. Each of my three groups of buys were during hours long spikes (I watched US30YTIP index every few hours, more often when it opened on Monday).

I felt this was a win-win investment, if I can hold through a future spike in inflation inside my IRA.

Case 1 – A future spike in inflation that sends YTM above 2.4%. But I get 170% to 185% inflation adjustments on my initial investment. 10% inflation sends my eventual payoff up 17% to 18.5%. Wait till inflation abates and YTM decline.

Case 2 – Inflation declines to 2% (I still get 3.4% to 3.7% inflation adjustment) and YTM declines. Capital gains as the YTM declines.

In both cases, I get a .125% coupon (inflation adjusted) 🤷🏻♂️ and the discount accrual adds value as 2052 approaches very slowly.

Only if the YTM increases without inflation increasing for as long as I hold my IRAs (75% in Roth, so no RMD for them) will this be a bad investment.

BTW, high discount TIPS are my first bond investment except for iBonds a few months before.

Before 2052, I do anticipate significant inflation from real world shortages (as opposed to monetary/fiscal caused inflation) due to Climate Change. I am looking for some protection from that. Although I also expect monetary/fiscal inflation as well before 2052.

“On the flip side, my core longer-term bond holding — the Vanguard Total Bond Fund ETF (BND) — has recovered nicely since the disastrous performance of 2022, when it was down 13.1%. BND had a total return of 5.66% in 2023 and is up 4.85% so far in 2024. It’s current SEC yield is 4.03%.”

If I invested $100,000 in 2022 (July) into BND and reinvested the dividends and interest what would BND be worth now? Thanks

I can’t do that calculation. If you did buy it and reinvested the dividends, what is your current total value? Morningstar reports annualized total returns, which were 10.8% over the last year and -1.68% over three years. By June 2022, BND had already fallen a great deal, so your returns are probably positive.

Your current value would be $106,925, which is an annualized 3.13%.

dividendchannel.com has a nice DRIP returns calculator that allows you to enter starting & ending dates, and compute with dividends reinvested or not.

DRIP Returns Calculator | Dividend Channel

David, I completely agree with your sentiment that there was something “magical” about 5% yields. When my father passed away six years ago, I found a bunch of financial files and newspaper clippings he had saved from the ’90s and early ’00s with banks advertising 5-6% interest rates. As a younger investor in my 30s, I remember thinking “wow, that was another era… will savers ever see rates that high again?”

Sure enough, 5% yields returned sooner than I expected, though only after the pandemic unleashed a frightening surge in inflation. Looking back at this rate-hiking cycle, I am pleased to have bought T-bills of every term with the highest auctioned yields of the past 20 years, the highest 5-year TIPS last October, and a 1-year bank CD paying over 6%. I also found a 15-month add-on CD with a 5% yield a couple of weeks ago.

My only regret was waiting too long to buy longer-term nominal treasuries. You never know when yields have peaked until they suddenly start to drop. Overall, though, I’m glad I can now sit back and relax as we enter a lower rate environment. Reading your blog these last few years has been tremendously helpful in guiding my fixed-income investment decisions (especially with I Bonds, which were the only game in town in early 2022). I always enjoy reading your articles and appreciate all of your “tips” and guidance.

If you’re buying brokered CD’s, be sure to check the secondary market. Fidelity has a nice selection. You can often pick up 30-40 bps (call protected) over new issues of the same maturity.

For taxable “cash”, I have been buying muni CEF’s at a discount yielding 6-7%. I think that is reasonably safe as long as rates are trending down.

I am a fan of brokered CDs because I don’t want to open additional accounts at new providers. Callable CDs are fine, as long as you like the yield through the first call date. I had a 5.3% CD due to mature on Dec. 15, but callable on Aug. 15, and of course on Aug. 15 it got called. I think a lot of CDs are going to be called in coming months.

Corporate Bonds are getting called as well. Most of us are probably guilty of not paying too much attention to whether any fixed income investment is callable, but now everything is getting called. Were learning our lesson.

I agree. When I was building my initial RMD ladder a few year ago, I didn’t pay much attention to the little “CP” notation. Learned my lesson, it’s a bit disruptive having to replace several corporates/CD’s.

I had some callable agency bonds because of the interest rate premium they pay. Of course they all got called over the past few weeks.

On my 6 mo journey from 1st T-bill to TIPS to munis a 6.5% farm bond was called 1 mo. after purchase, yielding only 2 wks interest from settlement. I then bought a 5.4%, paying attention that the 1st call was @1 yr, rationalizing that it’s like a tax eq. 6% CD. Thanks for validating that! The question is where to put this year’s payouts. Jennifer Lammer (who has quoted you) has discussed long term bonds in the case of a soft landing but if it’s a wartime recession are we doomed to sub-Drysdale returns and prospecting for Texas tea?

I agree that brokered CDs are less hassle, but the idea is to maximize one’s return. Direct CDs with banks, etc. are administered rates while brokered CDs are largely market rate determined. When rates were rising, brokered CD’s outpaced direct CDs. However, the advantage is now with direct CDs. I was just looking at 2 year offerings and direct CD are available at 4.5% APY while brokered have a 3 handle. Also, need to careful about APY Vs. rate when comparing; most brokered CDs do not reinvest interest, so your interest goes to your brokerage MMA, at a much lower rate.

I put about a third of my IRAs (@75% Roth) into high discount low coupon TIPS some months ago. Primarily 1/8% 2052 TIPS.

For every dollar I invested, I got 170% to 185% inflation adjustment – thus inflation protecting more of my portfolio.

Future inflation can come from monetary/fiscal policy or from real world shortages. I foresee both sources of inflation at elevated risk in the next decade. Arbitrary tax cuts that just balloon the deficit have been a consistent Republican policy since Reagan. Climate Chante and

System posted comment and I do not see how to edit

The direct effects of Climate Change and Climate Chaos plus the indirect effects – mainly more wars – will create real world shortages that will cause inflation.

If Trump is elected and enacts a 10% tariff on all imports with 30% on Chinese imports plus deports millions of workers, one result will be massive inflation. That is a certainty with the above policies.

With Harris, unlike Clinton, I do not foresee a budget surplus or even a major reduction in the deficit.

This year too hot weather is driving a shortage of orange juice (and snow crabs). The Panama Canal was short of water, reducing trade volumes.

Absent Trump, I do not anticipate significant inflation in the next few years, but I do before I drain my IRAs.

Hi alan-

I agree with everything you said, in the short term.

My preference for Trump comes from a belief that there is a small possibility that his policies will work out in the long term. There will be short term pain as prices go higher as we lose access to cheap Asian stuff. We’ll pay more for our electronics, more for our clothing, more for our cars. In the long run, however, there will be benefits. Our manufacturing will recover, we’ll have recovery of real jobs, there will be less need for expensive social welfare. The dollar will be expensive, but strong and might remain the global reserve currency. In short, over decades, the American economy will stop its slow deterioration and might even improve.

With Harris, it will be that last 3.5 years continued and compounded. We will continue to cripple our manufacturing segment with meaningless climate shackles, continue to weaken the dollar until it de facto loses its reserve status, continue to give people benefits that we do not fund. The inflation will have no chance of abating as we continue to eat our seed corn (e.g., current inflation moderating due in part to use of petroleum reserve to hold down gas prices). We are also at unknown but non-zero risk that some of the undocumented people that have entered over the past several years might do us real harm- infrastructure damage or terrorism, who knows what else.

We’re in for a rough decade no matter who is President, but return to at least some sound economic principles is better than current fecklessness.

Alan and Wtic, I am going to allow these two political comments because you both attempted to express moderate views. But please, no more comments focused on politics, which eventually leads to chaos.

Thank you for your forbearance, Mr Enna, and for writing this very useful blog.

I confess that I was not aware of a prohibition on politics related comments, and I will not do it again.

I read this blog due to my interest and large investment in TIPS, primarily as a way to insulate my retirement accounts from whatever things the people in charge of the government do to our economy.

Thanks….I was hoping for you to interve.

Thanks for the update. I guess it couldn’t last forever. I am watching the 10 yr and hoping it contintues to rise!

It’s always a pleasure getting sound advice from a nerd–particularly one who takes the best from all sources–even including rascals like Drysdale! Thanks-