But there is danger of an ‘outlier’ decision by the Treasury.

By David Enna, Tipswatch.com

It’s already Oct. 7 and we are closing in on Treasury’s November reset of the fixed and variable rates for U.S. Series I Savings Bonds.

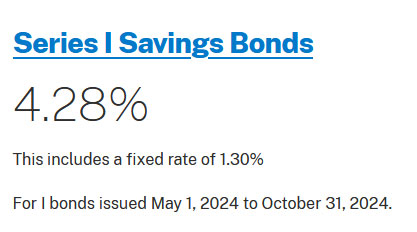

The current composite rate is 4.28%, which is calculated by combining a permanent fixed rate of 1.3% with a six-month inflation-adjusted variable rate of 2.96%. Both of those numbers will reset for I Bond purchases beginning November 1.

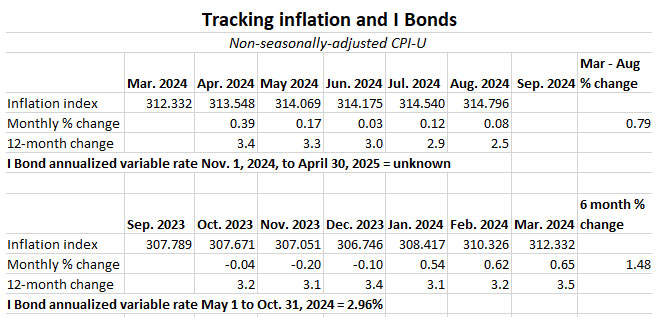

The variable rate. Thursday at 8:30 am EDT, we will learn the new variable rate, which will be set in stone by the release of the September U.S. inflation report, completing the March to September data used to set the rate.

For the months of April to August, non-seasonally adjusted inflation has run at 0.79%. It seems likely that September inflation will be around 0.1% (or possibly less) which would give a six-month total of 0.89% and result in I Bond variable rate of 1.78%. That’s a guess. We will know for sure on Thursday.

The key thing is that the six-month variable rate, which eventually rolls out to all I Bonds depending on the month they were purchased, will be significantly lower than current 2.96%.

The fixed rate. The Treasury does not disclose exactly how it determines the I Bond’s fixed rate, which appears to track at a discount to the real yield of a 5-year TIPS. This is the cryptic information it provides:

The Secretary of the Treasury, or the Secretary’s designee, determines the fixed rate. The rate is based on market rates that have been adjusted to account for the value of components unique to savings bonds. These include the early redemption put option, tax deferral feature, deferred purchase feature, and Treasury’s administrative costs.

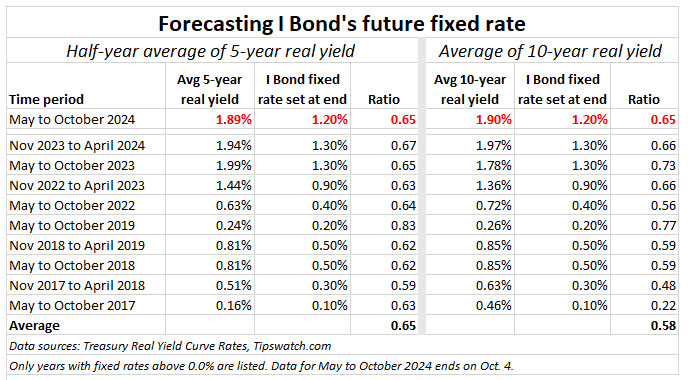

That statement makes it clear the Treasury examines “market rates,” and adjusts the I Bond’s fixed rate lower to account for the safety, tax-deferral and flexible maturity of I Bonds. I’ve tracked this decision for 13 years, and with the help of some Boglehead geniuses, I’ve settled on this predictive formula:

Take the six-month average of 5-year real yields and apply a ratio of 0.65.

I also look at the 10-year average, just as a back check. In this case, I am using the average of real yields from May 1 to Oct. 4, 2024. After applying the 0.65 ratio, the actual averages, so far, are 1.228619% for the 5-year TIPS and 1.235716% for the 10-year TIPS. The Treasury rounds the I Bond fixed rate to the tenth decimal point, or 1.20% for both these calculations.

You can see from the 5-year side of the chart that the ratio of 0.65 has been quite accurate, even for the November 2019 reset, when it appears the Treasury might have used a higher ratio to set the fixed rate at 0.20%. But it didn’t. The average of 5-year real yields was 0.24%. Apply a ratio of 0.65 and you get 0.156%, which rounds up to 0.20%.

So based on this data, which isn’t likely to change dramatically by the end of October, I’d predict that the I Bond’s new fixed rate will be 1.20%.

The tricky part

There is one thing I don’t know: Does the Treasury try to look forward to predict a trend in real yields? Based on the trend since 2017, when real yields have tended to move higher, it doesn’t look like it does.

October 2024 is an unusual case. The real yield on a 5-year TIPS dipped to as low as 1.41% on September 24. That is just 11 basis points higher than the I Bond’s fixed rate of 1.30%. Since then, however, in the aftermath of Friday’s positive U.S. jobs report, the 5-year real yield surged to close at 1.67%.

I follow real yields almost daily and here’s one thing I do know: You can’t assume to accurately predict the future. It is almost certain that the Federal Reserve will continue a series of short-term rate cuts well into 2025. But that doesn’t necessarily mean longer-term real yields will decline in lockstep.

Example: When the Fed announced a 50-basis-point rate cut on Sept. 18, the 5-year real yield closed at 1.49%. Today it stands at 1.67%.

So, in my opinion, the Treasury should not enter predictive mode and lower the I Bond’s fixed rate to adjust for potential future rate declines. That kind of decision would be an outlier and would be wrong.

I Bond strategy?

A new fixed rate of 1.20% would be a positive thing for I Bond investors, ensuring that this attractive rate would stay in effect for purchases through April 2025. The purchase cap resets on January 1, meaning everyone will have access to the new rate.

We will learn the new variable rate on Thursday, and it is likely to fall to a number around 1.8%, which combined with a fixed rate of 1.2% would translate to a composite rate of around 2.9% to 3.0%. Not exciting, for sure, but the key factor is the permanent fixed rate of 1.20%, which could end being quite attractive in 2025.

On Sept. 25 I posted an article about using the gift-box strategy to add to your I Bond holdings before the end of October. I am using this strategy, which I also used earlier this year, to lock in the 1.30% fixed rate. But it isn’t available to everyone, since it requires a trusted partner.

If the fixed rate remains at 1.20% into 2025, I Bonds will remain attractive as a way to build longer-term, inflation-protected and tax-deferred savings, with total safety.

Let’s hope the Treasury avoids the outlier route and sticks to its predictable formula.

• Considering an I Bond rollover? Do it the right way.

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I purchased the 5 year treasury at action on September 25, 2024. As you know, the coupon is 3.5% with the 5 year treasury now yielding 3.88%. How do you evaluate whether to sell the 5 year treasury in favor of allocating the funds, for example, to a more lucrative 5 year TIPS? Just trying to evaluate whether it is ever worth selling at a principal loss if I can get a better longer term yield someplace else. I also expect that the 5-20 year yields will be going up rather than down as the yield curve normalizes during the Fed’s lowering of short term rates. Thoughts?

This is impossible to answer, but I will say that my personal style is to buy Treasurys (mostly TIPS but some nominals) and hold them to maturity. Since Sept. 25, the nominal 5-year yield has jumped 39 basis points, so you will be selling at a loss. During that same time, the 5-year real yield has jumped 24 basis points, so a similar TIPS is now more expensive. (There is a 5-year TIPS auction coming up Oct. 24. I will be previewing that auction in an article posting Sunday, Oct. 20.)

Thanks! Yes, I am awaiting your preview of the Oct. 24 TIPS auction to see whether it makes sense to purchase.

Pingback: September inflation sets I Bond’s new variable rate at 1.90% | Treasury Inflation-Protected Securities

Thanks for the clear, well reasoned analysis. I recently made a gift box purchase for my grandson, a recent college grad. In order to receive his gift he must open a treasury direct account, and bide his time until next August when he can redeem it (or let it continue to grow). Hopefully he will pick up some knowledge about the bond world in the process. I will add that I learned a lot from small gifts of stock that my dad gave me. I especially learned about how basis clings to a gift!

It does feel like an opportunity to cash out more 0% fixed rate I Bonds, especially with low inflation making the three month penalty less significant. I had dropped a lot of the bonds that had passed their five year window in 2023 and may now drop some 0% bonds to rebuy and/or switch to TIPS.

When someone holding I-bonds in their gift box passes, do you know what happens to them?

If you die before granting the gift, the gift still belongs to the recipient, who has to claim it through TreasuryDirect.

The flip side of this is more complicated … if the recipient dies. If a second owner is named (which can’t be you) it would pass to the second owner. I am not sure of the way to add a beneficiary (beyond yourself), but read this … https://thefinancebuff.com/i-bonds-add-joint-owner-change-beneficiary.html

My wife and I have funded our gift boxes for planned deliveries out to Jan 2027. This past April we extended this out one more year so we could fund the purchase of $20,000 in fixed 1.30% fixed rate I-Bonds.

On the surface, I don’t think I would do this again, but then I keep second guessing myself thinking maybe I should?

The sudden reversal in nominal and real yields now has me second-guessing whether to buy more I Bonds through the gift box. Could we see an outlier scenario in which real yields move significantly higher next year with the economy growing more than expected, even as short-term rates drop? As much as 1.3% is an attractive fixed rate, I’m not entirely convinced it is the high-water mark for I Bonds in the medium-term. But maybe that’s just wishful thinking.

Real yields could definitely climb in the future, but most likely the fixed rate will be 1.2% or less through April. My thinking right now is to deliver one set of the 1.3% gift-box I Bonds in January, fulfilling the purchase limits for 2025. So then I would only have one set left. If the fixed rate climbs higher at the May 1 reset, I would consider adding another gift-box purchase.

The very low inflation rate is good for the overall economy and for stabilizing costs, so there’s that.

I realize you focus on the long-term accumulation of I Bonds but remember there are many of us who purchased I bonds as a short term investment when inflation spiked in 2021 and 2022. For this group, the low variable rate makes this a good time to redeem I bonds prematurely with a negligible interest penalty three months into the new rate.

That just seemed like it was worth mentioning as well.

I mention this often. I agree for short-term holders (and even long-term investors), I Bonds with low fixed rates are going to be unattractive when the variable rate drops to below 2.0% for six months. I wrote about the rollover strategy last month: https://tipswatch.com/2024/09/25/considering-an-i-bond-rollover-do-it-the-right-way/

You say “you can’t predict the future”. Actually you can predict anything you want. I think you mean most guesses about the future turn out to be inaccurate. Having said that “you can’t predict the future”, a lot of your article is about your prediction of the fixed rate (a mild lol). It’s a little like when people say “not to put a fine point on it” and then proceed to put a fine point on it.

I am not trying to be too pedantic, but you are an old newspaper guy. In fact, your guesses about future fixed rates have been remarkably accurate, whether based on a statistical model, your gut, or both.

As for me, I have more than enough in Ibonds and am not looking forward to 2031 taxes. I do enjoy calculating my tax deferred interest for each month, something I do twice a year, at the same time trying to forget about 2031.

The forecast of the fixed rate could be more than a guess *if* we knew the Treasury’s formula, for certain. But we don’t, so it will always remain a guess.

David, Do you think there is a single formula that doesn’t change over the years? Or does the Treasury redetermine it for each rate change? It seems remarkable that they have been able to keep this facet of the I Bond program confidential for this long.

I think Treasury settled on this formula possibly 10 years ago (if there really is a formula). It is similar to the formula that was used in the past to set fixed rates on EE Bonds, and may still be used today.

I agree that if the Treasury sticks to “Take the six-month average of 5-year real yields and apply a ratio of 0.65.” for the fixed rate, rates would have to shift dramatically (i.e. above 2.0% and/or below 1.0%) for that calculation to be anything but 1.2%. Though your caution that Treasury is not beholden to that formula is also accurate. I personally have rolled over some I-bond here in October thinking the fixed rate is unlikely to be this high in the foreseeable future.

I calculated what would happen if the 5-year real yield dropped to 1.2% for the next 18 market days (that won’t happen). If it did, the 0.65 ratio still ends up at 1.165%, which would be rounded to 1.20% for the fixed rate.

Yeah, I think you are right that its not likely to have a fixed rate this high in the foreseeable future. We’d have to go back 17 years to find a fixed rate that matches what we’ve seen in the last couple of resets:

https://www.treasurydirect.gov/files/savings-bonds/i-bond-rate-chart.pdf

Even with the current fixed rate, I still don’t want to buy any iBonds this month. Personally, I think a TIPS would be better for me if I wanted to buy more inflation protection (luckily, I got my fill around this time last year).

Also, thank you @David Enna for running this site and sharing all the knowledge found here.