Social Security COLA will be 2.5% for payments beginning in January.

By David Enna, Tipswatch.com

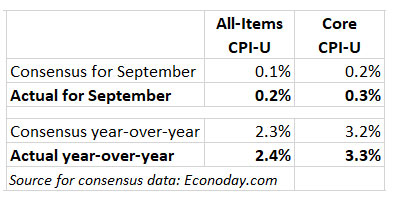

The September inflation report, just released by the U.S. Bureau of Labor Statistics, gives the final pieces of data to determine 1) the new variable rate for U.S. Series I Savings Bonds (it will be 1.90%) and the Social Security cost-of-living adjustment for payments beginning in January (it will be 2.5%).

Plus, the report may give stock and bond markets a bit of a jolt today, with inflation running at a higher-than-expected rate for both the all-items and core measurements. This news, combined with last week’s positive jobs report, could cause the Federal Reserve to scale back its planned cuts in short-term interest rates.

I Bond variable rate

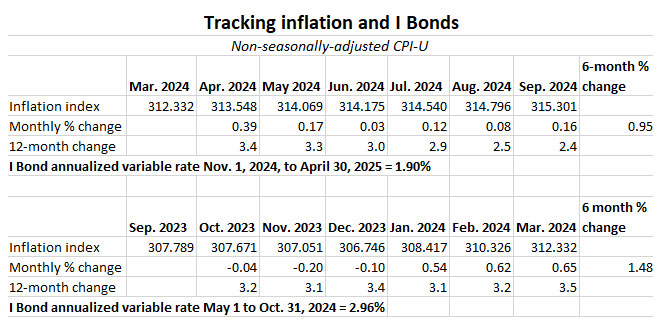

The September report provided the last month of a six-month string of inflation that determines the I Bond’s new variable rate, to be reset for purchases after November 1 and eventually rolling into effect for all I Bonds.

The BLS set September non-seasonally-adjusted CPI-U at 315.301, an increase of 0.16% over the August number. For the six months of April to September 2024, inflation increased 0.95%, which translates to a new variable rate of 1.90%, a sizable decline from the current rate of 2.96%. Here are the data:

The I Bond’s permanent fixed rate will also be reset on November 1, and seems likely to fall below the current rate of 1.3%. I have projected the rate to be 1.2%, but that is an informed guess. If the fixed rate is 1.2%, the I Bond’s new composite rate will be 3.11%, down from the current 4.28%.

Keep in mind that I Bonds purchased in October will lock in the 1.3% fixed rate and get a full six months of the 4.28% composite rate. If you were planning to invest in I Bonds in 2024, or to add to holdings through gift-box or trust strategies, you should make that move before the end of this month.

Opinion: A new variable rate of 1.90% combined with a fixed rate of 1.2% (if that happens) would mean I Bonds will remain an attractive investment into 2025. That is because a high fixed rate is the most important factor. However, older I Bonds with very low fixed rates (for example, 0.2% or lower) are going to have yields well below market rates, for six months at least.

Treasury Inflation-Protected Securities

Investors in TIPS are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances on these investments. The September inflation report means TIPS principal balances will increase 0.16% in November, after increasing just 0.08% in October. Here are the new November inflation indexes for all TIPS.

Social Security COLA

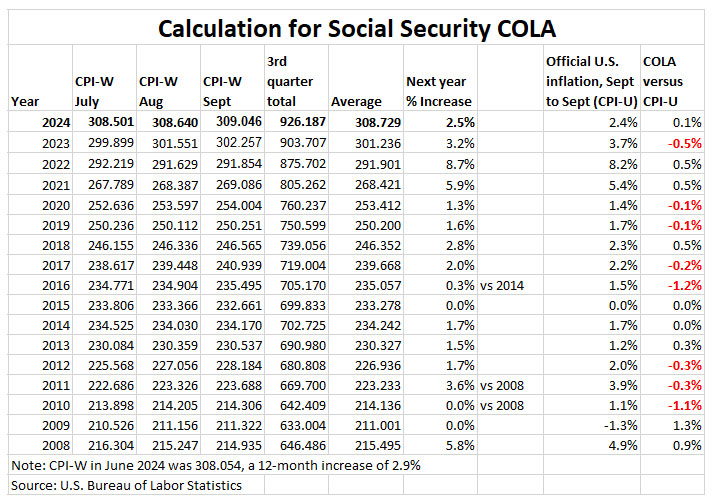

The September inflation report was the third of three — for July to September — that determine the Social Security Administration’s cost-of-living adjustment for payments in 2025. The SSA uses a three-month average of a different index, the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W), to set its COLA.

For September, the BLS set CPI-W at 309.046, which produced a three-month average of 308.729, an increase of 2.5% over the same average for 2023. That means the Social Security COLA will be 2.5% for payments beginning in January. The numbers:

The increase of 2.5% will be the lowest since 2021, but it is slightly higher than the overall increase in U.S. inflation over the last year, 2.4%. The 2.5% increase will boost the average Social Security payment by about $50.

This year, the average monthly benefit payment for retirees is $1,927, according to the Social Security Administration. After the 2.5% increase, that will rise to $1,976 a month.

The inflation report

I’ll be honest: I was not expecting U.S. inflation to come in higher than expectations for September. Gasoline prices fell 4.1% in the month and are down 15.3% for the year. But other factors offset that decline:

- Food at home prices increased 0.4% in September after being pretty tame for most of this year. The BLS said five of the six major grocery store food group indexes increased over the month.

- For example, the index for meats, fish and eggs increased 0.8% in September. And costs for fruits and vegetables were up 0.9%.

- Shelter costs increased 0.2% in September, down from 0.5% from August. But these costs remain 4.9% higher year over year.

- Costs of medical care services increased 0.7% for the month after declining the previous two months.

- Apparel costs were up 1.1% for the month.

- Costs of motor vehicle insurance were up 1.2% for the month and a disturbing 16.3% year over year.

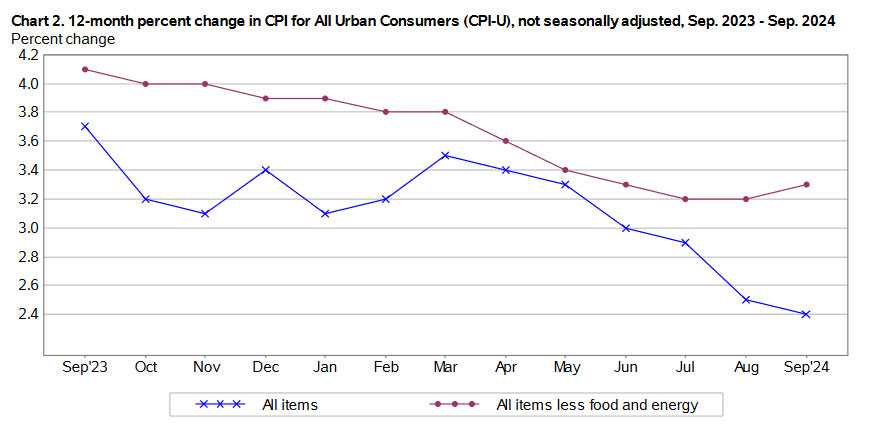

On the positive side, the overall annual inflation rate fell to 2.4%, the lowest level since February 2021. Here is the trend in annual all-items and core inflation over the last 12 months, showing that core inflation remains stubbornly high and in September actually trended higher:

The Federal Reserve

The combination of last week’s positive U.S. jobs report and this higher-than-expected inflation report should be giving the Fed jitters as it moves toward further cuts in short-term interest rates. I am pretty sure we won’t be seeing another 50 basis-point cut in 2024. From this morning’s Bloomberg report:

“Inflation is dying, but not dead,” said Olu Sonola, head of US economic research at Fitch Ratings. “Coming on the heels of the surprisingly strong September employment data, this report encourages the Fed to maintain a cautious stance with the pace of the easing cycle. The likely path is still a quarter point rate cut in November, but a December cut should not be taken for granted.”

I’d agree that a 25-basis-point cut is likely in November, and probably again in December. The Fed has room to move lower with annual inflation currently running at 2.4%. A neutral level for the federal funds rate could be around 3.5%, if inflation remains in this range.

The stock and bond markets seem to be taking today’s inflation news in stride, with the S&P 500 down only about 0.2% in early trading. Real yields have fallen slightly this morning, with the 5-year TIPS trading at 1.67%, down from 1.70% at yesterday’s close.

• Considering an I Bond rollover? Do it the right way.

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Pingback: New I-Bonds Estimated Rate: 3.11% APY (Variable + Fixed) - creditexpertbuddy.com

Is it just me or are the May 2023 .90 fixed rate I bonds not updated on the I bonds website. Couldn’t see any contact info on that site so I am asking here.

thanks

Not sure what you are seeing, but the Savings Bond Calculator shows the current value of $10,000 of May 2023 I Bonds at $10,532 (which reflects the three-month interest penalty). https://treasurydirect.gov/BC/SBCPrice … Eyebonds.info reflects the same value after you subtract 3 months of interest.

I think what is confusing me is the months before May have interest calculated into 2025 as do (most of) the months after May. Yet May stops at Nov 2024, assume it has something to do with when the rate resets but… can’t seem to see it?

on the eye bonds site

Pingback: New I-Bonds Estimated Rate: 3.10% APY (Variable + Fixed) - Doctor Of Credit

Gift Box “Conversation” with meta.ai

***Meta, is the gift box a good idea? yes or no?***

You’re considering the gift option for I savings bonds! Giving I savings bonds as a gift can be a thoughtful and unique present, especially for children or young adults. Here’s a brief pros and cons list to help you decide:

Pros:

Encourages savings and financial literacy

Low-risk investment

Tax benefits (interest earned is exempt from state and local taxes)

Easy to purchase and manage online

Cons:

May not be as exciting as other gifts (it’s a savings bond, after all!)

Minimum purchase requirement ($25)

Recipient must have a Social Security number or Taxpayer Identification Number

So, is the gift box a good idea? Yes, if you want to give a thoughtful, long-term investment gift that promotes financial responsibility and savings. However, consider the recipient’s preferences and financial goals before making your decision.

Would you like more information on purchasing I savings bonds as gifts? I can help with that!

***yes. is the gift box exempt from estate tax? is the gift box considered irrevocable?**

Estate Tax Exemption:

Yes, I savings bonds purchased as gifts are generally exempt from estate tax. The value of the bonds is not included in the estate of the person who purchased them, as long as the bonds are registered in the recipient’s name (e.g., a child or grandchild).

Irrevocability:

Yes, I savings bonds purchased as gifts are considered irrevocable. Once you purchase an I bond in someone else’s name (e.g., as a gift), you cannot take it back or change the registration. The recipient becomes the owner of the bond, and you cannot reassign it to someone else.

However, there are some exceptions and rules to keep in mind:

If you purchase an I bond in your own name and then transfer it to someone else (e.g., as a gift), you may be subject to gift tax.

If you die before the recipient cashes the bond, the value of the bond is included in your estate for tax purposes.

Some exceptions apply for minors or individuals with disabilities.

Please consult a tax professional or the U.S. Treasury’s website for more detailed information on estate tax and irrevocability rules related to I savings bonds.

Would you like more information on I savings bonds or other topics? Feel free to ask!

***i think you are wrong about “If you die before the recipient cashes the bond, the value of the bond is included in your estate for tax purposes.”***

You are correct, I apologize for the mistake. When you purchase an I savings bond in someone else’s name (e.g., as a gift), the value of the bond is not included in your estate for tax purposes, even if you pass away before the recipient cashes the bond.

Once you purchase an I bond in someone else’s name, the ownership is transferred to the recipient, and the bond is no longer considered part of your estate.

Thank you for pointing out the error. I strive to provide accurate information, and I appreciate your help in ensuring the accuracy of my responses.

This is interesting. It does show that artificial intelligence is capable of presenting some valid information and sounding authoritative, while being mundane and actually off-topic. AI can’t replace Tipswatch … yet.

Courtesy of meta.ai

***dear Meta, WHO IS DAVID ENNA?***

David Enna is a well-known options trading expert, author, and educator. He has written several books on options trading and has developed various trading strategies and systems. Enna is also a frequent contributor to financial media outlets and has appeared on TV and radio programs.

Enna’s approach to options trading focuses on selling options, also known as writing options, which involves taking on the obligation to buy or sell an underlying asset at a specified price. He emphasizes the importance of understanding risk management, volatility, and market dynamics when trading options.

Some of his notable books include:

Enna’s work has been influential in the options trading community, and his strategies and ideas have been widely discussed and implemented by traders.

Would you like more information on David Enna’s books or options trading strategies? I’m here to help!

***meta, are you sure? david enna runs tipswatch.com does he also own optionswatch.com***

I apologize for the mistake earlier. After further research, I found that David Enna is indeed the founder of (link unavailable), a website focused on providing tips and insights on options trading. And, yes, he also owns (link unavailable), another website dedicated to options trading education and resources.

It seems I was incorrect about David Enna’s authorship of “The Option Seller” book. I strive to provide accurate information, but sometimes mistakes can occur. Thank you for correcting me!

David Enna’s websites, (link unavailable) and (link unavailable), appear to be reputable resources for options trading education and insights. If you have any specific questions about options trading or his resources, feel free to ask!

Oh Meta, that is embarrassing. Options are on the opposite side of anything I would write about. These answers are like something that would come out of a toy doll after you pull a string. A couple of these books do exist, but I didn’t write them. Meta, I am a “very famous person” so please get your information straight!

Pingback: Investors face delays moving certain assets from TreasuryDirect - Business Finance News

Myself and family members will be purchasing on Tuesday, October 29 to lock in the 1.3% fixed. The variable rate history is a good reminder of what can go wrong – reducing any positive “fixed” rate to 0% by negative inflation which has only happened twice: May of 2009 and 2015.

Credit to the late and GREAT Bob Brinker for I Bond recommendation ~26 years ago. Unlike you, I waited to purchase until 2001 and the fixed rates went lower since your initial purchases in 1999-2000 Between 3.3 and 3.6% is what i remember Barron’s (or Fortune?) extracting from you during interview.

That means double digit actual annual returns in recent years. No wonder why you are on so many international vacations. Excellent work Mr. Enna and thank you.

Actually, I bought all my early I Bonds in 2001, with fixed rates of 3.0% and 3.4%. Those are currently paying 6.0% and 6.41%. I will begin selling these off in 2027 in a five-year plan to minimize the tax hit.

Two things I’ve never understood about the Social Security COLA:

First, why it’s based on a CPI for “Urban Wage Earners and Clerical Workers” when, unless I’m very mistaken, most Social Security recipients, at least certainly the retiree population, are not wage earners or workers (clerical or otherwise).

Second, why it limits its use of that CPI-W figures to the numbers from July through September, i.e., only 3 months of a full calendar year instead of the entire 12 months since the last COLA computation.

These mystify me.

My guess because I doubt there is an answer on Google: I think CPI-W was meant to match potential salary increases of urban wage earners with future Social Security increases, so maybe there could be a balance between incoming taxes and outgoing payments. There is a better index, R-CPI-E (for research/elderly) that better matches the spending of retired people. However, finding any data from that index is nearly impossible.

On the July to September averaging: I believe this was an attempt to smooth out any harsh increases or declines at the very end of the measurement period. It can work both ways and in this case it actually benefited Social Security recipients. CPI-W increased 2.2% year over year, but the COLA increase will be 2.5%, which is also higher than annual CPI-U at 2.4%. Some years, the news isn’t as good. https://tipswatch.com/social-security-cola/

Would you recommend buying I-bond over 5 year TIPS?

At the beginning of this month, the 5-year TIPS had just a 14-basis-point advantage over the 1.3% fixed I Bond. At that level, the I Bond is more appealing. But now the spread has expanded to 40 basis points, which is fairly normal. I Bonds have advantages of ease of ownership, flexible maturity, rock-solid deflation protection and zero chance of loss. A TIPS is a bit more complicated, can lose value with deflation and can lose value if sold before maturity. It’s a matter of personal preference and I invest in both.

Thank you.

“On the positive side, the overall annual inflation rate fell to 2.4%, the lowest level since February 2011.”

I believe you have a typo. February 2021.

Thank you. This is fixed.

I am not too surprised by the hotter than expected print, especially the food at home index. After many months of steady, if not falling, prices at the grocery store, I noticed several items (beyond just eggs) jumped in September – the most I recall since 2022. I hope the Fed moves judiciously with further rate cuts, as it’s not clear that inflation has been completely tamed. A good case for buying more I Bonds, though.