Real yields are holding up, but the curve is widening.

By David Enna, Tipswatch.com

The October auction of a new 5-year Treasury Inflation-Protected Security is always a baffler. The auctioned real yield is highly likely to be lower than many investors expect. Plus, this 5-year maturity is sensitive to potential near-term actions by the Federal Reserve.

Thursday, the Treasury will offer at auction $24 billion of CUSIP 91282CLV1, a TIPS that will mature on Oct. 15, 2029. Some facts:

- $24 billion is the largest auction size in history for this term. A year ago, in October 2023, the auction size was $22 billion.

- The coupon rate and real yield to maturity will be set by the auction’s result.

- As of Friday’s market close, the Treasury’s estimate of the real yield to maturity of a full-term 5-year TIPS was 1.65%, up 21 basis points since Oct. 1.

The October ‘surprise’

Why is the auctioned real yield of this TIPS likely to be lower than expected? It’s complicated, but real yield expectations are often based on the secondary-market trading of the most recent TIPS of that term. The most recent TIPS of this term is CUSIP 91282CKL4, auctioned on April 18, 2024.

That April auction got a spectacular result, with a real yield to maturity of 2.242%. Since then, real yields have been slipping lower. On the secondary market, the April TIPS is currently trading with a real yield of 1.64%. But the key factor is that any April TIPS tends to have a higher-than-market real yield, because it will be exposed to weak non-seasonally adjusted inflation data in its final months to maturity. By comparison, the October TIPS will get a slightly lower-than-market yield.

For example, in October 2023, the auction of a new 5-year TIPS was expected by many investors (including me) to get a real yield of about 2.57%, but instead auctioned at 2.44%. That sent me hunting for an explanation, and I found it. Read this: “There is an explanation for everything, right?”

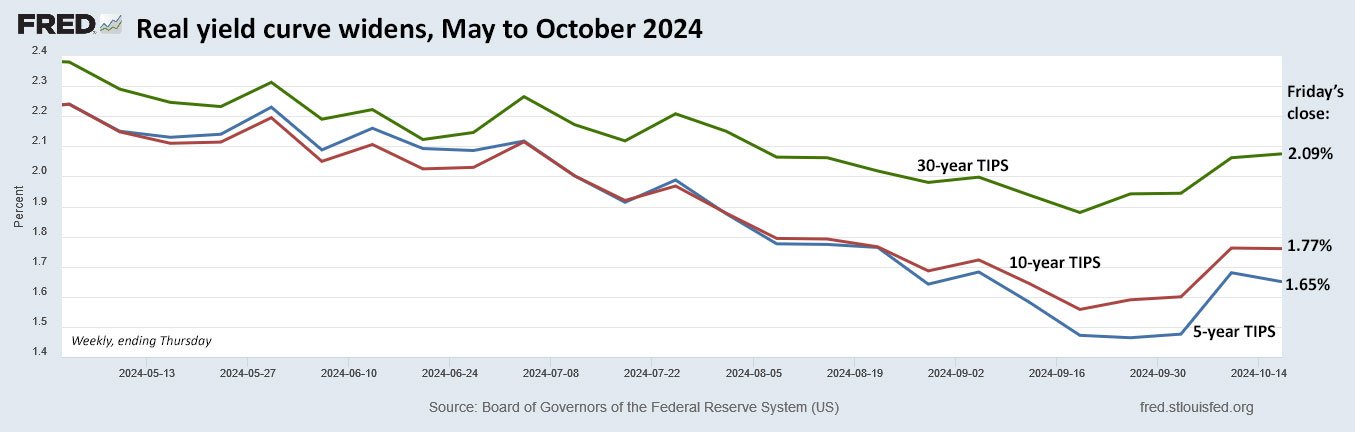

Data back this up, as you can see in this chart of secondary-market TIPS yields, with the October yields consistently lower than April yields. The effect is magnified as the TIPS gets closer to maturity:

So … when looking at this new 5-year TIPS, understand that the real yield to maturity is likely to come in lower than the Treasury estimate, which is currently 1.65%, or the secondary market trading at 1.64%. Things will change by Thursday, of course.

The yield trend

Real yields (meaning the yield above inflation) have declined mightily since the fall of 2023, but remain in an attractive range. What has been interesting is that the yield curve is widening, and actually beginning to look “normal,” with longer-term TIPS having higher yields than shorter-term TIPS.

This is a predictable result of the Federal Reserve’s path toward lower short-term interest rates. The Fed controls short-term rates, but generally can’t control longer-term rates, unless it relaunches quantitative easing (which it shouldn’t). Of the standard maturities, the 5-year TIPS is most sensitive to Fed actions.

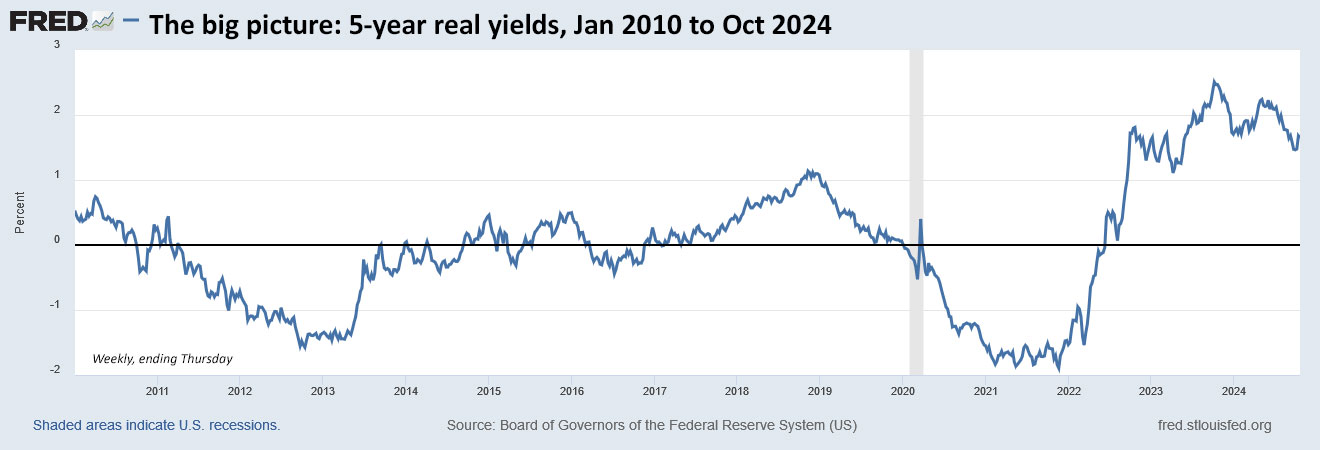

So today the baseline 5-year real yield is hovering around 1.65%, down a whopping 94 basis points since the 2023 high of 2.59% set on October 3. In my view, 1.65% remains historically attractive, as shown in this chart of 5-year real yields over the last 14 1/2 years:

No one can say where real yields are heading, but getting a return 1.65% above inflation seems attractive enough, while not spectacular.

Inflation breakeven rate

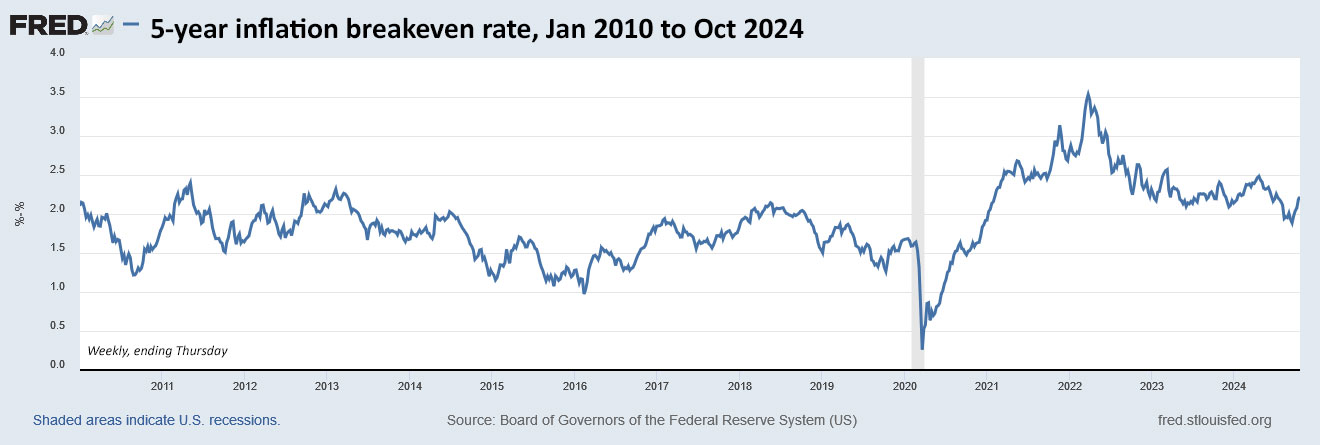

At Friday’s close, a 5-year nominal Treasury note was yielding 3.88%, which at this point indicates an inflation breakeven rate of 2.23% for this new TIPS. That is more or less in line with recent trends. U.S. inflation over the last 5 years has run at 4.2%, but seems unlikely to reach that level over the next 5 years. Or …. maybe it will?

Do you think inflation will run higher than 2.23% over the next 5 years? If so, this TIPS is a sensible investment versus the nominal 5-year Treasury. Here is the trend in the 5-year inflation breakeven rate over the last 14 1/2 years, showing that 2.2% is on the slightly high side of normal:

Pricing

This is a new TIPS, so investors should be paying very close to par value, or slightly less. CUSIP 91282CLV1 will have an inflation index of 1.00042 on the settlement date of October 31, which means an investor buying $10,000 par will be getting $4.20 additional principal. That is negligible.

Thoughts

This auction looks attractive enough, but I have no need to add to the 2029 rung of my TIPS ladder. So I will be passing. Investors could also look at the U.S. Series I Savings Bond, with a real yield of 1.3% for purchases this month. Because of the simplicity and safety of I Bonds, I’d say these two investments are equally attractive. But the $10,000 purchase cap on I Bonds limits their usefulness for many investors.

If you are investing, you can track the Treasury yield estimate each day on this page, and see the yield of the most-recent April TIPS in real time on the Bloomberg U.S. Yields page. But just keep in mind that the result at Thursday’s auction could be 5 to 10 or more basis points lower than what you are seeing on those pages.

This TIPS auction closes Thursday at 1 p.m. EDT. Non-competitive bids at TreasuryDirect must be placed by noon Thursday. If you are putting an order in through a brokerage, make sure to place your order Wednesday or very early Thursday, because brokers cut off auction orders before the noon deadline.

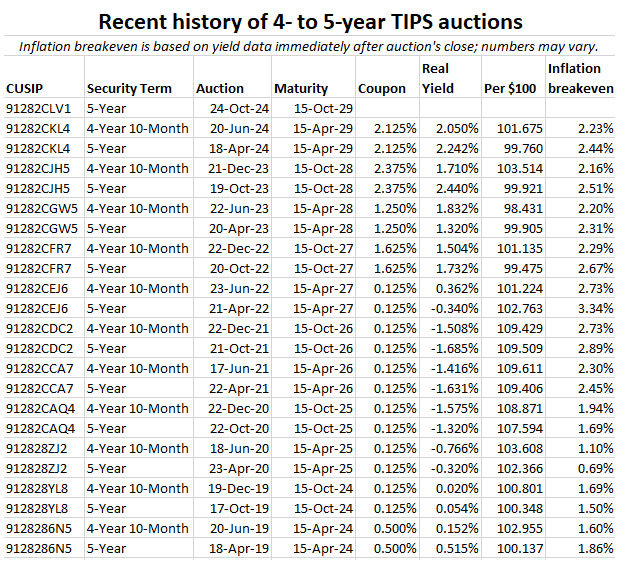

I will be posting the auction results soon after the close on Thursday. Here is a history of auction results for this term over the last 5 years:

—————————-

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Pingback: New 5-year TIPS gets a real yield of 1.670% to potentially lukewarm demand | Treasury Inflation-Protected Securities

Wednesday morning update: At the market close Tuesday, the Treasury estimate of the 5-year real yield was 1.75% and the April TIPS was trading at 1.77% on the secondary market. Real yields are rising this week.

Thank you for this analysis! The I-bond “gifting loophole” may be closing, as some folks have gotten emails from TD to deliver what is in their gift box asap (according to Jennifer Lammer’s faithful followers). Something to consider, perhaps, when weighing TIPS vs. I-bonds. Has anyone heard anything more about this?

I am watching Jenn’s video right now and she has “apparent” confirmation that the purchase limit would be waived for deliveries over the purchase cap. If that is true, the email should have stated that clearly. And yes, her video says TD was saying “changes are coming.” At this point, I have no answer. Ridiculous.

Out of curiosity, I went to the TreasuryDirect home page and clicked on the top-of-the-page link for “News.” That took me to https://treasurydirect.gov/news/ . None of the recent announcements had anything to do with gift box bonds. Then I entered “gift box” in the Search box of the News page: “No results.”

TreasuryDirect has really made a mess with these unexplained bulk emails telling people to deliver-gift-bonds-as-soon-as-possible withOUT reference to longstanding annual purchase limits applicable to the gift recipients’ own accounts.

I just saw this link below after Googling for it. Watched Jen’s video too. Yes. The email is valid. Email is Not clear on the annual limit. As for the changes. What changes? Real cloak & dagger stuff going on if you ask me. “Ridiculous”? I have more to say but can not say it here on this polite forum. I have not received this email yet. Luckily for me it is between spouses so we don’t have to worry about Gift Tax filing, if over the annual limit for it.

https://treasurydirect.gov/indiv/research/email-gifts/

THANKS for all you do to keep us updated about these things.

David, David, thanks again for the 5yr TIPS analysis. FRED has a 5yr forward inflation table saying 2.39% as of 10/18. If everything stays the same and the nominal yield at auction is 3.88% and the break even is 2.23%, does that mean that if I did a proportion with 2.39%, 2.23%, and 3.88%, that the 5yr TIPS would have about a 4.15% return if inflation averages 2.39%? When I put in my info, a 4.15% return on a Treasury is similar to a 4.71% CD on the Fidelity tax calculator. Am I applying the FRED table and possible 4.15% real yield correctly in this scenario? Is adding to an existing 4.75% new 5yr MYGA (similar to a CD taxwise) a better return than this new 5yr TIPS? Thanks!

If the real yield is 1.65%, let’s say, and inflation actually averages 2.23% over the next 5 years, your nominal return is going to be 3.88%, exactly the same as the nominal Treasury.

Thanks. So in that scenario, if the average inflation is 2.39% over the 5 years, higher than 2.23%, is the nominal return about 4.15%? Thanks, David

It would be about 4.04%, if … the real yield is 1.65% and inflation averages 2.39% over 5 years.

Need to decide between I Bonds or these 5 yr TIPS. I will be retired when they mature. I Bonds I can use for kids education.

The interest on I Bonds can be tax-free if used for educational expenses for you, your spouse, or children listed on your tax return as dependents. There are limitations, however. Read this: https://www.treasurydirect.gov/savings-bonds/tax-information-ee-i-bonds/using-bonds-for-higher-education/ And see income limits here: https://www.irs.gov/pub/irs-pdf/f8815.pdf

Thanks. I put in a order today for the 5yr TIPS. Let us see what kind of yield we get. Can use the money to pay property tax and other insurance costs when it matures.

Do you know what interest rate these TIPS will have for the twice a year interest payments?

Most likely, the coupon rate will be set at 1.50% or 1.625%, depending on the auctioned real yield. The coupon rate is set 1/8th percentage point below the real yield.

Thanks for the auction preview. I am still pleased with my purchase last October, despite the lower than expected result. Time will tell whether I would have been better off buying the 5-year nominal due to the high breakeven rate.

You mention that 5-year yields are more sensitive to the Fed than longer-term TIPS. Does this mean we’ve likely seen the end of 2% real yields on the 5-year for the foreseeable future? Or could 5-year yields rise even with the Fed continuing to cut short-term rates?

We definitely could see 2.0%+ 5-year yields in the future, but that would probably require a surge in inflation and a new round of Fed tightening. Can’t be sure, of course. …. As it ended up, that October 2023 purchase was a winner. Congrats on that purchase.

Thanks, David. This confirms my read of things. I do see upside risks to inflation but am cautiously optimistic it will stay tame for the next year or two.

After a lot of second-guessing, I’ve decided to buy another set I Bonds before October 30. It will be interesting to see over the next few years if the 5-year TIPS continues to be the best predictor of the I Bond fixed rate (though I’m sure there will be some surprises along the way).

David,

We’ve been thinking about starting to buy TIPS (in addition to I Bonds, not instead of) and would do it within Roth IRAs, which, in tax terms, we consider the least complicated place to hold them.

But we’ve been buying I Bonds for many years, and are accustomed to their “pay face value” character, i.e., pay $10,000, get $10,000 “worth” of I Bond principal.

So buying “new” TIPS at original auction, and very close to par value, is easy to understand, but we’re having trouble wrapping our minds around the idea of paying a premium for past TIPS on the secondary market.

Any opinion on paying extra to buy the previous 5-year TIPS, maturing April 2029, with coupon 2.125%, instead of the new 5-year being auctioned this week, i.e., whether the higher coupon is “worth” the surcharge on the purchase price compared to the 5-year being auctioned this week? How about the 5-year TIPS maturing April 2028 (1.25%) or October 2028 (2.375% but still without a lot of built-in inflation adjustments)? Ocober 2027 (1.625%)?

We know (in the standard disclaimer on this website) that you’re a financial writer, not a financial adviser, but we’re just trying to figure out what are the pros and cons. Thanks.

In general, I’d rather buy the new TIPS close to par at auction, but this is not really a big deal. The one overriding factor is the real yield to maturity, which will be similar for all these investments. For longer-term TIPS, you may have to buy a lot of unprotected accrued inflation, sometimes at a premium price. I’d still do it if that is the only TIPS available in that year.

Once you buy a TIPS in a brokerage account, you are going to see its value fluctuating every day. That can be disturbing, but you can ignore the volatility if you are holding to maturity.