By David Enna, Tipswatch.com

It’s good news when a monthly U.S. inflation report matches expectations. And October delivered, even though annual all-items inflation ticked higher and core remained too strong for comfort.

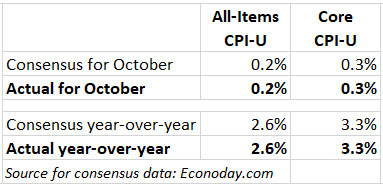

The U.S. Bureau of Labor Statistics reported that all-items CPI-U increased 0.2% on a seasonally adjusted basis in October, the same increase as in each of the previous three months. Over the last 12 months, the all-items index increased 2.6%, higher than September’s 2.4%. Core inflation, which removes food and energy, held steady at 0.3% for the month and 3.3% for the year.

All these numbers matched economist expectations in a clean sweep, which hardly ever happens. Inflation is hard to predict.

The BLS noted that shelter costs increased 0.4% in October, accounting for more than half of the all-items increase. Shelter costs were 4.8% higher year over year. Those increases were partially offset by a 0.9% drop in gasoline prices, which were down 12.2% year over year. More from the report:

- Food at home prices rose only 0.1% for the month, after rising 0.4% in September, and are up 1.1% year over year.

- Electricity costs rose 1.2% for the month and 4.5% year over year.

- Apparel costs fell 1.5% for the month and are up just 0.3% for the year.

- Airline fares rose 3.2% for the month and are up 4.1% year over year.

- The costs of motor vehicle insurance rose 1.2% and are up 14.0% year over year.

- Medical care services were up 0.4% for the month and 3.8% year over year.

- Costs of new vehicles were flat for the month and down 1.3% for the year.

- Used vehicle costs rose 2.7% but are still down 3.4% year over year.

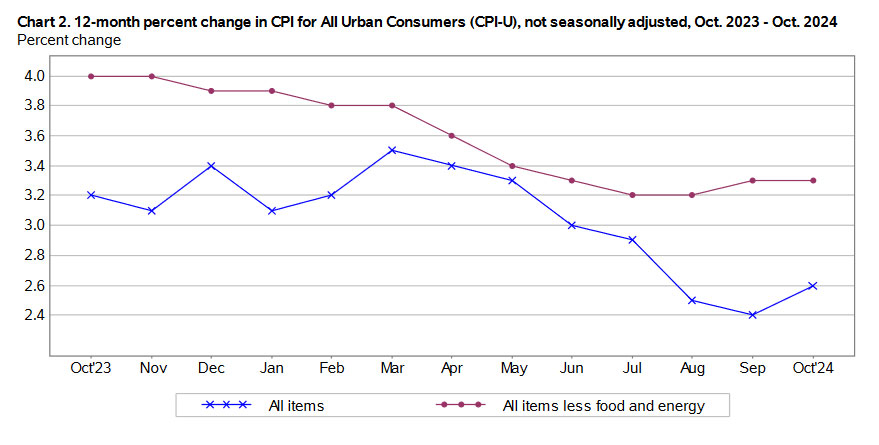

Overall, while this October inflation report met expectations, it also clearly shows U.S. inflation has not been tamed. This is not good news. Here is the trend in U.S. inflation over the last year, showing the uptick in all-items costs:

What this means for TIPS and I Bonds

Investors in Treasury Inflation-Protected Securities and U.S. Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances for TIPS and set future interest rates for I Bonds.

The BLS set the October inflation index at 315.664, an increase of 0.12% over the September number. We are heading into the time of year when non-seasonal inflation will be running lower than adjusted inflation. Don’t be surprised if we see one or two months of deflation in this index before the end of the year.

For TIPS. The October number means that principal balances for all TIPS will increase 0.12% in December, after rising 0.16% in November. Over the 12 months ending in December those balances will have increased 2.6%. Here are the new December Inflation Indexes for all TIPS.

For I Bonds. October marks the first month of a six-month string that will determine the I Bond’s new variable rate, to be reset May 1, 2025. After one month, inflation has increased 0.12%. It’s way too early to draw any conclusions from that. (But in October 2023, non-seasonal inflation fell 0.04%, the first of three consecutive deflationary months.) Here are the data:

What this means for future interest rates

Overall inflation rose in October, which was expected but can’t be welcomed. Because the numbers were in line with expectations, we can probably expect the Federal Reserve to go ahead with a 25-basis-point cut in short-term rates in December.

The effect of that cut on the economy would be minor because longer-term rates have increased dramatically in the last few weeks. U.S. 30-year mortgage rates have increased from about 6.1% at the beginning of October to 6.8% today.

From this morning’s Bloomberg report:

The figures underscore the slow and frustrating nature of the battle against inflation, which has often moved sideways — sometimes for months at a time — on its broader path down. …

“October’s CPI report remains in the same holding pattern as the past few months – inflation isn’t picking back up, but it’s also not cooling any faster,” said Anna Wong of Bloomberg Economics.

“October’s CPI report contains no information that would discourage the FOMC from cutting rates again at the December meeting,” said Michael Arnold, Bloomberg Economics Editor.

My impression is that this report changes nothing. Inflation remains well above 2.0% and will continue to be a long-term danger if the U.S. economy and stock market hold strong.

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

The idea that this is good news because it was within “expectations” is an odd take. Seems like some coping compensation. You don’t have to carry water for the Fed and policy makers – you don’t work for them

I think you are trolling me, but … when I say this was good news I was talking about the market reaction. Meeting expectations is good for the stock market, especially. If you actually read the article, you would have noticed I wrote: “Overall, while this October inflation report met expectations, it also clearly shows U.S. inflation has not been tamed. This is not good news.”

Can someone explain why strong economy and stock market contribute to higher inflation? Is it simply because there is more money available to spend and the company profits are higher? I’d love to understand this relationship better.

More wealth, definitely. Also a tight labor market, more development meaning more use of commodities, more travel, more car purchases, etc.

Hi DB,

I understand too kinds of inflation – not enough products/services – prices go up. Too much money printed – value of money goes down.

Of course, all the illustrious “experts” out there say that this is an outdated thinking, “fiat currency”and so on.

The only thing that makes sense about the stock market – its already inflated like crazy from stock buy backs over the last couple of decades – when it goes up just keeps getting inflated.

When inflation is up, stocks get more attractive because they are more likely to “keep up” with the inflation. Prices go higher on items, therefore stocks get more EPS since everything is more expensive. Hence, stock prices increase. Sure you’re getting more EPS for just the inflation (ie buying power is still the same; now you get $1.20 EPS instead of just $1.00), but hey, you got the adjustment to keep up, right?

However, 4% interest on treasuries and bank accounts are still the same and lower than the uptick of inflation. That’s why stocks are starving for lower interest rates. The more unattractive the interest rate, the more attractive stocks look and therefore more people buying stocks which leads to higher stock prices. Where stocks run into trouble is when people finally run out of money and now they aren’t even making a dollar per share like they originally were. No, now they’re down to $0.50 or even losing money. All the sudden 4% looks delicious, but then they are cut to 2% (pure example).

Maybe oversimplified, but one of many reasons.

Thank you all for the explanations on the relationship between inflation and stock market/strong economy. I learned something new.

Rates rising on longer term bonds suggests to me that the market thinks that the Fed is not really serious about getting inflation down to 2%. That 2% target is now on average, so given recent history, they need to overshoot on the way down. I don’t see how they can cut the Federal funds rate again next meeting, especially given that some of Trump’s proposals could be inflationary.

I’m retired with a zero COLA corporate pension, so count me as an inflation hawk.

Between the economy staying strong and the stock market skyrocketing, I dare say we can officially claim this inflation has been “sticky.” Not saying nothing will ever happen (duh!), but compared to how it was declining at a fairly good rate, it then stopped abruptly and didn’t get to below 3.0% until July of this year. Now it’s going back up after 2% started to look possible. Gas prices going down really “saved” us. I’d say we’d easily still be 3-4% if gas hadn’t declined.

Just my two cents. Which literally aren’t worth anything. 😢😂

Hey, its worth more than two cents, good observations

I agree and the price of oil affects nearly everything else.