Troubling conclusion: U.S. inflation is no longer slowing and remains too high.

By David Enna, Tipswatch.com

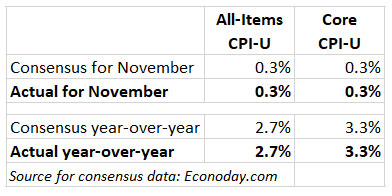

Although annual U.S. inflation rose from 2.6% in October to 2.7% in November, financial markets are likely to view today’s report as a positive, because it matched expectations.

The U.S. Bureau of Labor Statistics reported this morning that both all-items inflation and core (which excludes food and energy) rose 0.3% in November. Those increases matched economist expectations, which – surprisingly – have been fairly accurate recently.

This isn’t exactly cause for celebration, as annual inflation remains too high and seems to be drifting higher. Core inflation has increased 0.3% in each of the last three months. But the stock and bond markets like predictable results. Stocks were up in premarket trading.

The BLS again pointed to shelter costs as a primary inflationary factor, with costs rising 0.3% for the month and 4.7% for the year. That increase, the BLS said, accounted for about 40% of the overall all-items increase. Also, gasoline prices increased 0.6% for the month, but have fallen 8.1% over the last year. The November increase broke a seven-month trend of declining gas prices. More from the report:

- The costs of food at home increased 0.4% for the month and are up only 1.6% for the year. But the costs of dining out — food away from home — have increased 3.6% year over year.

- Apparel costs were up 0.2% after falling 1.5% in October.

- Costs of new vehicles rose 0.6% but are down 0.7% for the year.

- Used car and truck prices rose a sharp 2.0% in November after rising 2.7% in October. But they are still down 3.4% year over year.

- Airline fares rose 0.4% for the month and 4.7% for the year.

- Costs of medical care services rose 0.4% in November and 3.7% for the year.

- Motor vehicle insurance costs rose only 0.1% for the month but remain 12.7% higher for the year.

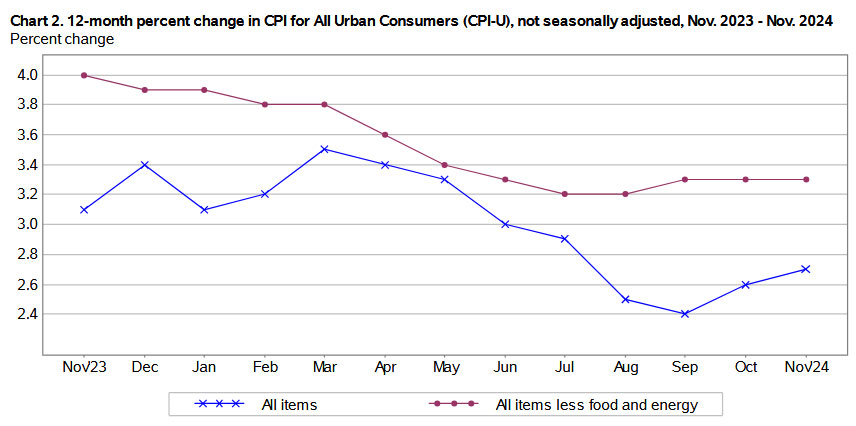

The BLS noted that price increases were widely spread across all major categories. Here is the trend for annual all-items and core inflation over the last 12 months:

This chart presents strong evidence that declines in U.S. inflation have ended, for the time being.

What this means for TIPS and I Bonds

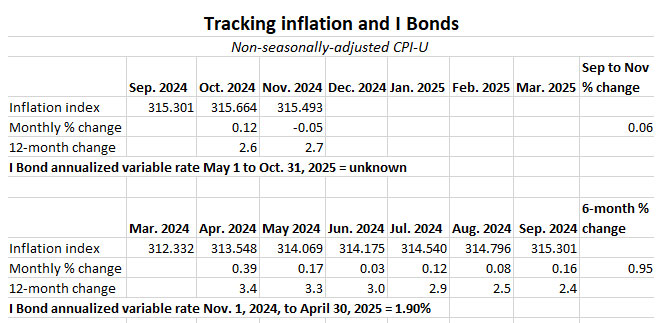

Investors in Treasury Inflation-Protected Securities and U.S. Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances on TIPS and set future interest rates for I Bonds. For November, the BLS set the CPI-U index at 315.493, a decrease of 0.05% from the October number.

For TIPS. The November inflation report means that principal balances for all TIPS will decline by 0.05% in January, after rising 0.12% in November. It is normal to see deflationary non-seasonal numbers in November and December. For example, in 2023, non-seasonal inflation declined 0.2% in November and 0.1% in December.

This is likely to reverse course in January. Earlier this year, for example, non-seasonal inflation rose 0.54% January while adjusted CPI-U increased 0.3%. Here are the January inflation indexes for all TIPS.

For I Bonds. The November inflation report is the second in a six-month string that will determine the I Bond’s new variable rate, which will be reset May 1. So far, after two months, inflation has increased just 0.06%, which would translate to a variable rate of just 0.12%. This is meaningless. It’s too early to make any assumptions. Here are the data:

What this means for future interest rates

Clearly, inflation remains too high and is not showing signs of falling. But the Federal Reserve has been signaling it is likely to go ahead with a 25-basis-point decrease in the federal funds rate next week. This report seems unlikely to change that plan.

This morning’s Bloomberg headline is right on target: “US CPI Brings No Surprises, Firming Up Fed Rate-Cut Bets.” From the coverage:

The report suggested that disinflation has essentially stalled in recent months. Headline CPI notched the first back-to-back annual acceleration since March, while core has been stuck at 3.3% — well above a figure consistent with the Fed’s 2% target for a separate price gauge, the PCE – for three months now. …

Shelter costs as usual made up the main portion of the rise in CPI, at almost 40%, although they did slow from the previous month. …

“Especially given the slowing in shelter, this should be very comfortable for the Fed to lower policy rates 25 basis points in December and continue cutting in 2025,” Citigroup Inc. economists Veronica Clark and Andrew Hollenhorst said in a note.

I agree that a 25-basis-point decrease seems likely next week, which would put the federal funds rate in the range of 4.25% to 4.50%, still comfortably higher than the annual U.S. inflation rate of 2.7%.

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Hi David,

Received this in an email from Treasury Direct yesterday:

“TreasuryDirect aims to provide Americans a safe, secure way to save for the future. Because we want our customers to maximize the benefit of investing in Treasury securities, we are discontinuing the ability to fund a Certificate of Indebtedness (C of I) though payroll. You are receiving this email because within the last year, you funded your C of I from your paycheck. You will need to take action before January 31, 2025.

What is C of I?

C of I is a non-interest earning Treasury security intended to be used as a source of funds for purchasing eligible interest-bearing securities.

Whats happening?

As of January 31, 2025, TreasuryDirect customers will no longer be able to fund C of I from their paycheck.

What do I have to do?

Contact your payroll provider to stop electronic deposits before January 31, 2025. After this date, any deposits to your C of I will be rejected.

How do I learn more?

Additional information about Payroll C of I can be found here. We will also be sending reminder emails in advance of the change.”

The link leads to the TD User Guide Sections 301-310:

“User Guide 302 Learn More About The Payroll Savings Plan

Please Note: A Payroll Zero-Percent Certificate of Indebtedness is a Treasury security that does not earn any interest. It was intended to be used as a source of funds to purchase Series EE and Series I Savings Bonds through the Payroll Savings Plan.Stopping your payroll allotment/direct deposit and redeeming your Payroll C of I.

The Payroll Savings Plan will be discontinued on January 31, 2025. You must contact your employer (payroll office) to have your payroll allotment/direct deposit stopped. There is no need to edit your Payroll Savings Plan information in TreasuryDirect when you stop your allotment/direct deposit.

You may redeem all or part of your Payroll C of I by going to ManageDirect and selecting the Redeem Securities text link. You may choose to redeem the full amount or a partial amount. You must select a payment destination bank for the Payroll C of I. Note: Redemption of your Payroll Zero-Percent C of I does not stop your payroll allotment/direct deposit.Viewing Payroll Savings Plan transaction records.

You can access history records about savings bonds purchased through the Payroll Savings Plan, view records about your Payroll C of I transactions, and view changes made to your Payroll Savings Plan by clicking the History tab.

User Guide 307 Learn More About Payroll Zero-Percent Certificate of Indebtedness

The Payroll Zero-Percent Certificate of Indebtedness (Payroll C of I) is a Treasury security that does not earn any interest. It was previously intended to be used as a source of funds for purchasing Series EE and Series I Savings Bonds through the Payroll Savings Plan in TreasuryDirect, which will be discontinued on January 31, 2025.

For more information about this, see Learn more about the Payroll Savings Plan and read our FAQs.

The incoming credits from your payroll office will result in the purchase of a Payroll C of I within your TreasuryDirect account. Each time your Payroll C of I balance reaches your designated purchase amount, a savings bond will be issued. (For example, if your payroll allotment/direct deposit is $10 each pay period, and you have chosen a purchase amount of $25, after your third allotment/direct deposit is received, a $25 savings bond will be purchased from your Payroll C of I and the remaining balance will be $5 until the next allotment/direct deposit is received.)

You may redeem all or part of your Payroll C of I by going to ManageDirect and selecting the Redeem Securities text link. You may choose to redeem the full amount or a partial amount. You must select a payment destination bank for your Payroll C of I. Note: Redemption of your Payroll Zero-Percent C of I does not stop your payroll allotment/direct deposit. All Payroll C of I purchase and redemption activity is conveniently recorded in your C of I History.”

So I assume you were having some of your paycheck sent to the C of I for future investments? I would suspect that this is no longer a common practice. I suspect this is one of several changes coming in 2025. Thank you for sharing this.

Yes, some of paycheck weekly was sent to C of I. I wonder if it is just part one before shutting down C of I completely,”(Payroll C of I) is a Treasury security that does not earn any interest. It was previously intended to be used as a source of funds for purchasing Series EE and Series I Savings Bonds through the Payroll Savings Plan.”

Any thoughts/concerns about the possibility of the Bureau of Labor Statistics staff being replaced and future CPI data being not reported or reported incorrectly

It “could” be a possibility. I would say the current BLS is reliable. Unless almost everyone is replaced, it would be hard to doctor statistics without someone blowing the whistle.

I’m aware of this forum’s prohibition on political discussions, and, although the following obviously touches on public policy, I do not intend it as a “political” comment.

Apart from whatever other qualities they possess which causes them to seem like attractive places to hold money, the desirability of TIPS and I Bonds depends in very large part on the let-the-chips-fall-where-they-may honesty and accuracy of the “inflation” measure to which they are indexed.

In my general observation of the economy and in my experience (e.g., a manager who refused to raise my performance evaluation 1/10 point to Outstanding, which would have substantiated a pay raise, because “we’re not giving Outstandings this year”), there are executives and organizations which gather facts and then make decisions firmly based on the evidence at hand, and there are executives and organizations which decide in advance on desired outcomes and then tailor or torment or cherry-pick the “facts” to produce the predetermined outcomes.

I have the sense that during the next four years those of us who believe in the reality-based former may find ourselves disappointed and dismayed by the policy-based latter. I would be quite pleased to be proven wrong. In any case, although the issue surely doesn’t occupy my waking hours, I do occasionally wonder about the future inflation-protective value of our household’s TIPS and I Bonds if the “official” CPI comes to be seen as untrustworthy through ideological manipulation by executive fiat.

I wasn’t sure if you saw this Seeking Alpha article about iBonds in which you are appropriately referenced:

“About a month ago or a little more holders of “undelivered” I Bonds began receiving notices from TreasuryDirect “asking” them to Deliver their Gift I Bonds to the recipient “as soon as possible.” I first heard of this from David Enna at Tipswatch whose blog on TIPS and I Bonds is a sort of gathering place for individuals interested in inflation-protected securities.”

https://seekingalpha.com/article/4740269-i-bonds-on-second-thought-not-bad-idea-to-keep-buying-inflation-insurance

It’s interesting that there’s been radio silence since those notices went out. You would think there would be a leak somewhere about the intentions of TD in sending them out. I mentioned this once before, but my working hypothesis is a complete website redesign which requires the gift box to be manually moved to the new site unless owners do it themselves. Time will tell.

I appreciate the alert. The author, Jim Sloan, is one of the best. We have corresponded often.

Good morning David. Today’s Auction for the nominal 10 yr reopening Note had a Bid-to-Cover ratio of 2.7. Would you please explain this ratio as an indicator of market appetite for the issue.

Thank you, Dale

It is the ratio of total bids versus the size of the auction. I only track bid-to-cover ratios for TIPS auctions, and 2.7 would be considered an indication of very strong demand. For 10-year TIPS, the ratio tends to fall well below 2.7. For today’s 10-year note reopening, the when-issued prediction was 4.252% but the yield ended up at 4.235%. So demand was strong.

Thank you.

Thank you for the quick update today! What do you think this means for Treasuries of 2-, 3-, 4-year duration? Would locking in the 4% rate now be a good idea, considering the Fed is likely to decrease the rate next week and probably during 2025 also?

If I had a need for money maturing in 2 to 5 years, I’d definitely take a hard look at nominal Treasurys paying more than 4%.

Thank you for the quick reply. I want to make sure I understand. Do you mean even a flat 4% or looks like 4.17% is the highest in that duration range, or do you mean much higher than 4%? (I’m sorry – I’m so literal!)

4% or higher. If it is way higher, all the better.

I’m guessing November and December tend to see deflation (as far as the variable rate for I-Bonds) due to all of the sales businesses are providing for the holidays? Between trying to get everyone to buy their products and also getting rid of old inventory (ie old, outdated technology such as computers) in order to sell the new stuff at the beginning of the year. Your opinion?

Yes, there are many “Black Friday” deals that start right away in November and carry through December. Seasonal adjustment accounts for this in the official CPI report. But non-seasonal presents the actual price declines. So you will often see deflation in non-seasonal numbers during the end months of the year.

I have started building a tip ladder that starts in 2031 and goes to 2050. I have purchased 5 rungs so far – 2031-2034 plus 2041. Given current rates would I be wiser to go further out to purchase rungs? I could then fill in the earlier rungs once they get back to at least a 2% real yield. I appreciate your articles and website. It gave me the courage and some understanding to do this. Thanks.

Impossible to answer, because we may not see 2% real yields for the 5- to 10-year maturities for years … or maybe in a month. These yields have been volatile. The 2% level is a nice target, but not always possible. (I’ve bought many TIPS with real yields well lower than that.) You can nail down 2% for the longer-term yields, so no problem there. But realize yields can go higher. Just hold to maturity and ignore the fluctuations.

Thanks for the prompt reply. I will keep watching and buying until they are all filled. It gives me great piece of mind. What finally assured me I should do it was your comparison of social security to a tips ladder. It is similar to buying yourself more social security. That was exactly what I wanted to do!

I “googled” the seasonal inflation adjustment by month and got only useless detailed data in my search.

I found out that these seasonal adjustments vary year to year, but only slightly.

I am considering buying TIPS nearing maturity.

A useful listing of seasonal inflation adjustments by month (in 2024) would be useful.

Such as

January +0.0023

February +0.0018

…

November -0.0030

December -0.0021

Thank you for your efforts & work !

TIPS nearing maturity are the most likely to be hit by short spells of deflation, so be aware of that: https://tipswatch.com/2024/06/23/dont-over-think-the-potential-threat-of-deflation/

Also, I have discussed this seasonal factor often, most recently: https://tipswatch.com/2024/10/20/what-about-thursdays-auction-of-a-new-5-year-tips/

If you want to go nuts, head here: https://www.bls.gov/cpi/seasonal-adjustment/ Download the Excel file “Revised seasonally adjusted indexes and factors, last five years” For example, the unadjusted index for Dec 2023 was 306.746, but the adjusted number was 308.742. The result was that official inflation rose 0.3% for the month, while non-seasonally-adjusted inflation was down -0.1%. Big swing. It all balances out over 12 months.

While updating the values of my TIPS today from the treasury TIPS/CPI website, I am confused as to why they are showing the inflation indexes were falling from 1/1/2025 to 1/31/2025. This does not make sense. The reported change was reported to be +0.3% for the month to month. The inflation indexes should all be up 0.3% (approximately because the 0.3% is rounded off).

Can anyone explain? When will they correct this mess?

As I noted in the article, TIPS principal balances are adjusted based on non-seasonally-adjusted inflation, which declined 0.05% in November, resulting in the slight decline in indexes for January 2025. The annual numbers balance out over time, so future non-seasonal months will be higher, beginning in January.

Thank you very much for your clear and thorough posts as I ease my way into owning TIPS. I was happy to participate in last month’s 10-year auction and I’m disappointed that this month’s 5-yr auction is unlikely to provide TIPS at greater than 2% real yield. Wanting that level of real yield, I am thinking of buying 10 to 30 year TIPS on the secondary market. 20- or 30-year TIPS could easily exceed my lifespan, but I don’t need the income from a ladder would sell them on the secondary market when needed (in the hopefully distant future). Before I dive into your posts on the secondary market, I’m wondering: am I missing something?

The 5-year real yield is about 1.72% right now, which I still consider attractive. I’d say look for the maturity dates that match your needs and plan to hold to maturity. There will be a new 10-year TIPS issued in January.

regarding buying 20 or 30 year tips, I’ve considered but what stops me is fact if I need the money when long bond yields are down, I lost potential significant value. By how much no idea.

Buying a long-term (20 to 30 year) Treasury of any kind isn’t the best idea if you feel you will need the money before maturity. It could work out fine, you could even profit, but if you don’t want to fear a loss you need to hold to maturity.