By David Enna, Tipswatch.com

I was alerted by a reader yesterday about an email sent from TreasuryDirect informing him that it is “discontinuing the ability” to fund savings bond purchases through payroll deductions.

Of course, the Treasury didn’t make this easy to understand. Technically, it said Treasury is ending payroll contributions to its zero-interest Certificate of Indebtedness (C of I) account, which is then used to buy savings bonds at regular intervals.

The email said:

As of January 31, 2025, TreasuryDirect customers will no longer be able to fund C of I from their paycheck. Contact your payroll provider to stop electronic deposits before January 31, 2025. After this date, any deposits to your C of I will be rejected.

The email links to TreasuryDirect user guide sections 301 to 310, which give “clarification” for this change. These instructions, naturally, are quite dense and mysterious, as is common with communications from TreasuryDirect. From User Guide 307:

The Payroll Zero-Percent Certificate of Indebtedness (Payroll C of I) is a Treasury security that does not earn any interest. It was previously intended to be used as a source of funds for purchasing Series EE and Series I Savings Bonds through the Payroll Savings Plan in TreasuryDirect, which will be discontinued on January 31, 2025.

The Payroll Savings Plan will be discontinued on January 31, 2025. You must contact your employer (payroll office) to have your payroll allotment/direct deposit stopped.

Rewriting history

The history of the payroll deduction program dates back at least to 1942, when the Treasury approved use of payroll deductions for the purchase of War Bonds. This later became known as the Payroll Savings Plan.

TreasuryDirect has a page providing a history of its Payroll Savings plan, noting that “In the minds of millions of Americans who grew up from the 1940’s through the 1990’s, savings bonds and payroll savings are synonymous. Many have never bought a bond in any other way.” But …

Payroll savings began a long decline in the 1980’s, as markets changed, and new financial products were created and began to be offered by employers. Products including 401(k) plans and employee stock option plans, both designed to help employees save for their futures as defined benefit retirement plans, gradually became the rule rather than the exception among large employers. These plans were more attractive to many employees, despite being less liquid.

In early 2003, Congress ended funding for the marketing of savings bonds, accelerating a previously slow decline for the payroll savings plan.

And then … “The payroll savings plan will be discontinued on January 31, 2025.”

And that means?

I suspect this is part of changes we will see in the savings bond program in the early months of 2025. I doubt the payroll-deduction plan is widely used anymore, so this may not affect many investors. Many employers, apparently, do not participate.

We know from recent “mysterious hints” from TreasuryDirect that changes could be coming to gift-box purchases of savings bonds, a purchase loophole that has been widely used in recent years as Series I Savings Bonds became attractive. And earlier this year, Treasury eliminated the ability to purchase paper savings bonds in lieu of a federal tax refund.

It seems odd that Treasury would eliminate the payroll-purchase program, which would appeal to ultra-small investors who might want to buy $100 lots of savings bonds at regular intervals. But, as I noted, this could be little used and a maintenance nightmare for the Treasury.

A lingering question would be: Is the zero-interest C of I being shut down completely? I doubt that, because this is where Treasury places funds with no known destination. This can happen when a user has incorrect banking information or no connected bank account. It is also where some investors briefly park money from maturing investments to await reinvestment.

And of course, some people are going to ask: Is Treasury preparing to close down the savings bond program entirely? I really don’t think so. That would be a disaster, because for many small-scale investors I Bonds are only easily accessible inflation-protected investment.

In addition, I Bonds and EE Bonds generally pay lower interest rates than most other Treasury investments, so the Treasury actually saves on borrowing costs by issuing savings bonds. Plus, actual payments to investors are usually deferred for many years.

As usual, Treasury could have done better with this communication. For example, it could have provided this information …

A simple alternative

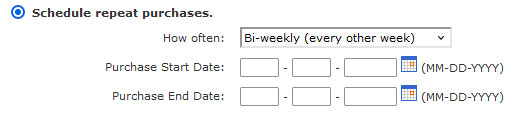

If you were using the payroll deduction program and want to continue regular purchases of savings bonds, you can do this easily at TreasuryDirect.

- First, log into your account and navigate to the “BuyDirect” page.

- Select the savings bond you wish to purchase.

- Then, in the “purchase frequency” section, set up repeat purchases. Options are weekly, biweekly, monthly, quarterly etc.

Reminder: Your total purchases for a calendar year can’t exceed the purchase limit of $10,000 per person per year.

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Really annoyed about this

I had $192 every week going into I-Bonds from my paycheck; it was set-it-and-forget-it heaven. Perfect for someone that is not super investment savvy like I am.

I respect all y’all’s knowledge on this stuff, but people like me find all of this a real effort. It was nice to have one small element of my savings – $10k per year, plus my tax return going somewhere I didn’t have to think about.

Now both of those options are gone.

Now I’m gonna have to learn the TD website again and figure out how to keep buying the I-Bonds or just abandon them going forward.

Not sure how this makes anything better.

Thank you for the post – it was the only informative thing I could find about this.

God bless you

I understand the reasonings behind this decision — as David says “this could be little used and a maintenance nightmare for the Treasury.” But it seems shortsighted to me, as a revitalized savings bonds program via the Payroll Savings Plan could serve as an unofficial national pension program, especially for low-income workers (and by reissuing the U.S. Individual Retirement Bond).

Basically they don’t want to be a receptacle for ACH pushes inbound, which could come from literally anywhere, not just a payroll. They only want people to use TD to pull money in and push money out, not any other bank web site.

This is just the pessimist in me, but I don’t think TD, savings bonds, etc. will be around much longer. Five or so years. All in all, the amount of savings bonds and money raised via TD is a rounding error for the Treasury. The current incoming administration has made “waste” and cost cutting their focus. Most people aside from Tbills and Ibonds use their brokerages to buy treasuries.

Shutting down TD could be one way to increase “efficiency.” I personally wouldn’t mind buying TIPS, I, or EE bonds via a brokerage given the ability to have a consolidated view of my assets and decent customer service.

The real question is whether brokerages find Treasuries to be a worthwhile business endeavor. I am doubtful that most brokerages would want to pick up the slack given there wouldn’t be much profit for doing so.

The one necessary role for TreasuryDirect is the sale and distribution of savings bonds. If TD goes away, I think savings bonds would be discontinued.

In addition, per User Guide 153, “The option to fund your C of I through ACH credit [i.e. a push into TD initiated by your outside bank] will be discontinued on January 31, 2025.”

As I am reading this, I interpret it as no effect on ACH requests initiated from your Treasury Direct account for transfers in or out. Am I correct?

I’d say that’s correct. Most buyers would bypass C of I when making new investments with outside money. So the most common use would be a short-term holding spot for reinvestment, and I “think” that will continue to be allowed. All of this TreasuryDirect verbiage appeared to be focused on money coming in from outside sources, for the purpose of making a future purchase of savings bonds.

Thank you, David, but I’m not sure that quite answers. Continuing the User Guide 153 bit on ACH Credits cited by Diego:

“You should not request your financial institution to schedule future deductions to deposit into your C of I. For more information, read our FAQ.”

I think of my normal procedure of funding the C of I to be by submitting a transfer request to Treasury Direct – not by submitting a request to my bank as implied above. So I’m wondering if Treasury is cutting off the ability to fund the C of I from the outside altogether, or merely to limit funding requests to those initiated within their own system which they presumably feel is more in their control.

Of course, the FAQ referenced in that element of the User Guide provides all the clarity of the Mississippi after a torrential rain. So maybe I will just have to wait and see what the end of January brings.

User Guide 152 still states, in part (Bold Emphasis added):

There’s no limit to the amount you may hold in your C of I. You may build the amount in your C of I a number of ways:

Thanks for the write up David!

This TD posting confirms that TD knows how to post changes…ergo, where is the expected changes for IBonds for the gift box…must be none!!!!!

When I started work for the federal government in 1968, there was pressure from my boss to sign up for payroll savings bond purchases. I was tight for money, but signed up for a $1 deduction every 14-day pay period. It took more than 8 months to accumulate the $18.75 purchase amount and the bond was back dated to the mid-point of the accumulation period so the day I got the bond it was already more than 90 days old and I could immediately cash it at the bank.