By David Enna, Tipswatch.com

April 11, 2025, update: Welcome to the I Bond ‘buying season’

April 10, 2025, update: I Bond’s variable rate will rise to 2.86% on May 1

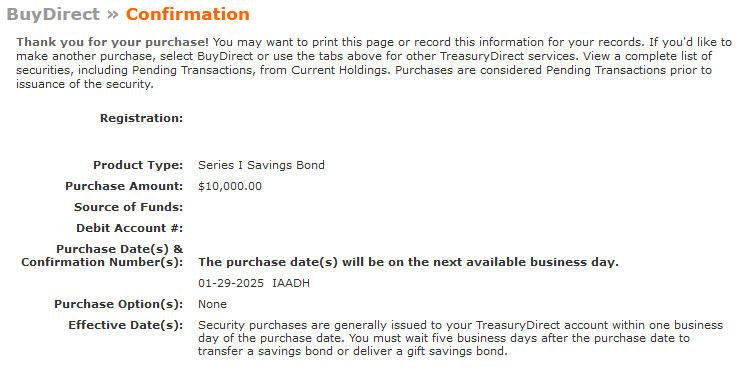

Update, Jan 31, 2025: I noted in this article that I was going to make a “test” I Bond purchase in January 2025 to see if it would trigger a purchase limit because of gift box deliveries in 2024. The transaction was scheduled for Jan. 29 and the money was withdrawn by the Treasury on that date. A day later, TreasuryDirect showed the I Bond in the account, dated Jan 1 2025. So it all worked without a hitch.

——-

I’m a big fan of all those Agatha Christie Poirot books, Sherlock Holmes, Philip Marlow, every episode of Columbo on TV. But even those great detectives would have a hard time figuring out TreasuryDirect.

So now we enter a new year, and the annual $10,000 per person purchase cap for U.S. Series I Savings Bonds has reset. But one big question remains for many investors: Can I buy I Bonds this year? And for others: When should I buy I Bonds this year? Or even … Why invest in I Bonds at all?

Just a reminder: An I Bond is a U.S. Treasury security that combines a permanent fixed interest rate with a six-month variable rate, creating an inflation-protected return. They can only be purchased in electronic form at TreasuryDirect.

Can I buy this year?

TreasuryDirect created a lot of confusion in October when it sent an email to investors holding I Bonds in a “gift box” for later delivery. The email seemed to urge delivery of those I Bonds “as soon as possible.” The email was strange, but it was authentic.

Read this for more information: “Deciphering TreasuryDirect’s mysterious gift-box email.”

The gift box program is a widely used loophole that allows people with a trusted partner (such as a spouse) to expand their purchases of I Bonds beyond the $10,000 per person limit. The idea in early 2024 was 1) buy gift I Bonds now to lock in the attractive 1.3% fixed rate, and then 2) deliver them in future years when the fixed rate is lower.

We all assumed one thing: You could not deliver gift I Bonds to anyone who had already purchased up to the limit in that year. TreasuryDirect’s email threw that assumption out the window. I called TreasuryDirect to try to get an explanation, and so did hundreds of my readers and fellow Bogleheads. We learned (unofficially):

- TreasuryDirect would like you to deliver gift I Bonds as soon as possible.

- It would be OK to deliver I Bonds to a person who had already reached the purchase cap.

- And … maybe (or maybe not) … the person receiving I Bonds over the limit would be locked out of buying I Bonds in future years, depending on the amount delivered.

- Unspecified “changes” may (or may not) be coming to the savings bond program.

In my case, last year: 1) My wife and I each bought one set of 1.3% I Bonds early in the year, along with two sets each for the gift box. After getting the Treasury’s directive, we successfully delivered those gift box purchases in November 2024.

Now it is January 2025 and I am ready find out: Am I subject to a purchase limitation this year? The answer apparently is “no.”

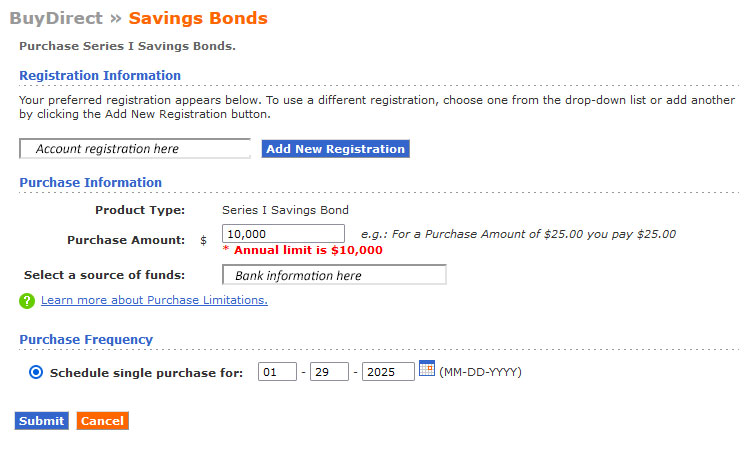

Last week, I logged into TreasuryDirect to place an I Bond order for my wife’s account:

Everything here is totally normal. Note that I set the purchase date for Jan. 29 because I Bonds earn interest for an entire month, no matter the day they are purchased. I clicked “submit,” looked at the review page and clicked submit again.

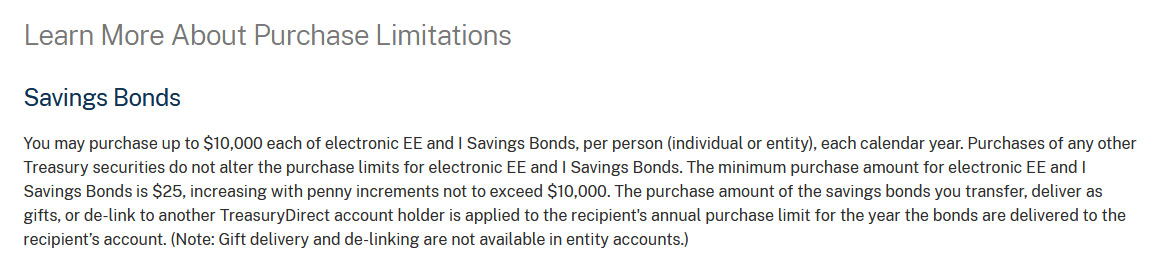

Again, totally normal. No warnings. No alerts. I think this purchase will go through on Jan. 29 as a routine transaction. Also, on the BuyDirect page, I noticed a link to “Learn more about Purchase Limitations.” I clicked and found this:

Notice this key wording: “The purchase amount of the savings bonds you transfer, deliver as gifts, or de-link to another TreasuryDirect account holder is applied to the recipient’s annual purchase limit for the year the bonds are delivered …”

My translation: If you receive $10,000 in gift I Bonds before you make your regular $10,000 purchase, you will not be able to buy more that year. But … if you make your regular purchase first, you can receive additional gift deliveries that year.

Important takeaway: If you are planning to deliver gift I Bonds this year, make sure to purchase your regular allocation before any delivery. Then, it appears, the gift I Bonds can still be delivered.

Also: If you made gift I Bond deliveries over the limit last year, you won’t be locked out of making a regular purchase in 2025. This is NOT official, but it is what I and others have experienced.

When should I buy I Bonds this year?

Although I set up a purchase for Jan. 29 to test my purchase theories, my usual advice would not be to buy in January, unless you feel the need to get the one-year-to-redemption clock ticking.

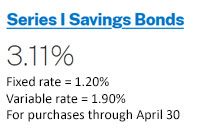

The current I Bond will pay 3.11% nominal for six months. You can do 100 basis points better in a decent money market account or high-yield savings account, for the time being. So there is no rush. Instead, be patient. I Bonds are a long-term investment.

April 10, 2025. We will get the March CPI report at 8:30 a.m. EDT, which will lock in the I Bond’s new six-month variable rate. We will also have a lot more information on whether the fixed rate will be likely to rise at the May 1 reset.

The period from April 10-28 is an ideal time to make a decision: Buy in April or buy in May, or continue waiting?

At this point, it looks possible the I Bond’s fixed rate could increase at the May 1 reset. For that to happen, using our back-of-the-envelope theory, the 5-year TIPS real yield would need to average at least 1.92% from November to April. That would get you back to 1.3%. At this writing, the 5-year TIPS is yielding 1.97%.

We won’t know until later this year. It is smart to wait. The variable rate is not a key factor in this decision, unless you want to make a short-term investment. The fixed rate is much more important for a long-term investor.

Oct. 15, 2025. The September inflation report will be issued on this day, locking in the next variable rate, and by then we will have information on the fixed rate reset coming Nov. 1. So the period from Oct. 15-29 is another potential “prime time” for an I Bond purchase.

Why invest in I Bonds at all?

Yes, at this point you can get a better nominal yield on a 13-week T-bill (4.36%) or a better real yield on a 5-year Treasury Inflation-Protected Security (1.97%). Both of those are attractive, safe investments. (And I invest in both.)

I Bonds, however, have unique qualities. They are an extremely safe and conservative investment. Interest accrues monthly and principal can never decline, even in times of deflation. Earnings are free of state income taxes and federal taxes can be deferred until the I Bond is redeemed or matures.

Also, I Bonds are a simple investment to buy and track, much simpler than a TIPS with a constantly changing market value and inflation accruals that update daily.

With an I Bond purchased today, you are guaranteed to earn 1.2% more than official U.S. inflation, with interest constantly compounding tax-deferred. You can redeem the I Bond after one year with a 3-month interest penalty, or after 5 years with no penalty.

My argument is that I Bonds should be viewed as a cash alternative in the form of a high-quality secondary emergency fund. You can let the principal grow without facing taxes, then after 5 years withdraw money as you need it, paying federal tax on the interest earned.

A lot of shorter-term, yield-hungry investors won’t see the appeal of I Bonds in 2025. That’s fine; there are great short-term options available right now. But many longer-term investors interested in building a sizable reserve of inflation-protected cash will want to buy I Bonds in 2025, up to the limit.

Rolling over 0.0% fixed-rate I Bonds

If you joined the mass movement into I Bonds back in October 2022, when the I Bond’s variable rate was about to reset from 9.62% to 6.48%, you are holding I Bonds with a fixed rate of 0.0% and your composite rate is going to be 1.90% for six months. That’s not a disaster, but many I Bond investors have been redeeming the 0.0% I Bonds and reinvesting the money into 1.3% or 1.2% fixed-rate versions over the last year. Or moving money into other investments.

That was the reason the gift box was so popular in recent years. Investors could redeem 0.0% sets, pay the tax on the interest, and then stash $10,000 into gift-box I Bonds to be delivered in future years. Then the Treasury set off chaos by encouraging these investors to deliver the gift-box bonds as soon as possible.

In the last two years, I have redeemed all our 0.0% fixed rate I Bonds and reinvested the money into the 1.3% or 1.2% versions (as of the scheduled Jan. 29 purchase). This makes sense for me, because I have large holdings in I Bonds and TIPS. Other people, still in the “accumulation phase” of I Bond investing, may want to hold the 0.0% versions and let them continue growing with inflation, tax-deferred.

The rollover process can be a little confusing, based on the limited information TreasuryDirect gives you for each holding. I wrote a guide back in September 2024.

“Just one more thing”

I think Treasury will make changes to the gift box program this year, but even if it doesn’t, I don’t plan to use it again in 2025. Under current rules, it appears that any amount of gift I Bonds can be delivered after an initial $10,000 purchase, Treasury has opened a gaping loophole, but only for people with a trusted partner.

What are your thoughts? Post your ideas and strategies in the comments section below. If you will bypass I Bonds this year, what alternatives are you considering?

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

thank you for the great info and forum!

We did the gift box (multiple) deliveries post regular $10,000 annual purchases in 2024-2025.

but I didn’t correctly deliver 1 of those 3 gifts, so need to deliver in 2026.

does same advice to buy in April 2016 for 2026 first $10,000 apply, then deliver the old gift box $10,000?

Pingback: Proven Retirement Income Strategies That Work in 2025 - Trend Nova World

Tipswatch: Would you please let us know if your January 29th purchase goes through.

I missed the boat on delivering our gift boxes in 2024 and I’m wondering what’s the best approach now. I converted all our prior 0% fixed rate bonds to giftboxes with 1.3% and we now have 4 giftboxes waiting in the sidelines.

I plan to max out the $10k this year. So if your Jan 29th purchase goes through I may just go ahead with the $10k purchase in Feb and deliver all 4 giftboxes right after. Unless Tipswatch or the community has a better advice for me to follow.

Thanks for all you do for our community.

Sure, but if I forget, remind me!

Did the purchase for I Bonds on the 29th go thru?

Yes, it did. I have updated the top of this article with information on that transaction.

Spouse and I redeemed all our I-bonds in 2024. Reinvested mostly in MYGA’s paying +6% interest. Used several providers so that we both stay below our state’s Insurance Guaranty Association maximum coverage amount. For short term, with immediate liquidity, I like high yield savings accounts, SGOV, FLTR and JAAA.

I just received a survey from the same research@ email that sent the “deliver asap” message… it was asking about a program change to gift giving:

The survey also asked if I had any undelivered gifts sitting around. I was able to say no 🙂

Wow. That is a strange development. I’d love to see the email but I haven’t gotten it yet.

You may be able to get there from the link below:

Yes, I posted the same thing a few minutes earlier below. Here is the key comment from TD included in the survey:

Gift Delivery/Acceptance Window

In the future, there may be a window of time in which a gift bond must be delivered and accepted. If the gift is not accepted within that timeframe, the gift bond would become the property of the gift giver and can be redeemed or kept by the gift giver. The following questions are about gift delivery timeframe.

8. What are your thoughts on this approach for gifting?

If they impose a 1-year limit for the gift being delivered and accepted it creates all sorts of potential problems, especially if the I Bond is just given back to the purchaser. How would the purchase limit be applied? This wasn’t a policy statement, so nothing can be determined from this questionnaire.

The survey offers a multiple choice response with options shorter than one year up to one year for a proposed gifting timeframe, with the opportunity to comment after you choose one of the options. I chose one year )the longest option) and suggested the $10K purchase limit was an impediment to gift delivery since the gift counts towards the purchase limit of the recipient.

It’s interesting to note that there was no question about the annual purchase limit at all. The entire survey focused on the gifting process.

Yes, returning gifts to the purchaser would create a new (even worse) loophole, especially since you can purchase gifts to an unlimited number of people.

Redeeming the gift purchase and returning the principal with minimal or no interest accrued back to the gift giver within the timeframe seems to solve that problem, if they go that route (if they even think of it).

I also just received this survey. Interestingly, when asked what is a reasonable time frame for someone to accept a gift, multiple options were given (1 week, 1 month, etc), but the highest “default” option was 1 year (there was also an “other” choice).

It appears to me they will are planning to close the gift program loophole that allows you to buy multiple years worth of future gifts, bypassing the yearly purchase limit.

It sounded like TD was addressing a gap between intent to deliver and acceptance by the recipient. This may come into play if the recipient doesn’t have a TD Account? Perhaps there is an issue where deliveries have been initiated, but the bonds are in a limbo state — not accepted. I didn’t get the impression they were trying to close any loopholes with the gift box program in general. Seems more of a program design vs. just a tech change as well.

Yes, the focus on gifts not being accepted seems to indicate TD is trying to find a solution to the problem. But it could also indicate it wants all gift I Bonds delivered as soon as possible, for reasons we don’t yet know.

A one year limit wouldn’t eliminate the loophole but it would severely restrict it by limiting it to two calendar years — the current one and the subsequent year — unless you could deliver multiple gifts beyond the $10K purchase limit.

Returning gifts to the purchaser over the purchase limit may create a new loophole.

So, I just got this email from Treasury Direct:

Subject: Help shape the future of TreasuryDirect

Dear TreasuryDirect customer,

The US Treasury is building a new experience for customers to purchase, manage and gift government securities and is seeking input on the experiences from current customers. If you are interested in participating in research that will inform and improve the future of purchasing and gifting government securities, please take this brief survey via SurveyMonkey.

https://www.surveymonkey.com/r/TGPHBXG?GG=1&GGN=2&PGN=4&UG=0&RG=0&RGN=0&UI=109448

Details: 17 questions. Estimated time to complete: 10 minutes

Please note that the US Treasury has not provided any information to SurveyMonkey, and that you may simply ignore this invitation if you do not wish to participate.

Thank you for your interest in helping improve the design of our products for all the public. We look forward to hearing your feedback!

If you have questions about the validity of this e-mail, please visit https://www.treasurydirect.gov/indiv/research/email/

U.S. Treasury Services

—

Please do not reply to this e-mail, this mailbox is not monitored.

I checked the link provided here and it is valid.

https://www.treasurydirect.gov/indiv/research/email/

This lends more credence to my website overhaul theory being behind the urgent gift delivery emails from the end of last year.

Hello David. I have an off-topic question I hope you can answer. Around 10 pm tonight I tried to place an order through Vanguard for the 3-year Treasury Note. The auction appeared to be closed; the Note didn’t have the usual link to click on to place the order. I’ve always been able to place an order the night before the auction, but not this time. Is it possible this is a VG fluke tonight or did something change with this auction’s dates?

You (or Vanguard) had the wrong date. That auction closed in the afternoon of Jan 6.

well I’ve been using the tentative auction schedule link from your blog roll for the last year and until this week the auctions closed according to that schedule. Even today when I look at the schedule it shows the three-year note was to close on the 7th. Is there another source you could recommend for upcoming auction dates?

Yes, I use the tentative schedules, too, to map out future TIPS auctions. About once every two or three years, Treasury changes the TIPS date, usually around the Thanksgiving / Christmas holidays. Or sometimes, just the auction closing time.

Those schedules are specifically listed as tentative. I would suggest verifying the auction date on the announce date at the latest. TreasuryDirect’s upcoming auction page can give you a little more advance on that.

https://www.treasurydirect.gov/auctions/upcoming/

Explanation for the change:

https://www.treasurydirect.gov/instit/annceresult/press/preanre/2025/SPL_20250102_1.pdf

thanks to you both. Makes sense the Carter observations would impact federal schedules.

Please take a look below – the wording is pretty straight forward about the issue of delivering gifts and that they would be included in the annual limit.

But, reading through the old posts and comments here – Is it true that some people were able to buy up to the limit in 2024 and then get an additional gift delivered in the same year?

eCFR :: 31 CFR Part 363 — Regulations Governing Securities Held in TreasuryDirect

§ 363.52 What is the principal amount of book-entry Series EE and Series I savings bonds that I may acquire in one year?

(a) The principal amount of book-entry savings bonds that you may acquire in any calendar year is limited to $10,000 for Series EE savings bonds and $10,000 for Series I savings bonds.

(b) Bonds purchased or transferred as gifts will be included in the computation of this limit for the account of the recipient for the year in which the bonds are delivered to the recipient.

(c) Bonds purchased as gifts or in a fiduciary capacity are not included in the computation for the purchaser. Bonds received due to the death of the registered owner are not included in the computation for the recipient.

(d) We reserve the right to take any action we deem necessary to adjust the excess, including the right to remove the excess bonds from your TreasuryDirect account and refund the payment price to your bank account of record using the ACH method of payment.

Yes, it is certainly true that people (including me) were able to buy to the limit and THEN deliver gift-box purchases in 2024. We delivered two each and TreasuryDirect actually seemed to encourage that.

These regulations say “gifts will be included in the computation of this limit for the account of the recipient for the year in which the bonds are delivered to the recipient.” That is the one clear statement of policy. So, reading this statement as literal, delivering a $10,000 gift will fill the purchase limit for the recipient. So no regular purchase will be allowed for the recipient after that. However … it doesn’t say that you can’t deliver gifts to a person who has already already reached the limit. It worked for me and many others, but this remains the “great mystery” and a loophole the Treasury will eventually have to reverse.

Ha-ha – talking about movies:

“The rules are… there ain’t no rules!”

My dad was a fan of Columbo and he became something of an acquired taste for me. (Columbo not my Dad) So I loved your last title “Just one more thing”.

My dad loved Columbo, too. During the Covid isolation, I watched every episode in order — also every Poirot and a many Miss Marples. Peter Falk had a great comic gift.

Impossible not to be delighted when the nun thinks Columbo is homeless.

Re: comparison of i-bonds and t-bills, has anyone else dabbled into “none of the above” e.g. fed farm 3130B4JS1 @5.65% mat. 1/35 1st call 7/25?

Sure, I think a lot of investors are grabbing up attractive nominal Treasurys and agency issues.

Would love to get some 1.2% fixed love, but not willing to take the 3 month hit again. Oh well….

For a short-term investment, you’d be better off with a 1-year T-bill yielding 4.18% vs an I Bond yielding 3.11% for six months and ? for six months, and then a three-month interest penalty on top of that.

By the way, my theory that the TD email was sent because they are migrating to a new website in 2025 which would require them to manually transfer gifts held in the gift box still holds. I have no inside information that this was their rationale, but it makes perfect sense in the website world. It’s much easier / less time-consuming / less expensive in man hours to have users to it for themselves. We shall see.

Maybe, but any migration could be quickly automated…and I don’t think the email served to reduce the gift box to zero. Many folks didn’t take any action. So they’d need to write and QA those migration scripts anyway…

Millions of Americans rushed to buy I Bonds back in the November 2021 – April 2022 period when the inflation rate soared to 7.12% and again in the May 2022 – October 2022 period when they reached a phenomenal 9.62%. Of course, those I Bonds had a 0% Fixed rate component but no one cared at those levels.

I was one of those people. My spouse and I shifted a decent amount of our cash savings to I Bonds using the Gift Box strategy. We started delivering the gifts in $10,000 increments in 2022 and thought we’d have to continue doing this on an annual basis for years to come.

Then we received the TD email to deliver those gifts by the end of 2024, which we did. This will save us a lot of of money now that I bonds are earning lower than market interest rates.

We redeemed some of those delivered gift I Bonds at the end of 2024 and will redeem the rest in 2025 to spread out the tax hit over multiple tax years. With the current I Bond inflation rate decreasing to 1.90%, the three month penalty is likely at its lowest point for short-term investors to exit this investment with minimal loss of interest to earn more in other investments.

That’s one piece of advice I suggest adding to your excellent summary. Short-term investors can always buy back into I Bonds if inflation spikes again. No need to hold those I Bonds any longer as a short-termer.

Good point. I thought strongly about writing about this issue when I was writing the piece, but eventually left it out. Now … I added it in. Thanks for the feedback.

👍

I never received the email from the treasury and so still have gifts in my and my partner’s gift box. I’ll probably keep holding for now and see if I want to purchase this year before deciding when to deliver the gifts.

I expect Trumpflation – tariffs, deporting workers essential to agriculture & construction etc, massive deficits from tax cuts. Plus likely Trumpcession.

I have $39,000 in 1.3% fixed iBonds & $1,000 in 0.9%. Just about enough for foreseeable emergencies, other than needing long term care.

I am liquidating stocks in my IRAs. In my Roth, I am buying 1/8% 2052 TIPS at a discount that will give me 180+% inflation adjustment tax free. (1/.5555). My heirs may get these, or I may resell if normalcy reappears.

I am buying nearer term discounted TIPS in my Traditional & SEP IRAs. Better than 100% inflation adjustment depending on the discount. I will either hold till maturity & use for RMDs or resell them if normalcy & sanity return.

in my cash account, I am buying TIPS from October 2025 (1/8%) till January 2028 (1/2%). These will be reinvested unless needed. It is hard to guess just how much economic and Financial chaos Trump will cause, but I see over 3% 5 year TIPS combined with 12+% inflation with 8+% unemployment as certainly possible. High inflation once in the CPI will likely mitigate 5 year TIPS unless the bond market is highly stressed. Buy Trump may well stress the bond market.

A variety of maturities within Trump/Vance’s term is one way to hedge my bets. The phantom income from TIPS inflation adjustments will hurt in my taxable holdings.

Some great bargains may appear within the stock market. Maturing TIPS are an ideal way to capitalize if they appear.

I sold 12% of my equities. Built up a cash reserve for five years for when we are both on Social Security pensions. Of course, I am entertaining the fantasy of buying back in when the market drops 20%.

The CDs that I bought at Fidelity don’t let me redeem them early. The portal makes me sell them, which means that I am playing the fixed-income market. I am keeping my funds in cash until I figure that out.

is there any chance the elimination of paper I bonds for tax refunds up to 5k will be restored and or switched to electronic form and or the annual purchase limit raised?

I don’t think paper I Bonds will ever come back. Too much administrative hassle. The purchase limit has been stable at $10,000 for 13 years. It should increase. We can always hope.

Many thanks for the continued valuable analysis. After much thought, we delivered all of our respective gifts in December. I continue to be enamoured with I Bonds and will be awaiting the 10 April CPI Report in order to determine timing of next purchase.

GVE

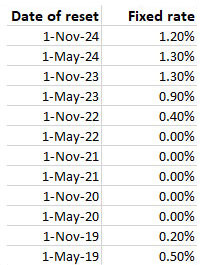

Help. My bookeeping is not super. Which of the I bond vintages over the last 4 years have a fixed component of 1.3 and 1.2? I know my earliest one does not have a fixed component, but need to be sure not to sell the ones with with the 1.3 and 1.2 fixed rates….UGH.

You need to know the date of purchase, of course. Do you have records of that?

UGH. THe TDirect site is down for maintenance…thanks for the list….most helpful, I forgot about the .90 fixed.

Maintenance can “sometimes” mean major changes in content. Or not.

They sent that “gift box” email in mid-October. Then the election happened. As a former government employee myself, I wouldn’t be surprised if all change efforts were paused or even cancelled. There will be a new Treasury head after all and they may not care one lick about changes to the iBond program (one way or the other).

This definitely could be true if we see a massive turnover in Treasury employees. For example, the decade-long, useful prediction for the I Bond’s fixed rate (0.65 * average 5-year real yield) may no longer hold. The one benefit of savings bonds for the Treasury is that interest rates are lower than market, and redemptions are off into the future, so that makes a case to keep them.

Well, my wife and I each delivered multiple $10k gifts to each other since the first of the year. I was glad to see it work, and was able to empty our gift boxes.

I was not ready to purchase I bonds yet this year, so we’ll see in April if it’s possible for us. If not, I guess we just buy more gifts? I really wish the treasury was more transparent with their plans.

This is the one scenario where the Treasury has given guidance: You shouldn’t be able to buy more in 2025. But nothing is certain with the Treasury.