By David Enna, Tipswatch.com

As I have noted many times in recent months, I believe there are changes coming in TreasuryDirect’s “gift box” program, which creates a loophole for buying I Bonds beyond the $10,000 per person annual limit for people with a trusted partner.

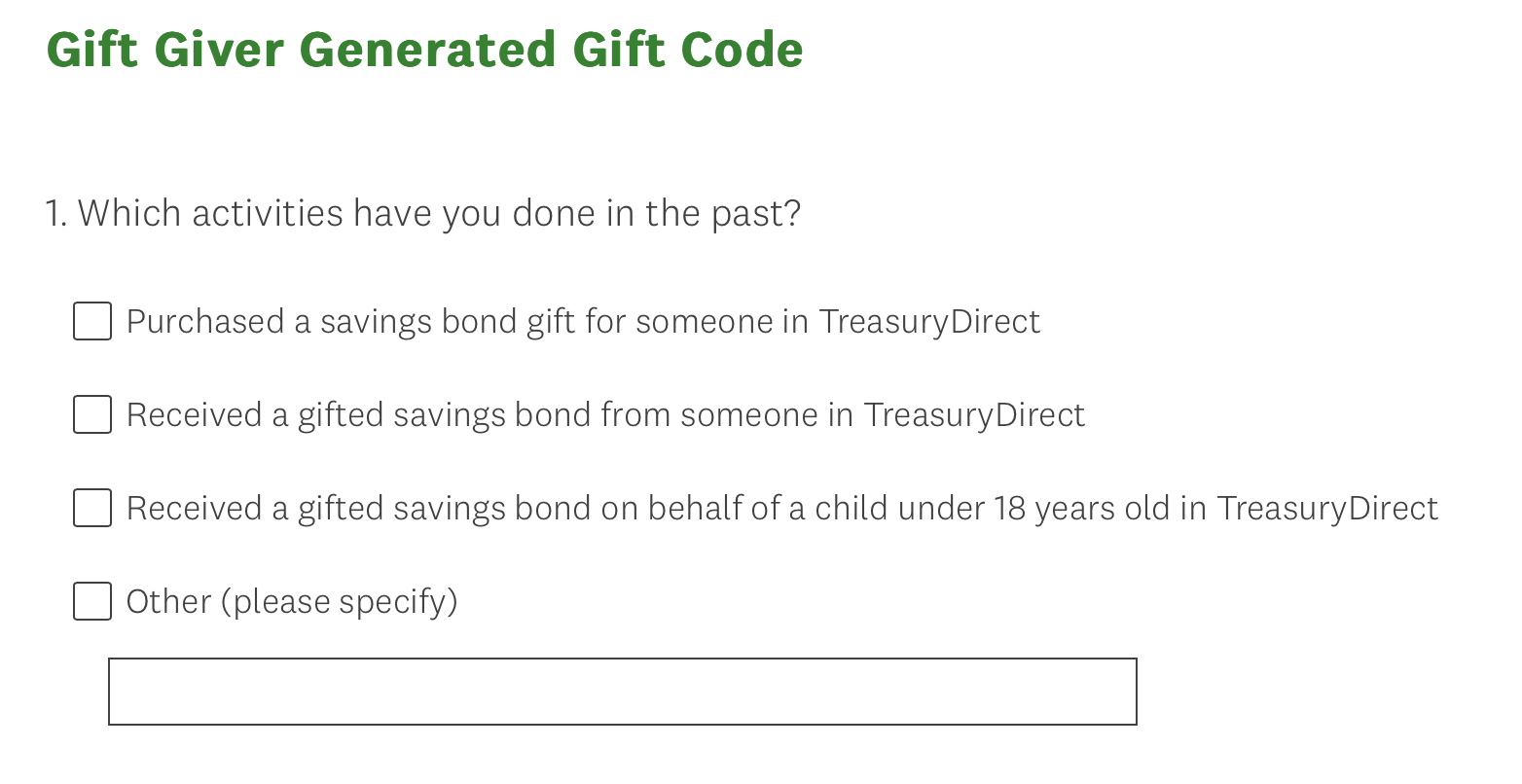

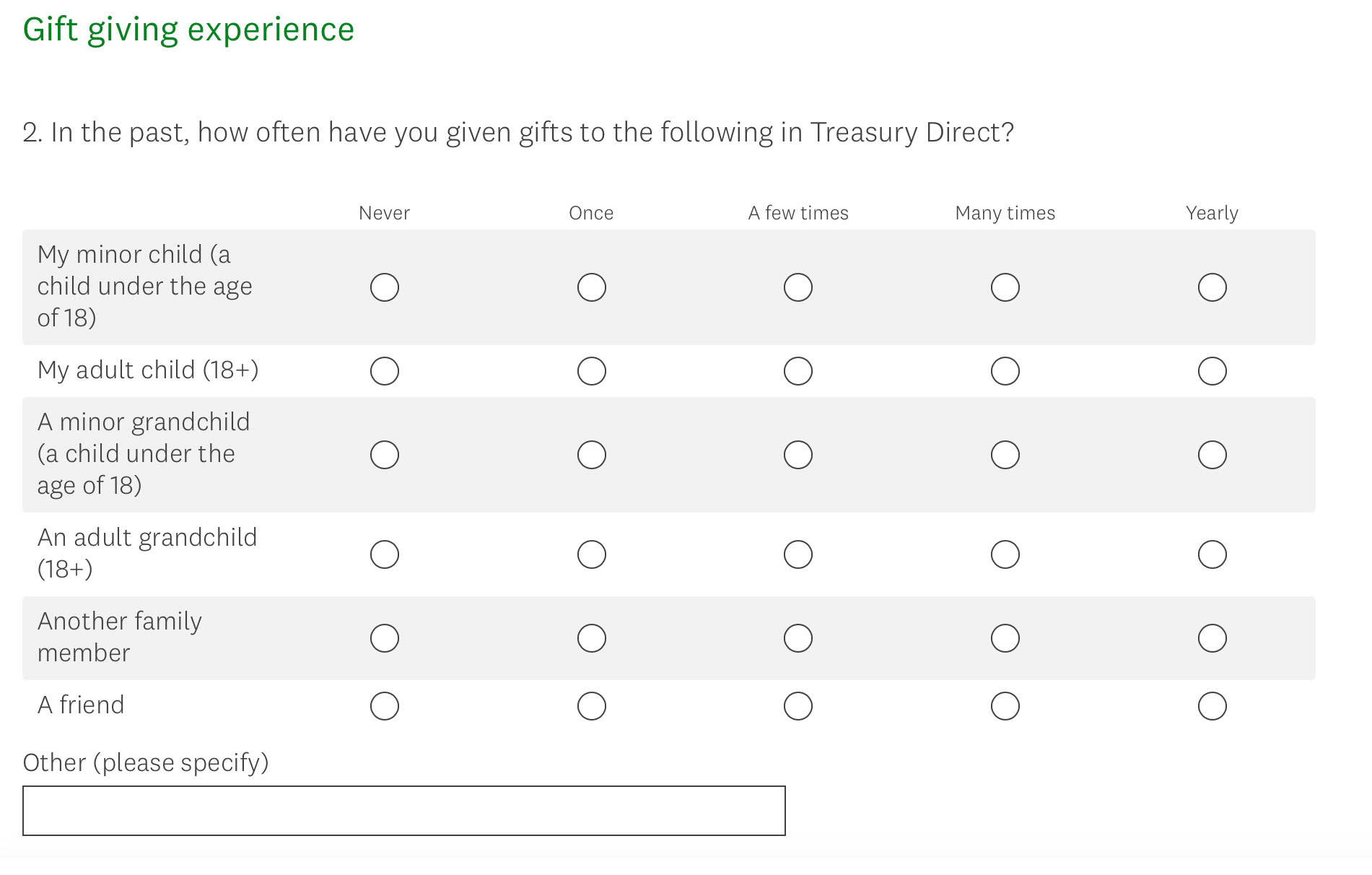

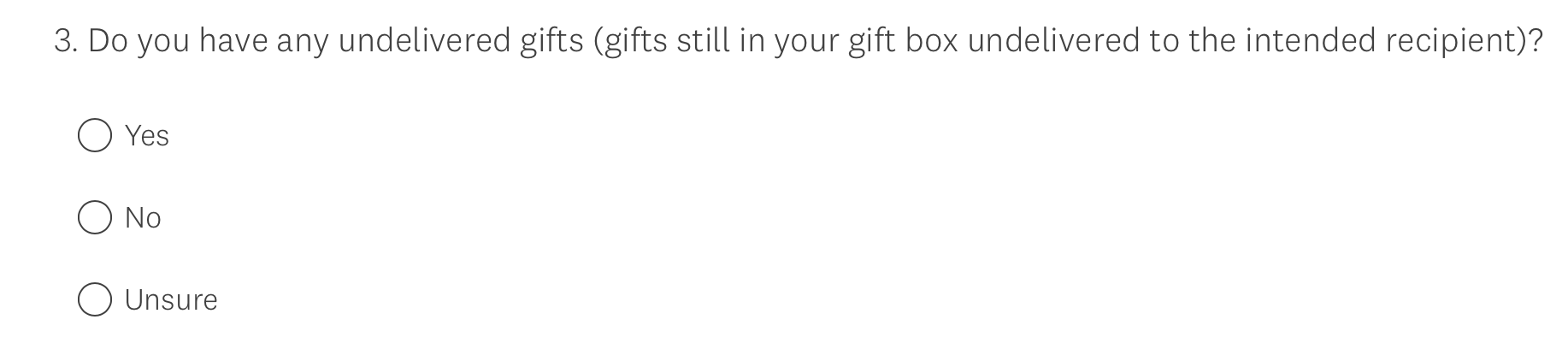

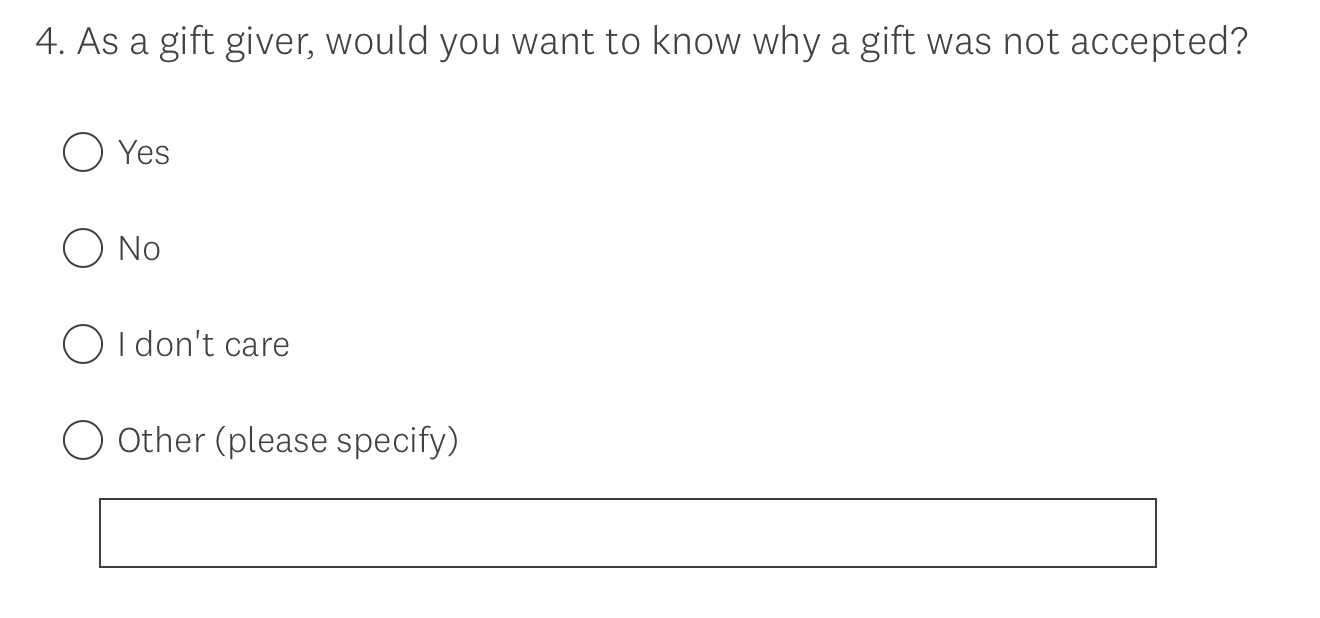

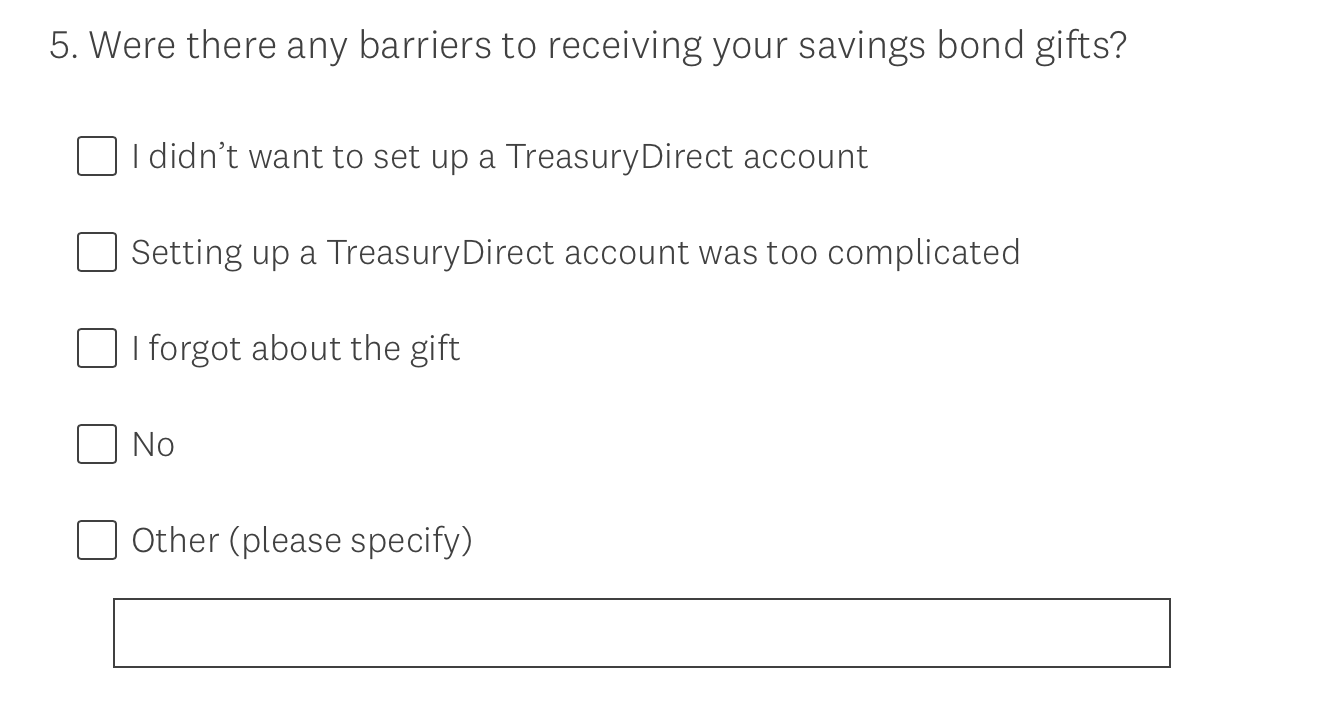

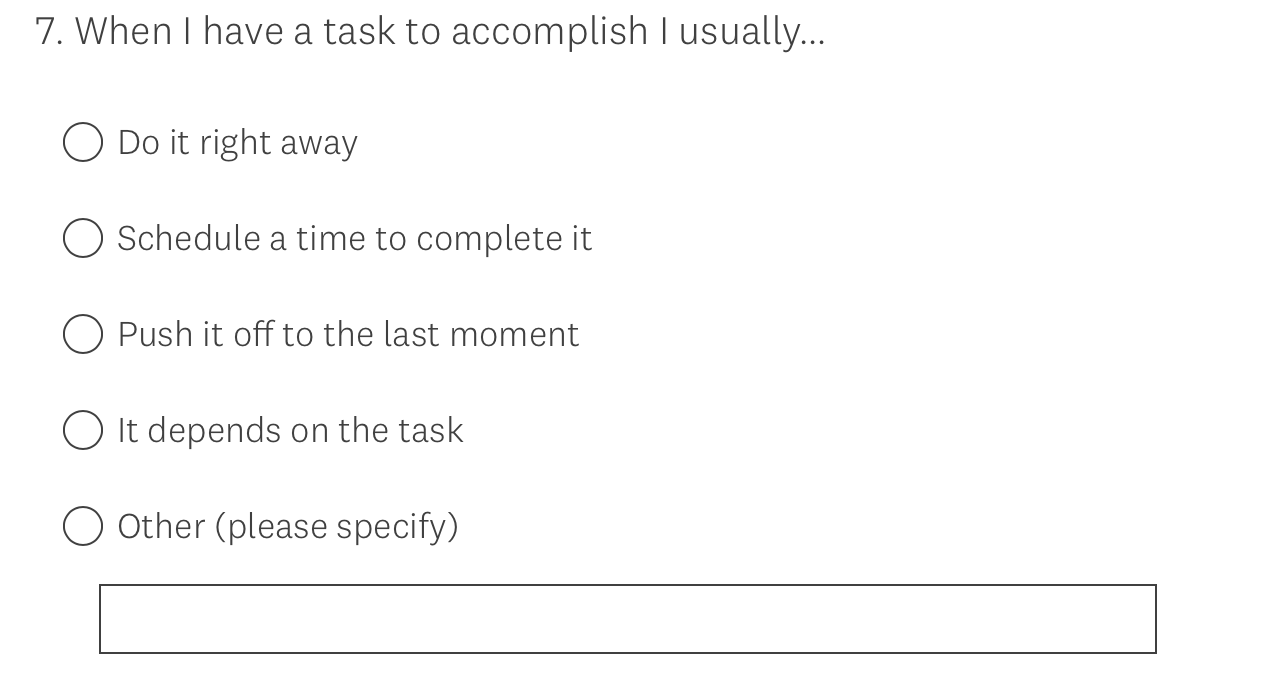

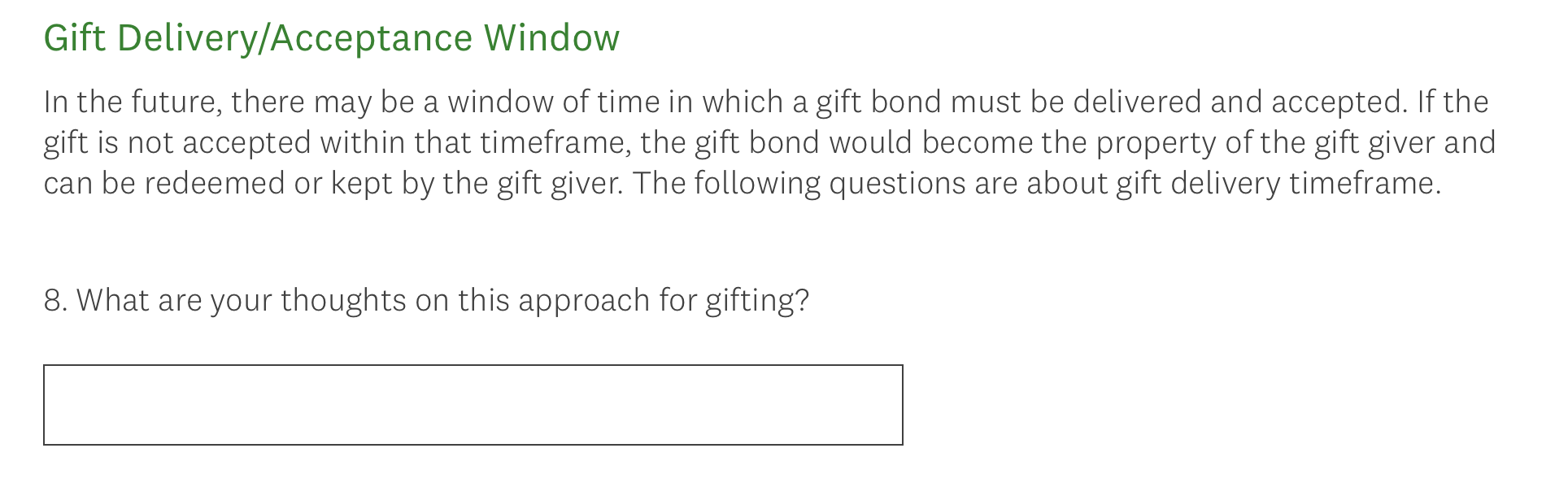

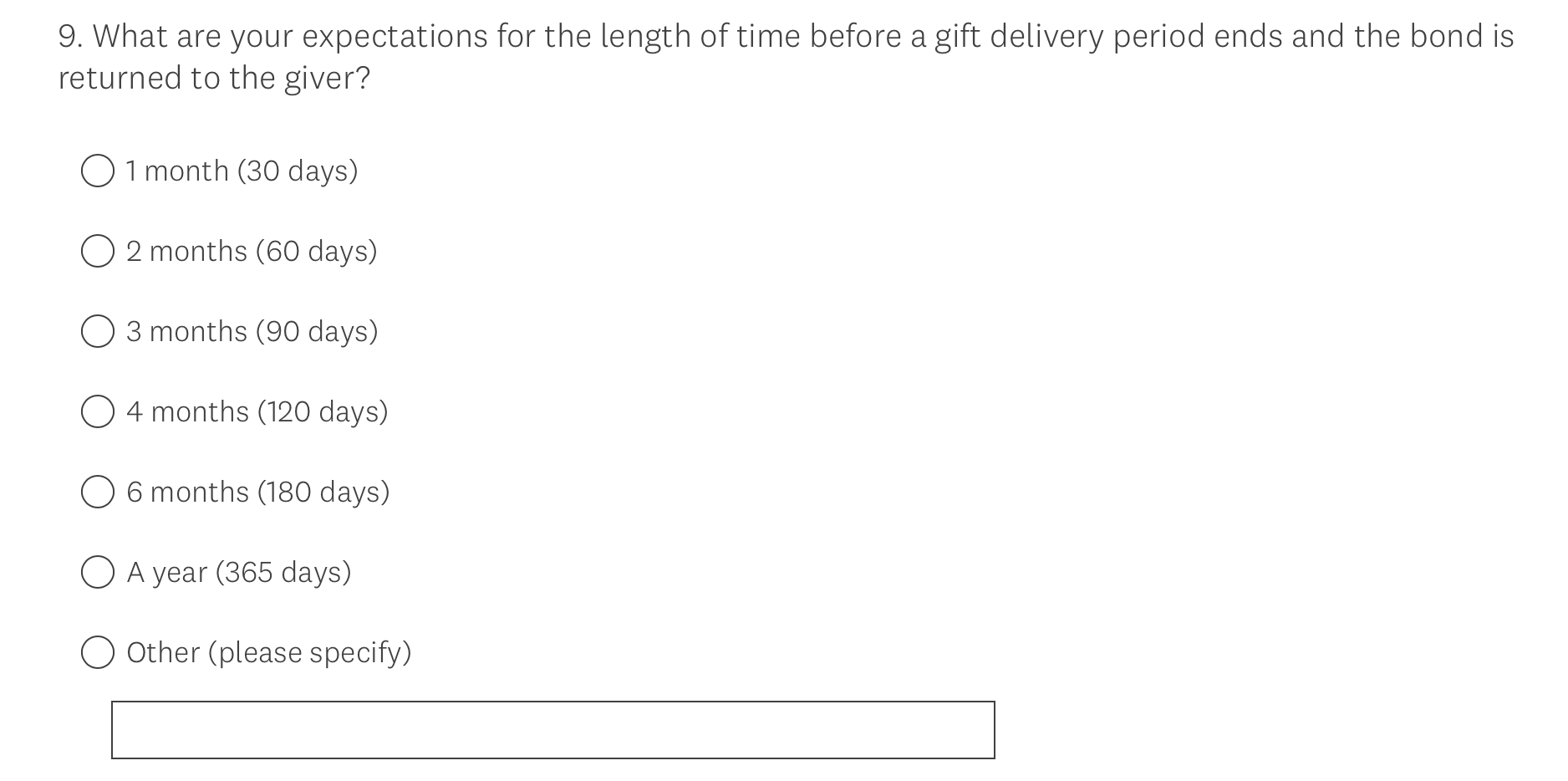

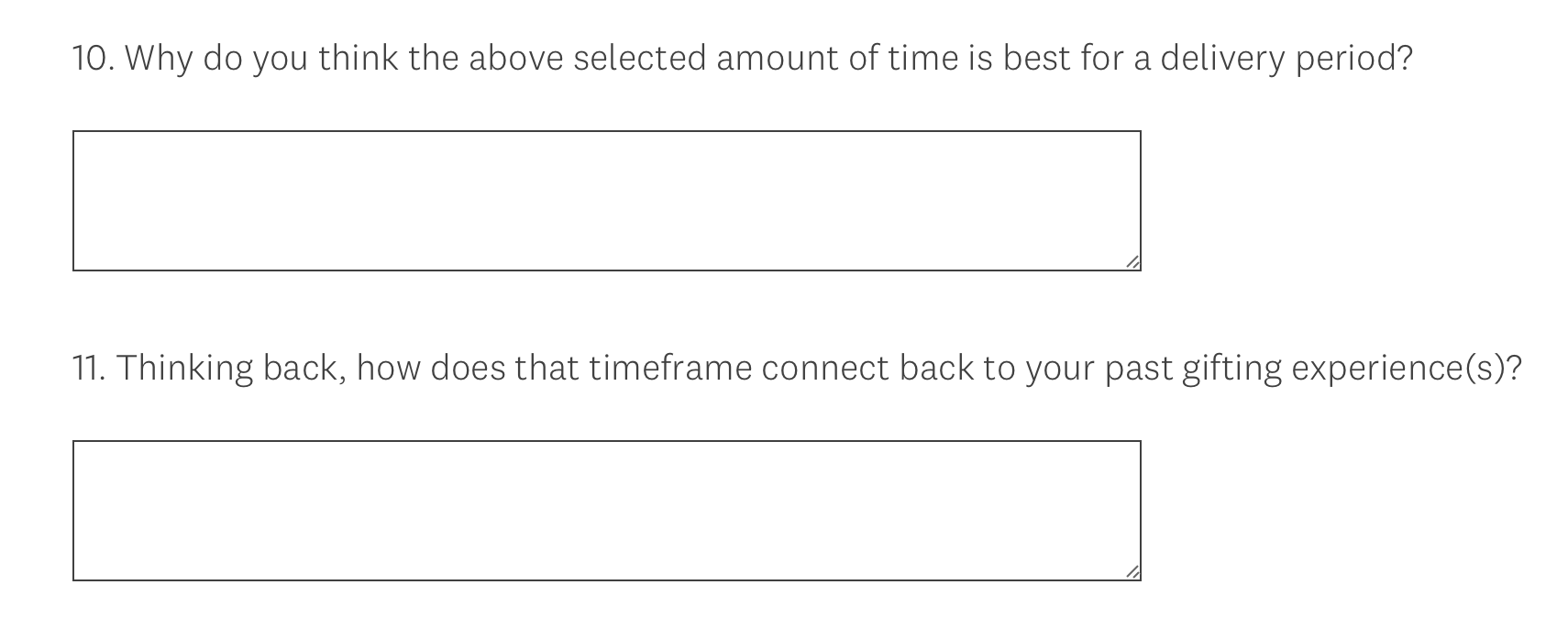

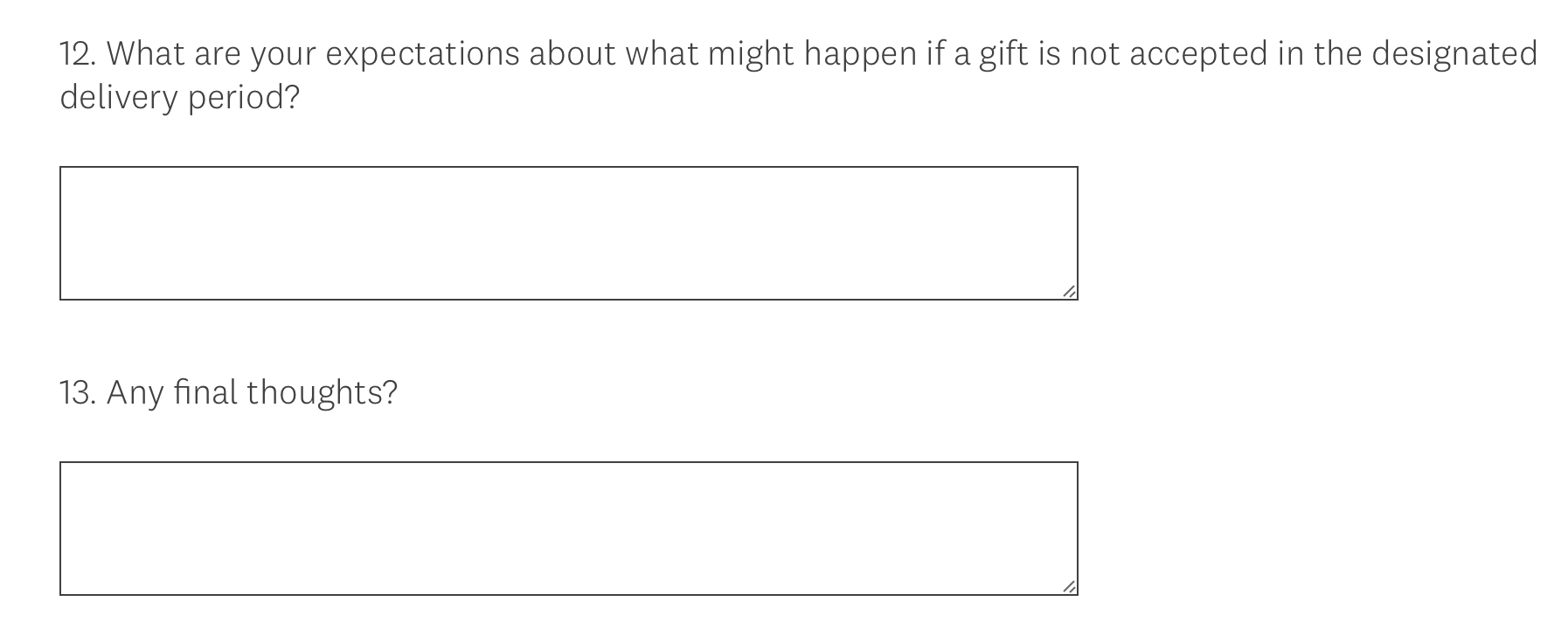

Today, TreasuryDirect began sending out an email asking investors to participate in a survey about the gift-box program. If you haven’t received the email, I am presenting the questions here for all of us to analyze:

Thoughts

I am still pondering what this means, but the core issue in the survey seems to be a new time limit on delivering bonds from the gift box. (There is no time limit now, and I Bonds in the gift box continue earning interest until delivered, possibly years in the future.) Some investors, I know, do not want a time limit, because these bonds are to be delivered to a child at some time in the future.

The Treasury has stipulated in the past that a gift box item is no longer the property of the giver. It can only be delivered to the recipient, who is actually the owner. But this survey seems to imply that savings bonds that aren’t delivered within some time frame (possibly up to a year) would be returned to the giver.

Returning the savings bond to the giver opens up another set of issues, but that’s too confusing to ponder with this limited information. As one Bogleheads commentator noted minutes ago:

That sounds like it’s opening up the door to gift yourself, which would be nice for unmarried people like me.

The survey also focuses on potential problems with gift-box bonds being accepted after being delivered, possibly because the recipient is unaware of the gift or does not have the required TreasuryDirect account.

And the survey really tells us nothing about the issue of using the gift box to add to holdings in a single year, bypassing the purchase limit if you have a trusted partner, such as a spouse. That’s the loophole I think should be closed, while at the same time raising the purchase limit to $20,000 per person per year.

I’m confused, but I’ve only had a few minutes to think about this. The discussion is now open. Join in with thoughts in the comments section. I will follow up with more information if I learn anything. Many thanks to readers who sent me alerts.

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Seems like there isn’t really an update on this – is everyone carrying on as before? Do you have a gift-box tutorial on the site? Trying to explain to a trusted partner… I also see the case for not making a tutorial (shining too much light on the loophole is likely to close it faster). Thank you for the gift of this site (wouldn’t be anywhere near my current level of understanding from subreddits alone – which is what initially put I-Bonds on my radar)!

That’s correct. I participated in the survey and that was the last Inheard of it. As for the Gift Box, this is, in my opinion, the definitive analysis of the I Bond Gift Box.

Buy I Bonds as a Gift: What Works and What Doesn’t

https://thefinancebuff.com/buy-i-bonds-as-gift.html

Is there any public data on gift boxes? What percentage of people use them? How much do people have pending? Are they usually for spouses, younger relatives, or does TD even have a way to tell that?

This community is definitely more focused on bypassing the annual limit than setting up gifts for grandkids, and it seems to be tainting our perspective. I don’t know if that perspective is actually the most common use case of the feature.

The reason this community is more focused on the annual purchase loophole than gifting to grandchildren etc. is because pure gifting is straightforward and the out use and delivery limit is somewhat ambiguous. This is also a blog to discuss inflation-protected investments more than gifts.

Following up with my earlier post…in the gift (other than spouse) perhaps TD is attempting to navigate around the present verse future “gift” for gift tax purposes. The annual gift tax exclusion is only applicable for present gifts. Conditional gifts are not subject that to exclusion and require filing of gift tax return with no tax due if generally within one’s lifetime exclusion.

I don’t know of any recent data on the use of gift boxes, but I am sure it surged after Dec 2021 when TheFinanceBuff.com discussed its uses. So every bit of the increase above normal levels of gifts since 2022 has been for bypassing purchasing limits.

I think the reason the limit was reduced and then allowed to get eaten up by inflation is because IBonds’ only constituency is small individual investors. Think about the constituency that hates IBonds — banks, brokers, mutual fund companies, insurance companies. etc. They all hate the fact that individual investors can invest directly with the govt for such an attractive investment product. No one in the investment community ever mentions IBonds to any of there investors. Wasn’t there an anchor on CNBC that hadn’t even heard of them? Good luck getting the limit increased with a govt bought and paid for by a financial industry that hates them.

I find the survey confusing and inconsistent and it could have been organized better so TD could better understand responses by audience groups.

The experience/objectives of a gift “giver” can be quite different from a gift “receiver”. Some people can be one or the other or both – which can lead to very different answers to survey questions. The survey should have been more clear and separated responses from a gift “giver” vs. a gift “receiver”. E.g. In question 5, a “giver” may be happy and content with the process, yet a “receiver” may be ignorant of the process. Also, it seems like maybe they should have differentiated “receivers” that are adults on behalf a minor vs. “receivers” that are adults receiving gift for themselves, since these can be different audience groups with different issues.

For TIPS watchers, its almost too bad they couldn’t have added had a direct question like, Are you using the gift box to bypass the $10,000 annual limit?

I probably won’t complete the survey in case they are tracking it be email. Thanks David for sharing this forum.

TD does not understand/appreciate the ramifications of gift tax law. For example, the survey suggests a gift purchase may be deemed revocable and consequently be deemed a future interest for gift tax law which would trigger a gift tax return being required! The annual gift tax exclusion is only applicable to transfers of present interests! Those who got the survey should ask for reconciliation

On this and other forums, I see commenters speculating on TD’s intent to close loopholes. I wonder if this is just our lens as beneficiaries of those loopholes. Instead, I think it’s more likely that TD doesn’t give a f* about loopholes and the minority of folks using them. If they cared, it would be super easy to enforce caps in the technology…they are under no obligation to send out surveys to enforce their own regulations. I think they’re trying to solve a problem related to bonds in a limbo state, which just happens to intersect with our gift box use case. Given that, it’s likely they may yet create more loopholes. And not really care about those either. Just my POV as a former gov (state) employee.

I would agree that, especially now, they don’t seem to care if you get around the 10K limit by having someone gift you an I Bond. The current wording by Treasury Direct seems to be deliberately vague on this point. And I wonder if in the end Treasury Direct is glad I Bonds have a dedicated group of fans like ourselves who keep the I Bond flame burning even when its allure has fizzled out due to inflation returning to a more reasonable level and thus I Bonds no longer wowing people. So if allowing loopholes for those in the know like ourselves to get over the 10K limit is the price the Treasury Direct has to pay (though I don’t think their suffering in any financial sense), then I think they don’t mind it at all.

The survey did not mention the $10K purchase limit, but it is an impediment for gifting and delivering I Bonds in a timely fashion because it counts towards the recipient’s purchase limit once delivered. It may not be an issue when buying a gift bond for a child or a grandchild who aren’t buying bonds themselves, but it is when gifting to an adult.

Many people have an issue with this limit. Why not separate the purchase limit from the gifting limit, and tie the gifting limit to the annual gift tax exclusion (currently $19K per recipient for 2025).

$10K annual purchase limit indexed to inflation)

$19K annual gift limit (indexed to the annual gift tax exclusion)

Deliver gift by the end of the calendar year it is purchased.

This would basically restore the original $30K limit ($29K in 2025) if combining the two limits, and index both limits for the future.

It also limits the delivery timeframe but in a flexible sliding scale way depending on when during the year you purchase the gift. This would allow for birthday or anniversary or high school graduation gifting during that year. Those that want to gift to a child years in advance can still do so within these rules.

To me, this creates a clear, transparent process, balances competing interests, and updates the limits in a way that makes sense.

I don’t understand not “accepting” a gift. Does this mean refusing or being unable to set up a TD account? I wonder how common that is.

Our grandson has not bothered to set up an account to receive the bond I informed him of last August. Of course, he can’t cash it until next August, if that is his plan. I think the answer here is procrastination. We helped two older grandchildren set up Schwab accounts, and they never bother to look at them (which might be a good thing…)

As it is, the gift box system forces Treasury to create legal trusts that can live “forever”. If I was the Treasury, I would not want to pile up paperwork-oriented legal obligations over the decades. After all, there is no extra charge for the gift-giving process: Treasury is building a bureaucratic time bomb without funding the cleanup crew.

Like many government agencies, I suspect Treasury Direct does not have the number of staff (not to mention the reasonable salaries to attract said competent staff) to handle the needs of it’s users. Case in point is dealing with gift delivery issues–not to mention people needing passwords reset, confirming basis for entity accounts, etc.

I Bond gifts seems an area they could more easily streamline so that there’s less headaches for them and what their limited staff can handle.

I got the survey request, too. My question is – Since bond owners lose 3 mo interest if redeemed in <5 yrs and can’t redeem it for the first yr unless for hardship, what is the driver for requiring delivery before 1 yr and think it’s reasonable to permit holding it up to 5 yrs before delivery? Heck I don’t even get why you can’t hold and gift at maturity (especially if the recipient were an infant). If that person refuses it then you should get the P&I to that point. Re:the loopholes, folks are not exactly making a mint at this rate and you can buy 30 yr t-bonds, so what’s the issue?

this is such a silly next step by the treasury. talk about useless and not addressing the real issue. I don’t know what manager or dept is making these silly choices but I’m sure the employees/developers are also shaking their heads at this impractical use of everyone’s time.

I gave 3 gifts I had built up to spouse in 2024 and will try to buy another 10k in 2025 and maybe even another gift each. If the loop hole is still there, I’m going to use it.

Maybe you all answered this. If i maxed out my personal annual purchase limit ($10000) in January and i buy a gift of $10000 for somebody, who decides in December he or she does not want it, where does that gift money and accumulated interest go? If it all goes back to me in the form of cash, do I suffer a three month interest penalty?

Why are there limits on iBond purchases in the first place? There are no limits on treasury bonds, bills or tips. Why with iBonds?

Except for gift giving to children/grand children, etc couldn’t all this be avoided by just eliminating the arbitrary 10k limit that by the way has not been increased to keep pace with inflation.

Yes, but I don’t the the limit will be entirely eliminated. It should definitely be higher, however, at least $20,000.

Limit used to be $30000, as you know, Why they lowered it to $10000 is beyond me. And why is it not inflation adjusted each year? All part of the many mysteries of Ibonds.

The official explanation for the reduction from the former $30,000 per year to $10,000 per year was that wealthy people were “backing up the truck” to buy I Bonds (and, at the time, could even buy them with a points-earning credit card, but that the Savings Bond program was intended, all the way back to its inception, as a vehicle for small savers.

I agree with Patrick, for what that is worth. Besides, what exactly is a “small investor” anyway? Furthermore, why not just create a version of TIPS with all of the features of I-bonds? For a government with $30+ trillion in debt now, why be so picky and bureaucratic about how willing “small investors” behave anyway?

The Treasury is setting I Bonds fixed rate in a way that is actuarily sound given that the I Bond can be held for up to 30 years or cashed out after 1. So it’s not like the government is losing money on these things. That being said, I see nothing wrong with increasing the yearly limit to 30K or even 50K or even higher. Either way, we have helping finance the government debt in a fair way. It’s not like the government is giving us an extra generous fixed rate, quite the opposite in my opinion. And that’s the trade off many us agree to so that we can have a safe, inflation-adjusted, and (after one-year) very liquid investment. And I think if the limit were raised, more people would see the benefit of utilizing I Bonds as part of their savings.

As the popularity of Tipswatch suggests (not to mention the Boggle heads groups on the subject), there is clearly a significant number of people who value what I Bonds can offer them. Yes many of these people are probably solidly middle or upper middle class but unlikely wealthy rich folks. Shouldn’t our needs, especially when they are not costing the government any money but are helping financing the federal debt, also be considered. I think if they really wanted to target I Bonds to less financially advantaged individuals then they should strictly enforce the 10K limit and the loopholes around, and offer a more satisfying fixed rate–even if it means the government is losing some money in the process. For example instead of the current 1.2 % fixed rate, how about a 1.7% fixed rate?

I have always noted that “a lot of wealthy people invest in I Bonds.” Sure, not the super rich, but well-off investors looking for capital preservation, especially against inflation.

Gift codes like other gift cards? Short expiration dates? Seriously? Like the gift cards that required laws put in place to protect consumers from unreasonable fees and expirations? They have expiration timeframes of at least 5 years by law. I know that savings bond gifting isn’t the same as retail gift cards, but this seems like a big step backwards that opens a lot of complications. Must be a federal government idea.

The form was sent by email. Is the response anonymous, or will they know the identity of the respondent? Some of the questions seem awful nosey, like a lawyer fishing for something. I would be reluctant to respond to a form like this.

Seems all kinds of legal issues might arise over the meaning of a gift if it can be returned to you and become your property. Collusion anyone? With no intent to avoid the purchase limit, I bought an I bond to give to my grandson in May 2026 for his college graduation. It will be most annoying to have to present it sooner, or take it back.

Obviously the key takeaway from the survey is the possible imposition of a gift delivery timeframe. I completed the survey and chose the longest default option which was one year. I commented that a notification to the gift giver and recipient before returning the gift to the purchaser would be appropriate. I also noted that the $10K purchase limit is an impediment to gift delivery since the gift applies to the purchase limit of the recipient in the year of receipt.

BTW, I thought Question 7 was not only superfluous but inappropriate. I’m not sure how that data is a relevant question to ask or how the answer affects the program.

In the survey reproduced above, the last answer to question 9 (on the time frame) is “other (please specify)”. If I receive the survey (doubtful because I didn’t get the earlier message about gifting gift box bonds as soon as possible) I’m going to put down something like 5 or 10 years. Mostly because aside from a way to load up on attractive rates, I view the gift box as a good way of storing bonds for milestone gifts. You might want to make a gift of a bond that could be cashed immediately without penalty (except for the income taxes, lol).

Agree that question 7 is ridiculous, and imo question 6 is not really appropriate either. One of my suspicions is that Treasury has decided to make changes, that most or all of them are already decided, and they hired a contractor to make a token survey so they could say they consulted with their customers. Perhaps too cynical!

My immediate take on it is that they are going to impose a limit as you said, probably to close the $10k limit loophole. Notice that there was no separate spouse/partner section in the how often have you given gifts question. The rest of it seemed to be aimed towards working out the mechanics of how a limit might work. The bit about what might happen if it isn’t accepted in the given time frame is interesting. Much like now, they’d have to accumulate interest and inflation adjustments from the time they are purchased. The money can’t just disappear, so they’d either have to give it back with interest or allow you to re-send it – presumably to the same person since there might not be anyone else you’d want to gift it to. If so, perhaps one could just keep resetting the clock until they are ready for their spouse to accept it.

Russ you said “Much like now, they’d have to accumulate interest and inflation adjustments from the time they are purchased. The money can’t just disappear, so they’d either have to give it back with interest“.

I had purchased a paper savings bond for a grandchild when they were born using their fathers SSN. Due to life’s circumstances, I wrote to Treasury and asked if I could redeem it because it couldn’t be delivered. They redeemed it for me at the price I paid, which was half of the face value of the bond. So, they CAN make the “money disappear”. I got no interest for over 10 years of holding the bond.

I am sorry for your sadness and I want to comment with additional perspective. Since gifting is irrevocable in the law if there was not a successor or next of kin to receive the principal and interest, then refunding the purchase price was a courtesy and not an obligation.