5-year real yields are declining. What does it mean for TIPS and I Bonds?

By David Enna, Tipswatch.com

April 11, 2025, update: Welcome to the I Bond ‘buying season’

April 10, 2025, update: I Bond’s variable rate will rise to 2.86% on May 1

April 3, 2025, update: My I Bond fixed-rate projection just fell to 1.10%

I’ve just returned from 3+ weeks in very southern South America — much of the time with limited internet access — and gosh, you folks have been busy.

Tariffs on. Tariffs off. Stock market down, up, then down. Treasury yields all over the place. Although I could monitor news some of the time, I am a bit lost about what’s been happening.

During that time away, I had three interview requests from separate Wall Street Journal reporters, plus NPR and Bottom Line. Something was triggering interest. At least twice during the trip, I noticed the 5-year real yield had fallen midday to 1.30%, down from 1.74% when I left on February 10. Things have stabilized a bit, but volatility is obviously a key market factor in March 2025.

In this brief time, the real yield of a 5-year Treasury Inflation-Protected Security has fallen much farther than the yield of the 10-year TIPS. Note in this one-year chart how the two yields tracked closely until October 2024, and then have widened dramatically:

The gap between the current 5-year real yield (1.57%) and the 10-year (1.99%) has been partially caused by higher inflation expectations over the next 5 years, now at 2.57%, compared with the 10-year inflation expectation at 2.35%. For a long period of 2024, the 10-year inflation breakeven rate was running higher than the 5-year.

Markets are concerned about future inflation, and that increases demand for TIPS, which in turn lowers yields. From a Bloomberg article this week:

But rising inflation is a real possibility now even if many investors are bracing for rate cuts, said Nicolas Trindade, who runs a number of funds at AXA Investment Managers. He expects volatility to increase amid the unpredictable economic strategy.

“The main risk for 2025 is a sharp resurgence in US inflation on the back of tariffs, tax cuts and immigration restrictions that could lead the Fed to open the door to hiking interest rates again,” he said. “The market is definitely not priced for that.”

This comparison of the real yields is important now for several reasons:

- On March 20, the Treasury will reopen a 10-year TIPS at auction. The real yield at this point would be 1.99%, a decline from 2.243% at the originating auction on Jan. 23. That’s down about 25 basis points.

- Then, on April 17, a new 5-year TIPS will be issued at auction. At this point the real yield looks likely to be about 55 basis points lower than the 2.121% set in the last auction of this term, a reopening on Dec. 19, 2024.

- And two weeks after that auction, the Treasury will reset the I Bond’s fixed interest rate for purchases from May to October 2025. My analysis of data through March 7 indicates the new fixed rate could hold at 1.20%, or potentially drop to 1.10%.

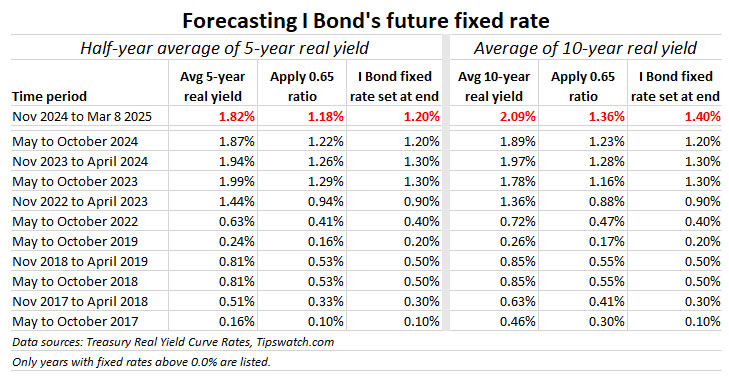

The 5-year real yield is key

The Treasury has never revealed a formula for setting the I Bond’s fixed rate, but it has stated it looks at real yield trends over time. TreasuryDirect has provided this cryptic information:

The Secretary of the Treasury, or the Secretary’s designee, determines the fixed rate. The rate is based on market rates that have been adjusted to account for the value of components unique to savings bonds. These include the early redemption put option, tax deferral feature, deferred purchase feature, and Treasury’s administrative costs.

I Bond watchers have observed that over the last decade one formula has accurately predicted the Treasury’s fixed rate decision: Apply a ratio of 0.65 to the average 5-year real yield over the preceding six months. This formula has worked without fail at least since 2017.

So now I am going to use that formula to look at how recent declining real yields could affect the Treasury’s May 1 decision. Here are the data:

I include the 10-year TIPS data in this chart simply as a back-check, but it is interesting to note that 10-year real yields would point to a higher fixed rate of 1.40%. (The fixed rate is always rounded to the one-tenth decimal.) But … ignore that. The 10-year real yield hasn’t been a reliable indicator of the rate reset.

At this point, as of March 7, 2025, the average real yield of a 5-year TIPS since November 1, 2024, has been 1.82%, much higher than the current rate of 1.57%. Applying a ratio of 0.65 to 1.82% gets you to 1.18%, which rounds to 1.20%, same as the current fixed rate.

So, yes, the fixed rate could hold at 1.20%.

But what if the 5-year real yield stays around this 1.57% level through April, or goes lower? If that happens, the I Bond’s fixed rate is likely to decline to 1.10%, at least. There are 57 market days remaining until late April. If you add in 57 days at 1.57%, the real yield average drops to 1.132%, which would round to 1.10%.

So, yes, the fixed rate could drop to 1.10%.

What we don’t know

The Trump administration could decide to ditch the long-standing formula for setting the I Bond’s fixed rate. That is certainly possible. Remember, there is no set formula required by law. Keep that in mind.

Or, maybe it could eliminate the savings bond program entirely, cutting off all new issues? Highly improbable, I’d say.

Also, real yields have been highly volatile over the last month and may continue to rise and fall unpredictably. We’ll have more certainty by mid-April.

Also read: A great mystery: I Bond buying guide for 2025

Suggested strategy: Wait

Maybe you haven’t noticed, but I Bonds are getting more and more attractive as the 5-year TIPS yield declines. An I Bond can be redeemed after 5 years with no penalty, so it is directly comparable to a 5-year TIPS, but has advantages of tax deferral, better deflation protection and no market fluctuations.

An I Bond with a fixed rate of 1.20% is more attractive than a TIPS with a real yield of 1.30% or 1.40%, in my opinion. So if TIPS yields continue declining, I Bonds with a fixed rate of 1.20% — or even 1.10% — will remain attractive.

My opinion: The best strategy for investing in I Bonds in 2025 is to wait at least until April 10, when the March inflation report will be released. Then you will know for certain what the new variable rate will be (probably higher than the current 1.90%) and have a better idea of the potential fixed-rate reset.

I am thinking an investment near the end of April will make the most sense. There is no harm in waiting. But if the fixed rate looks likely to rise, May would be the better choice. I will have more to say on this topic in mid-April.

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I bought an Ibond 2.5 years ago on advice from a Financial Advisor because the rate was over 9%. Now it is 1.9%. If I knew this I would not have gotten it. I’m thinking of withdrawing it and taking the penalty and putting it into my High Yield savings account at 4.3%. Question is would I be ahead by doing this?

Given the current administration’s pro-inflationary fiscal policies I’d hold on to it with both fists tightly clenched.

Is it possible in the last few days of April for the fixed rate prediction on the I Bond to get bumped to 1.2%? Real yields on the 5-year TIPS are skyrocketing…

It’s not likely using the forecast formula, with just a market few days left until the reset. As of Monday’s close the 0.65 ratio was coming up with 1.137%, which pretty solidly puts the forecast at 1.10% rounded. (Of course, we don’t know exactly how the Treasury will make this decision.)

If you want a short-term investment and aren’t looking for longer-term inflation protection, sure. That financial adviser did well, however. If you purchased that I Bond (0.0% fixed rate) in the October 2022 rush, you have earned about an 4.7% annual return. If you purchased it earlier, in April 2022, you have had a 5.0% annual return. But now the yield is probably 1.9% and will transition to 2.86% for six months.

Thanks for the replies. I bought it July 2, 2022 for the full 10 grand. From what I have been reading it looks like it will not get to about 3% return anytime soon. I am not a knowledgeable investor. I’m now thinking about a 15 month CD with a rate of 4.35%. I’m retired and are not looking for withdrawal anytime within the next 3 years or more.

A July 2022 I Bond will continue with the 1.9% composite rate through June and then transition to 2.86% through December. If you redeem you will lose the latest 3 months of interest and owe taxes on the interest earned.

It seems like no presidential administration ever wants to take advantage of the US Savings Bond program. Why can’t the Trump administration tell the Treasury department to set the EE Bond rate at 5%? This would be in effect subsidizing US Bond savers with above market interest rates. But the current 2.5% rate for EE Bonds is actually letting the government pay below market rates to savers.

Steven,

The rate on EE Bonds used to be indexed to 90% of the going market rate on recent 5-year Treasury Notes. Then the government switched to a periodically re-set but arbitrarily determined permanent fixed rate for each round of new bond issues, accompanied by a guarantee that the bond will at least double in value if held for 20 years.

The federal government IS “taking advantage of” EE Bond buyers–although not in the way you intend your comment. It’s accepting money from people who are willing to buy at inferior below-market rates, thus cutting the government’s own interest costs to finance the national debt. And I imagine that a very substantial number of those EE Bond buyers will redeem before the doubling point.

I consider EE Bonds such a bad deal that I’ve never been able to understand why anyone would buy them.

TChat, there was a time a few years ago when that 3.53% yield was much better than the 20-year Treasury, which started 2021 at 1.46%. So some investors bought in, knowing their money would double to a fixed nominal amount in 20 years. (And probably exceed inflation, too.) But I could never justify a purchase in that era.

The current EE rate is 2.6% with doubling after 20 years, for an effective yield of 3.53%. That is dismal. This savings bond is a relic. I think the fixed rate is fine, but the doubling period should be reduced to 16 (4.5%) or at least 18 years (4%) to reflect current market trends. The 20-year Treasury currently yields 4.64%.

Do you have any thoughts about the actual date range for the 5-year bond average that is used to calculate the I-bond fixed rate? The range may be six months long, but it’s probably not Nov 1, 2024 through Apr 30, 2025 (for the upcoming fixed rate setting on May 1) because someone has to formally set the rate, probably several days ahead of time. Might the date range actually be something like Oct 16 through Apr 15, for example; or Oct 1 through March 31? This sounds like a nit, but if you look at the past 5 cycles, a shift in the range by more than a few days can make a difference.

I just use (in this case) Nov 1 to the latest day possible in April, which would be around April 28 or 29. I know some Bogleheads have tried to play around with the six-month period, and they could be right. But because the fixed rate gets rounded to the one-tenth decimal point, it takes a fairly big shift to make a change. Right now, the average since Nov. 1 is 1.802%, which after the ratio is applied becomes 1.1718, or 1.2% rounded. If you add in dates since Oct. 15, the average is 1.793%, which after the ratio is applied is 1.1660%, which also rounds to 1.2%. In the closing days of April, the date range could make a difference, possibly.

The graph from the FRED showing 5 year and 10 year real yields was very informative and I would like to see the comparison in the future. Would you please post the link to it.

I keep a 5-10-30 year chart stored at FRED: https://fred.stlouisfed.org/graph/?graph_id=910716&rn=229 You can play around with the dates and you should find what you need.

Thank you

Thank you! A note: the logistics of getting cash into Treasury Direct can be frustrating. I will start replenishing my buying fund now, and prepare to buy in April.

Cheers!

I’m curious why it is frustrating for you. Presumably you move the money in to Treasury Direct from a linked bank account. If you are only moving it into the 0% Certificate of Indebtedness to park it until your purchase, I believe you are limited to $1000 per transaction. However that limit doesn’t apply if you use a linked bank account as the source of funds for a purchase. Or am I misunderstanding the source of your frustration?

You are correct! I have only used the Certificate of Indebtedness method, not the direct purchase method. Thank you, I will test it.

Yes, as Paul notes, using a linked bank account (or brokerage’s bank account) makes the process quite easy, for both purchasing and redemptions.

As Tipswatch and Paul R. have noted, the process of buying or redeeming I Bonds is indeed easy for anyone who can so so, strictly on a self-service basis, using a linked account. But for anything requiring action by a human TreasuryDirect employee, the wait can seem interminable.

Personal example: In Spring 2024, my wife and I received a single paper I Bond in lieu of cash as part of our 2023 federal income tax refund. (Treasury abolished that option after 2024.) We filed the TreasuryDirect form to convert that bond to electronic format and have it moved into our TreasuryDirect joint trust account. TreasuryDirect acknowledged receipt of that request, and assigned it a case number, in early August 2024. We’re still waiting. Knowing that TreasuryDirect is chronically understaffed–it’s not the first time we’ve had this experience–I nevertheless called TD last month, provided the case number, and asked if there was any problem. Answer: No, the request is just waiting in the queue for action.

There’s an ongoing Bogleheads thread on this topic, in which a number of people express particular concern about whether such prolonged TreasuryDirect delays will represent a nightmare for anyone trying to settle a TreasuryDirect customer’s estate. Some of the posters are liquidating their TreasuryDirect accounts for that, and other, reasons.

https://www.bogleheads.org/forum/viewtopic.php?f=1&t=402682

When news reports first came out about the workforce-slashing/systems-invading activities of Elon Musk’s so-called department of government efficiency, one of the first federal agencies mentioned was the Treasury Department’s Bureau of Fiscal Service, which, among other things, operates TreasuryDirect. So I think that any optimism about increased staffing and decreased processing time at TreasuryDirect would be unwise. Things will probably get even worse, not better.

I have had some feedback from readers dealing with estate issues who say TreasuryDirect is no longer answering the phone (and callers get a busy signal). That could have been a temporary disruption. In the last couple years, after the I Bond debacle in October 2022, TD has stepped up its customer service (of course demand was also lower). Now those improvements are probably slipping away. Estate issue were never going to be easy, and I can see a rationale in helping very old and frail people empty out accounts to some degree.

I agree with Tipswatch on the above latest comment (March 11, 2025 at 8:32 pm).

This morning’s CPI came in at 0.2 % / 2.8% and all the news outlets are cheering. Folks – that’s still not great. 2.0% annual run rate seems pretty distant. Most troubling (to me) is the continued march of food prices.

I was hoping to purchase a 3 year T-Note at auction tomorrow (03/11) but forecasted yield is down near 3.9 (at Fidelity). Guess I’ll stick with short term TBills for the time being. Just have two more rungs on my bridge ladder to cover.

Will be watching the TIPs auction as it nears, as well as considering another set of IBonds.

Any thoughts on the upcoming 5 year TIPS auction next month? Are you likely to be a buyer?

I probably won’t be a buyer because I have a good amount of TIPS maturing in 2030. It’s too early to say where that auction is heading because of the current volatility.

I’m going to buy at the end of this month (March), because there is a non zero possibility of funny business like changing the schedule of I Bond releases and at this point, there is no need to wait for one more month of data since we have enough data points on inflation.

I’d say. “That’s fine.” There is almost no way that the fixed rate will rise higher than 1.2% at the May 1 reset, so buying near the end of March is fine.

The one-sentence “termination” e-mail arrived in Erica Groshen’s inbox at 8:32 am last Tuesday.

Groshen, a former commissioner of the US Bureau of Labor Statistics, had spent more than four years as a member of a little-known but highly respected federal advisory board that helped the US government produce accurate and reliable economic data. That was until Tuesday, when the Federal Economic Statistics Advisory Committee (FESAC) was summarily dismissed, another casualty of President Trump’s assault on the federal government—and the concept of public policy expertise itself …

BLS, of course, is the federal agency which computes the serveral versions of the Consumer Price Index on which the inflation adjustments of TIPS, I Bonds, Social Security, etc., are based.

But until Green Acres’ post above, I had never heard of FESAC. This is one of several news reports about the termination of that body:

https://www.usnews.com/news/politics/articles/2025-03-04/trump-administration-disbands-two-expert-panels-on-economic-data

OK, this is troubling. The BLS is part of the Labor Department, which is about to be headed up by Lori Chavez-DeRemer, who appears to be a moderate on labor issues. But the two advisory groups were disbanded by Commerce Secretary Howard Lutnick. The members of the committee were unpaid, so this was not a budget issue.

The Wall Street Journal notes: “The move also follows a suggestion from Lutnick over the weekend that the government could change how it calculates the size of the economy by separating government spending, which would be a sharp departure from academic theory and international norms.”

More from free version: https://www.msn.com/en-us/money/markets/trump-admin-disbands-two-committees-advising-on-economic-stats/ar-AA1AfSQv

The Green Acres post, above, which began this series of comments, appears to have been lifted verbatim from the first two paragraphs of an article in The Nation magazine, about whether the Trump administration has broad intent to doctor statistical reporting about the economy and thereby gaslight the public. Concerning the FESAC, here are some paragraphs which followed:

“I was so disappointed,” Groshen told The Nation. “It’s so important to have these high-level advisory committees because statistical agencies have to be continuously improving, which means getting expert advice and information from outside of government. Eliminating an advisory committee like this suggests an intent to make the government less transparent. . . .

David Wilcox, a senior fellow at the Peterson Institute for International Economics who served until last week as FESAC’s chairman, said in an interview that disbanding the advisory committee—an all-volunteer [i.e., unpaid, so abolishing the FESAC is not a matter of budget-cutting] panel of experts from the private sector and academia—will deprive the public of an independent, nonpartisan brain trust whose goal was to help the government improve statistical accuracy in response to new technologies and ever-changing economic conditions.

The same article reports that, in a departure from current (and widespread international) practice, plans may be afoot to strip government spending out of the method for computing U.S. GDP. This would, among other things, make less visible the administration’s own sledgehammer budget cuts and mass firings of government employees.

It seems we are entering a period where information is manipulated to follow policy, instead of policy itself being based on first-rate information. It’s a reminder of how some of the same people also handled the reporting of COVID statistics.

The bond market in general – just from looking at Breakeven Rates / Real Yields and the shape of the nominal yield curve – seems to be signalling we are heading towards slow(er) economic growth over the next 3-5 years coupled with historically above-average inflation. So yeah – stagflation.

Seeing the lack of support and investment in the Treasury Direct platform, the message has been clear for years that the Treasury Dept has no desire to support a retail business. Trump may put a bullet in I-bonds, but government support for this product has been minimal.

“The Trump administration could decide to ditch the long-standing formula for setting the I Bond’s fixed rate. That is certainly possible. Remember, there is no set formula required by law. Keep that in mind.”

I’ll take this as a reminder but to believe this administration is being thoughtful about how it handles the I Bond fixed rate formula assumes they are deliberately thinking through anything. And The Odd Couple taught us what happens when you assume.

”Or, maybe it could eliminate the savings bond program entirely, cutting off all new issues? Highly improbable, I’d say.”

Given the indiscriminate wrecking ball approach over the past 7 weeks, destroying another institution of our system of government like the venerable savings bond actually would not surprise me.

marce607c0220f7, I agree with your comment about the “wrecking ball approach.” And agree that it has been “indiscriminate” in the way it has been done, i.e., just wipe out all the employees possible without any evaluation of skills, performance, or agency mission need. It has not, however, been “indiscriminate” in terms of the agencies targeted. They are all federal agencies whose mission is to improve the lives of ordinary people: consumer financial protection, consumer product protection, National Labor Relations Board, Equal Employment Opportunity Commission, antitrust programs, Medicaid, aid to needy people in developing countries, anything that aims to remedy past disadvantages of minorities, etc. The agenda may not even be explicity stated AS an agenda, but the pattern is clear.

Now, back to the main topic, I’ve been watching the numbers in this newest post by David (and, welcome back, David, I was missing my regular “fix” of your commentaries), and what to do about I Bonds has indeed gotten more complicated. I’m thinking of doing exactly as David suggests, waiting until mid-April, and then making moves.

In Fall 2024, we redeemed a bunch of older I Bonds with zero percent fixed rate component–all the ones we could redeem without the total interest earnings driving us into a higher federal tax bracket–and bought new ones at 1.30%, using the apparent “loophole” of being able to buy almost unlimited amounts of gift box purchases between husband ad wife, and then deliver all of them immediately despite our previous understanding about gift box amounts and annual purchase limits. I hope that option is still available this year, since, unless I missed the news, I haven’t seen anything saying otherwise.

Tipswatchchat, I recall in prior posts when I suggested you get rid of 0% I-Bonds, I got a stern rebuke. I am proud of you, you saw the light and took action. As a long term investment, a fixed rate is significant and a lot of people including myself and Mr. Enna got rid of the 0% I-bonds.

Someone had commented that the interest the government pays on

I- bonds is now lower than the majority of Government debt (T-bills, T-Notes etc). So it would not make sense to eliminate savings bond program. But……… wrecking ball approach as you said. You never know.

Chris, I don’t remember what I said at the time about holding on to zero-fixed I Bonds–and please don’t go looking for it to quote me back to me :-)–but if the tone came across as “a stern rebuke,” then you have my apology. My writing style is declarative (all those reports I had to write in my former job), but not meant to be unkind to anyone else.

What I was wrestling with mentally, and still do, is that all those old I Bonds may have a zero fixed rate but they also have a lot of “embedded” interest earnings over the years (including the high inflation rates that returned in the period after the worst of Covid), which are also compounding. So, if I paid $X for a zero-fixed I Bond a certain number of years ago; and if I am of sufficient age that the maturity date of that old I Bond is already beyond what I think (considering family history) is going to be my life expectancy; and, with accrued earnings, the redemption value of that old I Bond is now 150% of $X; then am I better to keep the old I Bond and all its embedded earnings, or redeem it for a new one that pays 1.30% fixed but “starts from scratch” in the earnings department and also starts its own new five-year clock for redemption without interest penalty?

This is exactly the kind of “on the one hand/on the other hand” situation that usually makes me feel like my head is going to explode. But I decided that (1) I don’t actually need the money right now; and (2) if I “recycled” all of the old I Bond redemption proceeds into new I Bonds, I would actually own a greater face value quantity of I Bonds at the new fixed rate than I earned previously at the old fixed rate, but without having to invade other savings to buy them.

That may or may not be your own reasoning, but in any case, it is good to learn that you are proud of me. 🙂

The Savings Bond program, which includes the highly unique inflation-linked I Bond, has always been targeted toward small-scale, middle-class investors. But a lot of rich people buy I Bonds over many years because of their unique cash qualities. Unfortunately, I expect there will be few voices of support in this administration. I can’t see it being killed, though. It’s a good deal for the government (paying rates usually lower than market) and also has the benefit of deferred payouts on the debt.

I could also see it go the other way as well- increasing the annual purchase limit. Potentially by a lot.

This is the dream scenario, yes.

I doubt any of the wrecking crew know what an I-Bond is, because (as our host notes) they are for middle-class folks who want a (close to) zero-risk place to tuck away savings. So I don’t see with all the chaos in the Administration that anyone would see a political reason to destroy I-Bonds. I would say the same for TIPS. However, there is huge incentive for the wrecking crew to fiddle with the monthly CPI calculations, as tariffs lead to inflation. The constraint on this would be Social Security annuitants, who would cry foul. Nevertheless, it is a risk. Perhaps our host could write about this risk?

Good grief and your innuendo. What has this once great blog become with the political nonsense.

Never remember all the political rhetoric the past four years.

Is it possible to just report objectively?

Please read what I (Tipswatch) have written and tell me where I am not being objective. To be objective means to observe. I have to report what I observe. I try not to speculate or delve into conspiracies. Commenters, however, can express their views, as long as the political rhetoric remains on topic and reasonable.