By David Enna, Tipswatch.com

Over the years, I have been known to rail against Federal Reserve commentary coming on the eve of auctions of Treasury Inflation-Protected Securities. So often, it seemed, a fairly attractive auction ended up with a mediocre real yield, thanks to the Fed.

This more or less happened yesterday, with Federal Reserve Chairman Jay Powell issuing a remarkably mixed message: 1) we can (possibly) expect two more rate cuts this year, 2) we can (probably) expect higher inflation this year and next, and 3) we can (probably) expect slower economic growth and higher unemployment this year and next.

Given all that, the Fed decided to hold short-term interest rates at current levels but also to slow down the pace of its balance-sheet reductions, which could help lower longer-term interest rates.

To me, that message seemed to forecast “stagflation,” a combination of higher inflation and slower economic growth. But the stock and bond markets were pleased. For one day, stock prices surged higher and bond yields fell.

And the result could be seen in today’s Treasury offering of $18 billion in a reopened CUSIP 91282CML2, creating a 9-year, 10-month TIPS. Most of the week, this TIPS looked likely to get a real yield somewhere in the range of 1.98% to 1.99%, but today’s result was a bit lower: a real yield of 1.935%.

That’s not really so bad. This TIPS was trading on the secondary market earlier Thursday with a real yield of 1.87%, gradually rising to 1.91%. The “when-issued” prediction, revealed just before the auction’s close, was 1.93%. The bid-to-cover ratio was 2.35, indicating lukewarm demand.

In this case, my preview article’s advice to buy this TIPS on the secondary market earlier in the week was correct. Real yields of around 2.0% were available before Powell spoke. (But trust me, it doesn’t always work out that way.)

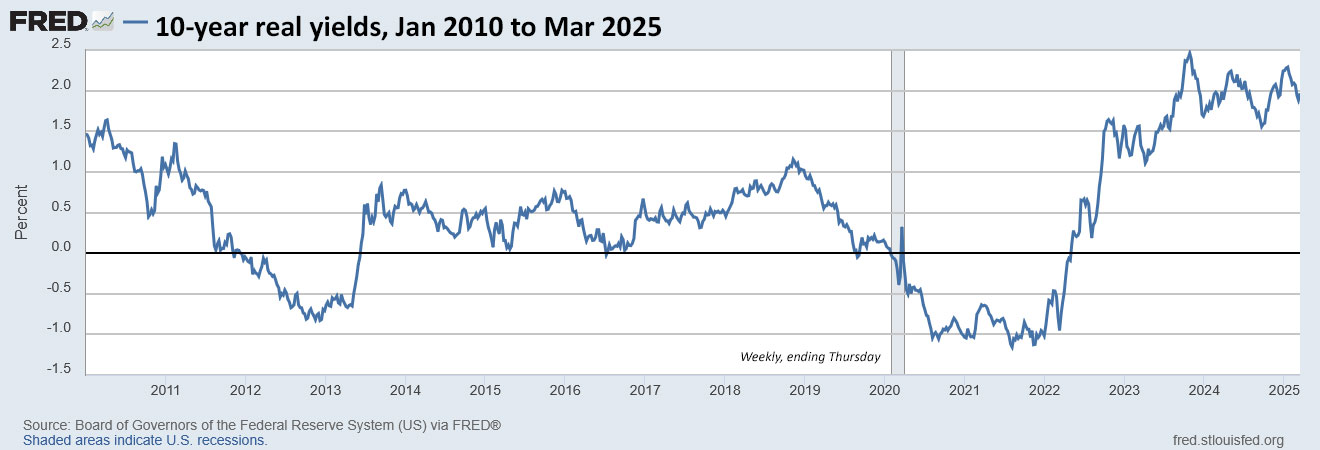

The truth: This auction result is not bad at all. A real yield of 1.935% is attractive by historical standards, even if it is a bit below recent trends. Here is the trend in the 10-year real yield over the last two years:

The longer-term trend shows more clearly the historic value of today’s higher real yields:

Pricing

CUSIP 91282CML2 carries a coupon rate of 2.125%, set by the originating auction on Jan. 23. Because today’s auctioned real yield came in below the coupon rate, investors had to pay a premium price of 101.685184. In addition, this TIPS will have an inflation index of 1.00639 on the settlement date of March 31.

With that information, we can calculate the investment cost of $10,000 par value at this auction.

- Par value: $10,000.

- Actual principal purchased: $10,000 x 1.00639 = $10,063.90.

- Cost of investment: $10,063.90 x 1.01685184 = $10,233.50

- + accrued interest of $44.30

To sum up, an investor purchasing $10,000 par value at auction paid $10,233.50 for $10,063.90 in principal. From then on, the investor will earn inflation accruals plus 2.125% interest on inflation-adjusted principal over the next 9 years, 10 months.

Inflation breakeven rate

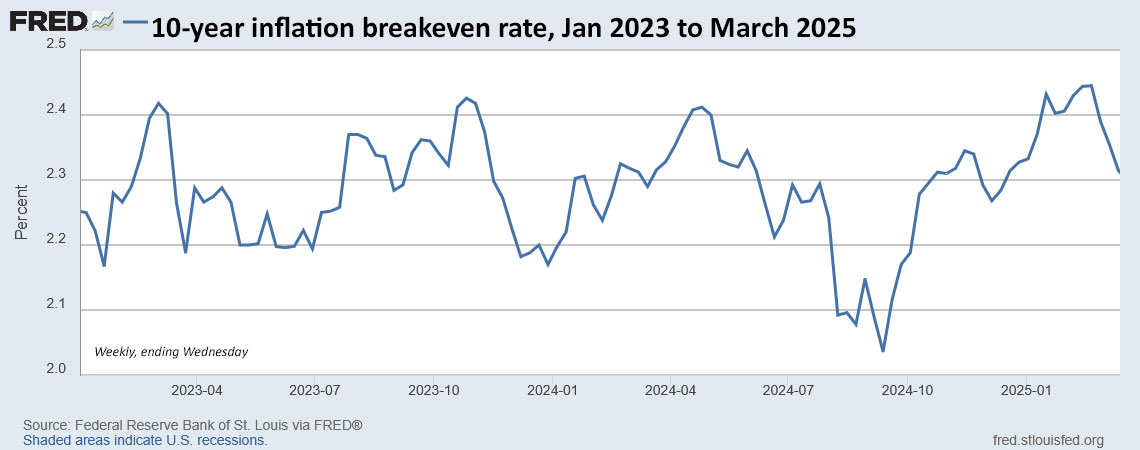

With a 10-year nominal Treasury note yielding 4.23% at the auction’s close, this TIPS gets an inflation breakeven rate of 2.30%, a bit lower than recent trends. This means it will out-perform the nominal Treasury if inflation averages more than 2.30% over the next 10 years.

Here is the trend in the 10-year inflation breakeven rate over the last two years, showing the sharp decline in inflation sentiment in recent weeks:

Thoughts

Let’s be realistic: A real yield of 1.935% is fine, even if it falls a bit short of the coveted 2.0% mark. It’s a good return on a very safe investment, especially if held to maturity.

While I watched Powell’s news conference yesterday, I was fascinated by his repeated use of the term “uncertainty” when describing current economic conditions. He said:

“I don’t know anyone who has a lot of confidence in their forecast. Forecasting is always really, really hard. And in the current situation, uncertainty is remarkably high.”

From today’s Wall Street Journal report:

Officials projected weaker growth, higher unemployment and higher inflation than they had anticipated in December. Moreover, nearly all officials judged that if their forecasts were to be proven wrong, it would be in the direction of even softer growth, more joblessness and firmer price growth.

A combination of stagnant growth and higher prices, sometimes called stagflation, could make it harder for the Fed to cut interest rates this year to pre-empt any slowdown.

So should we expect big moves in Treasury yields in coming months? Definitely not in short-term rates, where the Fed will hold policy stable. Longer-term rates are “going with the flow,” and I have no idea where that flow is heading.

So getting an above-inflation yield of 1.935% for nearly 10 years on a very safe investment looks like a sensible path, at least for a portion of your overall portfolio.

Here is the history of 9- to 10-year TIPS auctions over the last four years:

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I know I have had made this observation repeatedly, but before the inflation- indexed securities were instituted the debate (federal reserve bank of Saint Louis) was over how much the government would save because of the inherent risk premium implicit in nominal issues. So I am not that surprised at any manipulation by chairman Powell before an auction of ten year TIPS. Perhaps a slight difference in results for we investors, but how much would a few basis points save the government?

Powell had no reason to manipulate an $18 billion TIPS auction coming in the next day. But because of the way TIPS auctions are scheduled (usually on a mid-to-late-month Thursday), they often fall on the day after the Fed’s rate decision and news conference, always on a Wednesday. The bond market has less than 24 hours to react. It’s just a coincidence of timing.

Would you explain how a a bid to cover ratio of 2.35 indicates lukewarm demand? And where did you find that information? Thank you so much!

The Treasury auction result (which I link to in all auction stories) shows the bid-to-cover ratio in small print at the bottom of the page: https://www.treasurydirect.gov/instit/annceresult/press/preanre/2025/R_20250320_3.pdf … Bid to cover is an indication of demand, but every auction type and term can be different. It represents the number of bids received divided by the number of bids accepted. The Treasury adds this note: “The bid-to-cover ratio excludes any bids or awards for accounts of foreign and

international monetary authorities at Federal Reserve Banks and for the account of the Federal Reserve Banks”

I track this number for each auction (going back to 2020) and today’s number of 2.35 was pretty much in the mid-range of those results, not high, not low. A low number (like 2.18 for an 10-year reopening on July 21, 2022) indicates weak demand.

Auction result announcements can be found on TreasuryDirect: https://www.treasurydirect.gov/auctions/results/

Tnx,

Similar question along the same lines – do the competitive bidders have an option to submit some nonsense superhigh yielding bid? For example, if someone submits a bid asking for 5% real yield – would such bid be counted as part of “bid” in the “bid to cover ratio”?

Not sure how the competitive part works and what to make of this “bid-to-cover” number.

I don’t know the procedures for a competitive bid since that is out of my league. But in the past I have noticed at rare times some super-low bids on T-bills, I guess as a placeholder. Those bids do get filled at the high yield.

I agree: The yield is not what it might have been but is fine. I am a fundamentalist: I think the real yield on TIPS is a proxy for what investors expect real yields will be over the ten years, or, in other words, what real economic growth will be. Given the U.S. government’s high tariff and otherwise generally destabilizing policies, “stagflation” is a good consensus opinion. We might soon once again look back in fondness at any positive real yield on TIPS.

Well said I think, the future may be unknowable but we still must make a guess.