It had a real yield negative to inflation. And it was a winner.

By David Enna, Tipswatch.com

One of the basic rules of investing in Treasury Inflation-Protected Securities is: Get the highest possible real yield and ignore all the other noise.

But it doesn’t always work that way. Let’s time-shift back to the depressing early days of the COVID pandemic, when stock and bond markets were reeling. On April 23, 2020, the Treasury auctioned a new 5-year TIPS, CUSIP 912828ZJ2, with a real yield of -0.32%.

In other words, this new TIPS was guaranteed to under-perform inflation by 0.32% over the next five years. That was totally undesirable, right?

Wrong. At the time, a 5-year nominal Treasury was yielding just 0.37%, meaning this TIPS got an inflation breakeven rate of 0.69%. a wildly low number. Investors were betting that inflation would average just 0.69% from April 2020 to April 2025.

As often happens, investors were very wrong. In fact, inflation over the last five years has averaged 4.3%. And so investors in CUSIP 912828ZJ2 did much better than investors in a nominal Treasury at the time.

We know CUSIP 912828ZJ2’s final return because the February inflation report issued on March 12 set its inflation index at 1.23240 as of April 15, the maturity date.

The data page for this TIPS on EyeBonds.info shows it produced a nominal return of 3.904%, crushing the 5-year Treasury’s note return of 0.37% by an annual margin of 3.61%. That was a direct result of the soaring inflation we saw beginning just a year later, rising to 4.2% in April 2021 and topping off at 9.1% in June 2022.

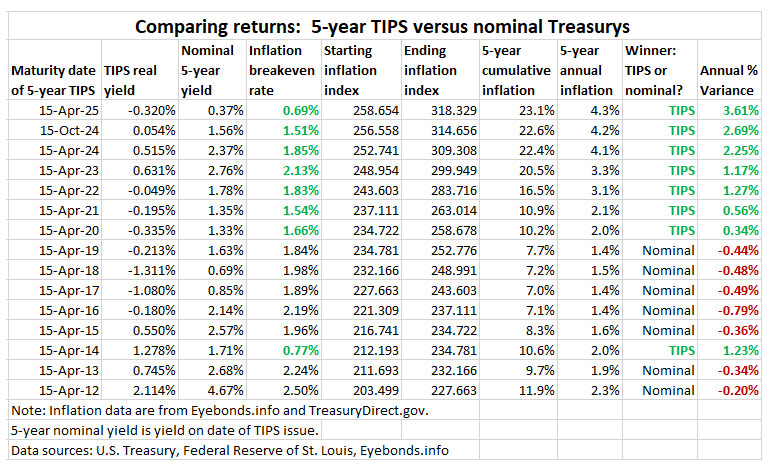

Here are data for all 5-year TIPS that have matured since April 2012. Note that the early trend of under-performance has dramatically shifted because of the ultra-high inflation of recent years.

To view this chart at a glance, the annual variance number in the last column shows how the inflation breakeven rate compared to actual 5-year annual inflation. When the numbers are green, a TIPS was the superior investment. When they are red, the nominal Treasury was the better investment.

Fair warning: The next decade could be entirely different, especially since inflation breakeven rates are now running much higher, around 2.4%.

Big winner: The I Bond

Here things get interesting. In April 2020, you could have invested in an Series I Savings Bond with a fixed rate of 0.20%, which seems crazy but again demonstrates the lagging effects of the Treasury’s fixed-rate decisions. That fixed rate was set in November 2019, when 5-year real yields were higher. It remained in effect until the end of April 2020.

Clearly, an I Bond with a fixed rate of 0.20% is going to outperform a TIPS with a real yield of -0.32%. Data on EyeBonds.info show a $10,000 purchase of this April 2020 I Bond is now worth $12,412, for an annual return of about 4.4%.

Notes and qualifications

My TIPS vs. Nominals chart is an estimate of performance.

Keep in mind that interest on a nominal Treasury and the TIPS coupon rate is paid out as current-year income and not reinvested. So in the case of a nominal Treasury, the interest earned could be reinvested elsewhere, which would potentially boost the gain. For certain, we don’t know what the investor could have earned precisely on an investment after re-investments.

In the case of a TIPS, the inflation adjustment compounds over time, and that will give TIPS a slight boost in return that isn’t reflected in the “average inflation” numbers presented in the chart.

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Thought I was brilliant to buy a 5 yr MYGA in 8-2021 at 3%.. after all 5 yr CD was paying under 1.5.. Still I would like to see a chart of the MYGA yields to Tips for comparison. Currently one can get a 3 yr MYGA at 6% or 7 yr at 6.2.. from direct buy option Canvas annuity.. Guaranteed by your state and interest is tax deferred.

That is an interesting chart comparing the return of 5-year TIPS that matured every year starting in 2012. https://tipswatch.com/

This is a small sample, and it is historical data, so the significance re: future results is highly questionable. I don’t know if the 2012 starting date was cherry-picked or not. However, the results make sense.

TIPS outperformed nominals in 8 out of 15 years and nominals outperformed TIPS in 7 out of 15 years. Pretty much a draw.

HOWEVER….

In all the years that nominals “won”, the outperformance was LESS THAN 1%/year, and in 6 out of the 7 years where nominals won, the outperformance was less than 0.5%/year. Pretty close to a draw.

In 6 of the 8 years that TIPS won, it outperformed nominals by MORE THAN 1%/year, and in 2 cases, more than 2%/year.

This could be mere coincidence.

However, it makes sense. TIPS especially protect against UNEXPECTED inflation. When inflation is close to expected, returns will probably be close. But circumstance can force inflation to greatly exceed the predicted status quo, in which case TIPS can outperform nominals by a large margin. (And even if TIPS “lose” to nominals, with positive yields they still offer the inflation protection that nominals do not).

It seems to me that there is less risk of open ended negative returns with TIPS. I guess that nominals would do better in a depression … maybe? Seems we have a very big bias against depression scenarios in the US.

Would be interested to know if you have done a similar chart for 10 year maturities.

Yes, these are posted on my TIPS vs Nominals page: https://tipswatch.com/tips-vs-nominal-treasurys/

I see that the April 2028 TIPS are ~ 1.25% and the Jan 2029 are ~ 1.35%. I currently have 25% of our TIPS in a ladder extending to 2032 (77 years old guy). I bought a lot of those April 2025 TIPS at 2.23%.

Maybe I should look for more safety during these next 4 years. Our stock portfolio has taken a beating. Usually I only have bought TIPS at near 2% but now I’m thinking safety is paramount.

David (and others) what do you think of these unexciting TIPS yields for purchase now?

Not so bad when the term is less than 5 years. A year ago, a new 5-year TIPS got a real yield of 2.242%, quite a bit higher. I have not idea where real yields are heading in this environment. The 5-year tends to track lower when the Fed begins reducing short-term interest rates, however.

Thanks David. I see that I can buy nominal Treasuries in an ETF like VGIT with a SEC yield of about 4.08% currently. But of course, I have no idea where inflation or rates are headed with this unusual economic policy uncertainty.

So maybe accepting some certainty in bonds is the best bet. As always the future is cloudy. As mentioned I have 25% of the portfolio in a TIPS ladder and another 9% in iBonds maturing in 2031. So pretty well set up for a 77 year old.

For near term money (5-10 years), and as a retired 60 year old spending almost solely from investments, inflation protection with some risk of nominal returns being greater seems like a welcomed trade off. If I were younger and investing bi-weekly or monthly into my 401k I’d just keep dollar cost averaging and be happy I’m now buying at a discount relative to a few months ago and rebalance on occasion.

I currently have a mix of US and high quality corporate nominals (ETFs) with target date maturities and TIPS for my short to intermediate term money. I also have some Vanguard VCIT/VCSH (short to intermediate term, high quality corporates). I have a nice batch of Government Agency bonds with 5%+ rates but I expect they will be called away…which is OK as they are short term anyway.

“… show a $10,000 purchase of this April 2020 TIPS is now worth $12,412, …”

You may choose to redevelop this because some readers will think you are saying the TIPS is now worth $12,412, which it is not. An I Bond purchased in April of 2020 will have that value in April of 2025 which seems to be $100 more than the the 5 year Tips maturing on April 15th, 2025.

Dumb error and it is now fixed. Thanks for the alert.

I picked up this TIPS in early March 2023 with a real yield of 1.957%. It was my first purchase of a TIPS on the secondary market, when I was just starting to get a feel for acquiring them other than at auction. My total gain over that two year period is well over 11%. By comparison, the two year nominal T-Notes issued February through April 2023 had an annual yield of 4.673%, 3.954% and 3.969% respectively. I’m happy enough with the results.

This chart of 5 year TIPS returns presents a near perfect, real example I would use to teach the cost and benefit of “insurance” or investment hedges – in this case a frequent smallish insurance premium (nominal outperforms TIPS) with an occasional relatively large payoff (TIPS outperform nominals). The fact that the April 2025 maturity started with a negative yield reflects a relatively high insurance premium that happened to pay off well. I could imagine that being the case over the next several years if we experience “stagflation” as some suspect.

I have always been curious about inflation as it was extraordinarily high when I was in high school and college, peaking at 13.5% in 1980 and plunging after 1981 with a 30 year mortgage at 16.6% (I wish I would have bought $100,000 of 30 year nominal Treasuries then). I took my first economics classes in 1982 – a great time to experience macroeconomics in action.

As I work with my modest income (Average AGI of $28,500), retired taxpayers we, of course talk finances. Renters have been hit the worst by far while homeowners express concerns about homeowners’ insurance and maintenance costs (still much less than a rent increase of 10-15%), few discuss new car prices but all discuss increased cost of repairs and maintenance, and, of course, medical insurance and costs.

I’m curious to see if stagflation sets in, what the components of inflation will be as labor costs and service prices typically flatten or decline while goods prices increase relative to overall inflation. If my introductory and graduate economics classes were accurate, both imported and locally-produced goods prices will increase as some domestic producers take advantage of relative pricing power. Seems like a good time to own TIPS even if the insurance premium is relatively high. I could imagine an ETF being created that tries to track goods vs. services prices….

Why would labor and service costs decline during stagflation?

Perhaps that happened in the 70s-early 80s but I don’t recall.

Automobile dealers make more money off repairs than by selling new cars. If new (and used) car prices shoot through the roof secondary to tariffs, more people will likely keep their old ones which will require more repairs and increase demand (and presumably price) for service. I assume that would also be the case for other goods as well.

Plus, if one combines that with the decline of cheap labor as more and more undocumented immigrants are deported, there will be increased wage demands for labor that will be passed on to the consumer.

Antje – Note that I said labor costs may decline relative to other prices – not necessarily decline. Your point regarding immigrant labor (legal and otherwise) is a good point, especially when it comes to food and construction prices. It’s relatively easy to track immigrant labor, but labor performed by those without work visas is obviously much harder to track. I know in Michigan farmers are very concerned about labor shortages along with tariff impacts on product demand.

Your example of car dealerships is a good example – during a recession I agree more people will try to extend the life of their cars (though they are at a record high now at over 12 years on average). Though, I note dealerships have lost market share to independent and chain garages in part due to price shopping with rapid inflations, and service makes up < 50% of dealers’ gross profits now. So, do consumers price shop more or defer maintenance to the minimally required?

In great part, however, labor and service isn’t subject to tariffs like goods and thus the main difference. And, managers making decisions on how to adapt to higher goods prices will try to reduce spending on labor on services if they do not have pricing power to pass along tariffs. Thus, near term market concerns of recession. We’ll see in 5-15 years, assuming tariffs stay in place, if there is a revival on high paying manufacturing jobs. I personally expect there will be even greater automation.