By David Enna, Tipswatch.com

Update, 2:15 pm April 9: Just about 12 hours after enforcing crippling tariffs on much of the world, President Trump changed course and announced a 90-day pause on reciprocal tariffs (above the new baseline 10%) on every country except China, which now will face tariffs of 125% on exports to the United States.

The stock market has reacted positively, with the S&P 500 index now up about 8% from where it was trading at 1:19 p.m. But the 10-year Treasury nominal yield remains elevated at about 4.42%. A reopening auction for a 10-year Treasury note was well received today, getting an attractive high yield of 4.435%, up from 4.310% last month.

So now we get a 90-day reprieve. It is hard to see what will change in three months if the White House continues to demand an even balance of trade with every nation.

——————————————–

Just a week ago, in the early stages of our brand-new “Tariff Crisis,” the stock market was falling sharply and the U.S. Treasury market was acting as a safe haven, with yields falling as buyers poured into the Treasury market.

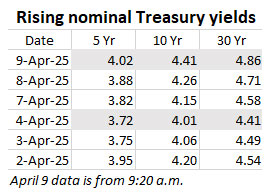

This crisis isn’t even a week old and yet the S&P 500 has already lost about 13% of its value since closing at 5671 on April 2. That was last Wednesday, and since then we have had only four full trading days. Over that time, short-term Treasury yields have been fairly stable, while longer-term nominal yields have been climbing.

As the chart shows, Treasury yields dropped initially, as expected, but then after the weekend began rising quickly, up 40 basis points on the benchmark 10-year note and 45 basis points on the 30-year bond. That’s a big jump, especially at a time when you’d expect yields to be at least holding stable.

Treasurys are traditionally considered to be among the safest of safe-haven assets. Investors rushing to sell Treasurys during a time of crisis is a sign of market distress.

So why and how is this happening? I’ve heard countless experts interviewed on this topic in the last two days and not one could give a definitive answer. But here are some theories:

China and other nations are dumping Treasury investments.

I think this is probably a factor and it would make sense for China to try to use its longer-term Treasury holdings to disrupt President Trump’s desire for lower interest rates. From an article on Investing.com:

Venture capitalist and Trump supporter Chamath Palihapitiya … said Tuesday afternoon that he is hearing from people that China has been dumping U.S. Treasuries in an effort to move yields up and shift the narrative.

“I’m hearing they are dumping UST to try and move rates to shift narrative and make our upcoming Treasury auctions more expensive,” Palihapitiya commented on X. “May make sense to delay auctions to next week. China can’t sell indefinitely.”

Investors are losing confidence in U.S. Treasurys

This also makes sense as our nation careens toward another debt-limit and budget crisis. From BusinessInsider.com:

Analysts at Deutsche Bank said in a note on Tuesday that the heavy sell-off “spoke to broader concerns about the safety of US assets and their capacity to act as a haven in times of market stress.” …

“A trend which will be watched closely is an apparent loss, whether temporary or otherwise, of US assets’ safe-haven status. Treasurys sold off heavily amid some speculation China and other parties are dumping their holdings as a retaliatory tool,” said Russ Mould of UK-based investment platform AJ Bell.

Hedge funds are unwinding losing bets.

From the Wall Street Journal:

Many analysts have been pointing the finger at leveraged hedge-fund trades. The strategy at the heart of concerns is known as the basis trade, and was a key driver of the 2020 “dash for cash.”

Hedge funds buy cash Treasurys and sell a Treasury futures contract to another investor, betting that the two prices will converge as the settlement date nears. The difference, or spread, is often very small, but hedge funds use leverage to increase the profits.

When the market makes large moves—as seen in the past few days—traders who had been betting on what they viewed as the sure thing of convergence can find their positions taking on water. They are often forced to sell.

This theory was embraced by Treasury Secretary Scott Bessent this morning in an interview with Maria Bartiromo of Fox Business:

Some highlights from that interview:

Bessent: Maria, I wanted to address in the meantime there is one of these — I’ve seen it very often in my career — there is one of these deleveraging convulsions that’s going on right now in the markets and I think it’s in the fixed-income market. There’s some very large leverage players who are experiencing losses they’re having to deleverage. I believe there is nothing systemic about this.

I think that it is uncomfortable but normal deleveraging that’s going on in the bond market and I expect that as we see the leverage come down … the market will come down.

Jump to 16:24

Bartiromo: You know, the fixed-income issue has been a debacle this morning that is why I assume rates are moving up. The yield on the 10-year, we were wondering if there was a deleveraging issue and whether or not China is dumping Treasuries. Is that what you see right now? Is China dumping Treasuries to try to put pressure on this market?

Bessent: You know, Maria, I think it works against their purposes if they’re dumping Treasuries because they have to buy something else. If they sell dollars and they strengthen their currency and as I said earlier they’ve actually been weakening their currency, which is a loser for everyone.

And again, when I hear all these stories, the dollar’s no longer the reserve currency, you know, if you end up with the Chinese who are willing to use their currency as a trade tool, that doesn’t seem like a very good reserve to me.

Thoughts

I have been saying for some time that the United States is heading into a period of unprecedented economic uncertainty. Some of the cause of that uncertainty has roots stretching back a decade or more. But this Tariff Crisis has brought everything to the surface, on fire. It is hard for me to imagine a solution in the near term.

The Treasury market seems to have been weakened, but most of the probable causes seem like they could be short-term effects as the stock and bond markets struggle through this chaotic period. Most likely, it will recover.

And then, could the Federal Reserve come to the rescue? I hope that doesn’t have to happen, but I have been predicting a major bailout of some sort as U.S. big-money investors grab at high-risk investments. In this case, most likely, the Fed would try to calm the market by buying longer-term Treasurys, not by cutting short-term interest rates.

If I wasn’t finished building a TIPS ladder at this point, I would probably be diving into the secondary market to take advantage of this disruption and attractively high real yields on longer-term TIPS: 2.17% on the 10-year, 2.46% on the 20-year, 2.61% on the 30-year. But yeah, that would take an investor with guts.

Do I have the answers or solutions? No. Let’s hear your ideas.

See you tomorrow with news of the March inflation report and finalized I Bond variable rate.

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I do not understand why there is so much concern about the 10 year Treasury rising about 33 basis points last week. After all the yield curve is only mildly sloped now with the 10 year – 3 month = 4.48 – 4.34 = 0.14% . Yes it was a fast rise as the bond market goes but still the net result seems to be a pretty flat yield curve.

Any good guesses on why there is so much fuss about the bond market?

During times of financial crisis, you’d expect to see high demand for Treasurys and lower yields. But the opposite has happened. A week ago, the 10-year nominal closed at 4.01% and five days later, in a time of high stock market volatility, it rose to 4.48%, an increase of 47 basis points in 5 days. Hopefully, this was just a momentary shock.

Is it possible this is a rational market reaction to perceived inflationary policy? The Fed is apparently not going to lower rates. The market is demanding a yield premium for holding longer dated Treasuries. Seems to make sense and that premium is quite small.

I could imagine the 10 year going even higher if past yield curve slopes are used. What am I missing?

I have listened to numerous explanations of how the impact of the tariffs is a one time price adjustment and is not inflationary because the change in price is not the result of a supply/demand imbalaance. My paranoid self tells me that we may well see a CPI adjustment to take out the “one time price adjustment” cause by the tariffs. If that happens, will there be any trust in the purpose of TIPS? We already live with hedonic adjustments and substituions. I have a 10 year ladder, but am watching the langauge closely.

I can’t send a link because it leads to a paywall but yesterday a financial pundit I follow (Jim Jubak) wrote this:

“Inflation-linked bonds, TIPS or Treasury Inflation-Protected Securities–are the biggest losers in this month’s Treasury market selloff. The cause of the drop in this market extends beyond damage done by rising inflation expectations. The problem also is a result of a drop in liquidity on the TIPS market. And as such it’s a sign of increasing stress in the financial markets in general.”

“Yields on TIPS have risen even more than those on regular Treasury bonds. (Which means the price of TIPS has fallen.) The 30-year TIPS yield, for example, has gone up 41 basis points to its highest level since 2008, while the regular 30-year yield is up about 32 basis points at the highest level since January.

A Bloomberg TIPS index lost 2.3% this month through April 10, while an index of comparable regular Treasuries lost about 1%.

It would be a mistake to conclude that inflation expectations are the sole driver behind the recent underperformance in TIPS, Michael Pond, head of global inflation market strategy at Barclays Capital, told Bloomberg.

The market for TIPS is smaller than that for other Treasuries, with about $2 trillion outstanding versus about $20 trillion of regular notes and bonds. As a result, even when there’s a reason for inflation expectations to drop, once they start falling, “liquidity starts to dry up and the TIPS market dislocates from fundamentals,” Pond said. “We’ve seen this movie before,” Pond said, pointing to the financial crisis in 2008, the March 2020 Treasury market liquidity crisis and–to a lesser degree–the regional banking crisis in early 2023.

The current problem in the TIPS market is exacerbated by what Barclays describes as a mismatch between supply and demand, as the U.S. Treasury has continued to increase the size of its TIPS auctions while holding the size of other auctions steady. At the same time, investor demand for long-maturity TIPS has been declining since 2022, when the funds that held them suffered losses as interest rates rose.

“We’ve been warning for a while about exactly this sort of breakdown in the TIPS market,” and advising investors to position for breakeven rates to fall more than warranted by fundamentals, Pond said. “The TIPS market has a tendency to break.”

I don’t think we’re at the point of a liquidity crisis in the TIPS market or in any other part of the financial markets. But the system is definitely showing signs of stress.”

I’m having trouble following his concerns (Jubak rarely mentions TIPS) but I would be interested on your take on his commentary and what would it look like for the TIPS market “to break”.

Thanks!

This is a Bloomberg article I am quoting in my auction preview story tomorrow. I think this is a free link to it: https://t.co/1AehF0eZ2R

Can you please help me to understand “Treasur(ie)s sold off heavily amid some speculation China and other parties are dumping their holdings as a retaliatory tool“.

Is it not possible to actually know whether China is dumping Treasuries?

Thanks

I heard an analyst on Bloomberg say he needed to see a data release to get a better idea. China was already trimming its Treasury holdings, but it still has enough to create a swing in long-term yields (if that is happening). This could accelerate if U.S. trade is cut off, meaning China would have fewer dollars to invest.

so if less demand for UST (because the Chinese don’t have more $s from selling more than they buy) then rates will rise. And that implies a trade deficit results in lower interest rates. Why doesnt POTUS Trump like that?

It is amazing how the ZIRP years of 2008/2009 and 2020 have absolutely warped the world’s expectations of interest rates.

We have become anchored to historically low rates and now freak out about any return to levels that would have been considered normal many times in history.

Short-term thinking and ignorance of history is just rampant in the financial world right now.

I don’t think Trump wants to negotiate down tariff rates. I think he wants the revenue. He has found a way to raise taxes without raising taxes directly.

I just heard Liesman say the current effective tariff rate after the pause is estimated to be 27%. That is because we import so much more from China. Nothing has really changed.

Most gains evaporated by close. I had put in a big order for tomorrow’s 30 year auction expecting to get something between 4.8 and 4.9%. I ended up cancelling. Volatility has burned me 3 times in the past year with auctions.

I have a simpler theory. Investors initially believed the tariffs were here to stay, so they bought a large amount of U.S. Treasuries. However, today’s pause in tariffs sparked hope that the policy might eventually be canceled. As a result, they rushed to sell Treasuries and moved their money back into the stock market. That’s why we saw sharp drop in Treasury prices and surge in stocks today.

It would take guts to make a 20- or 30-year investment commitment at a time of high volatility and an uncertain future. Of course, those are often the best times to make investments. Yes, holding to maturity would mean that the investor would get those real yields to maturity.

Today’s auction showed very strong demand for today’s 10 year treasury. Looks like the treasury market is not crumbling.

Trump pauses tariffs for 90 days on some countries. Dow immediately jumps 5 percent, NASDAQ 8 percent.

People need to relax, chill. The mainstream and most financial media have a bad case of Trump Derangement Syndrome, which causes anxiety among a lot of readers where anxiety should not exist. I guess the media gets more clicks that way. Don’t fall for it. Let’s see how the tariffs play out. Remember, Trump likes to deal. That’s what he does.

As of this writing, 10-year nominal is at 4.41% and real yield is at 2.15%. IMHO, administration saw writing on the wall when the bond market started going down. David’s sharing Scott Bessent’s video and other reports helped to come up with this opinion. Messing with the “safe haven” status of the Treasurues can be suicidal. I believe reality has finally been injected on how to evaluate the world of Tariffs. Hopefully we can move onwards and upwards with fiscal legislation and hit new all time highs in the equity markets. It is so much more fun to thoughtfully and constructively grow not just our economy but create a win-win for all. I am hoping the 20-year bond auction will fetch 5+%..I will be guessing and ready to buy if I see it happening….ok I will also settle between 4.9 and 5.0%…. 8))

Chander, the 20 year hit a high of 5.068% today, but has since dropped to 4.814% as of this post. You have to be more nimble (lol).

For people who do not understand Trump: Trump makes deals. If you go to a Marrakesh rug market, you see a rug you like with a posted cost of 100 dirhams. You only want to pay 70 dirhams. You tell the rug merchant you will give him 60, and he moans and groans and says 90. You say no way you will change from 60. He moans and groans and says 80. You say, absolutely not, no way will I pay more than 60. He moans and groans and says 70. You say, okay, it’s a deal. Sometimes you have to walk away for a while, like Trump did to Zelinsky.

We don’t work that way in the United States for most purchases, EXCEPT on big ticket items like a house, most real estate, or maybe a car, where some dealing is expected. The United States economy is the biggest ticket item. Expect more dealing. Don’t freak out.

I agree that one needs to be nimble to grab good deals. I will be buying 20-year Treasury Bonds for income (coupon) and not YTM. I am 69 and most likely our daughter or grand kids will use the principal. It is hard to find ~5% coupon in the secondary market, but I need to work harder on finding one. I take your point.

Having grown up in India for 22 years, I have the experience of its Bazaars. I can give you numerous unbelievable example of negotiated lowered prices from list prices. The “art of the deal” is over hyped. I am gald that intensity on this whole Tariff saga is coming down. How much it materially benefits or hurts our economy only time will tell, or we will never know the facts.

The President announced tariffs on penguins! TDS is believing that the Trump knows what he’s doing!

I understand that the intention with blanket tariffs covering those unhabituated islands is to prevent a crafty outfit from claiming they are manufacturing and shipping from them to avoid any tariffs.

🎯 Tipswatch. That’s why I come here, for the financial facts.

It’s a preposterous explanation by an administration that is not intellectually honest, has a record of deception, a problem with truth-telling, and has not earned the benefit of the doubt.

The entire rationale for the tariffs was based on a false premise. The tariff chart was fabricated nonsense. They refuse to do the hard work to get things right. That’s how you end up tariffing penguins. None of this is open to interpretation, unless you bring political bias into the analysis.

Let’s hope they do a lot better, for the sake of our collective financial well-being.

If that territory was listed on the tariff schedule separately from Australia why not include a reciprocal tariff whether there are imports exports there or not? It’s just a clerical precaution that doesn’t cost anything.

And there are reports despite the 0 population that there were exports coming from there from corporations specifically located there for some reason.

Dealing with Trump: “I have this rug for sale for $1,000.” Hmmm … I will think about it. “No, I meant $1,500.” Wait, I’ll do $1,000! “No, now it is $2,000.” OK, forget it. “$2,500 and I demand my money right now“

You are applying logic with the assumption that we are dealing with a rational human being. I can tell you want to believe that, but decades of irrational behavior, disregarding laws and rules, and behaving in an unhinged way say otherwise. And that is not a red or blue analysis. The only derangement we are seeing is coming from the White House.

The tariff policy was based on the false premise that foreign countries pay them. That belies the facts of how tariffs work. They are paid by American importers, passed along to American distributors, and paid for, in part or in whole, by American consumers which is a regressive form of taxation. The tariff chart used to establish the tariff amounts was comprised of junk numbers derived from a discredited formula that bore no resemblance to actual tariff rates, including two uninhabited islands near Australia where the penguins reside. This left most analysts laughing in derision at the sheer incompetence. On the heals of SignalGate, that was a really bad look.

There are many examples of how abnormal the behavior has been, whether it be Canada, Greenland, or Panama. But the most recent example made absolutely no sense. When Netanyahu came to the White House in person and committed to removing all tariffs, eliminate all trade gaps, and pointed out that Israel has not imposted retaliatory tariffs like many other countries had done, the president’s response to the question of whether he would remove the tariffs on our good friend, Israel, was “Maybe yes, maybe no.” The sheer arrogance of that statement is staggering. That is no way to engage in international relations and run the government of the greatest economic power and nation on earth.

We have witnessed little understanding by this administration of the value of allies and even less respectful discourse with them. They are our trading partners, not our trading enemies. None of this is normal, and no one should be okay with creating a fake crisis that buckles the global economy, creates chaos in global financial markets, and threatens our individual wealth and the world order, only to pause the fake crisis we never should’ve had in the first place. What happened today is a relief, but much of the damage has already been done.

This is not over by any stretch of the imagination. Foreign countries will be looking to new trading partners. There is no appreciation that the trade imbalance ends up coming back to us when foreign countries buy our debt and maintain the dollar as the global currency. A tariff pause just kicks the chaos down the road and isolates us further from the rest of the world. The 10% across the board tariffs remain firmly in place. The trade war with China is worsening by the day, with tariffs now up to 125%, where many of our goods are sourced, in some cases, solely. By all estimates, continuing on this path will cause GDP to diminish (the Fed estimate was already reduced), inflation to rise (the Fed estimate was already raised), unemployment to rise, consumer confidence to wobble (it is already down significantly), and the stock market to have a harder time to recover fully.

Where we go from here is uncertain, and uncertainty is not the friend of the investment community which we are a part of here, or global stability and the world order for that matter. Here’s hoping more rational voices can influence our policies moving forward, for the sake of all of our well-being.

marce607c0220f7, thank you so much for that cogent and well-written comment.

Very well stated, based on facts!!!

This administration is redefining trade in the USA for the benefit of our country.

This is a win.

Disconnect the politics from what is happening and realize how this will transform our country for years and decades.

Interpret what is and what is not nonsense at your discretion. Everyone is entitled to their opinion, but there isn’t anything in those paragraphs that isn’t factually accurate. Your reaction does the opposite of taking politics out of it.

On a substantive level, what you are omitting (or perhaps conflating) is the difference between intent and execution. The intent of lowering trade barriers in other countries to U.S. goods and services is a worthwhile goal. The execution of achieving that based on a foundational misunderstanding of who pays tariffs, a completely fabricated chart showing current tariff rates that have no basis in reality, and by using an anvil instead of a scalpel to destroy Americans’ wealth and upending global financial markets by crashing the stock market and almost collapsing the bond market has been a disaster resulting from incompetence, not a surprise if you’ve followed his approach to other matters of consequence.

Well said. Facts for those willing to accept them.

From a macro scale, we’re risking creating or deepening a recession. To improve the fortunes of manufacturing, a mere 10% share of GDP in a nation with the highest GDP in the world. Through imposing a tax increase that will, for the average taxpayer, not be offset by tax cuts and will add another trillion or two to our national deficit.

This has to be the dumbest thing ever. And they call setting our financial goodwill on fire “a win.”

I have a mix of bonds in my Traditional IRA to get me to 2035 when I plan to start Social Security. Today I did sell some nearer term target date bond funds that had appreciated nicely, and I unlikely need in the near term, to buy more CUSIP 91282CML2, a 1/15/2035 maturity TIPS at 99.773 with a coupon of 2.125%.

I was using Fidelity secondary market and a limit order and for the first time it was hard keeping up with the market and getting my limit order in due to volatility (it was dropping in price rapidly at the moment and within 20 minutes was well above that price). I calculate my real yield to maturity of my 2035 TIPS mix at 2.18%, which I will gladly take.

In Fall of last year I rebalanced my portfolio and sold off some stock index funds to reduce my mortgage, and bought some TIPS and bonds to stay around 50/50.

Not related to TIPS, but I followed a hunch for the first time since 2008 when I bet Ford would make it through the recession…..I also last Fall sold off some of the stock index funds that were over-weighted in the Magnificent 7 and bought my first individual stock – Berkshire Hathaway/B ….I’ll let you know in 10 years or so, but it looked rather prescient after this past couple of weeks (BRK/B up 15%, SP500 down 8% since the election). I gave up on individual stocks around 2005 figuring I’d never beat Warren Buffett. Now I’ll bet on who he has mentored the last 20 years.

Has the recent change in treasuries caused you to to rethink your I-bond outlook?

No. I still think the fixed rate will fall to 1.1%, if the Treasury sticks to its traditional, but unspecified, way of setting the rate.

I have only bought at auction and am tempted to dabble in the secondary market just to see how it goes, but I don’t understand it well enough. Would someone please explain any advantage of buying a TIPS with a low coupon, like 91282CDX6 with 0.125, vs 912810FH6 with 3.875? I understand you will pay less for the one with the lower coupon. Is there also less deflation risk?

Or do you ignore the coupon?

thx

Please see the link on this website….maybe that will help.

https://tipswatch.com/2023/02/05/tips-on-the-secondary-market-things-to-consider/

While I have never worried about deflation much, when buying in the secondary market, as noted in the link JackS posted below,

“Also notice the inflation accruals. CUSIP 912810FR4 has an inflation index of 1.57905, while CUSIP 912828H45 has an index of 1.25666. So with one you are buying $15,790 of adjusted principal and with the other, $12,566.50.”

when you buy TIPS at with large inflation accruals you do have greater risk associated with deflation. But, if the TIPS is a good measure of your personal deflation then you are also experiencing a reduced cost of living….that’s the trade off with any hedge.

If you look at CPI since about 1900 (https://www.usinflationcalculator.com/inflation/consumer-price-index-and-annual-percent-changes-from-1913-to-2008/) the only period of remarkable deflation was the beginning of the Great Depression (1930-1932) and you’d have been much happier owning TIPS then (if they existed) than nearly anything else except nominal treasuries especially if your local bank failed. But, your TIPS would still have only lost about 25% in value while the Dow Jones lost about 90%….and your TIPS recovered rather nicely during the high inflation during and post-WW2 (two years of 9%+ and 16% in in 1946) if you could hold to maturity.

This morning for over an hour the on the run 10 year TIP (2.125 coupon from jan) had a higher yield (2.26) than the older ones! In my personal opinion real yeild on 2.25% or higher on 10 year or shorter TIPS is too good to pass up

The spike I recall in TIPS was during 2008 and lasted about 2 months. The 5 year yield got as high as 4.24% according to the FRED chart.

… A lot of assets were doing poorly then and so it was said that TIPS were being sold to increase investor liquidity. Of course, holding TIPS to maturity would still work nicely. I could not take advantage of the spike as I did not have available cash and well it was scary then.

My bonds are doing fine with TIPS and iBonds and cash. Wish I could say the same about the equities. 😦

Here’s another theory:

In a social media post on Wednesday, the former U.S. Treasury secretary Lawrence H. Summers said the broader sell-off suggested a “generalized aversion to US assets in global financial markets” and warned about the possibility of a “serious financial crisis wholly induced by US government tariff policy.” See link below for source.

https://www.nytimes.com/2025/04/09/business/economy/bonds-tariffs-safe-haven.html

I did add to my 2033 TIPS holdings this morning with a real yield of 2.066%. Breathtaking contrast in real yields compared to a week ago. I will be interested in your comments about the upcoming 5 Year Auction.

Well, I am happy. Although I had previously bought only at the auctions, this morning I ventured into the secondary market and got what I believe is a terrific rate on the 10 yr tips (2.262%). Only wish I would have bought more but who knows where things go from here. The 5 yr spiked to as high as 1.75% which I never would have expected given it was at 1.38 just a few days ago. Perhaps the 5 year auction next week, which I originally was not going to participate in, will be once again attractive….but long time yet for that.

In these types of markets, you need to have guts as you say, and take a calculated risk. Which I have been doing not only in the Treasury market but also with stocks that have safe and decent yields.

I wish I hadn’t already completed my 30-year ladder, as this really would be a good time to buy. I’m considering buying some more 2055 TIPS to fund 2056 and several years thereafter.