March prices slipped into deflation, a bit of a surprise.

By David Enna, Tipswatch.com

April 30 update: I Bond gets a new fixed rate of 1.10%, composite rate of 3.98%

The just-released March inflation report gives us something we desperately need: Some clarity.

Now we know that the inflation-adjusted variable rate for the U.S. Series I Savings Bond will increase to 2.86% on May 1, up from the current 1.90%. This was finalized by the inflation report, which had non-seasonally-adjusted inflation rising 0.22% in March.

Non-seasonally-adjusted inflation increased 1.43% during the six months from October 2024 to March 2025, which translates to the new six-month annualized variable rate of 2.86%. This rate will apply to all I Bonds purchased from May to October, but will eventually roll into effect for all I Bonds no matter when they were purchased. The data:

The current variable rate, in effect for purchases through the end of April, is 1.90%. When combined with the current fixed rate of 1.2%, the I Bond’s composite rate is now 3.11% annualized. The new variable rate will increase to 2.86%, but it seems likely that the I Bond’s fixed rate will fall to 1.1% on May 1, creating a new composite rate of 3.98%.

If you buy in April, you lock in the 1.2% permanent fixed rate for up to 30 years. You will get six months of 3.11% and then six months of 4.08%. I think it makes sense to purchase in April, if you view this as a longer-term holding.

I will have more on this later this week.

The inflation report

Let the conspiracy theories begin! No, I am just kidding. However, the March inflation report, just released by the Bureau of Labor Statistics, was unusually mild.

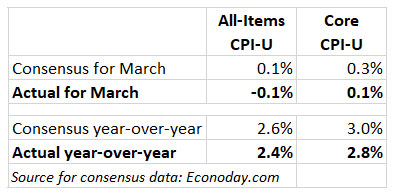

Seasonally-adjusted all-items inflation declined 0.1% for the month and the annual rate fell from 2.8% in February to 2.4% in March. Core inflation, which removes food and energy, rose 0.1% in March and 2.8% year over year, down from 3.1% in February. All of those numbers were below consensus estimates.

Annual inflation at 2.4% is the lowest rate since last September. And it’s unusual to see a deflationary month in March. The last time that happened was March 2020, when COVID fears were sweeping the nation. So what exactly happened?

One important factor, the BLS noted, was a 6.3% decline in the price of gasoline, which is now down 9.8% year over year. On the other hand, the cost of food at home increased 0.5% for the month and 2.4% year over year.

Shelter costs increased just 0.2% for the month and are up 4.0% for the year. That was the smallest 12-month increase since November 2021. Other items from the report:

- The cost of piped gas service increased 3.6% in March after rising 2.5% in February. Those costs are now up 9.4% year over year.

- Prices for used cars and trucks fell 0.7% for the month and are up only 0.6% year over year.

- Costs of new vehicles rose just 0.1% for the month and were flat year over year. (It will be interesting to see how this changes as tariffs roll into effect.)

- Apparel costs rose 0.4% for the month and were up only 0.3% year over year. (This is another item that could be hit by rising tariffs.)

- Motor vehicle insurance costs fell 0.8% for the month but are up 7.5% year over year.

- Airline fares fell 5.3% for the month and 5.2% for the year.

Apparently, the sharp decline in gasoline prices and the moderation in shelter costs were enough to push the all-items index into deflation in March. That trend for gas and shelter could continue into much of 2025, but could be balanced off by the unknown costs of unknown future tariffs.

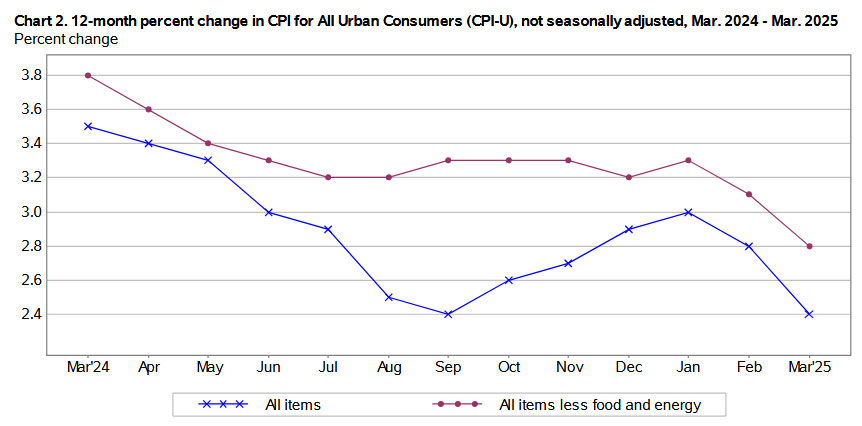

Here is the trend in all-items and core annual inflation over the last year:

This is exactly the type of chart President Trump and the Federal Reserve would like to see, with both core and all-items inflation falling for two consecutive months. However, the current chaos over tariffs and the brewing debt-limit crisis puts a lid on celebrations.

Do we know where inflation is heading for the rest of this year? Inflation? Deflation? It’s anyone’s guess.

What this means for TIPS

The BLS set the non-seasonally-adjusted CPI-U inflation index for March at 319.799, an increase of 0.22% from the February level. That means that principal balances for all TIPS will rise 0.22% in May, after rising 0.44% in April. Here are the new May inflation indexes for all TIPS.

What this means for future interest rates

Bloomberg is leading with the perfect headline this morning: “Trump Tariff Concerns Overshadow Upbeat US CPI Report.” This March inflation report was good news, but the positive vibes are overshadowed by tariff-related turmoil in the stock and bond markets. And, of course, tariffs seem likely to trigger higher inflation in coming months.

Bloomberg does a survey of 67 inflation forecasters and not one predicted a negative number for all-items inflation in March, and not one predicted a core increase of only 0.1%. From their economists Anna Wong and Stuart Paul:

March’s surprisingly soft CPI report showed little to no pass-through from President Trump’s initial tariff increases on Chinese imports. Apparel, furnishing, and recreation items – goods that have high import content from China – all saw either price declines or only soft price gains in March.

The real signal is that consumers are pulling back on discretionary spending. Services categories like airfares, car rentals, hotels, all saw deflation.

In all, we think the report provides space for the Fed to cut rates.

The financial markets have begun pricing in multiple rate cuts by the Federal Reserve this year, up from possibly one from earlier readings. That assumes the U.S. economy is slowing down. This March inflation report helps support the rate-cut theory, but the Fed still needs to pause and see the actual effect of tariffs on prices.

It also indicates an increasing chance of stagflation — a slowing economy combined with rising prices. From Edward Harrison, via Bloomberg:

That speaks to the Fed holding rates steady for the foreseeable future until the full economic effects of Trump’s policy changes become clearer.

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Please help me to understand… for my ibonds issued 1 April 2024, my composite rate for the next 6 months is 4.16%, correct?

My fixed rate is 1.3% and adding the 2.86% variable rate for the next 6 months, equals 4.16%.

Am I missing anything?

I will be posting an article Sunday on this topic. Actually, if you bought in April 2024 your fixed rate is 1.3% and the composite rate will be 4.18% for six months, based on the formula the Treasury uses to set the composite rate. But that rate will begin in October 2025 for six months. This chart helps explain that: https://eyebonds.info/ibonds/10000/ib_2024_04.html

Thank you for your update.

My husband and I purchased multiple I-Bonds using the Gift Boxes during the 9.62% variable rate with the zero fixed rate in 2022. Treasury Direct allowed us to deliver the all of the gift purchases in 2023. Will it be correct to assume since the best time to redeem some of the zero fixed rate I-Bonds will be in now (April) before the variable increases on 5/1/25 with the lower 3-months penalty to repurchase the higher fixed rate of 1.2% towards the end of April? I realized the best redemption time is on the second day of the month, but since the variable rate is going up and penalty is low now, it may be ok to redeem at least a couple bonds to be replaced towards the end of April. Thank you in advance for your reply.

One thing to realize: When you redeem in a certain month, that month earns no interest and it won’t count in the three-month penalty equation. If you redeem in April, the interest penalty would be applied to Jan, Feb, March. If you redeem in early May, the penalty applies to Feb, March, April. In either case, the penalty would apply to the current variable rate. I assume you are looking to raise money for another purchase in April? If so, redeeming this month makes sense, but you’ll have earned no interest in April.

Thank you for pointing it out that the last 3 months which is already figured in the interest amount that I am seeing when I login Treasury Direct, correct? I could purchase without redeeming first, so I could redeem in early May and lose the penalty to the 1.9% (Feb, March, April) and lock in the 1.2% fixed rate when I purchase near the end of April, did I get it right? Late night foggy brain when I submitted the question and still foggy when I read it. The timing of purchasing and redemption of I-Bond to maximize the interest earning still confuse me. Thank you for your patience.

Inflation will be skyrocketing due to tariffs (it continues to be bad since the covid stimulus). Plus the dollar is tanking for the same reaosn. So it is likely the variable rate will increase significantly as we saw in the 2020-21 period.

Quite honestly an extra .1% fixed rate is not enough incentive to take a 1% haircut over the next 6 months unless you are planning to hold this puppy for decades. The smarter play is to buy on May 1 – lock the 1.1% (assuming tipswatch is correct), and then enjoy the higher variable rates with zero risk for the next couple of years. I only wish I could buy more than $10k.

Thank you for the report, as always. When the variable rates are known, I think it would be valuable information for your readers if your April/October I Bond reports included the breakeven periods when comparing a higher short-term variable rate vs. a potentially higher/lower long-term fixed rate, like the one from your post on 4/13/2023 (props to hoyawildcat). Readers and yourself may have varying opinions on how long exactly is a “longer-term holding” such that purchasing in April is a better deal.

I hereby call upon hoyawildcat to try to duplicate this information. Later today, I will be posting an April vs. May analysis and my conclusion is that this will be sort of a toss-up.

Thanks for the update.

Too many moving parts. The dollar is crashing now. But oil prices are headed down (I think Trump made a deal with the oil producers in the middle east to up their production and he will take care of the Houthis. This helps hold down inflation and also hurts Putin which he seems to have had some kind of falling out). Tariffs (also known as Taxes — his Big Beautiful Taxes) will increase inflation but will dampen consumption. The stock market rout will also slow things down maybe to the point of a recession. Arghhh!

I am thinking it might be better to wait until October to buy if I can count on the 1.1 fixed rate. Get that 3.98 then and probably a higher variable rate in November. But knowing myself I will probably do 5 in April and 5 in October or December.

Totally agree about too many moving parts. I think if this inflation number had been released a week later it would have looked worse. And will look a lot worse in May. I suspect the November 2025 variable rate on the I Bond will be pretty impressive. But if we are in a full blown depression by that point… who knows.

One positive thing about the November rate reset, no matter when you buy, it that the November rate will be available in January when the purchase cap resets. Of course, the future may be no clearer by then.

Please tell me if I understand this right. The variable rate looks higher in may but you are suggesting buying in April because the fixed rate might be better? Thank you

That’s correct, but I agree a 0.1% difference in the fixed rate doesn’t make much of a difference. When you buy in April you lock in the 1.2% fixed rate (permanently) and get a composite rate of 3.11% for six months, and then that new 2.86% variable rate will go into effect in October, for six months. So you get 3.11% for six months and then 4.08% for six months.

If you buy in May, and the fixed rate does fall to 1.1%, you will get 3.98% for six months, and then an as-yet undetermined composite rate starting in November.

Could uncertainty be reducing consumer demand?

I’d say yes, except that fear of higher prices from tariffs could cause consumers to speed up purchases before prices increase.

Pingback: New I-Bonds Estimated Rate: 3.98% APY (Variable 2.88% + Fixed 1.1%) – Thefinancecentral

As usual thanks for the timely report.

I have a technical question/comment.

“Non-seasonally-adjusted inflation increased 1.43% during the six ..”

Since inflation is the rate of change of prices, shouldn’t it be written as:

“Non-seasonally-adjusted inflation was1.43% during the six months … ”

or

“Non-seasonally-adjusted inflation index increased by 1.43% during the six months … ”

With compounding over time, I-bonds may be your best reliable friend when you get old.

A huge factor in retirement is that the principal balance can never decline and all interest can be deferred until redemption. So with regular purchases you can build a fantastic back-up reserve fund, adjusting to inflation, and available for withdrawals when you need the money.

Pingback: New I-Bonds Estimated Rate: 3.98% APY (Variable 2.88% + Fixed 1.1%) - Doctor Of Credit

March CPI actual, i.e., not seasonally adjusted is .22. Seasonally adjusted it is -.1. Seasonal adjustments are a mathematical attempt to eliminate monthly effects using a statistical model based on historical data. The model no doubt works better for some economic measures than others. It would be useful if BLS provided a statistical measure of confidence of each seasonal adjustment of each economic measure.

One has to remember that the big assumption is that the variables driving the current seasonal adjustment work the same way as past seasonal adjustments. This may or may not be true. For CPI change I prefer to look at the non-seasonally adjusted number.

My expectation was for seasonal monthly inflation of about 0.0%, and non-seasonal of about 0.2%, so the spread looks right for the month of March.

My implied point is the main stream media will glom onto the -.1 seasonally adjusted change in CPI and say we no longer have to worry about inflation, when in fact CPI increased .22. My comment was more concerned about seasonal adjustments being used by government bureaucrats to spread disinformation.

Here is what the BLS news release for today says “In March, the Consumer Price Index for All Urban Consumers fell 0.1 percent, seasonally adjusted, and rose 2.4 percent over the last 12 months, not seasonally adjusted.” BLS does not mention in its release that real monthly inflation actually INCREASED .22 percent. Well, the Fed and I-bonds know all about this, which is all that really matters to me personally, but it is never a good idea for government bureaucrats to mislead the public with half-truths.

A very nice report.

Very nice report. The only problem is how much is just distortion because of the on again/off again tariffs (although we seem to have kept the 10% tariff) and the market reaction (the price of crude appears down and the price of US Treasuries is falling with rising interest rates). And you need , soothsayer, Ouija board, magic 8 ball and several fortune cookies to know what will happen next. What makes things even worse is we still don’t have a rational explanation of either goals or methods which are either consistent or which makes any sense. That means other than the chaos we currently see there is no way to judge the economic results of the Trump tariffs or economy. Next up is the debt limit. Will the Congress (and the president who seems to have great power over the republican 51%) do what is necessary or try some political stunt such as defaulting, renegotiating the debt or punishing China or our Canadian or European allies? The law, economic realities and/or common sense do not appear to be impediments to the quasi-religious beliefs of the MAGA crowd and/or their leader who does not have policies or theory but just makes deals or abrogates the ones he made in his last administration and we are not even 6 months into this presidency. I think the results speak for themselves.