A predictable result in unpredictable times.

By David Enna, Tipswatch.com

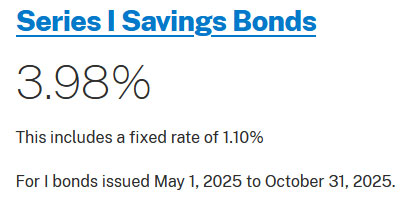

The U.S. Treasury held to past practices today, setting the new fixed rate for the U.S. Series I Savings Bond at 1.10%, as expected, and the new composite rate at 3.98%, also expected.

This was welcome news, indicating the new administration will maintain consistent support for the savings bond program.

No news release has yet been posted; that should come tomorrow. Bizarrely, just a few minutes after the new rate was posted at 8:30 a.m. on TreasuryDirect, it was taken down and the site was again showing the 3.11% composite rate in effect through April 30.

At 10:10 a.m., the site went live again with the new rate, 3.98%.

In recent years, TreasuryDirect has posted the new rate a day early. Even though the rate change officially takes effect May 1, any purchases today at TreasuryDirect will get the new rates. I confirmed this with a test order this morning:

For the time being, I am going to ignore this flip-flop and assume the fixed rate was set at 1.10%, variable rate at 2.86% and composite rate at 3.98%. And that is what an investor will get with a purchase today through late October.

Update: Here is TreasuryDirect’s news release on the new rates.

What is an I Bond?

The U.S. Series I Savings Bond is a U.S. Treasury security that protects the investor against increases in inflation:

- The fixed rate will never change. Purchases through Oct. 31, 2025, will have a fixed rate of 1.10%, down from the previous rate of 1.20% in effect through April.

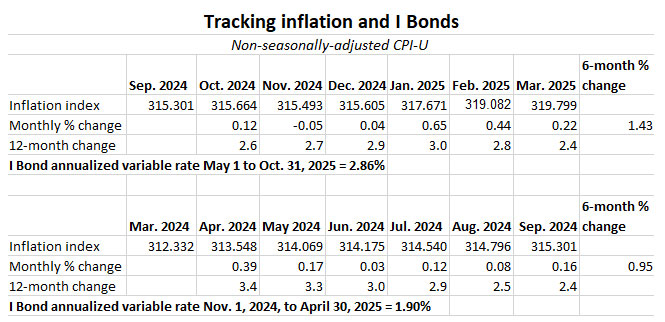

- The inflation-adjusted rate (often called the variable rate) changes each six months to reflect the running rate of inflation. That rate is now set at 2.86%, based on inflation of 1.43% from October 2024 to March 2025. This new rate applies to all I Bonds, no matter when they were issued. (However, the effective start date of the new interest rate will vary depending on the month you bought the I Bond.)

- The I Bond’s current composite rate is now 3.98%, annualized, for a full six months for any bond purchased from May to October 2025. That is an increase from 3.11% for I Bonds purchased in April.

The fixed rate. The Treasury has not revealed a method for setting the I Bond’s fixed rate. But over the last decade, it appears to have leaned heavily on this formula for setting the I Bond’s new fixed rate: Apply a ratio of 0.65 to the average 5-year TIPS real yield over the preceding six months. It seems to have held to that formula for this reset:

This was one area that concerned me in the new administration, because changes in policy are always possible. But today’s decision is reassuring that we can expect Treasury to follow predictable policies of the past.

The variable rate. This component of the I Bond’s composite rate wasn’t in doubt. It is based on six months of inflation, in this case 1.43% from October 2024 to March 2025. Double that rate and you get the annualized variable rate, 2.86%.

Again, it is worth noting that this new variable rate will go into effect for all I Bonds, no matter when they were issued. So if you are holding 0.0% fixed rate I Bonds, you will get 2.86% interest for six months. The starting month of the new rate depends on when you initially purchased the I Bond.

The composite rate. The I Bond’s composite rate isn’t calculated by simply adding the variable and fixed rates. The Treasury uses a formula that adjusts for compounding factors of the fixed rate:

[Fixed rate + (2 x semiannual inflation rate) + (fixed rate x semiannual inflation rate)]

So with a fixed rate of 1.10% and inflation rate of 1.43%, the new composite rate calculation looks like this:

0.011 + (0.0286) + (0.0001573) = 0.0397573

Rounding gives you 0.03976. Turning the decimal number to a percentage gives a composite rate of 3.98%. This rate is in effect for six months for I Bonds purchased from May to October 2025. I Bonds purchased in the November 2024 to April 2025 period will eventually get a composite rate of 4.08% for six months.

What this all means

Let’s assume the posting, then pull-down, then re-posting of the new composite rate was an accident and not the result of some Treasury official running down a hall screaming, “We can’t do that!” The fixed rate is the key to an attractive I Bond, and a rate of 1.10% above inflation remains appealing.

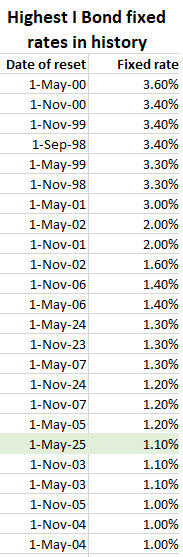

The chart shows all the times in history, dating back to September 1998, that the I Bond’s fixed rate was 1.0% or higher. While May 2025 is low on this list, note that only four of these high-level resets happened in the last 17 years.

I Bonds are a unique investment, one of the safest in the world, because they are backed by the U.S. government and provide protection against official U.S. inflation, no matter how high it rises. I Bonds earn tax-deferred interest, are free of state income taxes, can never lose a cent of value and have a flexible maturity date.

Purchases are limited to $10,000 per person per year, unless you add to holdings through gift-box, trusts, or business-owner strategies. So it makes sense to buy nearly every year, but especially when the fixed rate is appealing, as it is today. I consider I Bonds a cash-equivalent investment. Hold them for one year and cash out with a three-month interest penalty, or redeem in five years with no penalty. All the while, there is zero chance your investment will lose value.

Now that we are in the May to October purchase period, you should feel no rush to invest. If you want the I Bond issued in May, wait until late in the month, like May 28, to make the purchase. You earn a full month of interest no matter when you invest.

Another option is to hold tight until mid-October, to see where inflation has been heading and also get a reading on the next fixed rate, to be reset November 1.

I made my I Bond purchases earlier this year, so I am done. Let me know what you are thinking in the comments area below.

Update on EE Bonds

The Treasury set the new fixed rate for EE Bonds at 2.70%, up from the current 2.60%. It also maintained the doubling period of 20 years, meaning that an EE Bond will earn an effective rate of 3.53% if held for 20 years. This compares with a the 20-year Treasury bond, currently yielding 4.66%.

It is hard to make a case for EE Bonds as a short-term investment (especially because of the three-month interest penalty for redemptions before five years) or long-term holding (because you can do much better with a Treasury bond.)

If short-term interest rates fall dramatically before November (unlikely) the EE Bond could begin to look attractive. Otherwise, this savings bond is a non-factor.

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Pingback: Higher I Bond Rates Amid Stubborn Inflation – Global Finance

I have a good looming tax problem in that the $116,000 in I-Bonds we purchased from December 1998 to October 2001 are now worth $515,976.80. As much as I hate to redeem any of my 3.0% to 3.6% fixed rate I-Bonds early, I’ve come to the conclusion that our after-tax funds will be higher if I start redeeming some of them each of the next three years, before their 30-year maturity dates, shifting more of the interest from the 22% (25%?) tax bracket to the 12% (15%?) tax bracket. I had been making Roth Conversions each year to get to the top of the 12% bracket, but I probably should have shifted to the early I-Bond redemption strategy a couple years sooner.

“An EE Bond will earn an effective rate of 3.53% if held for 20 years.” This is compounded interest. To double an investment in 20 years without reinvesting interest payments, a bond would need to offer a fixed interest rate of about 5%. Does this mean the EE Bond is better than any 20-year bond with interest rate smaller than 5% ?

No, I wouldn’t say that. You can’t simply “take away” the reinvestment of interest, which could be at a lower rate, but also could be at a higher rate. It is true, though, that getting tax-deferred compounded interest on the EE Bond is an advantage.

David, you were nicely called out by Beth Pinsker at MarketWatch today. I believe she really liked “A predictable result in unpredictable times.” Here’s a link: Sitting on cash? Lock in this new Series I bond rate to protect your savings from inflation. – MarketWatch

I have worked with Beth on many stories in the past. She’s a good one.

Beth Pinsker writes: “When inflation is high, the fixed rate typically goes to zero, and when it is low, it goes higher.”

Isn’t this an oversimplification? I thought real interest rates (and by extension the I Bond’s fixed rate) typically rise during inflationary periods and drop during periods of low inflation and/or low growth.

Or was the main driver of rising real yields from 2022-2024 the increase in nominal yields in response to the Fed’s tightening cycle?

I would say that sentence isn’t accurate. If inflation is high, the Fed should be raising interest rates and therefore you’d see the I Bond’s fixed rate rise. However, in the Covid aftermath, there was a cause-and-effect situation, with interest rates moving very close to zero, while government money flooded to individuals. That created a time of 0.0% fixed rates + four-decade-high inflation. In the aftermath of high inflation, the Fed started raising interest rates, as you note, and the fixed rate rose to 16-year highs.

I bought $5K, planning to make a decision later on whether to buy more in the current window or wait till October. However, I’m not totally confident that the current administration won’t start meddling in these bond programs.

To clarify, I bought $5K at the 1.2% fixed rate.

I have written to my Representative to ask that they advocate for US Savings Bonds being tax-free at the Federal level.

There are tax cuts being proposed, this would be better policy than other proposals that I’m seeing…

Thanks for what you do.

Let me remind everyone here: before the past few years, when I bonds became popular, I didn’t even really know about tips or I bonds. I knew vaguely about tips but not much.

Not once in 26 years of education and 15 years of scouring the internet did I ever hear them mentioned. Not a single economics teacher, not a single financial journalist, not a single financial advisor, not a single youtuber, not any of the major blogs, not even a single poster at bogleheads forums.

Very underappreciated investments.

dolph, can’t imagine what you mean when you say that “not even a single poster at Bogleheads” was talking about I Bonds.

Mel Lindauer, one of the founders of the Bogleheads forum, and a moderator of its predecessor, the Vanguard Diehards forum at Morningstar, was already talking enthusiastically about I Bonds a couple decades ago, maybe even earlier, when new I Bonds could still be bought with a fixed rate (i.e., before the CPI-based inflation addition) of 3% or more. That’s how my wife and I originally learned about the existence of I Bonds. Since then, there have also been many Bogleheads threads about I Bonds over the years.

Back then the purchase limit was also $30,000 per person per year instead of the current 10,000, I Bonds were still available on paper, and, for those with rewards points programs, it was possible to make an I Bond purchase at TreasuryDirect using a credit card. Alas, those days are long gone. And so are our own 3%-fixed I Bonds, which we later redeemed.

Otherwise, yes, agree with you that they are “underappreciated investments.”

This Bogleheads monster thread has now been active for more than four years:

https://www.bogleheads.org/forum/viewtopic.php?f=10&t=346091

Back in 2021, when the I Bond variable rate was about to increase from 7.12% to 9.62%, I remember Becky Quick of CNBC saying on air,” What is an I Bond?” As TipswatchChat notes, Bogleheads and followers of radio host Bob Brinker were well aware of I Bonds all the way back to the late 1990s, but most financial advisers and nearly all media “experts,” were not.

To be fair, I think part of the reason some people may not have been aware or interested in I Bonds is that they haven’t always seemed like such a great investment. I learned about and bought my first I Bond in 2011, but I ended up not being especially pleased with it. It had a 0% fixed rate, and there were several 6-month periods during its first 5 years when it barely earned any interest (maybe even one in which it earned no interest at all).

I probably should have redeemed it during one of those extremely low-interest periods, when the 3-month penalty would have been minimal, but I’m not sure I realized that at the time. I held onto it for a little more than seven years, hoping it would improve, and it did improve some, but not as much as I would have preferred. Finally I needed that money to buy a car, so I redeemed it and forgot about I Bonds for a few years.

In recent years I Bonds have become more attractive again so I have gotten back into them, but I don’t assume they will stay that way. The higher fixed rates should help, though. Even my remaining 0% fixed rate doesn’t seem too terrible, relatively. It is currently earning 1.9%, and although that is the lowest it has been so far, it is still higher than the average that I got on my first I Bond during 2011-2019.

I started writing about I Bonds back in March 2011, which happened to coincide with a decade of Federal Reserve intervention and very low interest rates for most of those years. If was a sad time for TIPS and I Bonds. If you bought an I Bond in March 2011 with a fixed rate of 0.0%, you have earned an average return of about 2.64% over those 14 years. Not great when compared with a nominal yield of about 3.41% on a 10-year Treasury note available in March 2011.

Good advice. I usually buy my full allocation all at once to limit number of holdings and account “clutter”. When I was on the fence about buying in April, my better half convinced me to buy half the limit instead of being an all-or-nothing investor.

I like purchasing I Bonds in 5,000 or 10,000 increments because the bond values will always be whole numbers until you redeem them. But ultimately the best buying strategy depends on one’s individual needs.

Sorry, I meant to reply to Chris B’s comment below.

Buying is never an all or nothing proposal. The appeal of the higher 1.20% fixed rate led me to buy 9,000 in April and will do the the 1,000 in May.

“So it makes sense to buy nearly every year, but especially when the fixed rate is appealing, as it is today.”

I’m thinking it makes sense to buy if you’ve maxed out your pretax and Roth retirement contributions and still have money left for investing. So I didn’t buy.

Anyone disagree?

Opinion: I would prioritize the Roth and at least enough 401k contributions to get a company match. An investor’s first goal should be to build capital. I Bonds are a way of preserving capital.

“Current Rate: 3.98%

This includes a fixed rate of 1.10%

For I bonds issued May 1, 2025 to October 31, 2025″

– Treasury Direct

This is definitely online now (as of time of this posting). It may be illegal for TD to post the new rate one day ahead of time. It’s probably illegal for TD to give the new rate to purchases ahead of 11:59:59 pm EST on April 30. I-bonds are governed by an act of Congress. No bureaucrat should be allowed to fool around with an act of Congress. But they obviously do.

David’s table showing the top fixed rates is interesting (sorry, bad pun). Clearly the nature of the calculation has changed dramatically over time. When the government does away with the savings bonds program, I would like to read an insider’s article which reveals the secrecy of the fixed rate decisions and why the formula, if there was one, changed so much over time. In the mean time, congratulations to David for finding an accurate formula for predicting the fixed rate (accurate for now).

TreasuryDirect has posted the new rate one day early for several years, since purchases on that date (in this case, April 30) will get that new rate. So it is accepted policy. On past real yields … these TIPS and I Bond investments were very new in the late 1990s and early 2000s, and investors didn’t know how to price TIPS, or in the Treasury’s case, I Bonds. I got an EE Bond in 1993 that doubled in 12 years (6%) and then continued to pay 4% through maturity. We don’t see fantastic yields like that today. So I wouldn’t get hung up on comparing that early era to today’s era, where TIPS are an established investment.

Whatever the formula for I Bonds was in the past is ancient history. Treasury was guessing and trying to encourage demand in this new product.

“Accepted policy”; accepted by whom? Certainly accepted by the bureaucrats that made the policy. This kind of action is currently a big issue, this overreach by bureaucrats creating policy. Bureaucrats are hired employees, not elected government officials. As I mentioned, I-bonds were created by an act of Congress and must function according to that act. I stand by my comment “It’s probably illegal for TD to give the new rate to purchases ahead of 11:59:59 pm EST on April 30.”

I wouldn’t consider 2000 to be ancient history. 2000 BC was ancient history. I would welcome an impartial investigation into TD and its operations, given this and other problems we have seen. It would probably cause a stir in the bond markets, but maybe they should be stirred.

Patrick, you are going way overboard. It is correct for TreasuryDirect to tell you what interest rate you are getting if you purchase on April 30, because you are getting the May 1 rate on that day. There is no law governing this, and it is the right thing to do.

“Rate Change Deadline: To receive the current 3.11% rate for I Bonds in TreasuryDirect, you must complete your purchase by 11:59 p.m. Eastern Time on Wednesday, April 30.”

This was in a yellow box on the TD website. Not overboard. Just the facts. I seem to recall reading on this website that some people were getting the new rate, 3.98%, on purchases before 11:59 p.m. Eastern Time on Wednesday, April 30. Please correct me if I am wrong. Thanks.

Patrick, In reply to your post on May 1, 2025 at 1:13 am

You said to correct you if you’re wrong.

What you fail to understand is that if you asked for an I-Bond on April 30th and submitted the purchase. The bond purchase would BE completed on the next day, May 1st, which would give you the new rate. Unless you schedule bond purchase ahead of time, it always takes a day to COMPLETE the purchase. (Or the next business day) Anyone that logged in to TD on April 30th and bought an I-Bond thinking they were getting the old rate would be, and have been, shocked when they received the new rate when bond was issued the next day. No one is letting the “cat out of the bag”, they are just warning you about the rate you will receive if you follow through on a purchase after reading the yellow box warning.

TreasuryDirect could do a better job of communicating (as usual), so let’s give Patrick that point. The key word in the yellow message was “complete.” On the morning of April 30, there was no way to “complete” an I Bond purchase in April. It would be registered on May 1. So TD was right to show the new rate. TD could simply add a line, “New orders placed on April 30 will be completed on May 1 and get the May rate.” — This is actually shown on the order page, by the way, as I documented in the article.

what about your CofC account if it was funded?

Thanks for all you do, David. We ended up hedging our bets (because of all the current admin uncertainty) and buying the full 10k limit for my wife and her full 10k gift to me. I’ll do the same either at the end of October or after depending on the projected November rate reset. (And we still have one business account and two trust accounts to max).

Reassuring that the program seems likely to continue as is.

The math formula is missing a zero: 0.011 + (0.0286) + (0.0001573) = 0.0397573

You are right. Thanks for catching that.

I purchased $10K each for myself and spouse on Monday at 1.2% fixed. Thanks,

David, for the great information on this site (I Bonds and TIPS).

Did the EE go up a little? Still not a great deal aside from the tax deferral aspect.

Yes, it went up from 2.6% to 2.7%. I added a section on EE Bonds to the article earlier today.

I changed my mind at (literally) the 11th hour and decided to buy only $5k. Earlier this year, I wasn’t planning to buy any 1.2% fixed rate I Bonds after doing three sets of gift box purchases at 1.3%. But the possibility of a falling fixed rate suddenly made me indecisive. I waffled between no purchase, the full $10k or something in between. Admittedly, the less attractive composite rate for the first six months was a bit of a deterrent.

I placed my I Bond order at 11:58 p.m. and it was issued this morning at the 3.11% composite rate. I wouldn’t recommend others cut it this close, but my experience confirms that TreasuryDirect will process a purchase at the outgoing rate until 11:59 p.m. ET on the second-to-last business day of the month. At the stroke of midnight, their computer system moves the issue date to the 1st of the month and your I (or EE) bond will be issued with the newly announced rates.

The 1.10 and 3.98 are back up now.

David have you ever considered the possibility that TD doesn’t figure out the new rates anymore they just come and read your site. : )

I would be super pleased if this were true, but … nah. I do know that some Treasury officials read the site, however, at least occasionally, the ones most interested in maintaining the savings bond program.

It’s been posted on the Treasury Direct website again….treasurydirect.gov

I told my wife earlier today: “They will post this as soon as I head out for my morning walk.” Hah! I was still home. I did expect the announcement to come around 10 a.m. if Treasury followed past practices.

“No news release has yet been posted; that should come tomorrow. Just a few minutes after the new rate was posted on TreasuryDirect, it was taken down…”

David, did you just keep refreshing until you saw the change?

The new rate was posted on the site for about 10 minutes at 8:30 a.m. Then it was taken down. I didn’t expect to see the new rate until about 10 a.m., honestly.

Where can I find this info?