And … see below for travel news.

By David Enna, Tipswatch.com

Ever since Liberation Day on April 2, I’ve been watching financial markets in awe. At first, there were scary moments as the stock and bond markets roiled and American financial dominance came into question. Then, we got a surge in optimism because … “hey, it’s not that bad, right?”

Did I make a single financial move in those 40 days? No. I would have done some rebalancing when stocks fell into a bear market, but that phase seemed to last a couple hours. It is remarkable how little has changed amid all this turmoil.

I did a quick check and the value of my investments actually increased about 0.6% in the 40 days since April 1. Surprising.

Real yields

In “normal times” of financial panic you can expect to see stock prices falling and demand rising for U.S. Treasurys, as investors seek safety. And that is exactly what happened in the immediate aftermath of the April 2 tariff shock. In this case, shorter-term real yields fell more sharply than longer-term rates.

But then, after a weekend to ponder these U.S. moves, foreign investors and leveraged hedge funds began selling out of Treasurys, creating a shocking move higher in yields. The real yield of a 5-year TIPS rose 57 basis points in 6 market days. The 10-year real yield rose 50 basis points in that same time. The 30-year, 40 basis points.

Some financial analysts were predicting an end to “American exceptionalism” with potentially dire consequences.

Since May 1, the Treasury market has settled down, with real yields still elevated a bit, especially for the longer-term issues. I expect to see volatility continue for the rest of 2025.

Additional perspective

I have been saying for many months that I think a big bank / hedge fund bailout will eventually follow the great deal of risk that markets have been taking in early 2025. MarketWatch reporter Joy Wiltermuth posted an interesting article Friday with the headline: “Here’s how an obscure bet on bonds almost crashed the $29 trillion Treasury market, Fed official says.” (The link is to a free version.)

A massive bond bet backfired in April — and a top Federal Reserve official now says it likely sparked the biggest spike in long-dated Treasury yields since 1987.

Roberto Perli, who manages the Fed’s roughly $6 trillion securities portfolio, said Friday that the abrupt unwinding of a popular trade known as the swap-spread trade likely exacerbated April’s liquidity crunch in Treasurys.

The turmoil began after President Donald Trump announced sweeping new tariffs on April 2. At first, investors rushed into U.S. government debt in a “classic flight-to-safety” trade. But just days later, yields on long-dated Treasurys reversed sharply; the 30-year yield rose nearly 50 basis points in a week, its biggest such jump since 1987.

“One factor that appears to have contributed to this unusual pattern is the unwinding of the so-called swap-spread trade,” said Perli, manager of the New York Fed’s System Open Market Account, in a speech on Friday.

Perli also pointed to reports of leveraged investors being caught off guard by sudden moves in the Treasury market.

Investors piled into the swap-spread trade in early 2025 in hopes of a windfall should Trump usher in promised deregulation, especially for the banking sector. That trade backfired in April …

Trump pointed to a “yippy” bond market when he abruptly paused his April 2 tariffs for 90 days for most U.S. trade partners, with the exception of China.

And there you go. These are risky times when regulation is near zero.

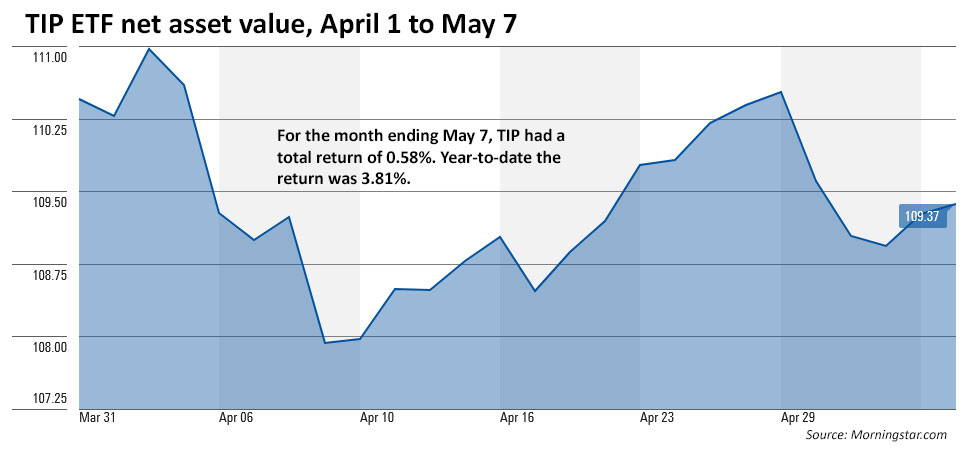

TIPS in general

The TIP ETF holds the full range of maturities of Treasury Inflation-Protected Securities. While it has had a volatile month, on May 7 it was showing a positive total return (including dividends) for both the last month and year to date.

One thing to consider: Shorter term TIPS are less volatile and less affected by interest-rate swings. The TIP ETF holds about 44 issues, and 27 of those mature in the next five years, where real yields have remained relatively low. That lessens the apparent volatility.

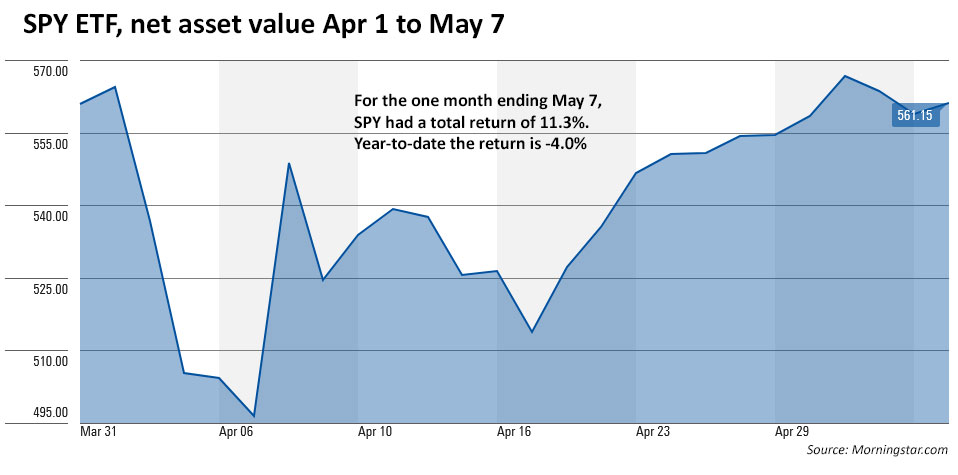

U.S. stock market

The immediate tariff reaction created fears of recession, plus the potential for global shunning of U.S. investments. The S&P 500, represented here by the SPY ETF, fell into bear market territory (down 20% from its previous high) on the morning of Monday, April 7. On April 9, President Trump announced a 90-day pause on “reciprocal tariffs” for most countries, except China. That helped calm the stock market, along with some positive earnings reports in recent weeks.

In this chart, note that the 11.7% total return from April 7 to May 7 is a bit misleading, because April 7 was the market low. In reality, very little has changed since April 1, up or down. The stock market remains down for the year to date.

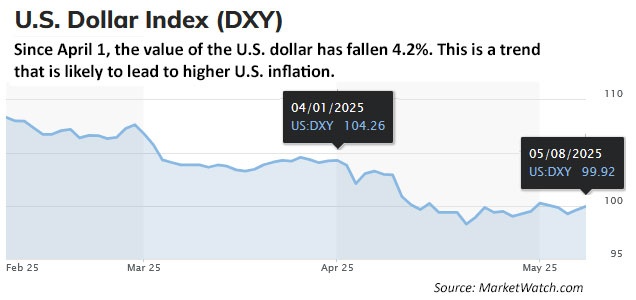

U.S. dollar

The trend toward a weaker U.S. dollar is bad news for U.S. consumers, who will already be facing higher prices triggered by 10% tariffs (at least) on global imports. But it could be good news for U.S. manufacturers, who might see improved demand for now-lower-cost exports (if they aren’t hit by new reciprocal tariffs).

A weaker U.S. dollar could lead to price increases for many imported products (food, clothing, raw materials, etc.) and could also be seen as a driving force behind the 13% increase in the price of gold over the last 60 days.

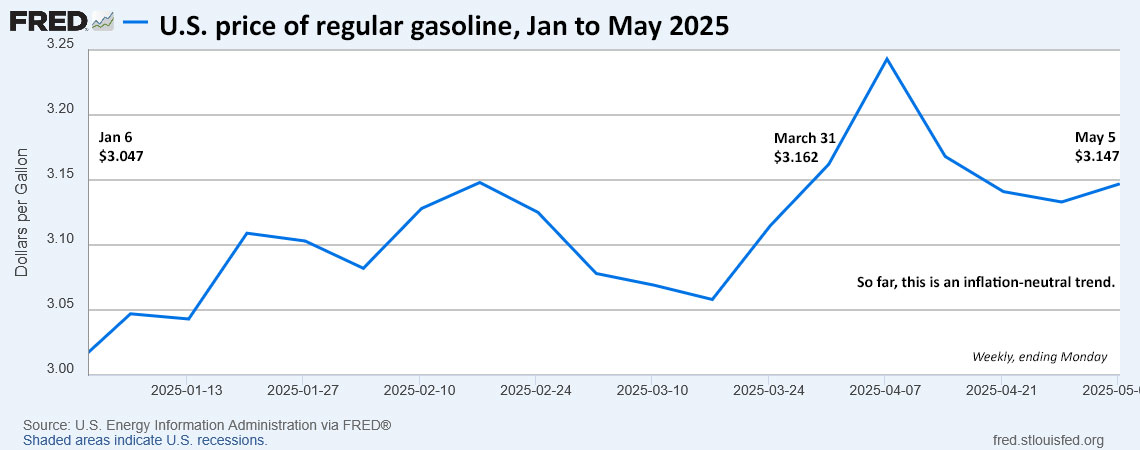

Gasoline prices

In an April 22 meeting with reporters, President Trump said, “We had a couple of states where gasoline was at $1.98 a gallon.” This was not correct. In fact, the lowest statewide price of gas on that day was $2.66 a gallon and the national average was $3.14.

It is true that the price of crude oil has been declining, fairly dramatically, in 2025. But so far, those price declines haven’t been reflected at the gas pump for U.S. consumers. This could be because of seasonal mix changes, or because the cheaper gas hasn’t been delivered yet, or just the fact that gas stations are always fairly slow to lower prices.

So far, Liberation Day has had nearly no effect on the price of gasoline. But if crude oil prices continue declining, I would expect to see lower prices in the near future.

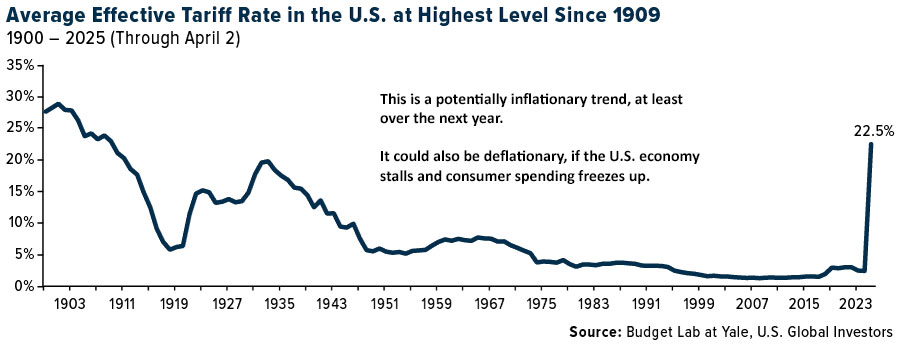

The effect of tariffs

So far, U.S. consumers have not seen a tremendous effect from the tariff rollout on April 2. A lot of retail firms front-loaded orders to avoid new tariffs, and Chinese goods have been virtually shut out from the U.S. by the current 145% tariff rate.

This chart, from Yale’s Budget Lab, is probably misleading because it is skewed by the 145% tariff on goods from China, which at this point U.S. consumers are not buying. But we do know a 10% tariff on all imported goods is currently in effect. The Budget Lab estimates the real tariff rate is about 18% if you factor in consumption shifts. That is the highest level since 1934.

The Budget Lab estimates the average cost of tariffs per household would be $2,600 per year. This is inflationary.

It also estimates current tariff levels could lower U.S. GDP by 1.1% and the unemployment rate could rise 60 basis points, costing 770,000 jobs. This is potentially deflationary.

These conflicting forces are reflected in this statement from Fed Chairman Jerome Powell on May 7:

The risks of higher unemployment and higher inflation appear to have risen. … Survey respondents, including consumers, businesses, and professional forecasters point to tariffs as the driving factor.

What we don’t know

Tariff policy is changing daily, sometimes more than once a day. So it is impossible for the markets to get a grasp on where the economy is heading. In addition, the U.S. is racing very quickly toward a thorny debt-limit crisis, plus tax and budget decisions that could greatly increase government borrowing.

So far, the financial effects of the Liberation Day aftermath have been surprisingly small. But in the future, keep on eye on the Treasury market, especially, to see if any cracks are forming. We went through a scary few days in early April. I hope we don’t revisit that fright.

In the meantime, inflation-protected investments like TIPS and I Bonds continue to look appealing, with real yields at or near 15-year highs.

What I do know

Today I am heading off for a week in Stockholm before joining the ‘Viking Homelands‘ cruise with … Viking, of course. I should have internet access “most of the time” and should be able to post the April inflation report on Tuesday morning, which is 2:30 p.m. in Stockholm. (The current forecast is for 0.2% all-items inflation for April.)

I will also attempt — on Sunday, May 18 — to preview the May 22 reopening auction of a 10-year TIPS. Then I hope to post the results after the auction’s close, when I can. At that point I have no idea where I will be.

Realize I may not be able to answer questions or follow financial news during this time.

* * *

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

“These are risky times when regulation is near zero.”

What regulations are near zero? I don’t think any relevant financial regulations have changed. Did I miss something?

Look at crypto currency, for example. It’s the Wild West again. And banks are dipping in. Tip of the iceberg.

Peggy Noonan makes my point today: https://www.wsj.com/opinion/broken-windows-at-the-white-house-republican-blind-eye-signs-of-disorder-0b79e925?st=bEuub5&reflink=article_copyURL_share

The thing about Chaos is that it is persistently omnipresent.

If some investors could make a treasury play that results in the president changing his policy and uttering words that make the market move by 9% in a few hours – that will certainly happen again.

Did Jerome Powell force Trump to the negotiating table with China by doing absolutely nothing?

The stock market liked the tariff reset with China and so did the dollar market. But this is truly a juggling act and the bond market signals that inflation will be getting worse – so was a ball just dropped?

In other words, It was a better play, again, to not act hysterically to short term financial events and stick to the plan? Who knew?

I think now is a good time to re-read When Genius Failed by Roger Lowenstein. This is about “genius” economists et al at Long Term Capital Management….who used techniques that were over-simplified models and enormous derivative bets on interest rates. Used copies < $10 might have tear stains or interesting notes 😀.

I bought a bit more Berkshire Hathaway on the dips this year as my only move to rebalance in the past 4 months plus some TIPS investments as bonds/bills matured.

I found it humorous that the BRK stock fell nearly 5.5% on the shocking news that a 94 year old CEO planned to retire in 9 months despite having made his transition plans rather well known… so much for perfect information being already priced into markets.

I was able to execute a Roth conversion on April 7. Still have more to do this year, but got to move more shares for the low price.

I like the idea of a Roth conversion on a big market dip. Good move, in my opinion.

Love that idea – told myself to do that too but didn’t get around to it in time. Nicely done.

There were many assets on sale at various times last month. What was described as volatility in the news meant there were some great bargains. EG several CA Munis (G.O. not specific to cities or other projects) had yields of over 4%. Also picked up ET stock position at a 9% yield (at the price bought, and assuming no dividend cuts).

I also like the idea of re-balancing a portfolio right after a big jolt in stock prices.

Thanks for the great post!

re: “Some financial analysts were predicting an end to “American exceptionalism” with potentially dire consequences.”It’s far too early in the ballgame to say they’re wrong. Foreign stock markets are UP for the year, and foreign investors are selling US Treasuries as well at an accelerated pace. Many savvy market participants (like Paul Tudor Jones) think that we have yet to see the bottom in the stock market.

The impact of Trump’s miscalculations and misunderstandings have not yet hit the real world, but the day of reckoning is fast approaching, with the next shock coming perhaps this weekend.

Trump still believes he’s got China over a barrel, while the Chinese have been preparing for this day for at least 5 years, at least since COVID. Despite all the tariffs in place on China since the beginning of April, Chinese exports were UP 8.1% in April over a year ago, due in large part to increased Chinese exports to Southeast Asia. While some of this no doubt will end up as Chinese goods being transshipped to the US, there are countries around the world who now see the US as an unreliable trading partner and are moving towards China. The dollar could lose its status as the world’s reserve currency, being replaced by a basket of foreign currency, which would have dire results for the US as far as borrowing costs go, for Treasuries and other debt.

We are only a few short weeks (and perhaps only days) from the first empty shelves we’ll see as Chinese goods become scarce. This will be the first time for many Americans that the reality of Trump’s miscalculations hit home.

There’s a possibility of a major shock this weekend. China was always better prepared to handle economic war, as they are less vulnerable to the domestic pain it will cause. But as I already stated, the Chinese are exporting as much as ever, just not to the US. They have repeatedly said they will not begin to negotiate unless Trump rolls back all tariffs, something his ego will never allow.

Trump’s announcement that “80% tariffs sound about right” is a signal to the Chinese that they do indeed have him in a corner, in an extremely weak bargaining position. I expect them to politely receive the American negotiators in a meeting the US virtually begged for (the Chinese were already scheduled to be in Switzerland, it’s not as though they agreed to come to Switzerland for negotiations).

And then I expect them to repeat that they’re unwilling to negotiate without a complete rollback of tariffs and end the meeting. That may be the signal to markets that the next leg down is about to start.

I think you nailed it. Trump claimed that other nations were… “kissing his ass…” begging him to make a trade deal. The Chinese play the long game and will be quite unwilling to cooperate with someone who scolds and disrespectfully abuses them like a 12 year old. I think they are going to set him up and watch him twist in the wind. Unfortunately, our retirement savings, the integrity of our financial system and the full faith and credit of the United States Government may be twisting in the wind as well.

Lol, this aged great

The CCP is our enemy. Not all of Trump’s actions are entirely economically motivated.

it doesn’t look like you are correct. Apparently the Chinese are negotiating in Switzerland, and they sent extremely senior officials to do so. Plus, the Financial Times reports that the purported rise in Chinese exports to SE Asia is mostly because those countries are facilitating trans-shipment to the U.S. In other words, there is no replacement market for the U.S. for production from Chinese factories.

“the day of reckoning is fast approaching” You must have been talking about UNH.